Autonomous Vehicle Insurance Washington: What Washington Drivers Need to Know

Autonomous vehicles are moving from science fiction to Washington roads faster than most drivers realize. The technology is here, the regulations are evolving, and insurance companies are scrambling to catch up.

At Secord Agency – A Trucordia Business, we’re breaking down what autonomous vehicle insurance in Washington actually means for you right now.

What Autonomous Vehicles Are Actually Operating in Washington Right Now

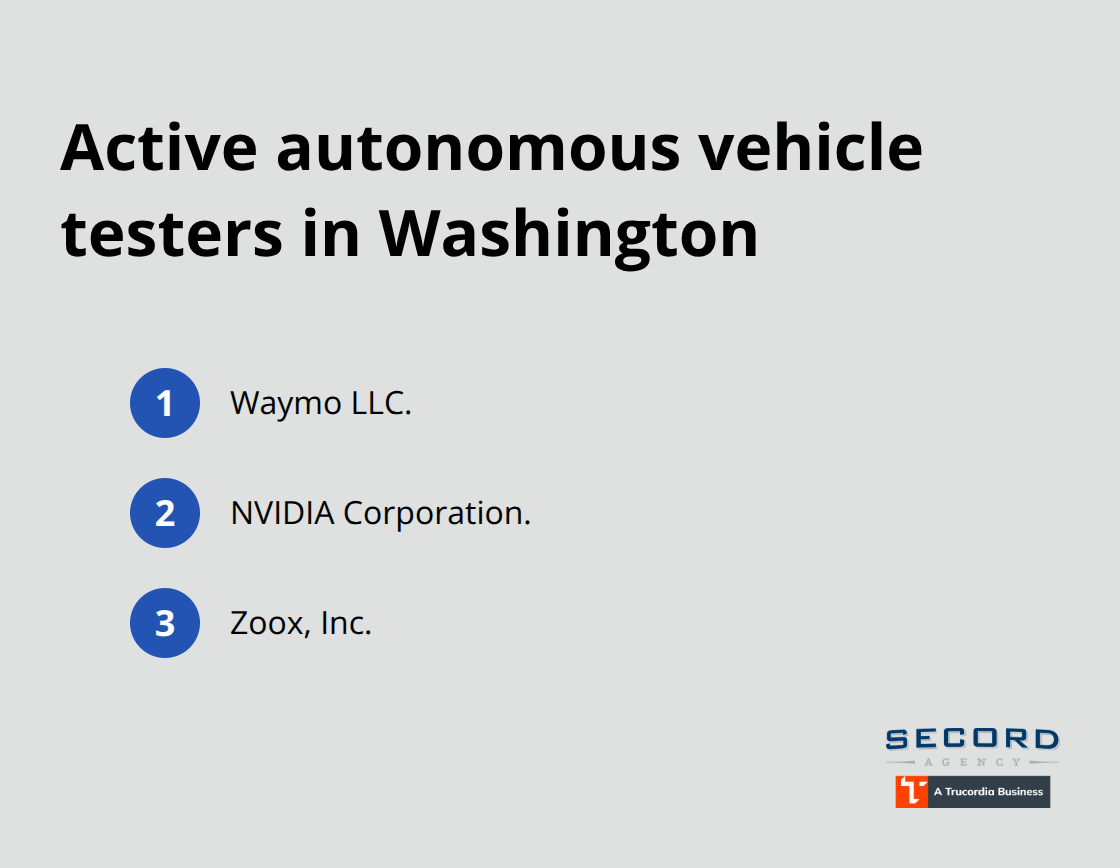

Three companies actively test autonomous vehicles on Washington roads today: Waymo LLC, NVIDIA Corporation, and Zoox, Inc. These aren’t theoretical projects or distant possibilities-they operate real vehicles on real streets under Washington’s self-certification pilot program, which took effect October 1, 2022.

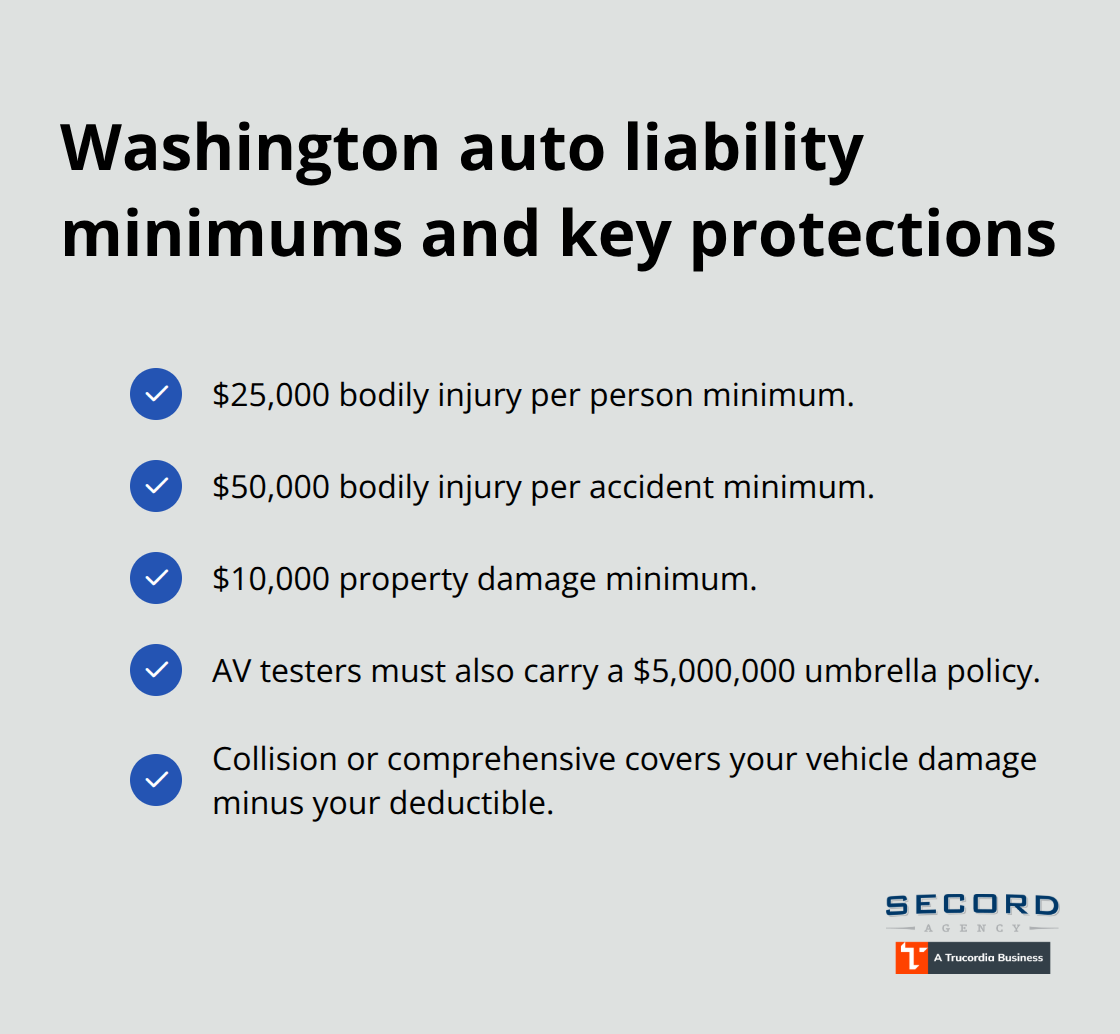

The vehicles meet SAE Level 4 or 5 automation standards, meaning they perform all driving tasks within their designed operating conditions without human intervention. This matters because Washington’s regulatory framework treats the automated driving system itself as the driver when it operates, fundamentally changing how liability and insurance work in a collision. Testers must carry umbrella liability insurance of at least $5,000,000 per occurrence, which signals how seriously the state views the risks these vehicles present. Every year by February 1st, these operators submit collision reports to Washington’s Department of Licensing, creating a public record of incidents that informs policy decisions.

How Companies Get Permission to Test

Before any company tests on public roads, they must self-certify with the state and provide proof of that $5 million umbrella liability policy. Operators must also give law enforcement 14 to 60 days advance written notice before testing periods begin. The notices must include specific vehicle details-make, model, color, license plate-so officers know what they’re looking at when an autonomous vehicle passes them on the road. Operators report moving violations and collisions to the Department of Licensing, and the state publishes this information publicly. This transparency requirement means you can actually track what happens with autonomous vehicles in your area rather than guessing.

What the Rules Require of Autonomous Vehicles

Washington’s framework requires vehicles to reach a safe condition if the automated system fails, and they must comply with all Washington motor vehicle laws relevant to their operational design. The regulations also mandate that operators communicate with law enforcement agencies in jurisdictions where testing occurs, enabling data sharing and coordination. These requirements create accountability and ensure that autonomous vehicles operate under strict safety parameters rather than in a regulatory vacuum.

What’s Coming Next in State Law

SB 5594, currently in the legislative process, would centralize all autonomous vehicle regulation under the Washington Department of Licensing and preempt local city prohibitions. This approach would standardize requirements statewide rather than allow jurisdictions to create patchwork rules. The bill treats the automated driving system as the driver or operator for traffic law compliance when engaged, shifting liability considerations in ways that affect how insurance coverage applies. Understanding these regulatory changes now helps you prepare for how autonomous vehicles will operate in Washington and what coverage you may need as this technology becomes more common on your roads.

Insurance Coverage and Liability in Autonomous Vehicle Accidents

Washington’s regulatory framework makes one thing crystal clear: when an automated driving system operates, that system becomes the legal driver. This creates a fundamental shift in liability compared to traditional accidents. In a collision involving a Level 4 or 5 autonomous vehicle where the ADS is engaged, fault determination hinges on whether the automated system performed its driving tasks within its operational design limits when the crash occurred. This distinction matters enormously for insurance claims because it potentially shifts liability away from the vehicle owner toward the company operating the autonomous system or the vehicle manufacturer. Testers currently operating on Washington roads carry umbrella liability policies of at least $5,000,000 per occurrence, which reflects the state’s assessment of potential damages from autonomous vehicle incidents. If you’re hit by an autonomous vehicle, your claim would likely be filed against that operator’s insurance policy rather than against a traditional driver’s personal auto policy.

What Your Current Coverage Protects

Your existing Washington auto insurance policy covers you if another vehicle strikes you, assuming the other party carries the required liability coverage. Washington requires every vehicle on the road to carry minimum liability limits of $25,000 per person for bodily injury, $50,000 per accident for multiple people, and $10,000 for property damage. Autonomous vehicle operators testing on public roads must meet these minimums plus carry that $5 million umbrella policy. If you drive a traditional vehicle and collide with an autonomous vehicle, your comprehensive or collision coverage pays for your vehicle’s damage regardless of fault, minus your deductible.

However, if the autonomous vehicle operator bears clear liability, your insurance company pursues a subrogation claim against their policy to recover those costs. The key point: your current policy protects you in autonomous vehicle accidents the same way it protects you in accidents with human drivers, provided you carry the coverage. If you only carry liability coverage and an autonomous vehicle causes a collision where you bear fault, your policy covers the other party’s damages but not your own vehicle repairs.

How Autonomous Vehicle Accidents Differ from Traditional Claims

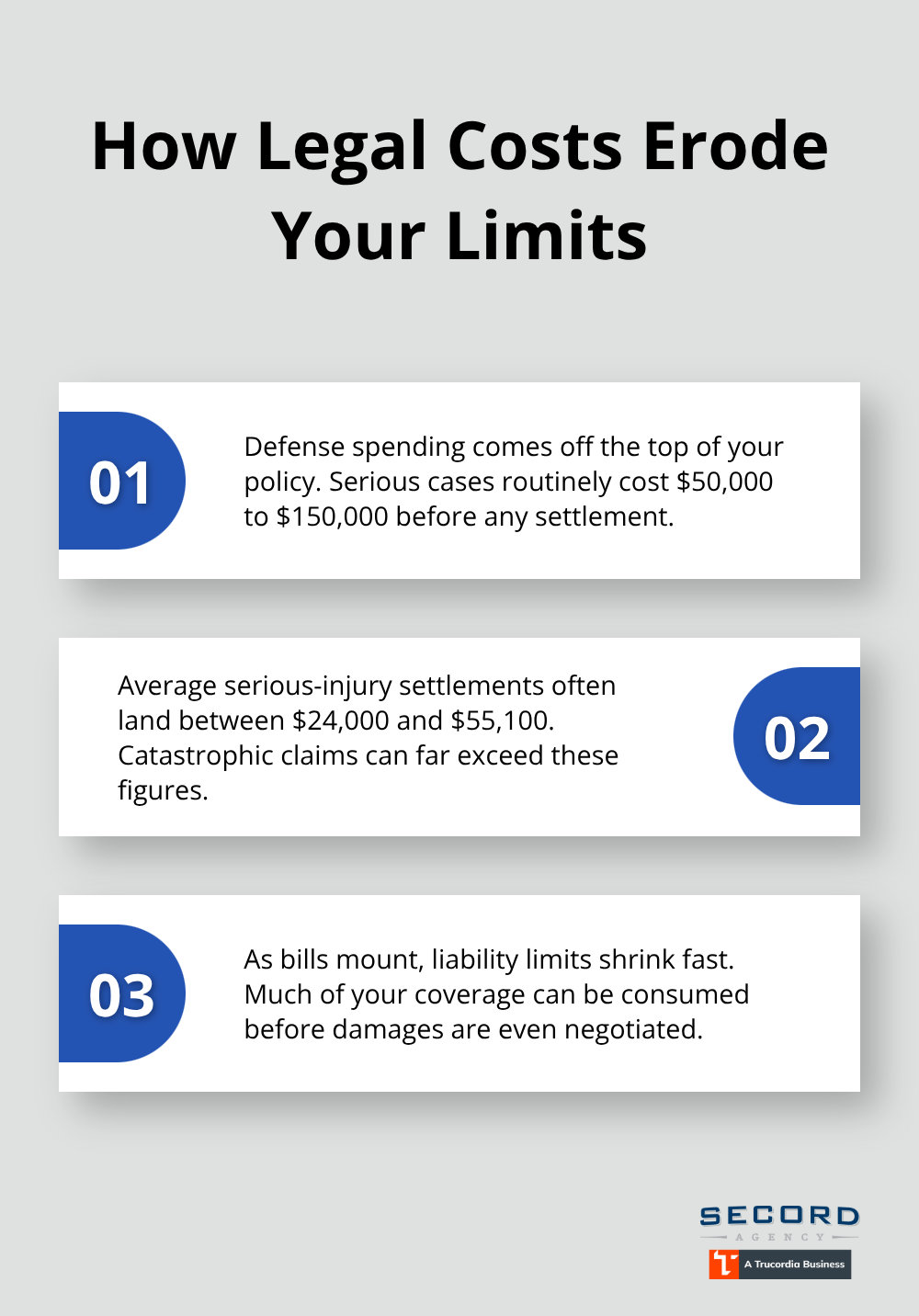

Autonomous vehicle accidents introduce complexity that traditional accident claims don’t present. When an ADS operates, investigators must determine whether the system performed within its operational design limits and whether any software or hardware failure contributed to the crash. This analysis requires technical expertise that goes beyond standard accident investigation. Insurance companies must examine system logs, software versions, and safety records to establish fault-a process that takes longer than traditional claims. The operator’s insurance must cover bodily injury, death, and property damage resulting from the autonomous vehicle’s operation, but determining what “operation” caused the accident requires deeper technical analysis than a fender-bender between two human drivers. Your insurance company may need to hire specialized experts to evaluate autonomous vehicle incidents, which could affect claim timelines and outcomes.

What Changes as Autonomous Vehicles Expand on Washington Roads

As autonomous vehicles become more common on Washington roads beyond the current three testing companies, insurance companies will adjust how they price coverage and what they cover. SB 5594 would standardize autonomous vehicle regulation statewide, which could lead to standardized insurance requirements across Washington rather than jurisdiction-by-jurisdiction variation. Insurance companies are still developing underwriting models for autonomous vehicle risk because accident data remains limited. The annual collision reports that operators submit to the Department of Licensing by February 1st each year create a growing public record that insurers will use to assess risk. Currently, that data is sparse because only three companies operate autonomous vehicles on Washington roads. As more operators enter the market and testing expands, insurers will have better information to price premiums accurately. You should expect that comprehensive coverage will become more valuable as autonomous vehicles increase, since collision claims involving autonomous vehicles may differ from traditional accident claims in terms of fault determination and repair complexity.

Preparing Your Coverage Now

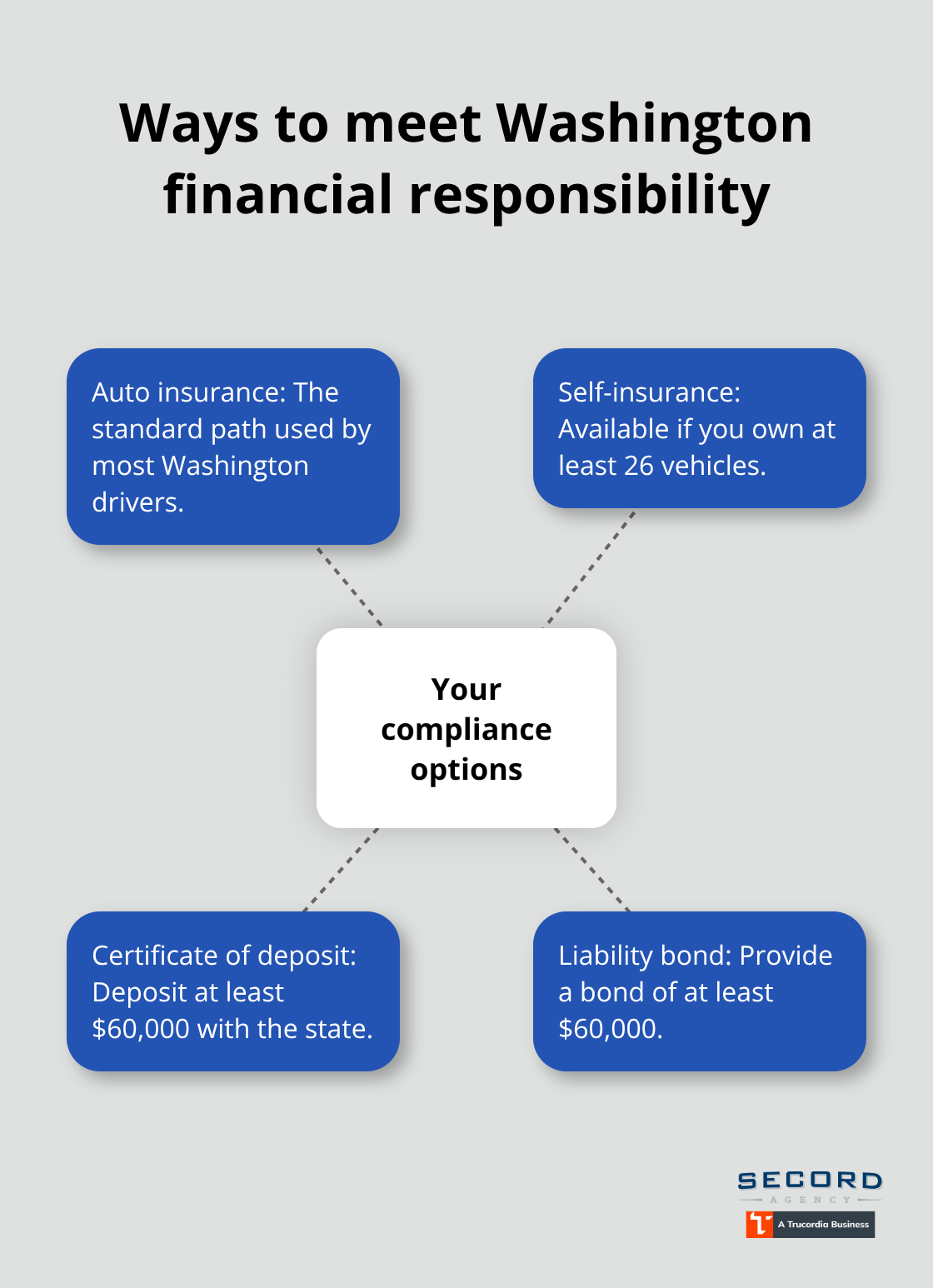

Contact an independent insurance agent who shops multiple carriers to review your current coverage limits now, before autonomous vehicle adoption accelerates. An agent can identify gaps in your protection and recommend adjustments that make sense for your situation. Washington offers flexibility in how you meet financial responsibility requirements-auto insurance, self-insurance (if you own at least 26 vehicles), a certificate of deposit of at least $60,000, or a liability bond of at least $60,000. Most individual drivers rely on auto insurance, but understanding all options helps you make informed decisions.

Your agent can also explain how your specific policy handles autonomous vehicle incidents and what additional coverage might protect you as this technology becomes more prevalent on Washington roads.

What You Should Do Right Now About Autonomous Vehicle Insurance

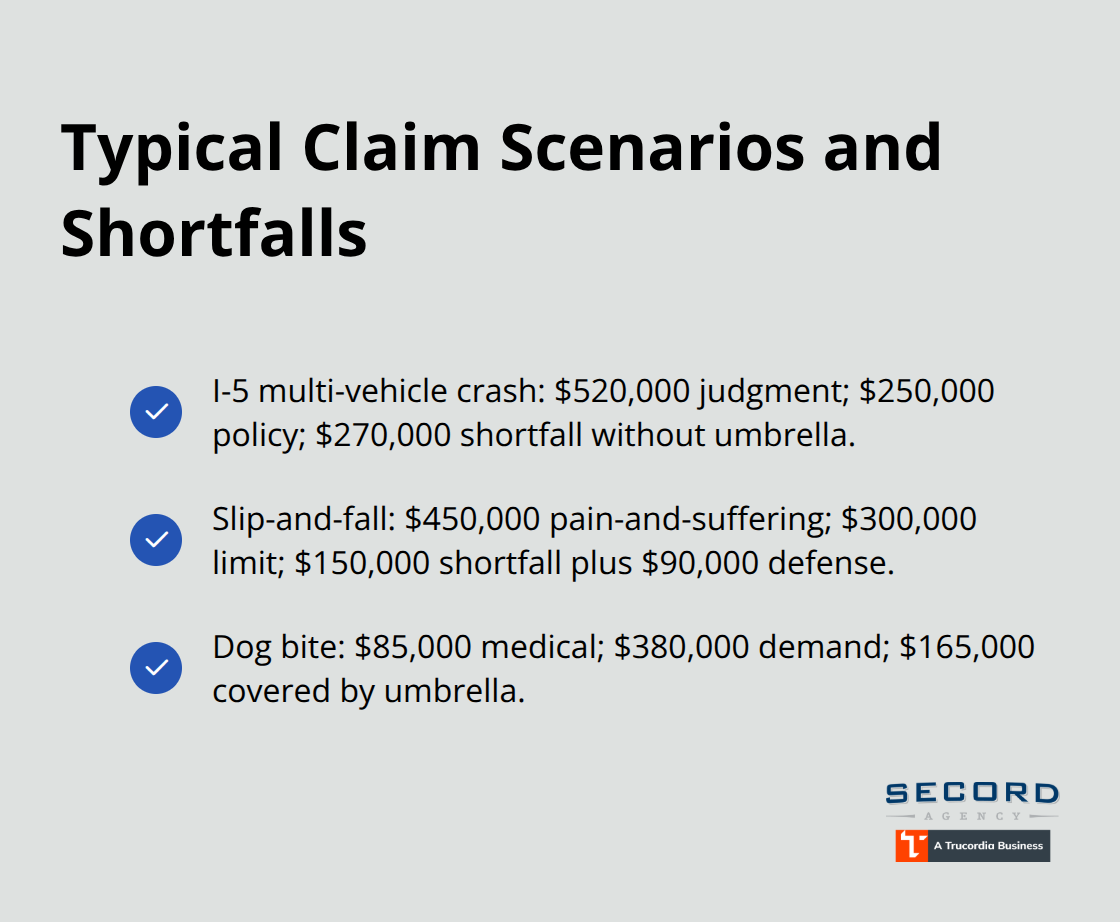

Schedule a policy review with an independent insurance agent who shops multiple carriers rather than selling policies for a single company. An agent examining your current coverage can identify whether your liability limits keep pace with autonomous vehicle risks on Washington roads. Washington’s minimum liability requirement of $25,000 per person and $50,000 per accident made sense when vehicles traveled slower and crashes caused less damage, but autonomous vehicle operators carry $5 million umbrella policies because the state recognizes that modern vehicle incidents can create catastrophic losses. Your $25,000 minimum coverage becomes inadequate fast if an autonomous vehicle causes a serious multi-vehicle collision. Request that your agent explain how your collision and comprehensive coverage apply if an autonomous vehicle hits you, and ask specifically whether your deductibles and limits align with the potential damages autonomous vehicle accidents could create.

Increase your liability limits now

Most Washington drivers carrying only the state minimum liability limits should increase to at least $100,000 per person and $300,000 per accident, which costs significantly less than the jump in protection provides. If you own assets worth protecting or drive regularly in congested areas where autonomous vehicles currently test, increase to $250,000 per person and $500,000 per accident. Comprehensive coverage becomes increasingly valuable as autonomous vehicles expand on Washington roads, since autonomous vehicle accidents may involve complex fault determination that takes longer to resolve than traditional claims. Your agent can run quotes showing how much additional premium each coverage increase costs, allowing you to make decisions based on actual numbers rather than guesses.

Understand autonomous vehicle accident complexity

The three companies currently testing autonomous vehicles on Washington roads file annual collision reports with the Department of Licensing every February 1st, creating a growing public record of incidents that insurers will use to adjust pricing and coverage terms as data accumulates. Autonomous vehicle accidents introduce complexity that traditional accident claims do not present. When an automated driving system operates, investigators must determine whether the system performed within its operational design limits and whether any software or hardware failure contributed to the crash. This analysis requires technical expertise that goes beyond standard accident investigation, and insurance companies must examine system logs, software versions, and safety records to establish fault.

Contact the right resources

Contact the Washington Department of Licensing at autonomousvehicles@dol.wa.gov to request the latest self-certification data on autonomous vehicle operators in your area, which tells you which companies test near your home or workplace. The department publishes annual reports summarizing autonomous vehicle testing activity, providing transparency into how these vehicles operate in Washington. Review your current policy documents to understand your deductibles, coverage limits, and any exclusions that might apply to autonomous vehicle incidents, since many policies written before 2022 may contain language that does not address autonomous vehicle scenarios. Ask your insurance agent whether your policy covers rental vehicles or rideshare services, since autonomous vehicle fleets will eventually enter those markets and you may need explicit coverage if you use those services.

Prepare documentation for future claims

Document your vehicle’s current condition with photos and maintenance records, establishing a baseline that helps with damage claims if an autonomous vehicle causes a collision before your next policy renewal. An independent agent can also track how SB 5594 progresses through the legislature, since standardized state regulation could shift insurance requirements in ways that affect your coverage needs. Secord Agency, a Trucordia business based in Seattle’s Wallingford neighborhood, shops multiple carriers to deliver tailored coverage that matches individual situations rather than pushing cookie-cutter policies.

Final Thoughts

Washington’s autonomous vehicle insurance landscape shifts faster than most drivers expect. Three companies already operate Level 4 and 5 autonomous vehicles on your roads under strict state oversight, and they carry $5 million umbrella liability policies that reflect serious risks. The regulatory framework treats the automated driving system as the driver when it operates, fundamentally changing how liability works in collisions.

Your current auto insurance protects you in autonomous vehicle accidents the same way it protects you from human drivers, but your liability limits may not keep pace with the potential damages these vehicles can cause. Increasing your coverage now costs far less than facing inadequate protection when an autonomous vehicle causes a serious collision. Annual collision reports filed by operators create a growing public record that insurers will use to adjust pricing and coverage as autonomous vehicle incidents become more common.

We at Secord Agency help you navigate this transition by reviewing your current coverage and identifying gaps before autonomous vehicle adoption accelerates on Washington roads. As an independent agency, we shop multiple carriers to find tailored autonomous vehicle insurance in Washington that matches your actual situation rather than pushing generic policies. Contact us to schedule a policy review and prepare your coverage for Washington’s autonomous vehicle future.