Homeowners Umbrella Overview: What Your Extra Liability Really Covers

Your homeowners insurance has limits. When someone gets seriously injured on your property or you cause major damage elsewhere, those limits can disappear fast.

A homeowners umbrella overview shows you why most homeowners are underprotected. We at Secord Agency – A Trucordia Business help Washington homeowners understand what extra liability coverage actually does and why it matters for your financial security.

What Umbrella Insurance Actually Is

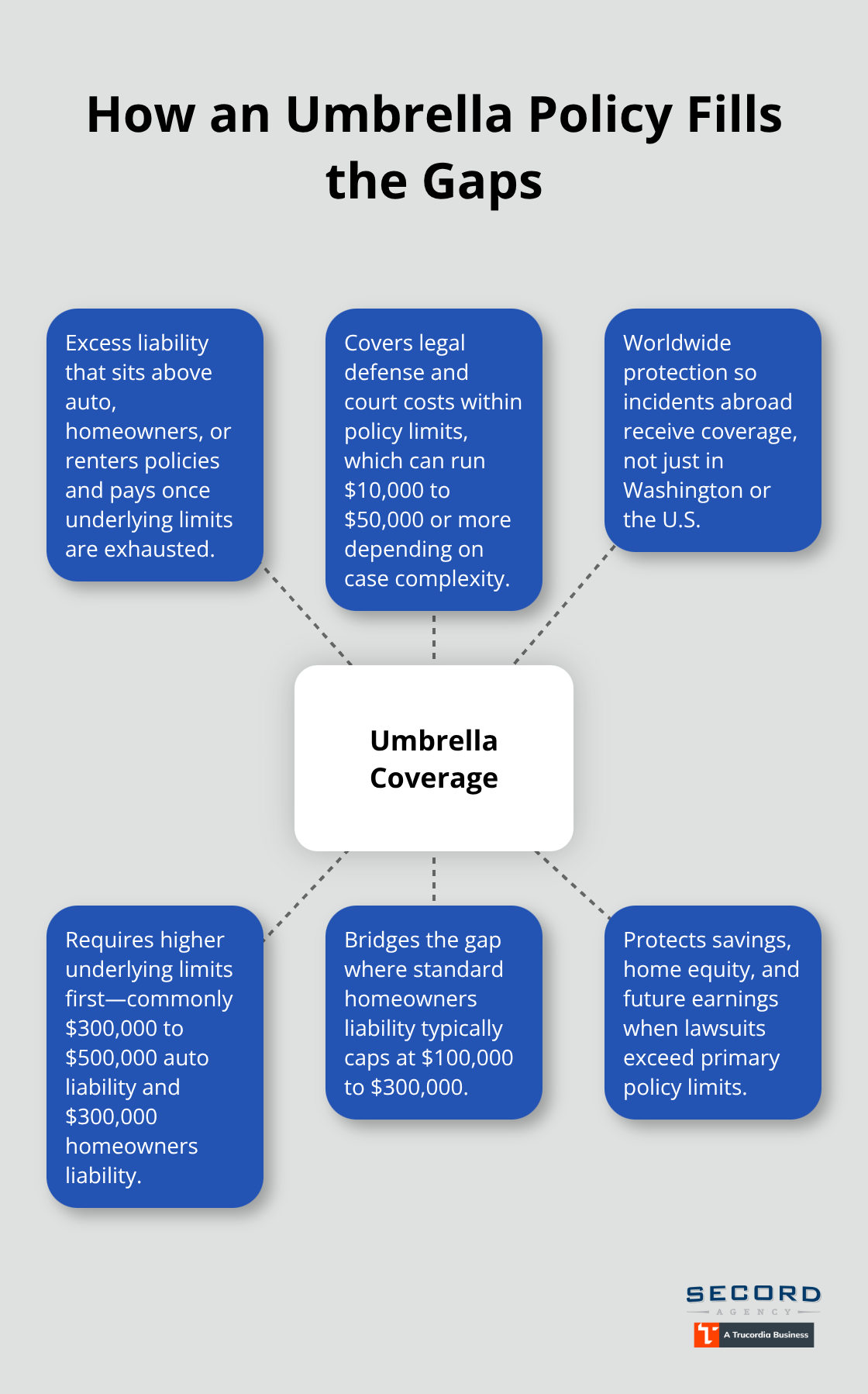

A homeowners umbrella policy is straightforward: it’s extra liability coverage that sits on top of your homeowners and auto insurance. When someone sues you and the damages exceed what your primary policies cover, your umbrella kicks in to pay the difference. According to the Insurance Information Institute, umbrella policies typically start at $1 million in coverage and cost around $150 to $300 per year for that initial million dollars.

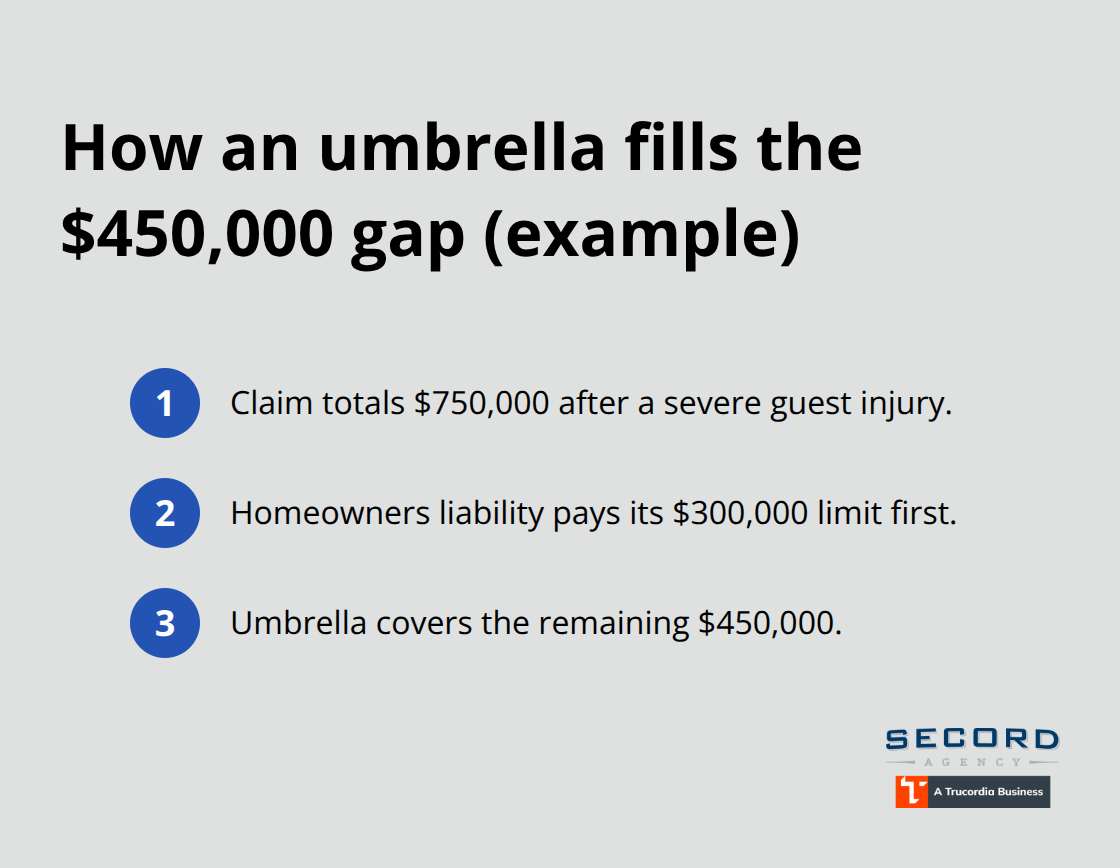

The real value emerges when you face a serious liability claim. If a guest suffers a severe injury on your property and medical bills plus pain and suffering damages reach $750,000, but your homeowners liability limit is only $300,000, your umbrella covers the remaining $450,000. Without it, you’d be personally liable for that gap. Washington homeowners often underestimate their exposure because they assume their standard homeowners policy handles everything.

It doesn’t-most homeowners policies include $100,000 to $300,000 in liability coverage, which sounds adequate until an actual lawsuit happens.

How Your Umbrella Coordinates with Existing Coverage

Umbrella insurance doesn’t replace your homeowners or auto policies-it requires them. Insurance Information Institute data shows carriers typically demand minimum underlying limits before issuing an umbrella: homeowners liability around $250,000 to $300,000 and auto liability around $250,000. This isn’t arbitrary. Your primary policies must be solid because the umbrella only activates once those limits are exhausted.

If you have a weak homeowners policy with $100,000 in liability and purchase a $1 million umbrella, you’ve created a dangerous gap. An injury claim could max out your $100,000 limit, then jump straight to your umbrella, but that $100,000 shortfall between policies might not be covered depending on how your umbrella is written. The coordination matters because defense costs including attorneys’ fees, court costs, and expert-witness fees come out of your policy limits. If your homeowners policy pays $250,000 for defense and settlement, your umbrella’s $1 million starts at $750,000 remaining, not the full million.

Coverage Limits That Match Your Reality

The Insurance Information Institute notes that umbrella policies provide worldwide coverage, which matters if you own vacation property or frequently travel. A $1 million umbrella works for many homeowners, but your actual needs depend on your assets and risk profile. If you own a home worth $600,000, carry $200,000 in savings, and have investment accounts totaling $300,000, a $1 million umbrella provides reasonable protection.

High-net-worth individuals or those with rental properties often need $2 million to $5 million in umbrella coverage. Consider your specific liability risks too. Owning a pool, trampoline, or large dog significantly increases your exposure. Hosting frequent gatherings or having teenage drivers on your policy raises your odds of a claim. A real example from industry data shows that two teenage drivers can push annual car insurance costs to around $6,000 and raise umbrella premiums from approximately $1,000 to $3,000 yearly, reflecting the increased risk they represent.

Identifying Your Personal Liability Gaps

Your current homeowners and auto policies likely leave you exposed in ways you haven’t considered. Most standard policies exclude certain liability situations-rental property claims, business-related incidents, or personal injury claims like defamation and slander. An umbrella policy extends protection to these personal injury scenarios, covering false arrest, libel, and invasion of privacy claims that your primary policies won’t touch.

The gap between what you own and what you could lose in a lawsuit often surprises homeowners. You can face liability claims that exceed your net worth, which means a single incident could threaten assets you’ve spent decades building. This reality makes understanding your umbrella’s actual scope essential before a claim forces you to learn what isn’t covered. The next section examines exactly what homeowners umbrella policies cover and what they leave unprotected.

When You Need Umbrella Coverage

A homeowners umbrella isn’t something everyone needs immediately, but certain life situations create genuine liability risk that demands it. The Insurance Information Institute identifies specific exposures that elevate your vulnerability: owning a pool, maintaining a trampoline, keeping a large dog, hosting frequent social gatherings, or having teenage drivers on your auto policy. These aren’t theoretical risks-they represent documented claim patterns insurers track closely.

High-Risk Situations That Demand Protection

If you host regular parties or holiday events, your property becomes a venue where injuries happen more frequently. A guest slips on your deck and breaks their arm, and suddenly you face medical bills, lost wages, and pain-and-suffering claims that your standard homeowners policy won’t fully cover. The same logic applies to pools and trampolines: they attract liability claims at rates significantly higher than properties without them.

Teenage drivers present another concrete risk factor. Insurers price coverage increases based on actual accident frequencies and claim severity, not guesswork. Your exposure multiplies when multiple risk factors combine on one policy.

Your Asset Protection Threshold

The real question isn’t whether you’re wealthy enough for umbrella coverage-it’s whether you have anything worth protecting. If you own a home, carry any savings, or have retirement accounts, an umbrella makes sense. Washington homeowners with property worth $400,000 or more combined with $100,000 in liquid savings face meaningful exposure.

A single serious liability claim could force asset liquidation or wage garnishment that lasts years. High-net-worth individuals with multiple properties, investment portfolios, or rental income absolutely require umbrella protection; many should carry $2 million to $5 million in limits rather than the standard $1 million. Even middle-income homeowners benefit from starting with $1 million coverage, which costs only $150 to $300 annually according to Insurance Information Institute data. The affordability shifts the calculation entirely-the cost is so low relative to the protection offered that skipping umbrella coverage becomes the riskier financial choice.

Washington’s Liability Landscape and Legal Exposure

Washington state doesn’t legally require umbrella insurance, but the state’s legal environment makes it practically essential for homeowners with substantial assets. Washington follows a comparative negligence standard, meaning courts can find you partially liable even if you weren’t the primary cause of an injury. This broadens your exposure significantly compared to states with stricter liability rules.

Additionally, Washington has no caps on non-economic damages in personal injury cases, which means pain-and-suffering awards can reach six or seven figures in serious injury claims. A guest suffers a permanent spinal injury at your home, and the jury can award whatever they deem appropriate for their suffering without statutory limits. These legal realities make the gap between your homeowners policy limits and potential liability awards dangerously wide. Your homeowners policy’s $300,000 liability limit looks adequate until you face a claim in an environment where damages routinely exceed that amount. Understanding what your umbrella actually covers becomes the next critical step in protecting yourself against these Washington-specific risks.

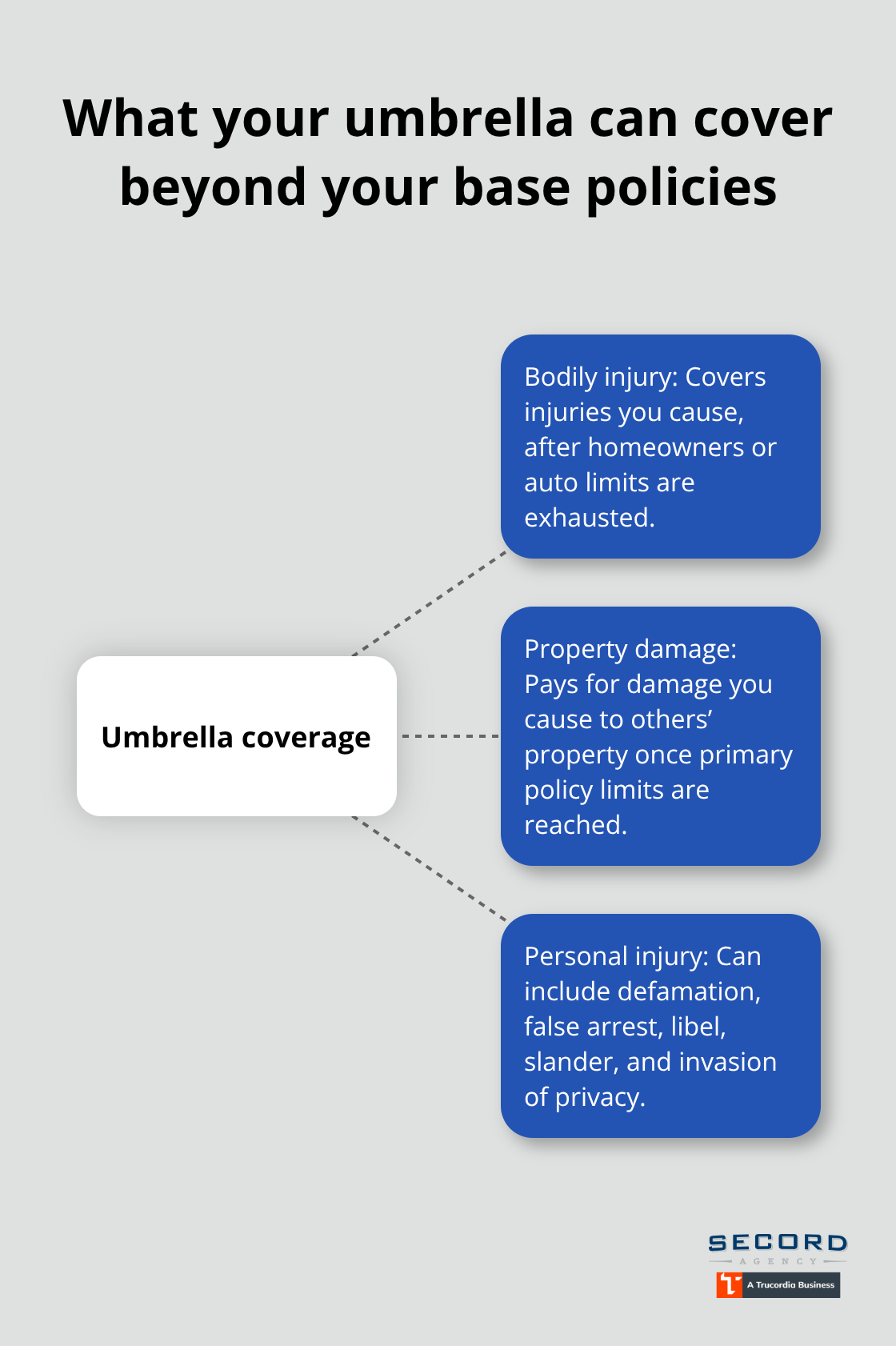

What Your Umbrella Actually Pays For

Your umbrella policy covers three distinct categories of liability that your homeowners and auto insurance either won’t touch or won’t cover fully. Understanding exactly what triggers umbrella protection prevents the shock of discovering mid-claim that something you assumed was covered actually isn’t.

Bodily Injury Claims and Medical Expenses

Bodily injury claims form the largest category of umbrella payouts. When someone suffers an injury on your property or due to your actions, your homeowners liability coverage pays up to its limit, then your umbrella takes over. A guest falls down your basement stairs and suffers a serious head injury requiring surgery, hospitalization, and ongoing physical therapy. Medical bills alone might reach $200,000, but add pain and suffering damages and the total claim could hit $600,000. Your homeowners policy covers the first $300,000, and your $1 million umbrella covers the remaining $300,000.

Umbrella policies also cover defense costs including attorney fees and court expenses, which means those costs don’t reduce your available coverage limits. This protection proves invaluable because legal defense in serious injury cases can involve substantial expenses before any settlement is reached.

Property Damage Liability Coverage

Property damage liability works similarly but applies to damage you cause to someone else’s belongings. You accidentally back your car into a neighbor’s fence, causing $15,000 in damage. Your auto policy’s property damage limit covers this easily. But what if your teenage driver causes a serious accident that totals another vehicle and damages surrounding property, with total damages reaching $175,000? Your auto policy pays its limit, your umbrella covers the excess.

Personal Injury Liability Protection

Washington homeowners often overlook personal injury liability coverage that umbrella policies provide. This covers claims for defamation, false arrest, libel, slander, and invasion of privacy-situations your standard homeowners policy explicitly excludes. If someone publicly accuses you of something damaging on social media and you can prove the statement was false, you can sue for defamation. Your umbrella covers your defense costs and any judgment if you lose, protecting you from legal expenses that could run substantial amounts even before any settlement.

What Your Umbrella Won’t Cover

The distinction between what umbrella covers and what it doesn’t matters enormously when a claim arrives. Your umbrella will not cover damage to your own property, liability from intentional acts, or claims arising from business activities. If you operate a home-based business and a client suffers an injury during a service you provide, your homeowners umbrella won’t respond-you need separate business liability coverage.

Rental property claims also fall outside standard homeowners umbrella protection. If you rent out a guest house and a tenant suffers an injury due to your negligence, that claim requires landlord liability coverage or a commercial umbrella endorsement. Umbrella policies coordinate with underlying policies, meaning your homeowners and auto coverage must be adequate. If your homeowners liability sits at $100,000 and you carry a $1 million umbrella, you’ve created a gap. Claims between $100,000 and where your umbrella begins might not receive full coverage depending on how your policy coordinates. Washington homeowners should maintain at least $300,000 in homeowners liability and $250,000 in auto liability before adding umbrella protection. That foundation ensures your umbrella activates properly when needed and covers the full scope of what you expect.

Final Thoughts

Your homeowners umbrella overview shows that standard policies leave you financially exposed when serious liability claims strike. A single injury on your property or accident you cause can easily exceed your homeowners liability limit of $300,000, especially in Washington where courts impose no caps on pain-and-suffering damages. Umbrella protection starting at just $150 to $300 annually for $1 million in coverage bridges that gap and protects the assets you’ve spent years building.

Assess your current situation by reviewing your homeowners and auto policy declarations to confirm your liability limits sit at $250,000 or higher for each. Evaluate your specific risk factors-hosting frequent gatherings, owning a pool, having teenage drivers, or maintaining rental property all increase your vulnerability. The affordable cost makes umbrella protection a prudent financial decision for any homeowner with meaningful assets to protect.

We at Secord Agency – A Trucordia Business help Washington homeowners navigate this decision with personalized guidance tailored to your coverage needs. Contact us for a quote and let our team review your current coverage to identify gaps and recommend appropriate umbrella limits for your situation.