Private client group insurance: Tailored Solutions For High-Value Clients

Standard group insurance plans weren’t built for high-net-worth clients. They cap coverage at levels that leave affluent individuals exposed to significant financial risk.

At Secord Agency – A Trucordia Business, we’ve seen firsthand how private client group insurance solves this problem. This guide walks you through specialized protection designed specifically for executives and wealthy business owners.

What Sets Private Client Coverage Apart

The Fundamental Difference in Approach

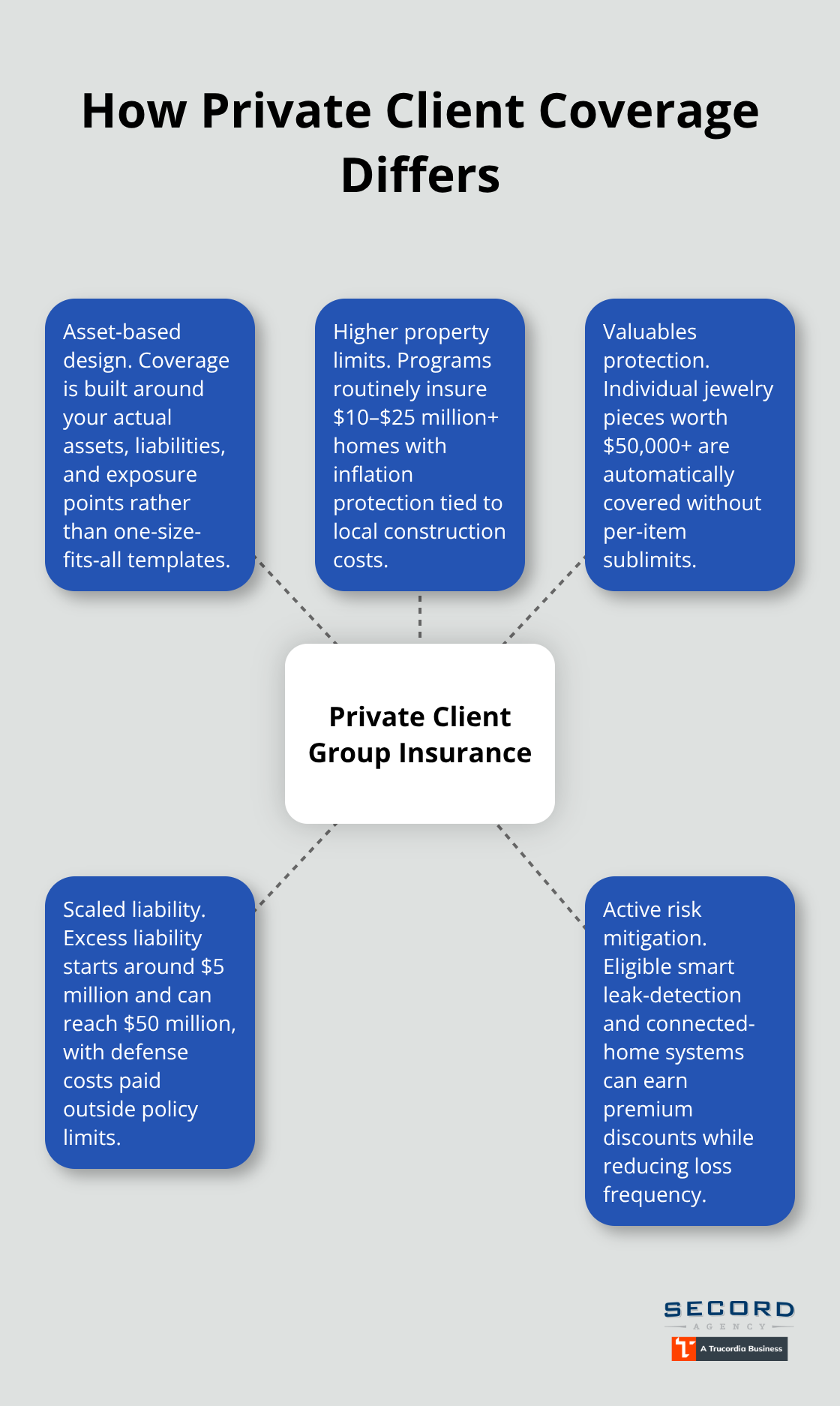

Standard group insurance treats everyone the same way. A $2 million home receives the same coverage structure as a $500,000 home. A $50,000 watch falls under generic jewelry limits. An executive with significant liability exposure gets a standard umbrella that stops well short of protecting their actual net worth.

This one-size-fits-all approach exists because mass-market policies are built for volume, not precision. Private client group insurance abandons this model entirely. It starts with your actual assets, your real liabilities, and your specific exposure points, then constructs coverage that matches those realities rather than forcing you into predetermined boxes.

Coverage Limits That Actually Protect Your Wealth

The gap between standard and private client protection widens dramatically once you examine the numbers. Standard homeowners policies typically cap dwelling coverage around $1 million, while private client programs routinely cover homes worth $10 million, $25 million, or higher with automatic inflation protection tied to local construction costs. Jewelry coverage illustrates the difference sharply: standard policies require riders for items above $2,500, while private client programs automatically cover individual pieces valued at $50,000 or more without per-item sublimits. Liability protection shows the same disparity. A typical group umbrella might offer $1 million or $2 million in coverage, which leaves a high-net-worth individual dangerously exposed. Private client excess liability starts around $5 million and extends to $50 million for complex family offices, with defense costs paid outside policy limits.

Why This Matters After a Loss

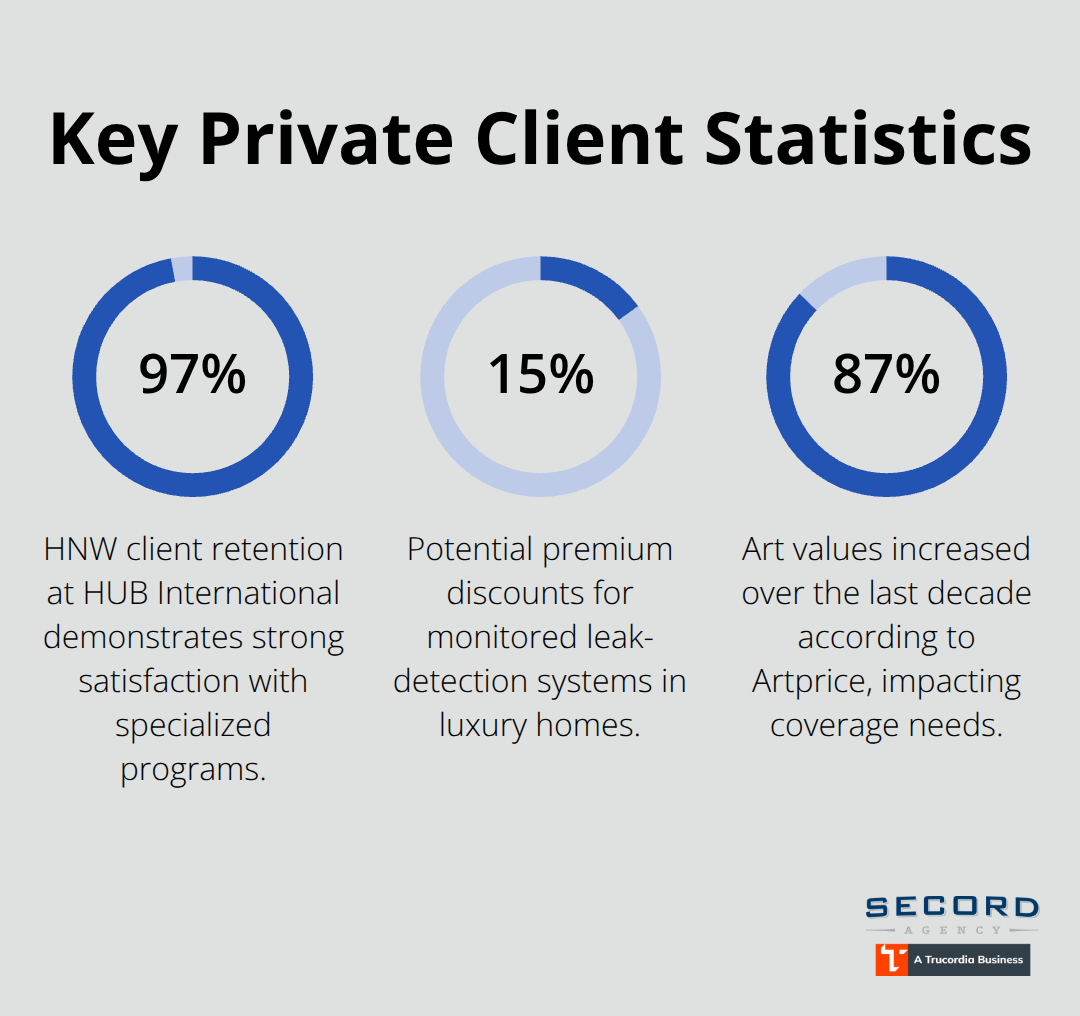

A single lawsuit involving significant injury or property damage can quickly exhaust inadequate limits, leaving personal assets vulnerable. HUB International, the largest privately held personal insurance brokerage in the U.S., serves 70,000 high-net-worth clients with a 97% retention rate, underscoring how specialized programs retain clients far better than standard offerings. The retention gap exists because private client coverage actually protects what clients own, whereas standard policies leave gaps that become painfully obvious after a loss occurs.

Active Risk Reduction Through Technology

Water damage detection systems in luxury homes illustrate how private client programs reduce risk actively. Many insurers offer discounts up to 15% for monitored leak-detection systems, and smart-home interconnection is increasingly standard for properties exceeding $3 million. These features give you real savings while protecting against one of the costliest exposures affluent homeowners face. The next step involves understanding which specific coverage options work best for your executive team and complex asset structure.

Coverage Options That Protect Executive Wealth

Enhanced Homeowners Protection for High-Value Properties

Executives and wealthy business owners face liability exposures that standard group plans ignore entirely. A lawsuit naming you personally, a guest injured on your property, or a professional liability claim can threaten assets that took decades to build. Private client group insurance addresses this by layering multiple coverage types that work together rather than in isolation. For executive leadership teams, the foundation starts with enhanced homeowners coverage that reflects actual property values, then adds specialized liability protection that scales with net worth.

Affluent homeowners need dwelling protection of 150% replacement costs, personal property coverage exceeding $100,000, and additional living expenses coverage. Private client programs handle this through agreed-value terms, meaning the insurer commits to paying the appraised amount without depreciation disputes. This matters enormously after a loss because you avoid the delays and fights that plague standard claims.

Specialized Coverage for Valuables and Collections

Jewelry coverage shifts from per-item sublimits of $2,500 to automatic coverage for individual pieces worth $50,000 or more. Art and collectibles receive the same treatment, with policies including automatic 10% annual coverage increases and triennial revaluations based on market data from sources like Artprice, which tracks that art values have risen 87% over the last decade. Worldwide transit coverage protects these assets during shipping or exhibition, and storage coverage extends to facilities like Geneva Freeport for executives with international operations.

Liability Protection That Scales With Your Net Worth

Liability protection for executive teams goes far beyond standard umbrellas. Private client excess liability policies start around $5 million and scale to $50 million for complex family offices, with defense costs paid outside the policy limits rather than eating into your coverage bucket. This distinction matters: a $5 million umbrella with outside defense costs provides substantially more actual protection than a $10 million umbrella with defense costs eroding the limit. Crisis management and reputation protection are embedded in policies, providing rapid access to specialists who cost $25,000 to $75,000 monthly when hired independently.

Integrated Risk Management Across Your Portfolio

Integrated risk management coordinates your personal and business portfolios to eliminate gaps that exist when coverage is purchased piecemeal. This coordination identifies exposures across multiple properties, vehicles, and business interests that siloed policies miss entirely. Executives with household staff need workers compensation and disability coverage for employees managing properties or providing care, a requirement that standard group plans never address.

Carrier Strength and Claims Capacity

The financial strength of carriers matters significantly here: AM Best recommends ratings of A+ or A++ for wealth protection to ensure capacity for large losses. PURE Insurance holds an A rating with over $2 billion paid in claims since 2007, while Chubb maintains AA- with $40 billion in net premiums written. These carriers have the surplus to handle major claims without delay or dispute. Selecting the right insurance partner requires understanding not just coverage options, but also the operational capabilities that determine how well your claims are handled when they matter most.

Getting Your Private Client Program Right

Selecting an Insurance Partner for Complex Portfolios

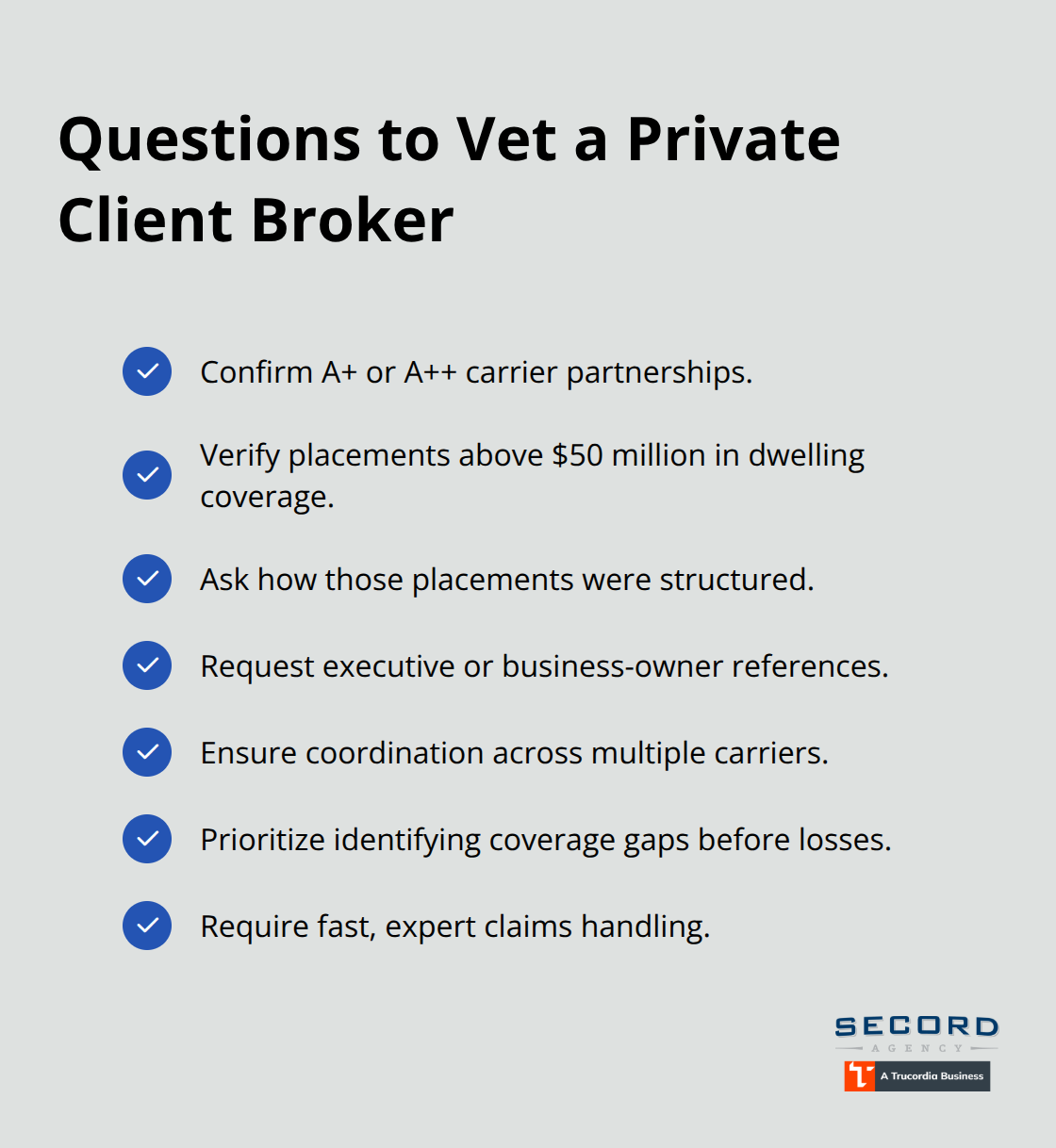

Selecting an insurance partner for private client group coverage demands more scrutiny than standard shopping. You need a broker who understands executive compensation structures, can coordinate across multiple carriers simultaneously, and maintains established relationships with underwriters who specialize in high-net-worth risk. FirstMark Insurance Group operates across 39 states with access to 20+ carriers, serving over 11,000 clients with 28,000+ policies-the scale and carrier diversity that complex portfolios require. The critical factor isn’t finding the cheapest quote. It’s finding a partner who can layer coverage correctly, identify gaps before losses occur, and handle claims with the speed that high-net-worth individuals expect.

When evaluating potential partners, examine their carrier relationships directly. Ask which A+ or A++ rated carriers they work with and why. Ask whether they’ve placed policies exceeding $50 million in dwelling coverage and how they structured those placements. Request references from other executives or business owners in your industry.

A broker worth their commission will have concrete examples of how they’ve solved complex coverage problems for clients similar to yours.

Administration and Claims Processing Excellence

Administration and claims processing separate adequate brokers from exceptional ones. Private client group policies involve multiple coverage types across different carriers, and poor coordination creates delays that compound after a loss. Demand a client portal offering direct access to billing and policy details rather than waiting for email responses. When a claim arises, your broker should connect you immediately with dedicated adjusters experienced in high-value losses, not generic claims handlers.

Some carriers like Chubb maintain specialized adjustment teams for art and collectibles, while others like PURE Insurance leverage their $2 billion claims-paid history to establish streamlined processes. These operational differences matter far more than premium quotes when a significant loss occurs.

Ongoing Policy Reviews and Coverage Adjustments

Ongoing policy reviews happen periodically to ensure coverage aligns with your broader financial picture and long-term goals. Art values tracked by Artprice rose 87% over the last decade, meaning a $5 million art collection four years ago might require $7 million in coverage today. Property values shift with renovation, market conditions, and acquisition of additional residences. Liability exposures change with business growth, board positions, or public visibility.

Your broker should proactively flag these changes rather than waiting for you to notice gaps. Active management coordinates across your personal and business interests to ensure coverage evolves with your wealth and protects what actually matters.

Final Thoughts

Private client group insurance delivers protection that standard policies cannot match, and the specialized features we’ve outlined address real exposures that executives and wealthy business owners face daily. Standard group plans leave gaps that become catastrophic after a loss occurs, while tailored coverage anticipates those gaps and closes them before anything happens. Finding the right broker matters more than finding the cheapest quote, because your partner must understand your specific situation and shop multiple carriers to deliver actual protection.

We at Secord Agency – A Trucordia Business understand how to structure private client group insurance correctly for your situation and complex portfolio. Our team evaluates carrier relationships, examines claims-handling capabilities, and coordinates coverage across your personal and business interests to prevent the common scenario where executives discover gaps years after purchasing a policy. Whether you’re evaluating your current program or building one from scratch, contact us today to discuss how specialized protection works for your executive team.