Personal Umbrella Insurance Quotes Washington: Lock in Extra Liability

Your homeowners and auto insurance policies have limits. When a major accident or lawsuit pushes beyond those boundaries, your personal assets face real danger.

At Secord Agency – A Trucordia Business, we help Washington residents find personal umbrella insurance quotes that fill these gaps. Umbrella coverage adds an extra layer of liability protection-often for less than you’d expect.

What Umbrella Coverage Actually Covers

Personal umbrella insurance sits above your existing auto and homeowners policies, activating only after those underlying limits are exhausted. If you cause a serious accident or face a lawsuit that exceeds your current coverage, umbrella protection steps in to cover the difference. According to the Insurance Information Institute, $1 million in umbrella coverage costs about $383 per year, making it far cheaper than the financial devastation of a major liability judgment. Most policies start at $1 million in coverage, with each additional $1 million typically running $75–$150 annually.

Washington law treats umbrella policies as separate products, requiring you to add them explicitly to your insurance portfolio since they don’t automatically attach to your auto or homeowners policies under RCW 48.22.005. The coverage extends beyond simple bodily injury and property damage-it also protects against personal injury claims like defamation and malicious prosecution, which standard policies often exclude entirely.

Real-World Scenarios That Trigger Umbrella Protection

A guest at your home suffers a serious injury during a visit. Your dog bites someone and causes lasting harm. A teenage driver in your household causes a multi-vehicle accident that generates six-figure medical bills. Each scenario can exhaust your underlying limits quickly, leaving your personal assets vulnerable without umbrella coverage in place.

How Underlying Policies Work Together

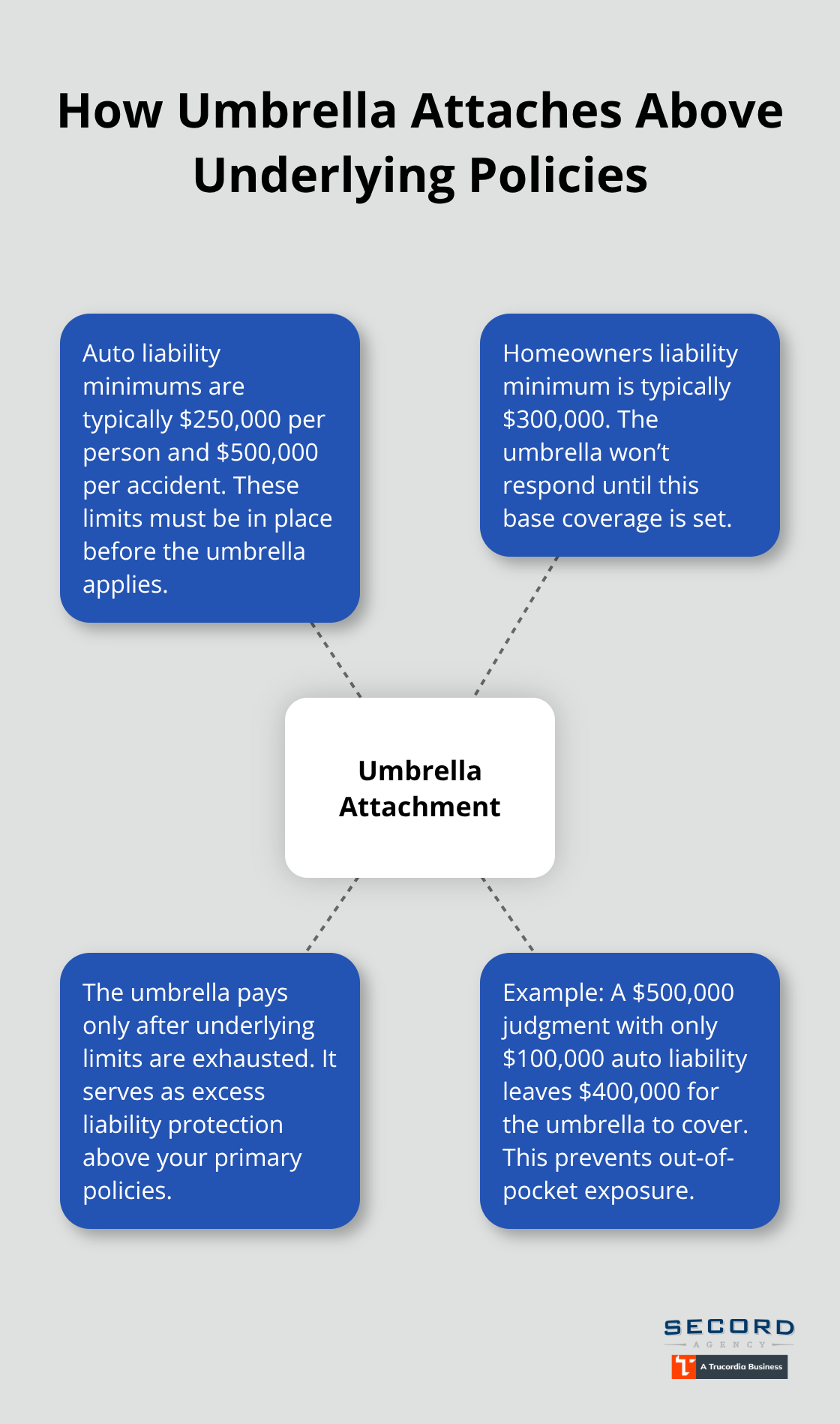

Your umbrella policy requires minimum underlying liability limits to attach properly-typically $250,000 per person and $500,000 per accident for auto liability, plus $300,000 for homeowners liability. These underlying limits act as the first line of defense; your umbrella only pays once those limits are exhausted. If you carry only $100,000 in auto liability and cause an accident resulting in a $500,000 judgment, your auto policy pays $100,000, then your umbrella covers the remaining $400,000.

Carriers set these minimums because they want to ensure you’re already protecting yourself adequately. One major carrier offering umbrella coverage in Washington requires that you also maintain their Personal Auto and Homeowner or Renter policies to qualify for their umbrella product, simplifying coordination across your coverage portfolio. This bundling approach often unlocks multi-policy discounts that reduce your total premium cost.

Matching Coverage to Your Net Worth

A practical strategy involves matching your umbrella limits to your net worth. If you own a home worth $400,000 with $200,000 in retirement savings, carrying $1 million in umbrella coverage aligns protection with your actual assets at risk. This approach ensures you carry adequate protection without overpaying for limits you don’t need. Washington residents with significant property values or multiple assets should evaluate their exposure carefully before selecting coverage amounts.

Why Washington Residents Face Higher Liability Exposure

Property Values Create Real Asset Risk

Washington’s median home price reached $520,000 in 2024, and property values continue climbing across most neighborhoods in the state. When your net worth grows, your liability exposure grows with it-a serious accident or lawsuit can now wipe out six figures in assets, not just thousands. A dog bite, a guest’s fall on your property, or a teenage driver’s multi-vehicle accident doesn’t care about your home equity or savings account. Without umbrella coverage, a single judgment forces asset sales, wage garnishment, or worse.

Washington law requires you to carry minimum underlying liability limits before attaching umbrella coverage, but those minimums often fall short of protecting what you’ve actually built. The Insurance Information Institute reports that average settlement amounts for serious personal injury cases range from $24,000 to $55,100, with medical costs and pain-and-suffering awards climbing faster than most people’s insurance limits.

Judgments Now Exceed Standard Policy Limits

Lawsuit frequency in Washington has increased significantly. A homeowner’s liability claim now averages $400,000 to $600,000 when it goes to judgment, well beyond what a standard $300,000 homeowners policy covers. Auto accident judgments regularly exceed $500,000 in cases involving permanent injury or multiple claimants.

Legal defense costs alone can run $50,000 to $150,000 before any settlement payment reaches the table. Your underlying auto and homeowners policies cover legal defense, but that defense happens within your policy limits-once you’re sued for more than your coverage allows, you pay additional attorneys out of pocket.

The True Cost of Umbrella Protection

A $1 million umbrella policy costs roughly $200 to $400 annually for most Washington residents, yet protects against judgments that could otherwise consume years of income and force liquidation of retirement accounts. The math is stark: umbrella coverage costs pennies on the dollar compared to the financial ruin that follows a major liability event.

Property owners with pools, rental units, or teenage drivers face even steeper risk. These exposures alone justify umbrella protection as a non-negotiable safeguard rather than an optional add-on. The gap between what your standard policies cover and what courts award in major cases has widened dramatically, making umbrella insurance less of a luxury and more of a practical necessity for Washington homeowners.

How to Get Personal Umbrella Insurance Quotes in Washington

Prepare Your Current Policy Information

Accurate umbrella quotes require your existing policy declarations from your auto and homeowners insurance. Carriers need proof of your underlying limits before they’ll quote you, and most Washington insurers won’t attach an umbrella without minimum underlying coverage in place-typically $250,000 per person and $500,000 per accident for auto liability, plus $300,000 for homeowners liability. If your current limits fall short of these minimums, you’ll need to raise them first. Raising your auto liability from $100,000 to $250,000 adds roughly $15 to $30 annually, a small price for unlocking umbrella eligibility.

Contact Multiple Carriers and Independent Agents

Once you have those declarations ready, contact multiple carriers directly or work with an independent insurance agent who shops the market on your behalf. Western National, for example, requires you to bundle their Personal Auto and Homeowner policies alongside their umbrella product, which often triggers multi-policy discounts that offset the umbrella cost entirely. An independent agent in Washington can pull quotes from five to eight carriers simultaneously, saving hours of phone calls and ensuring you compare apples to apples across coverage types and premium structures.

Request Detailed Quote Breakdowns

Two carriers might both quote $1 million in umbrella coverage at vastly different prices because they weight risk factors differently-one might charge more if you have a teenage driver, another might focus heavily on your property value or pet ownership. Request the full quote breakdown from each carrier, not just the premium. Ask specifically what personal injury coverages are included beyond bodily injury and property damage, since defamation and malicious prosecution protections vary significantly between policies. One carrier might include worldwide coverage automatically while another charges an extra $50 annually for it.

Average premiums for umbrella coverage range between $150 to $350 per year for $1 million in coverage, though your premiums may be higher based on your risk. Quotes substantially above this range warrant scrutiny-you’re either overbuying coverage you don’t need or the carrier is loading your premium with risk factors worth challenging.

Identify Available Discounts

Ask each insurer what discounts apply to your situation. Multi-policy bundling typically saves 10 to 15 percent, good student discounts apply if you have teenagers, and some carriers offer safety feature discounts for alarm systems or security cameras. A quote that drops from $450 to $380 after applying available discounts looks dramatically different than the sticker price.

Compare and Evaluate Your Options

Try obtaining at least three quotes before deciding, and specifically request that carriers explain any premium differences in writing so you understand whether you’re paying more for better coverage or simply a higher risk assessment.

Final Thoughts

Umbrella insurance protects what you’ve built in Washington. Your home, retirement savings, and future income face real exposure when a single accident or lawsuit exceeds your standard policy limits. A $1 million umbrella policy costs $200 to $400 annually, yet shields you from judgments that could otherwise force asset sales or wage garnishment.

Property values in Washington continue climbing, and with them, your liability exposure grows. A serious accident involving a guest, pet, or teenage driver can generate six-figure medical bills and legal costs that exhaust your underlying limits within weeks. Without umbrella coverage, you’re personally responsible for everything beyond that point.

Contact Secord Agency – A Trucordia Business to review your personal umbrella insurance quotes in Washington and lock in the extra liability protection your family needs. We shop multiple carriers to deliver competitive rates paired with personalized advice that matches your actual asset protection needs.