Homeowners Policy Advice Washington: Practical Tips for Better Coverage

Most Washington homeowners don’t realize their policies have significant gaps until disaster strikes. We at Secord Agency – A Trucordia Business have seen too many families face unexpected costs because they didn’t understand their coverage.

This guide gives you homeowners policy advice for Washington that actually works. You’ll learn what you’re missing, how to fix it, and exactly when to take action.

What Your Washington Homeowners Policy Actually Covers

Standard homeowners policies in Washington cover your dwelling structure, attached structures like garages, personal property inside your home, liability if someone gets injured on your property, and additional living expenses if you need temporary housing after a covered loss. Most Washington homeowners misunderstand what this actually means in practice, however. Your dwelling coverage pays to rebuild your home if it burns, but it typically excludes flood damage entirely-a significant gap since more than 40% of National Flood Insurance Program claims occur outside designated high-risk areas, according to FEMA data. Your personal property coverage reimburses you for belongings up to a percentage of your dwelling limit, usually 50-70%, but this applies actual cash value in many policies, meaning you receive depreciated amounts, not replacement costs. This matters enormously. If your roof is 15 years old and gets damaged, you might receive $3,000 instead of the $8,000 needed to replace it. Liability coverage typically maxes out at $100,000 to $300,000 per occurrence-insufficient if someone sues you after a serious injury on your property. Additional living expenses cover hotel and meal costs if your home becomes uninhabitable, but only up to a set percentage of your dwelling limit, often leaving homeowners short when displacement stretches beyond 30-60 days.

Coverage Limits That Don’t Match Reality

Washington homeowners typically pay $1,000–$1,499 annually for coverage, according to U.S. Census Bureau data, but this affordability often masks dangerously low limits. Many policies still use functional replacement cost instead of full replacement cost, meaning insurers pay what it costs to replace damaged items with less expensive substitutes rather than with materials matching your original home’s quality. This creates a painful surprise during claims. Your deductible-typically $500, $1,000, or $2,500-directly impacts what you pay out-of-pocket for each claim, and raising it to $2,500 or $5,000 can substantially lower your premium if cash flow is tight. However, you should choose a deductible only if you can actually afford it after a loss, since selecting one higher than your financial capacity defeats the purpose of insurance.

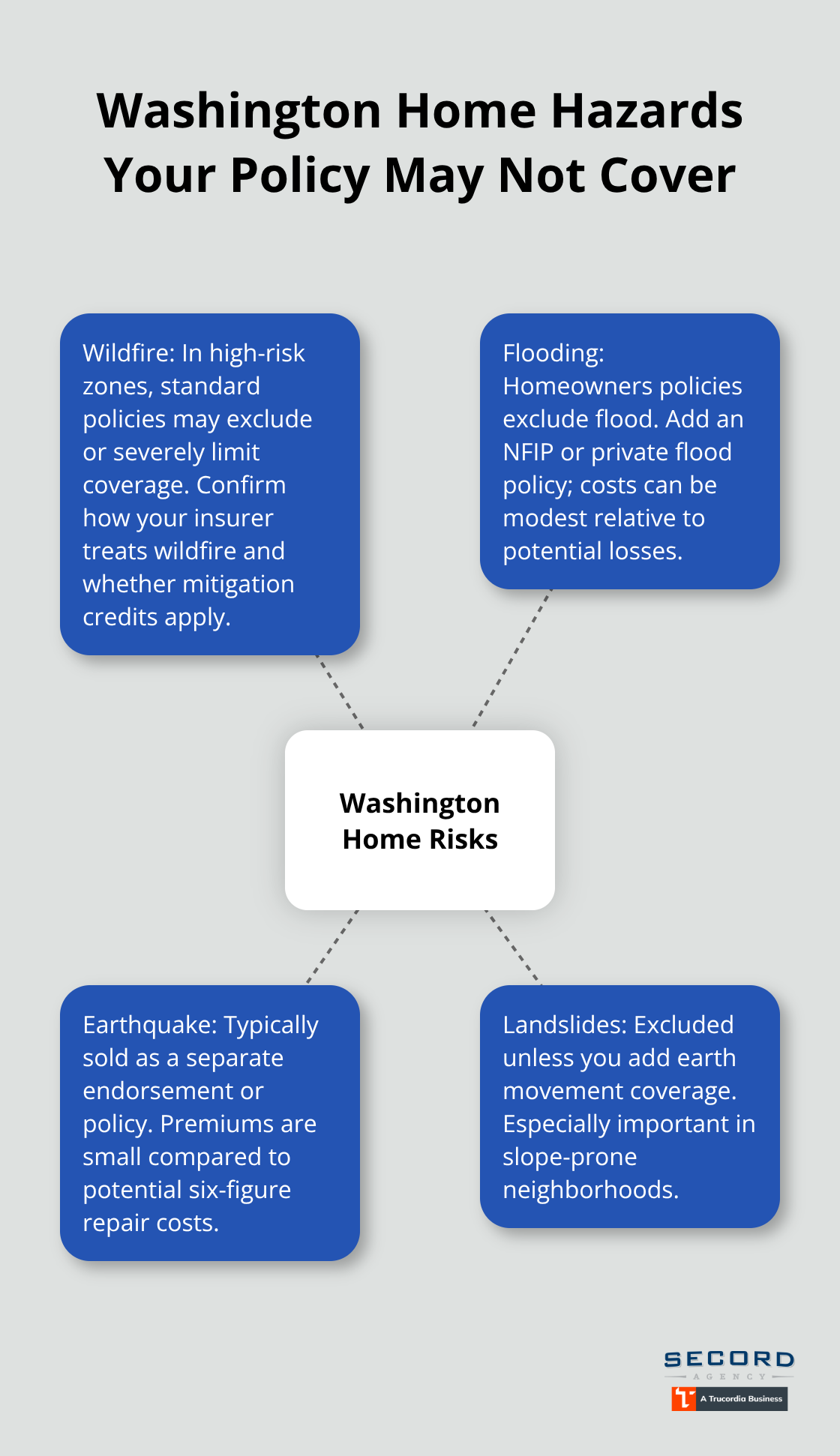

Washington-Specific Hazards Demand Specific Coverage

Wildfire risk grows across the state’s forested landscapes, yet standard policies often exclude or severely limit wildfire coverage in high-risk zones. Flooding from heavy rains and snowmelt presents seasonal coverage challenges, requiring separate flood insurance through the National Flood Insurance Program or private carriers-an annual flood policy for a $500,000 home costs around $100 and you can usually add it to your existing homeowners policy. Earthquake coverage, essential given Washington’s seismic activity, is sold separately and rarely included in standard policies. Landslides, common in parts of Washington, are excluded from standard policies unless you add specific earth movement coverage. Without these add-ons, a single weather event can wipe out your financial security while your policy sits useless. This is where the gaps between what you think you have and what you actually have become painfully clear-and where the next section shows you exactly what most homeowners miss.

What You’re Actually Missing in Your Coverage

Underinsurance: The Silent Financial Threat

Most Washington homeowners discover their gaps at the worst possible moment-after a loss. Underinsurance is the silent killer that leaves families thousands of dollars short. When the U.S. Census Bureau surveyed Washington homeowners, it found that many carry dwelling limits far below actual replacement costs, especially in areas where home values have climbed sharply over the past five years. A home worth $550,000 with a $400,000 dwelling limit sounds reasonable until you need to rebuild and discover current construction costs run $200 per square foot, not the $150 your policy assumed when it was written three years ago.

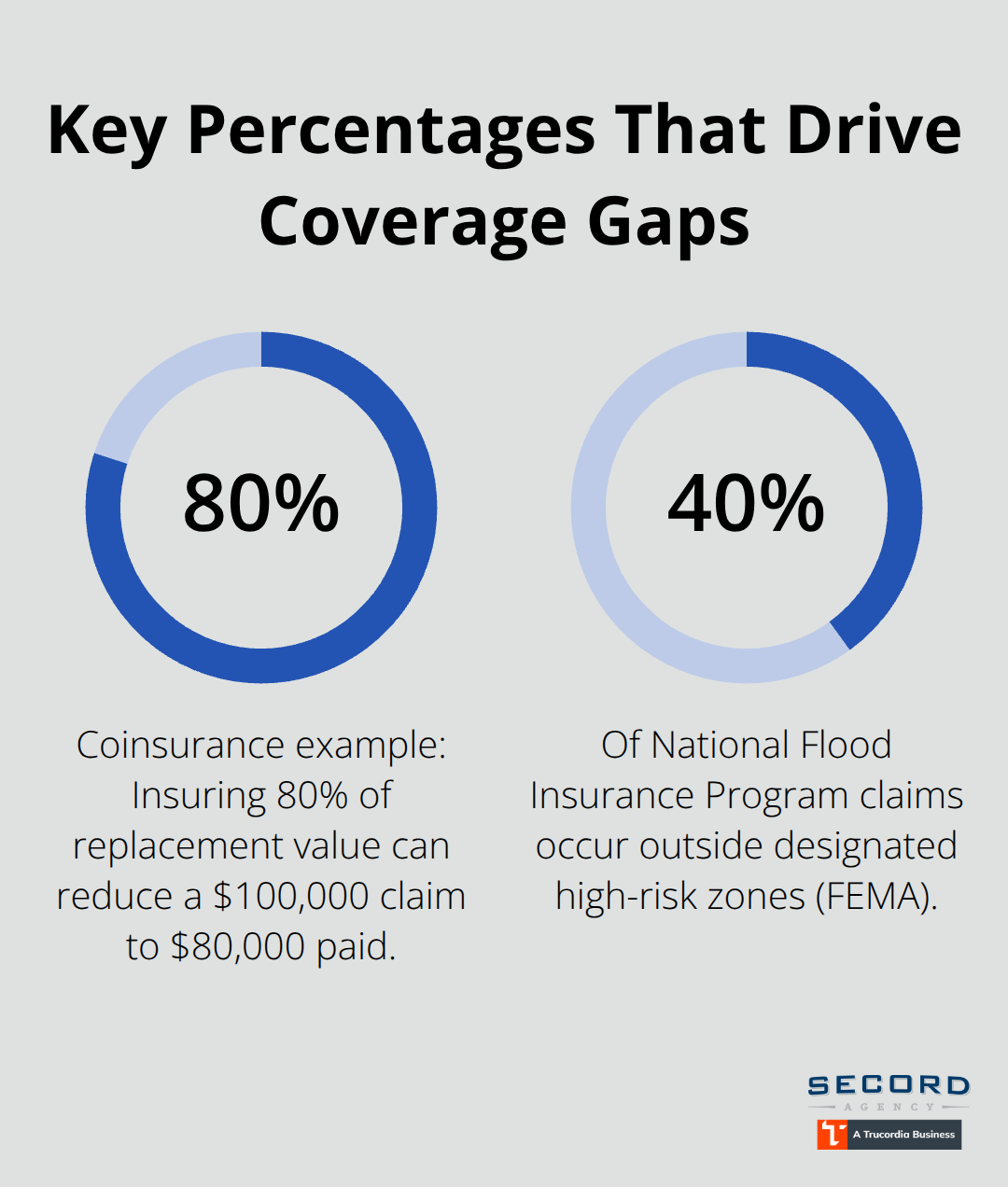

This coinsurance penalty hits hard. If your home is insured for only 80% of its replacement value and you suffer a $100,000 loss, the insurer may pay only $80,000, leaving you to cover the rest. Request a replacement cost estimate from your agent every two years, especially in hot real estate markets.

Ask specifically whether your dwelling limit reflects current building costs in your ZIP code, not outdated valuations.

Many Washington homeowners also fail to increase coverage when they add a deck, finish a basement, or upgrade their kitchen-improvements that add real value but go uninsured unless you formally notify your carrier. These updates can represent tens of thousands of dollars in unprotected assets.

Natural Disaster Gaps That Leave You Exposed

Natural disasters expose the most dangerous gaps. Wildfire, flood, and earthquake coverage gaps exist because insurers either exclude these perils entirely from standard policies or charge so much that homeowners skip them to save money. According to the National Flood Insurance Program, more than 40% of flood claims between 2014 and 2018 occurred outside high-risk zones, meaning your home could flood even if you don’t live in a designated flood area-yet without separate flood coverage you’d receive nothing.

A private flood policy for a $500,000 home costs roughly $100 annually, making it the cheapest insurance decision most Washington homeowners never make. Earthquake coverage typically runs $150–$300 per year depending on your home’s age and construction, a pittance compared to the $50,000–$200,000 in damage a moderate quake can cause. Wildfire exclusions in high-risk counties mean your dwelling and personal property get zero protection if fire spreads to your neighborhood, even if your home sits in an urban area.

Liability and Living Expense Shortfalls

The liability and additional living expense gaps matter just as much but receive less attention. Standard liability limits of $100,000–$300,000 offer minimal protection if someone suffers a serious injury on your property and sues-medical bills, lost wages, and pain-and-suffering awards regularly exceed $500,000 in Washington courts. Additional living expenses typically cap at 20–30% of your dwelling limit, which sounds adequate until your home stays uninhabitable for four months during winter reconstruction and you’ve exhausted your coverage by month two.

These gaps transform from theoretical concerns into real financial crises when disaster strikes. The next section shows you exactly how to close them with practical, affordable solutions that fit your budget and your home’s actual risk profile.

How to Close Your Coverage Gaps Without Overpaying

Build a Home Inventory That Actually Protects You

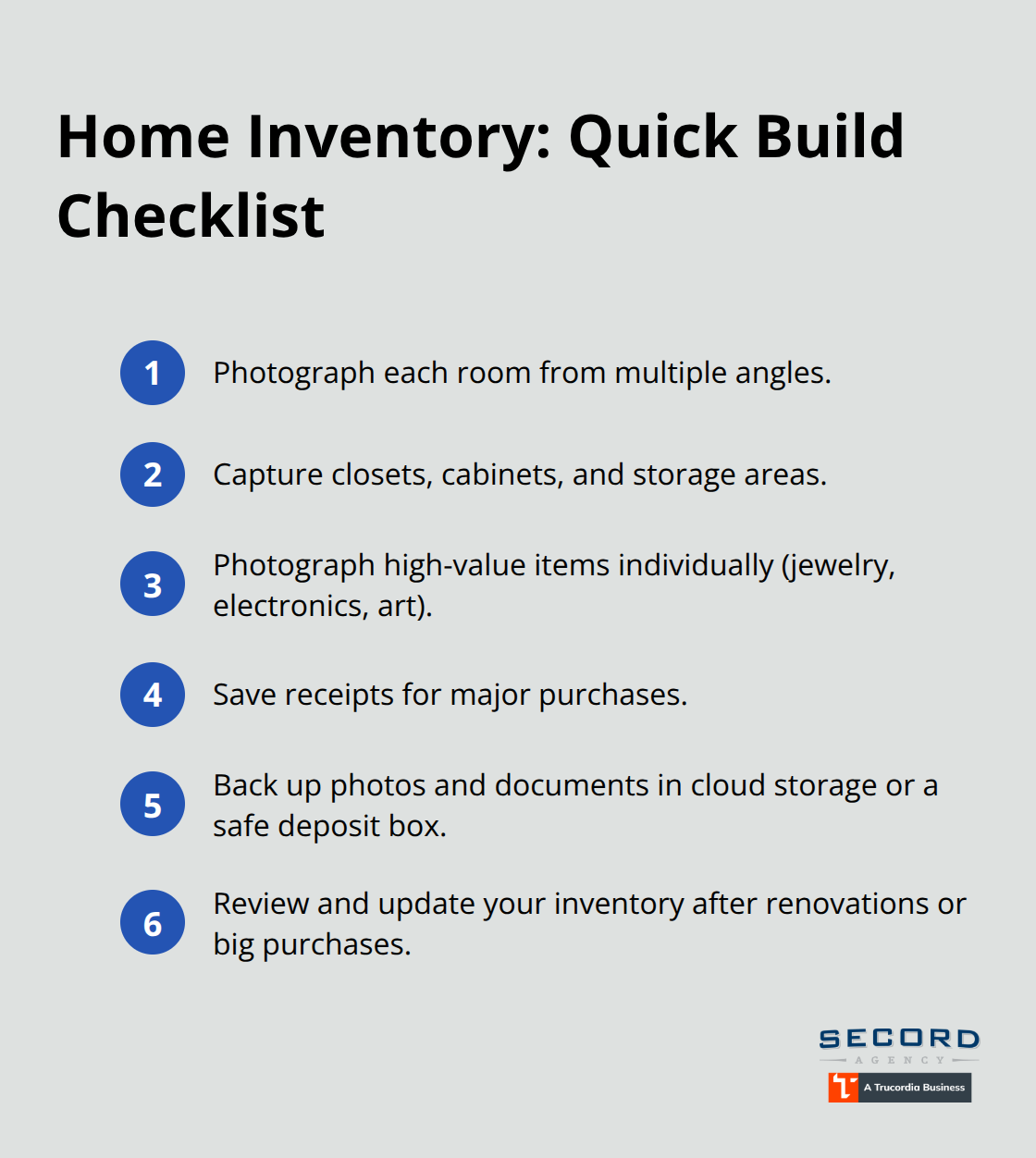

Most homeowners skip this step or create vague lists that fail during claims. Instead, take photos of every room in your home from multiple angles, including closets, cabinets, and storage areas.

Photograph high-value items individually-jewelry, electronics, collectibles, art-and keep receipts for major purchases. Store copies of these photos and receipts outside your home, either in cloud storage or a safety deposit box. This documentation cuts claim disputes dramatically.

When you complete your inventory, calculate the replacement cost of your belongings, not their current value. A five-year-old television might be worth $300 used, but replacing it new costs $800. Your personal property limit should cover the total replacement cost of everything you own, typically 50–70% of your dwelling limit. If your dwelling limit is $400,000, your personal property coverage should protect roughly $200,000–$280,000 worth of belongings. Many Washington homeowners discover their limits fall short here and adjust their coverage before a loss occurs.

Update Coverage to Match Current Home Values

Schedule an annual policy review with your agent in the same month every year-set it as a calendar reminder. During this review, confirm your dwelling limit reflects current replacement costs in your ZIP code, not valuations from three years ago. Construction costs in Washington have climbed steadily, and your coverage must keep pace.

Disclose any home improvements you’ve completed: a new roof, updated electrical system, finished basement, or deck addition all increase your home’s replacement cost and should trigger coverage increases. These updates represent tens of thousands of dollars in unprotected assets unless you formally notify your carrier.

Capture Available Discounts and Rate Reductions

Homes with updated roofing, electrical systems, and plumbing often receive 5–15% rate reductions. Installing smoke detectors, carbon monoxide alarms, and security systems generates additional discounts. If you’ve improved your home’s condition, these upgrades deserve recognition in your premium.

Ask your agent whether you qualify for discounts you’re currently missing. Inquire about credits for smart home devices that monitor water leaks or temperature changes. Some carriers offer reductions for completing a home safety course or installing weather-resistant upgrades.

Combine Policies and Shop Strategically

Bundle your homeowners policy with auto insurance through the same carrier-most insurers discount bundled policies by 10–25%, saving you hundreds annually. Ask specifically about loyalty discounts if you’ve been with your current carrier for three or more years.

Shop your policy every two to three years even if you’re satisfied with your current coverage, since rate competition shifts and new discounts emerge constantly. Independent agents who represent multiple carriers can show you options your current insurer might not offer, often saving you money while improving your actual protection. We at Secord Agency – A Trucordia Business work with multiple carriers to find coverage that fits both your budget and your home’s actual risk profile in Washington. If your standard homeowners policy leaves exposure in liability, personal umbrella insurance fills those gaps affordably.

Final Thoughts

Your homeowners policy requires active management, not passive acceptance. The gaps we’ve outlined-underinsurance, missing natural disaster coverage, inadequate liability limits-will not resolve themselves, and waiting until a loss occurs guarantees financial hardship. Washington homeowners who act now avoid the regret that follows claims denials or coverage shortfalls.

Start this month by pulling your declarations page and comparing your dwelling limit to what your home would actually cost to rebuild today. Check whether you have separate flood and earthquake coverage, confirm your liability limit matches your actual exposure, and notify your carrier immediately if you’ve made home improvements. These steps take minimal time and often save thousands when disaster strikes. Contact your insurance agent if you’re unsure about any coverage gap, and work with someone who asks questions about your home’s condition, your financial situation, and your risk tolerance before recommending coverage that actually protects you. We at Secord Agency – A Trucordia Business provide homeowners policy advice Washington homeowners can trust, pairing competitive rates with personalized service that keeps your coverage current as your home and circumstances change.