Seattle Homeowners Insurance Policy: A Comprehensive Overview

Seattle’s weather and geography create distinct insurance challenges that differ from most other regions. Windstorms, flooding, and earthquake risk mean your Seattle homeowners insurance policy needs careful consideration.

We at Secord Agency – A Trucordia Business help homeowners navigate these complexities. This guide covers the coverage types you need, how to find affordable rates, and why working with a local agent matters.

Why Seattle Homeowners Need Specialized Insurance Coverage

Wind and Hail: The Leading Cause of Claims

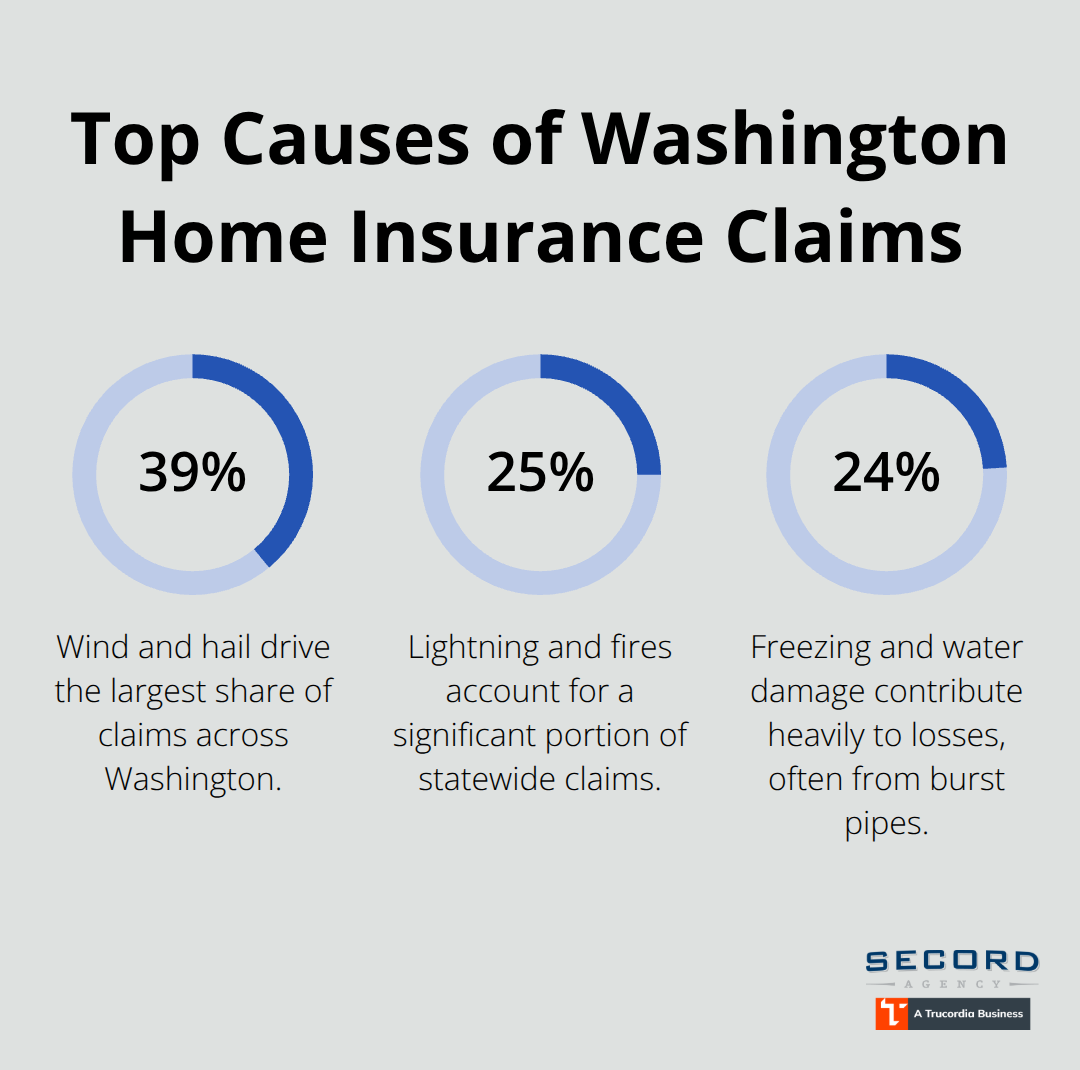

Pacific Northwest weather patterns create insurance demands that standard policies often fail to address. Wind and hail damage accounts for approximately 39.4% of Washington home insurance claims according to the Insurance Information Institute, making windstorms the leading cause of losses in the region. During strong storms, hail cracks roofing and siding while high winds tear off roof sections and scatter debris across properties.

These concentrated losses demand targeted coverage beyond what a basic policy provides.

Fire and Electrical Hazards

Lightning strikes and fires represent another 24.8% of claims in Washington. The National Fire Protection Association notes that 30% of home fires stem from faulty electrical wiring or malfunctions, while 44% start from unattended cooking. These statistics reveal that electrical safety and fire prevention matter significantly for Seattle homeowners. Installing and maintaining smoke detectors, along with regular electrical inspections, reduces your risk profile and may lower your premiums with some carriers.

Freezing and Water Damage Risks

Freezing and water damage rounds out the top three at roughly 23.5% of claims, primarily from burst pipes when temperatures drop below freezing. Frozen water expands inside pipes and causes ruptures when it thaws, leading to expensive water intrusion and potential mold growth. Insulating exterior pipes, installing frost-free hose bibs, and using heat tape on pipes in crawlspaces or basements prevents most freeze-related losses. These practical steps protect your home and demonstrate risk awareness to insurers.

Flood and Earthquake Coverage Gaps

Flood risk presents a separate challenge for Seattle properties. Standard homeowners policies exclude water damage from groundwater, heavy rainfall, or nearby bodies of water, yet atmospheric rivers and potential tsunamis threaten the region regularly. FEMA flood maps and First Street Foundation climate models pinpoint your actual flood risk at your specific address rather than relying on general neighborhood assumptions. Flood insurance through the National Flood Insurance Program is available, but it takes up to 30 days to activate, so securing coverage ahead of spring flooding season matters significantly.

Earthquake coverage is equally absent from standard policies and requires a separate endorsement or standalone policy. The U.S. Geological Survey confirms substantial seismic risk in the Pacific Northwest, making this protection essential rather than optional. Obtaining quotes for both flood and earthquake coverage during your initial policy shopping process prevents gaps in your protection timeline and often costs less than adding these protections later.

What Coverage Amounts Actually Protect Your Seattle Home

Dwelling Coverage Must Match Rebuilding Costs

Your dwelling coverage must reflect the actual cost to rebuild your home, not its market value. Many Seattle homeowners significantly underestimate rebuilding costs and purchase inadequate coverage. A 2,500-square-foot home built in 1955, like the South Seattle example quoted at $1,600 annually, requires careful assessment of current construction costs in your specific area. If your home suffers total loss and your dwelling coverage falls short, you absorb the difference-there is no safety net.

Replacement cost coverage pays to rebuild without depreciation, while actual cash value policies deduct wear and tear, potentially reducing payouts by 30% to 50%. Request a detailed replacement cost estimate from your carrier or a local contractor before finalizing coverage limits. This step prevents the painful discovery that your policy cannot cover full reconstruction expenses.

Personal Property and Scheduled Items

Personal property coverage typically equals 50% to 70% of your dwelling coverage amount, but this standard formula rarely matches your actual belongings. High-value items like jewelry, art, or electronics require scheduled riders listing them separately with agreed-upon values, protecting you against the depreciation penalty that standard coverage applies. A homeowner with $600,000 in dwelling coverage and standard 50% personal property coverage receives only $300,000 for belongings-insufficient if you own significant valuables.

Review your possessions room by room and document everything with photos and receipts; this inventory accelerates claims settlement when losses occur. Taking time now to photograph and list your belongings prevents disputes later about what you owned and what it was worth.

Liability Protection and Umbrella Policies

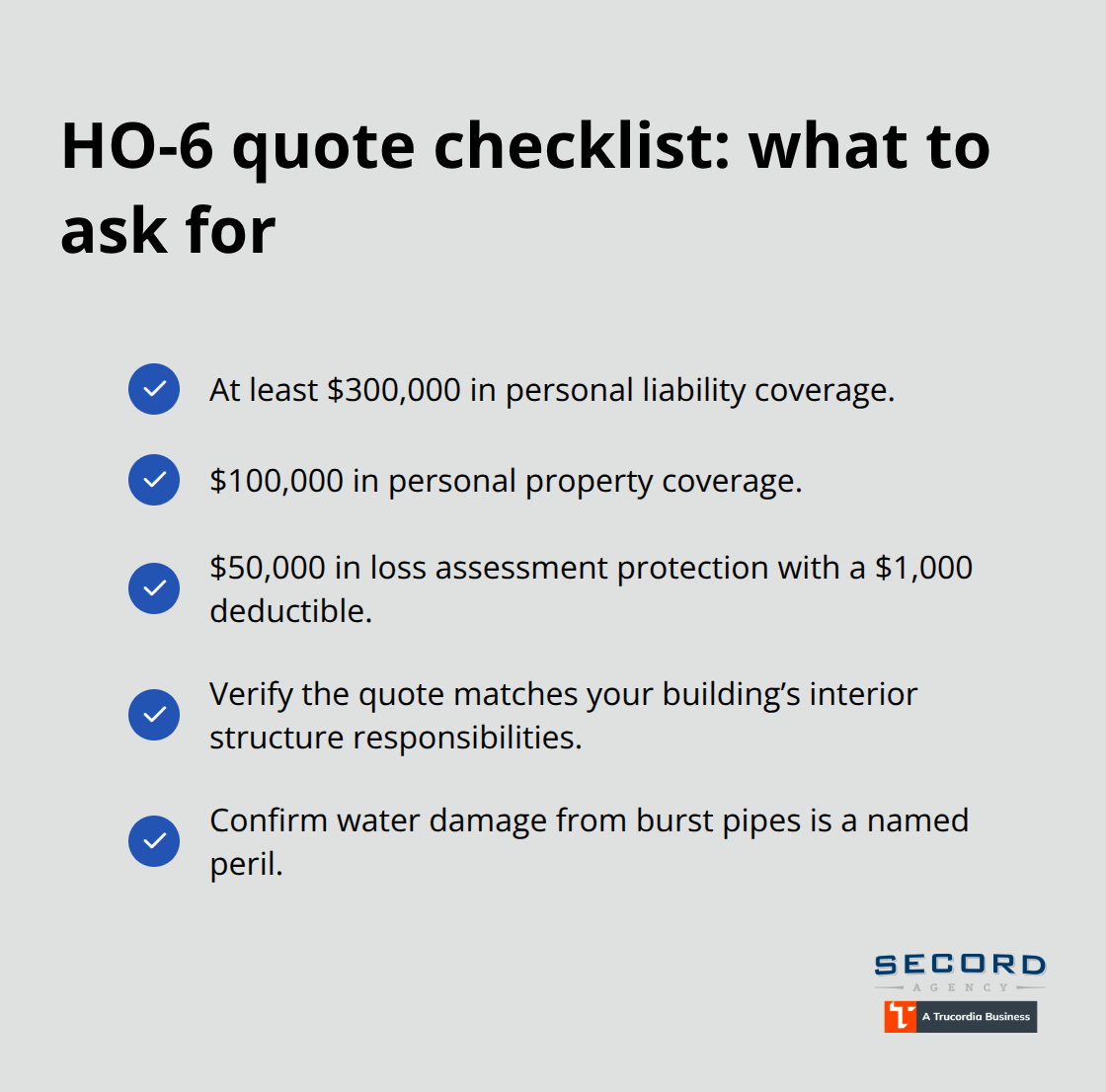

Liability coverage starting at $100,000 leaves your assets exposed to judgment claims that easily exceed this amount. Increasing to $300,000 costs relatively little, and an umbrella policy adding $1 million of liability protection typically runs $150 to $300 annually, making it an inexpensive safeguard against catastrophic claims. This additional layer protects your home equity and future earnings from major liability judgments.

Water Damage and Specialized Endorsements

Water damage beyond standard coverage requires specific attention in Seattle; water backup and sewer backup are commonly excluded or capped at modest amounts like $5,000 or $10,000, leaving households vulnerable during heavy storms. Adding water backup coverage and sewer backup as separate endorsements protects against costly intrusion from municipal systems backing up into your home. These endorsements matter significantly in a region where atmospheric rivers and aging infrastructure create frequent water-related losses.

Shopping Multiple Carriers for Complete Coverage

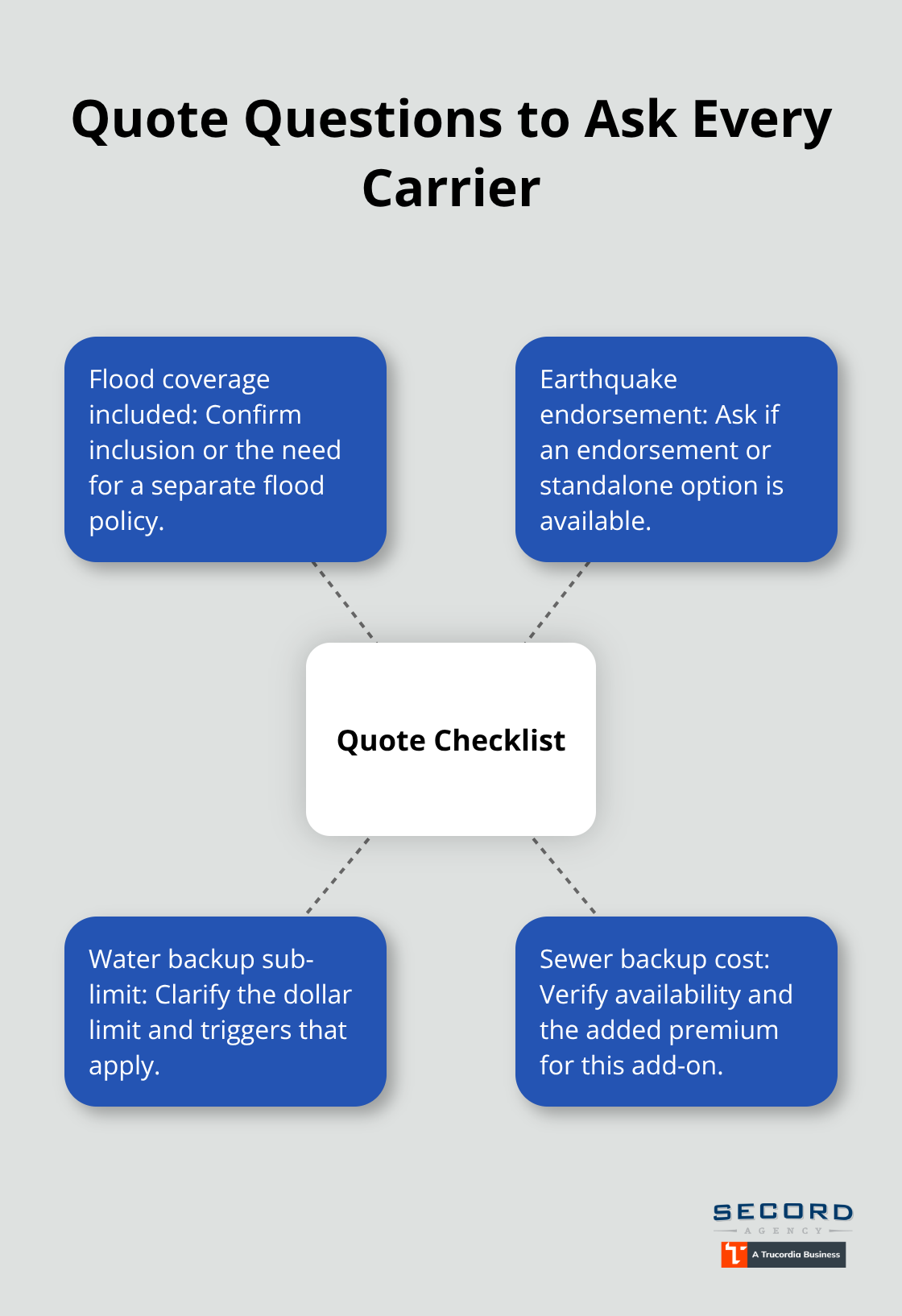

Earthquake and flood coverage require separate policies or endorsements costing roughly $300 to $800 yearly for earthquake and $400 to $1,200 for flood, depending on your specific risk zone and home characteristics. Shopping three to five carriers simultaneously lets you compare whether they include water backup, offer earthquake and flood options, and what their sub-limits are for specialized coverages. An independent agent representing multiple carriers can tailor coverage to regional hazards and bundle policies to reduce overall costs without requiring you to contact separate agencies. This approach ensures you understand exactly what protection each carrier provides and at what price, rather than accepting the first quote you receive.

Finding the Right Seattle Homeowner Policy Without Overpaying

Compare Quotes Across Multiple Carriers

Comparing quotes across multiple carriers is non-negotiable if you want affordable coverage that actually protects your Seattle home. The average homeowners insurance cost in Washington runs around $2,593 per year according to U.S. News, but premiums vary dramatically-from roughly $1,550 with PEMCO to over $4,600 with other carriers for identical $600,000 dwelling coverage. This $3,000 annual spread means shopping three to five insurers simultaneously reveals genuine price differences and coverage variations that matter.

When you request quotes, ask specifically whether flood coverage is included, if earthquake is available as an endorsement, what the water backup sub-limit is, and whether sewer backup coverage costs extra. Most carriers structure these protections differently, so direct comparison prevents missing critical gaps or overpaying for redundant coverage.

Evaluate Financial Strength and Claims Handling

PEMCO currently offers the lowest average premium at $1,550 annually in Washington, followed by USAA at approximately $149 monthly or $2,068 yearly, according to U.S. News data. However, cheapest does not always mean best-financial strength and claims handling reputation matter enormously when you file a claim after a major loss.

Check the Washington Department of Insurance website for complaint data and financial strength ratings before selecting a carrier, since a low premium means little if the insurer delays payment or disputes your claim for months.

Bundle Policies and Unlock Volume Discounts

Bundling your homeowners policy with auto, RV, or boat coverage generates substantial savings that single-policy shopping misses entirely. An independent agent representing multiple carriers can compare earthquake and flood options, layer on water backup endorsements, bundle policies across your entire insurance portfolio, and negotiate volume discounts without requiring you to contact separate agencies.

Beyond bundling discounts, many carriers offer reductions for protective devices like alarms and indoor sprinklers, claim-free history, and specialized discounts-PEMCO, for example, provides educator discounts that many homeowners never discover.

Review Your Policy Annually and After Home Changes

Requesting quotes annually matters more than most homeowners realize; your current carrier’s rates may have risen while competitors have lowered theirs, meaning you could reduce your premium significantly with a single phone call. After home improvements like a new roof or updated electrical wiring, notify your insurer immediately, as safety upgrades often qualify for discounts that offset the cost of renovation within a year or two.

An annual policy review (particularly after any home changes or life transitions) keeps your dwelling coverage aligned with current rebuilding costs and ensures your personal property limits match your actual belongings rather than an outdated estimate. Secord Agency, a Trucordia business based in Seattle’s Wallingford neighborhood, shops multiple carriers to deliver competitive rates paired with local, advocate-led service that simplifies quotes and claims while providing personalized advice and ongoing policy reviews.

Final Thoughts

Seattle’s unique weather patterns, seismic activity, and flood risk demand more than a standard homeowners insurance policy. Wind and hail damage, freezing pipes, earthquakes, and flooding represent genuine threats that require targeted coverage tailored to Pacific Northwest conditions. Your Seattle homeowners insurance policy should reflect actual rebuilding costs, include adequate liability protection, and address regional hazards that standard policies exclude.

Obtain quotes from three to five carriers simultaneously and ask directly about flood, earthquake, water backup, and sewer backup coverage to understand exactly what each insurer provides and at what cost. Review your dwelling coverage amount against current rebuilding expenses in your area rather than relying on outdated estimates or market value assumptions. Schedule an annual policy review to confirm your coverage aligns with home improvements, personal property changes, and evolving risk factors in your neighborhood.

Working with a local insurance agent eliminates the burden of contacting multiple carriers separately and comparing complex policy documents on your own. An independent agent representing multiple insurers bundles your homeowners policy with auto and other coverage to generate substantial savings, identifies specialized discounts you might otherwise miss, and provides ongoing guidance as your circumstances change. Contact Secord Agency today to review your current coverage and ensure your Seattle homeowners insurance policy matches your needs and regional risks.