Short-Term Rental Insurance: Safeguard Your Vacation Property

Short-term rental insurance protects your vacation property from risks that standard homeowners policies simply don’t cover. Guest injuries, property damage, and lost rental income can devastate your finances without the right protection in place.

At Secord Agency – A Trucordia Business, we’ve seen too many property owners learn this lesson the hard way. This guide walks you through the coverage options available and how to pick the right policy for your situation.

Why Standard Homeowners Insurance Fails Vacation Rental Owners

Your homeowners policy has a fundamental problem: it explicitly excludes business activities. When you rent your property short-term on Airbnb or VRBO, you cross from personal use into commercial operation, and your standard coverage stops protecting you. Standard homeowners policies deny claims related to short-term rental activity, leaving you exposed to guest injuries, property damage, and lost income. Insurers consider short-term rental a business, and your personal policy was never designed to handle that risk.

Guest-Caused Damage Creates Your Biggest Exposure

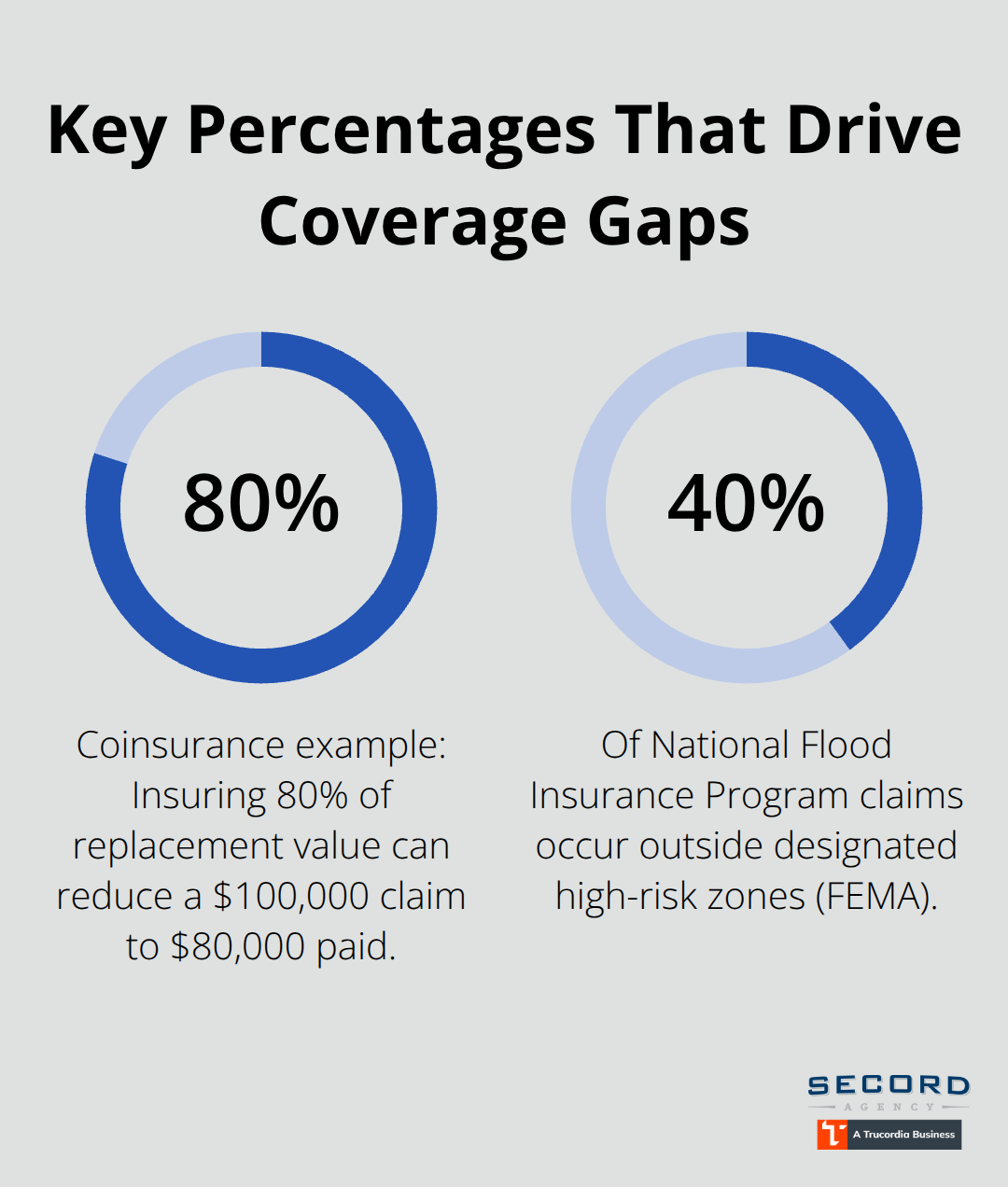

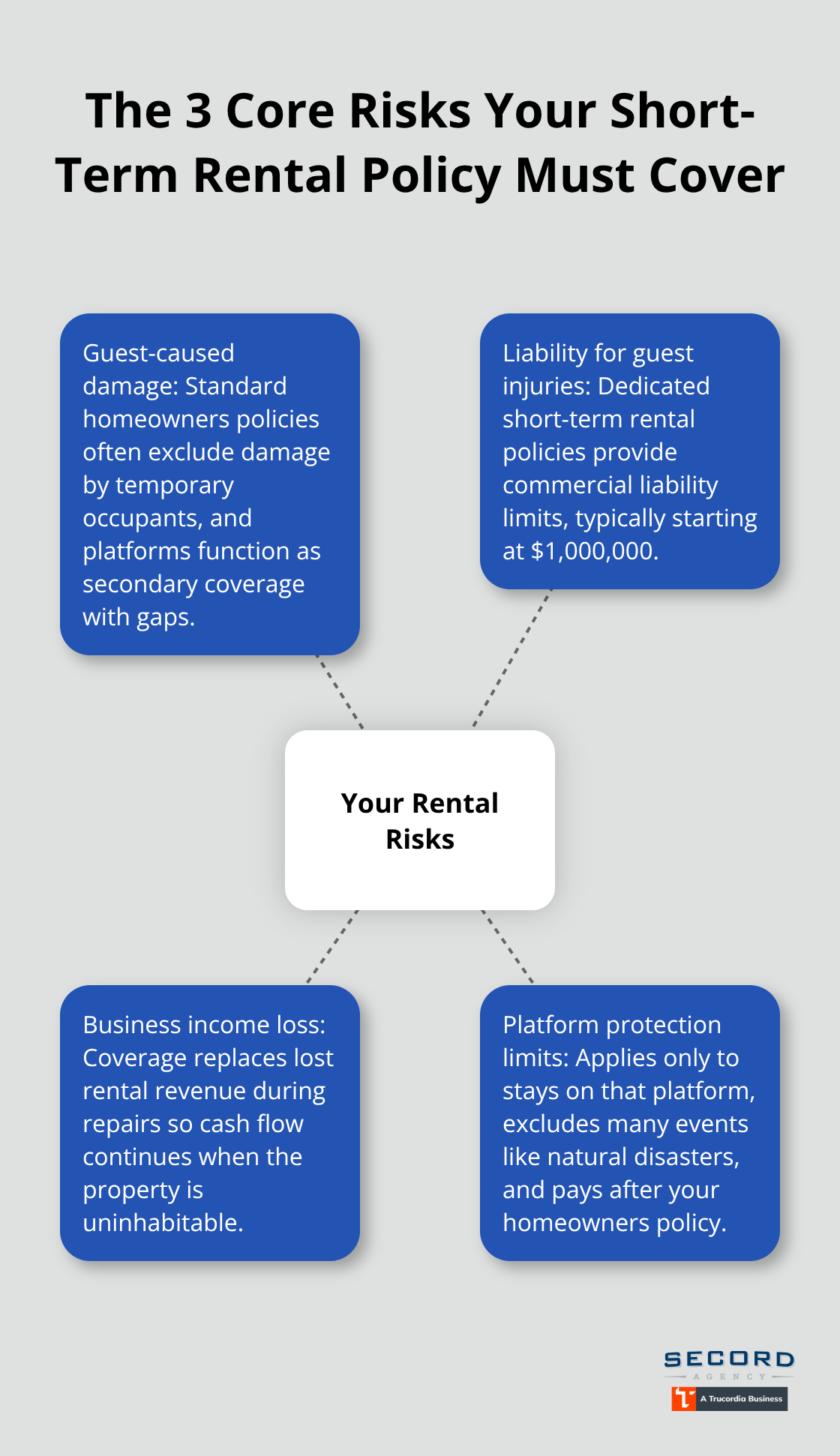

A guest slips on your stairs and breaks their arm. A renter damages your walls and furniture during a weekend stay. Someone steals your electronics. Your standard homeowners policy will likely reject these claims because they occurred during a rental period. You’ll cover the costs yourself, which can easily run into thousands of dollars.

Standard policies exclude damage caused by temporary occupants, and they certainly don’t cover vandalism or theft by people who aren’t permanent residents. If a guest damages your property, you have limited recourse. VRBO and Airbnb offer some protection-AirCover on Airbnb provides up to three million dollars in property damage coverage, and VRBO has similar protections-but these platform guarantees don’t cover everything. More importantly, they function as secondary coverage, meaning your homeowners policy pays first, and only gaps receive coverage afterward. That structure creates confusion and delays when you file a claim.

Liability Exposure Can Reach Six Figures

Liability exposure is equally serious. If a guest is injured at your property, your homeowners policy typically won’t cover the medical bills or legal defense costs. A slip-and-fall injury can result in significant liability exposure depending on the severity. Dedicated short-term rental insurance covers guest injuries with commercial liability limits, usually starting at one million dollars, which matches what most jurisdictions require for vacation rental permits.

Lost Income During Property Damage Leaves You Unprotected

Loss of income during property damage represents another critical gap. If a fire or break-in makes your property uninhabitable, your income stops immediately. Standard homeowners policies don’t reimburse lost rental revenue. Short-term rental insurance includes business income coverage that replaces your lost earnings while the property undergoes repairs, meaning you don’t face a financial crisis during recovery.

These gaps explain why platform protections and standard homeowners policies fall short for vacation rental operators. The right dedicated policy addresses all three exposure areas at once, which is why understanding your actual coverage options matters before you face a claim.

Your Insurance Options Beyond Platform Protection

Why Platform Protection Falls Short

Platform protections like AirCover and VRBO Host Protection sound comprehensive until you read the fine print. Airbnb’s AirCover covers up to three million dollars in property damage and three million in lost income, but it only applies to Airbnb stays, excludes natural disasters entirely, and functions as secondary coverage behind your homeowners policy. VRBO offers similar limits with comparable gaps. These programs exist to reduce platform liability, not to fully protect your business.

If you list on multiple platforms or face a natural disaster, platform coverage leaves dangerous exposure uncovered.

The real problem runs deeper: these protections don’t name you as the insured party. You depend on the platform to file claims on your behalf, which creates delays and uncertainty when you need answers fast. Platform protection works as a bonus layer, not your primary safety net.

Dedicated Policies Eliminate Coverage Gaps

Dedicated short-term rental insurance fills every gap that platforms and homeowners policies create. Policies from carriers like Proper Insurance offer one million dollars in commercial general liability, with the option to increase to two million dollars, plus all-risk building coverage with no sublimits on guest-caused damage, theft, or vandalism. You receive business income coverage without time limits, meaning lost rental revenue during repairs gets fully reimbursed.

Proper’s policies also include liquor liability and pet liability, covering damage from guest activities like pool use or bicycle accidents. Over 100,000 vacation rental owners have chosen Proper Insurance, indicating strong market adoption and claims experience. The average annual premium runs between 1,500 and 2,000 dollars according to MarketWatch data, though costs vary significantly by location, property type, and occupancy frequency.

Specialized Coverage for Your Specific Situation

For high-value properties or those in wildfire or flood-prone areas, specialized endorsements add layers of security. Theft protection, bed bug treatment, lock replacement, and squatter protection (covering legal costs and income loss) address risks that standard policies ignore. Foremost Insurance offers longer-stay policies covering rentals up to twelve months, useful if you host digital nomads or seasonal guests. American Family provides short-term rental add-ons to homeowners policies for properties rented up to sixty-two days yearly, including guest theft and identity theft protection in nineteen states.

Selecting the right carrier depends on your specific exposure. Frequent turnover demands stronger guest-damage coverage, while longer stays benefit from Foremost’s extended-term structure. Shopping quotes from multiple carriers reveals significant price differences-bundling short-term rental coverage with existing homeowners or landlord policies often yields discounts and simplifies renewals across your portfolio.

Finding the Right Fit for Your Property

Your property type, occupancy frequency, and risk tolerance shape which policy works best. A high-turnover urban apartment faces different exposures than a seasonal mountain cabin. Location matters too-properties in flood or wildfire zones need additional endorsements that standard policies won’t provide. Multiple carriers compete for your business, and their pricing structures vary widely based on these factors.

Getting quotes from three to five carriers takes less time than you’d expect and reveals which options fit your budget and coverage needs. The comparison process also highlights which carriers offer the digital tools and claims support that matter most to you when you actually need to file a claim.

How to Choose the Right Short-Term Rental Insurance

Match Your Policy to Your Rental Reality

Your property’s characteristics dictate which coverage structure actually works. A high-turnover urban studio rented 200 nights per year through Airbnb faces completely different exposures than a seasonal mountain cabin rented 30 nights annually. The first needs aggressive guest-damage coverage with no sublimits because frequent turnovers mean constant exposure to new guests. The second requires strong liability protection but might skip business income coverage since extended vacancy periods already factor into seasonal operation.

Carriers price policies differently based on occupancy frequency, and this matters enormously-a property rented 50 days yearly costs substantially less than identical coverage for 200 days. Foremost Insurance’s policies reflect this reality by offering lower premiums for longer-stay rentals up to twelve months, recognizing that digital nomads and seasonal guests create different risk profiles than rapid-turnover vacation homes.

Location amplifies these calculations. A beachfront property in a flood zone needs specialized water damage endorsements that a landlocked urban condo doesn’t require. Wildfire-prone California properties benefit from specific fire coverage enhancements. Your state and local jurisdiction also matters-American Family operates short-term rental add-ons in only nineteen states, so availability varies.

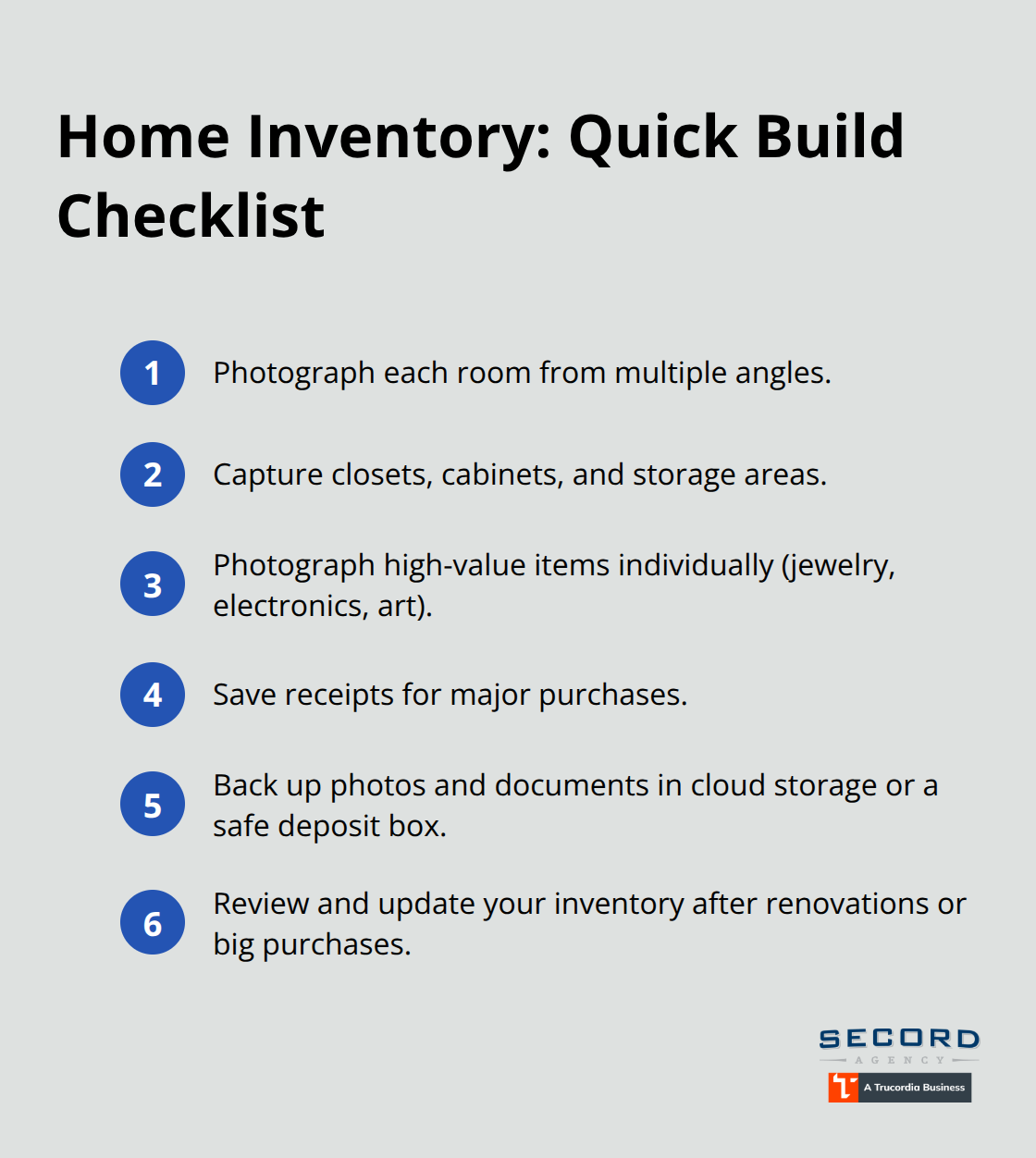

Before comparing quotes, document your actual operating pattern: how many nights per year, average guest tenure, occupancy rates across seasons, and whether you list across multiple platforms. This data transforms abstract policy comparisons into concrete decisions about which carrier’s structure matches your business.

Assess Coverage Limits Honestly, Not Optimistically

One million dollars in commercial general liability coverage represents the floor for most jurisdictions, not a ceiling. Many cities legally require this minimum for short-term rental permits, but your actual exposure might exceed it significantly. A serious guest injury with permanent disability can generate liability claims exceeding two million dollars. Proper Insurance offers the option to increase from one million to two million dollars, and that upgrade costs less than you’d expect relative to the protection it adds.

Your property value determines building coverage limits-insuring a five-hundred-thousand-dollar property for three hundred thousand dollars creates obvious gaps. Contents coverage should reflect what guests actually interact with: furniture, kitchen equipment, electronics, bedding, and décor. Policies with no sublimits on guest-caused damage matter here because one destructive guest can easily damage ten thousand dollars worth of contents.

Deductibles create direct cost tradeoffs that require honest evaluation. A five-hundred-dollar deductible costs more in premiums but means you absorb less per claim. A two-thousand-dollar deductible reduces premiums but forces you to cover more out-of-pocket when damage occurs. Calculate how many claims you’d realistically file annually-high-turnover properties experience more frequent minor damage claims, making lower deductibles financially sensible despite higher premiums. Low-occupancy properties might accept higher deductibles because claims happen infrequently.

Spending an afternoon with quotes from three to five carriers reveals exactly how these variables affect your costs, and the comparison process itself clarifies which coverage limits make sense for your specific situation rather than what marketing copy suggests.

Compare Premium Costs Across Multiple Carriers

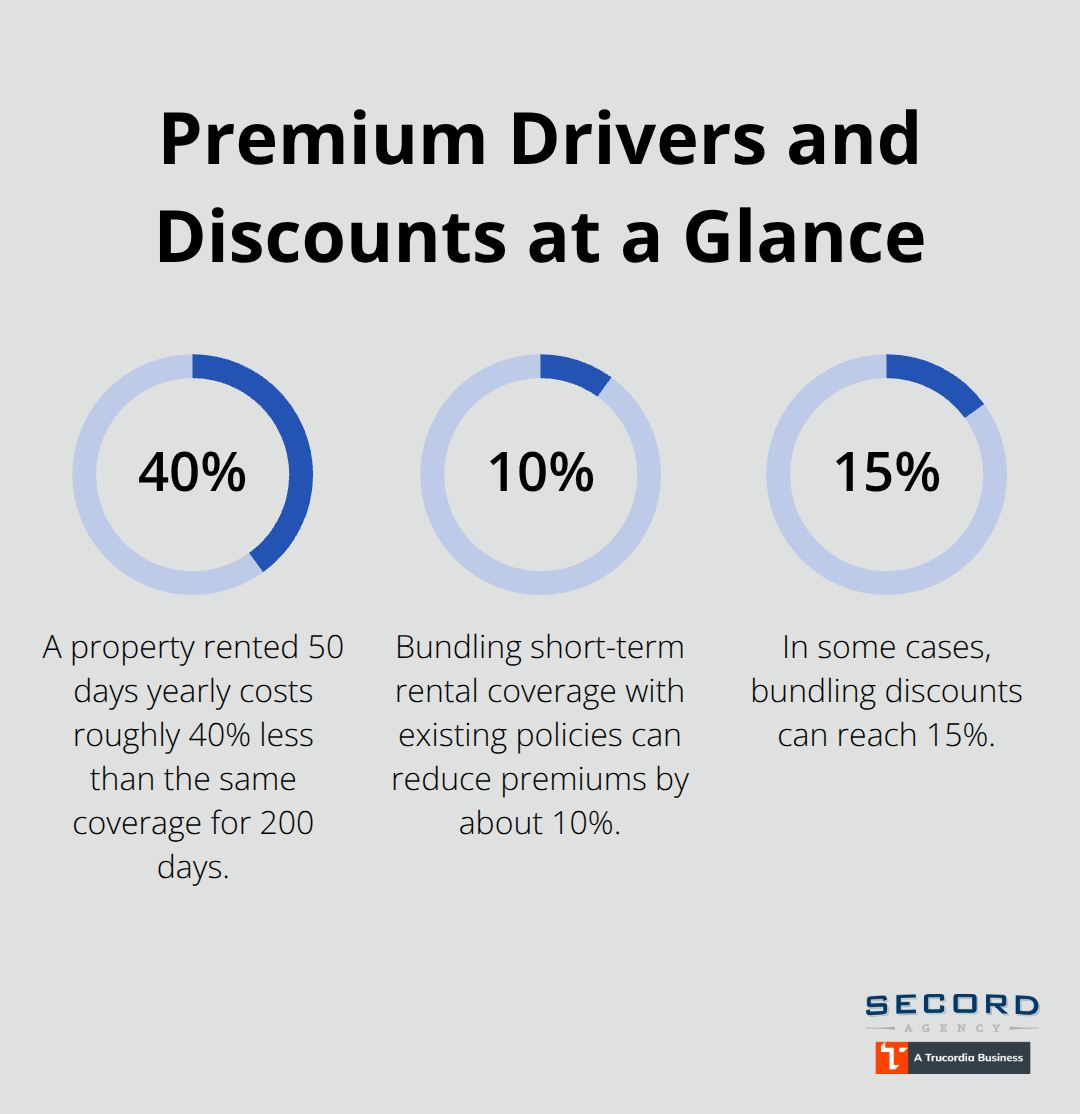

MarketWatch data shows average annual premiums between fifteen hundred and two thousand dollars, but this range obscures massive variation. A property in Seattle might cost twelve hundred dollars annually while an identical property in a California wildfire zone costs three thousand dollars. Occupancy frequency drives equally dramatic differences-a property rented fifty days yearly costs roughly forty percent less than the same coverage for two hundred days.

Bundling short-term rental coverage with existing homeowners or landlord policies often yields ten to fifteen percent discounts while simplifying renewals. Multiple carriers compete aggressively on price, meaning the first quote you receive almost certainly isn’t the best rate available. Getting quotes from Proper Insurance, American Family, Foremost, and regional carriers takes less than two hours combined and frequently reveals five-hundred to one-thousand-dollar annual differences for identical coverage.

Some carriers offer claim-free discounts after five years, and others provide reductions for monitored security systems or fire alarms. These credits accumulate and deserve evaluation alongside base premiums. The cheapest option isn’t always correct-a carrier with faster claims processing and better customer service might justify slightly higher premiums when you actually experience a guest-caused damage event.

Investopedia’s evaluation ranked carriers across complaint data from the National Association of Insurance Commissioners, revealing that some cheaper providers had significantly higher complaint rates. Balancing premium cost against financial strength ratings and complaint history prevents choosing a carrier that disappears or denies legitimate claims when you need them most. Shopping annually takes minimal effort and often reveals rate reductions or new carriers entering your market, ensuring you don’t overpay for coverage year after year.

Final Thoughts

Short-term rental insurance protects your vacation property from financial devastation, but only if you purchase the right policy and maintain it properly. The gap between platform protections and dedicated coverage is real and expensive-standard homeowners policies won’t cover your guests, and platform guarantees function as secondary layers with significant exclusions. You need a dedicated policy with your name on it, and getting quotes takes minimal effort to reveal exactly how much protection costs for your specific situation.

Contact three to five carriers, provide your property details and occupancy frequency, and compare what each offers. Review your coverage annually since property renovations, changes in occupancy patterns, or additions to your portfolio require policy adjustments. A property you rented 50 days last year might rent 150 days this year, and your short-term rental insurance should reflect that increased exposure.

We at Secord Agency – A Trucordia Business understand that navigating insurance options feels overwhelming, so our team shops multiple carriers to find coverage that matches your rental operation and your budget. Contact us for a quote and let us simplify the process, whether you need protection for a single property or comprehensive coverage across multiple listings.