Washington Landlord Insurance Quotes: Quick Local Comparisons

Landlords in Washington face unique insurance challenges that standard homeowners policies simply don’t address. Getting the right coverage protects your rental investment from liability claims, property damage, and income loss.

We at Secord Agency – A Trucordia Business help property owners find Washington landlord insurance quotes that match their specific needs. This guide walks you through what coverage matters, how to compare options, and which gaps could cost you thousands.

What Washington Landlords Actually Need to Know About Insurance Requirements

Washington doesn’t legally mandate landlord insurance, but this freedom comes with real consequences. If your property has a mortgage, your lender almost certainly requires it-and they won’t accept excuses when a claim gets denied because you skipped proper coverage. According to the Washington State Office of the Insurance Commissioner, average landlord property damage claims in the state exceeded $9,800 in 2022, with liability claims topping $22,300. Those numbers show why lenders protect themselves by requiring proof of coverage before they’ll fund your loan.

Why Lenders Demand Coverage You Might Think Is Optional

The Residential Landlord-Tenant Act shapes what you’re legally responsible for as a landlord, and your insurance needs to back up those obligations. If you rent out a property and something goes wrong-a tenant gets hurt on your premises, a pipe bursts and damages the unit, or a fire forces the tenant out for months-your homeowners policy won’t cover any of it. Homeowners insurance explicitly excludes losses on properties where the owner doesn’t live. That gap between what homeowners policies cover and what actually happens on rental properties is exactly why landlord insurance exists.

The Coverage Gap Homeowners Policies Leave Behind

Standard homeowners insurance protects your primary residence against fire, theft, liability, and weather damage. The moment you rent out that property, the policy becomes void for rental-related claims. Your carrier will either cancel the policy outright or deny claims, leaving you personally liable for everything. Landlord insurance fills this gap with three core components: dwelling coverage for the building itself, liability protection if someone gets injured on your property, and loss-of-rent coverage that replaces your income while the unit sits empty during repairs.

What Landlord Insurance Actually Costs in Washington

In 2023, Washington landlord insurance averaged about $1,190 to $1,860 per year for a $300,000 dwelling, depending on property age, location, and local hazards. That cost varies significantly based on whether your property sits in a high-earthquake zone like the Puget Sound region or faces wildfire exposure in Eastern Washington. Loss-of-rent coverage is the piece most landlords underestimate-it covers your mortgage, taxes, and operating costs when a covered loss makes the unit uninhabitable. Without it, you pay those expenses from your own pocket while the property produces zero income.

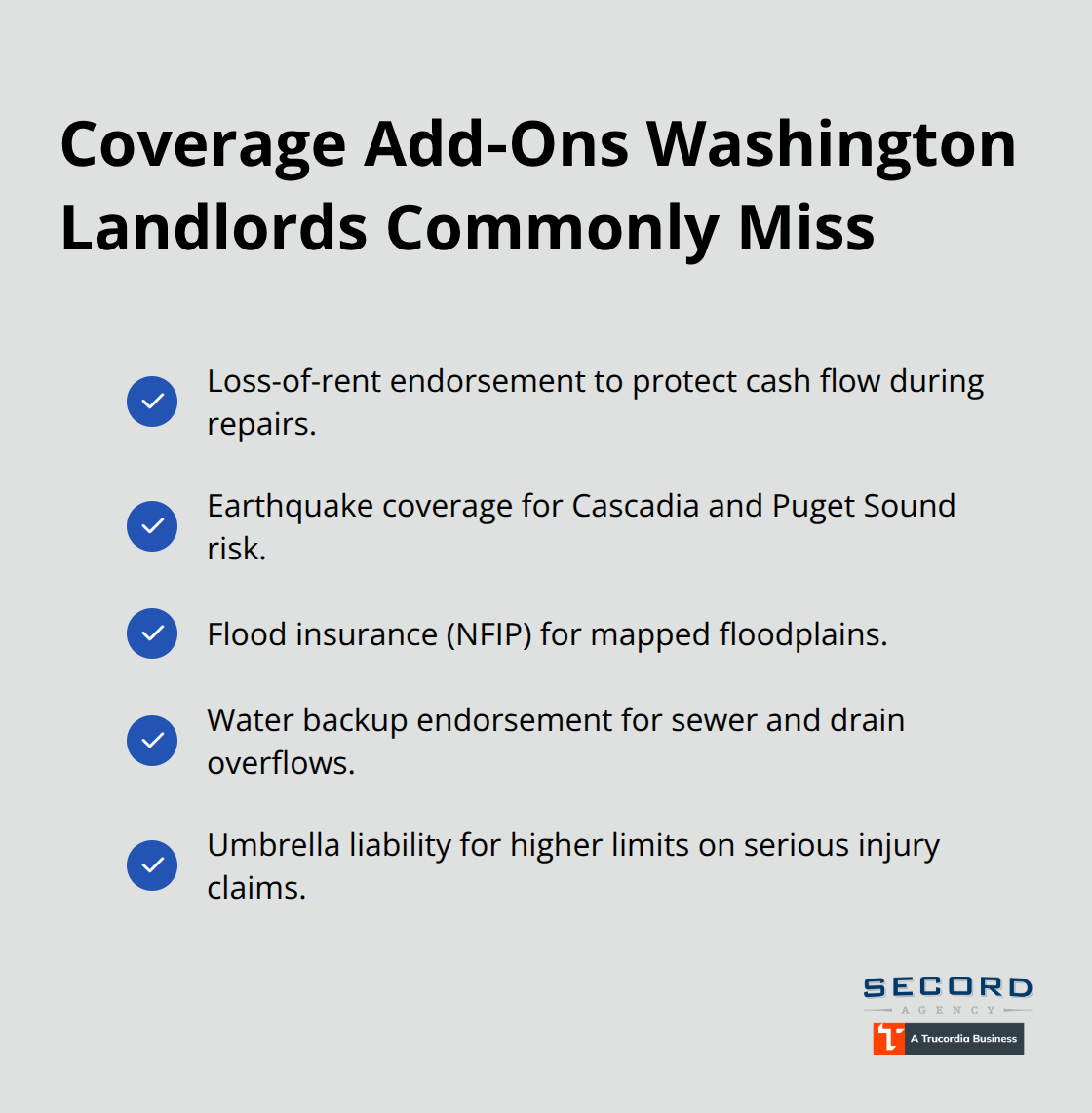

Earthquake Coverage: Not Optional for Western Washington

Western Washington properties need earthquake coverage as a separate endorsement or policy, since standard landlord policies exclude earth movement. Homes near the Cascadia Subduction Zone may face higher premiums due to the potential for significant earthquake events. This regional risk shapes what coverage you actually need when you compare quotes from different carriers-and it’s exactly the kind of local detail that separates adequate protection from dangerous gaps.

Getting Accurate Quotes From Washington Carriers

Provide the Right Property Information

To get a real quote, you need to provide specific information that directly affects your premium. Start with the property address-carriers use location data to assess earthquake risk, wildfire exposure, flood zones, and local crime rates, which can swing your quote by hundreds of dollars depending on whether you’re in Seattle’s Puget Sound zone or Eastern Washington. Next, provide the property type (single-family home, duplex, triplex, or four-plus units), year built, roof age, and roof material. Roof age matters significantly because most carriers limit or exclude roof damage if the roof exceeds 10 years old, and DP-3 policies handle this better than DP-1 or DP-2 forms.

You’ll also need to specify the dwelling replacement cost (not market value), the number of rental units, expected monthly rent, and whether the property will be occupied or vacant. If you plan to rent short-term through Airbnb or VRBO, disclose that upfront-standard policies exclude short-term rentals, and you’ll need a specialized endorsement that typically costs 20 to 40 percent more than long-term rental coverage.

Request Identical Coverage Limits Across Carriers

When comparing quotes across carriers like Safeco, Stillwater Insurance Group, or Progressive, request identical coverage limits and deductibles from each. Don’t compare a $500,000 liability limit from one carrier against a $1,000,000 limit from another-you won’t know which price difference comes from better rates versus different coverage. Deductibles directly impact your monthly cost: increasing from $1,000 to $2,500 typically cuts premiums by 8 to 15 percent, but only if you maintain a cash reserve equal to that deductible amount.

The average cost of landlord insurance across the nation is approximately $1,478 annually, but earthquake-prone areas in the Puget Sound region and wildfire corridors in Eastern Washington see surcharges up to 35 percent higher. Request specific information about what each quote includes: does it cover loss of rent during repairs, vandalism at vacant properties, or building code upgrades after a loss?

Understand How Policy Forms Affect Your Cost and Coverage

DP-1 policies are the cheapest but cover only basic perils like fire and wind, leaving you exposed to theft and vandalism unless you add endorsements. DP-3 provides open-perils coverage and costs 15 to 25 percent more than DP-2, but it’s worth the premium if your property has an older roof or sits in a high-risk zone. Regional hazards-Cascadia earthquake risk, atmospheric river flooding, wildfire smoke-affect your specific property’s coverage needs and cost in ways that standard quotes often miss.

An independent agent can shop multiple carriers at once and explain how these local factors shape your protection and premium. This expertise becomes especially valuable when you’re weighing the trade-offs between lower upfront costs and the coverage gaps that could expose you to significant losses. As you move forward with comparing quotes, the next step involves identifying which coverage gaps most landlords overlook-and how those oversights can turn into expensive mistakes.

What Most Washington Landlords Get Wrong About Coverage

Loss-of-Rent Coverage Protects Your Cash Flow, Not Just Your Income

Most landlords grab the cheapest quote they find and never ask what happens when the property sits empty for three months or when a flood forces tenants out. Loss-of-rent coverage is where the real financial damage occurs when landlords skip it. This coverage replaces your mortgage payment, property taxes, insurance premiums, and utilities while the unit is uninhabitable after a covered loss-not just the rental income you would have collected. If you own a $400,000 property with a $250,000 mortgage, your monthly costs easily exceed $3,500 even when zero rent comes in. Without loss-of-rent coverage, you absorb those expenses entirely from your own cash reserves.

In Washington, where median rent-to-income ratios run 15 to 20 percent higher than the national average, losing three months of rent while paying full operating costs can deplete your reserves faster than most landlords anticipate. The Washington State Office of the Insurance Commissioner reported that average property damage claims exceeded $9,800 in 2022, and many of those claims involved weeks or months of repair time. Standard DP-1 policies don’t include loss-of-rent coverage at all, so you must specifically request it-and most carriers offer it as an endorsement rather than automatic coverage. Request a specific dollar amount for loss-of-rent based on your actual monthly rent, not a generic percentage.

Earthquake Coverage Addresses a Real Regional Threat

Earthquake coverage represents one of two gaps that turn into catastrophic losses in Washington. Standard landlord policies exclude earth movement entirely, which means a Cascadia Subduction Zone event leaves you completely unprotected unless you purchased a separate endorsement. The Washington Geological Survey estimates a 10 to 15 percent probability of a major Cascadia earthquake within the next 50 years, with potential statewide replacement costs exceeding $50 billion. Homes near the Puget Sound region face the highest risk, and earthquake endorsements typically cost $150 to $300 annually depending on construction type and proximity to fault lines.

Flood Insurance Fills Another Critical Gap

Flood insurance through the National Flood Insurance Program costs $300 to $800 per year for properties in mapped floodplains, and more than 175,000 structures in Washington sit in those zones according to the Department of Ecology. If your property is in a Zone A or V flood zone, standard policies won’t cover water damage, and your lender will require proof of flood coverage before funding or refinancing. Sewer backups during heavy spring rain also fall outside standard coverage, so water backup endorsements protect you when atmospheric rivers overwhelm drainage systems.

Umbrella Liability Protects Your Personal Assets

High-value properties need umbrella liability coverage beyond the standard $500,000 to $1,000,000 limits that come with basic landlord policies. If you own multiple properties or a single property worth over $750,000, a $1 million to $2 million umbrella policy costs roughly $200 to $400 annually and protects you when liability claims exceed your underlying landlord policy limits. Courts in Washington have awarded liability judgments well above standard policy limits in cases involving serious injuries on rental properties, making umbrella coverage essential for protecting your personal assets.

Final Thoughts

Finding the right Washington landlord insurance quotes requires you to balance cost against the specific hazards your property faces. The cheapest quote won’t protect you if it skips loss-of-rent coverage, earthquake endorsements, or flood protection-gaps that turn into five-figure losses when claims happen. Your property’s location, age, and construction type determine which coverage forms make sense: DP-1 works for newer properties in low-risk areas, while DP-3 becomes essential for older roofs or Puget Sound properties near earthquake zones.

Request identical coverage limits across carriers so you’re comparing actual protection, not just price tags. Increase your deductible to $2,500 if you maintain a cash reserve, since that move typically cuts premiums by 8 to 15 percent without exposing you to unmanageable out-of-pocket costs. An independent insurance agent eliminates the guesswork by shopping multiple carriers at once and explaining how local hazards affect your specific property.

Start by gathering your property details: address, year built, roof age, dwelling replacement cost, and expected monthly rent. Contact Secord Agency to request quotes with identical liability limits and deductibles. Compare what each quote includes for loss-of-rent, earthquake, and flood coverage, then secure your rental investment by purchasing a policy that protects your cash flow, not just your building.