Condo Insurance Washington: Protect Your Unit and Personal Property

Condo insurance in Washington protects more than just your unit-it covers your personal belongings and shields you from liability claims if someone gets injured on your property. Many condo owners mistakenly believe their HOA’s master policy covers everything, which leaves dangerous gaps in their protection.

We at Secord Agency – A Trucordia Business help condo owners understand exactly what they need to cover and how to find policies that fit their situation. This guide walks you through what condo insurance covers, how it differs from homeowners insurance, and how to select the right policy for your investment.

What Your Condo Insurance Actually Covers

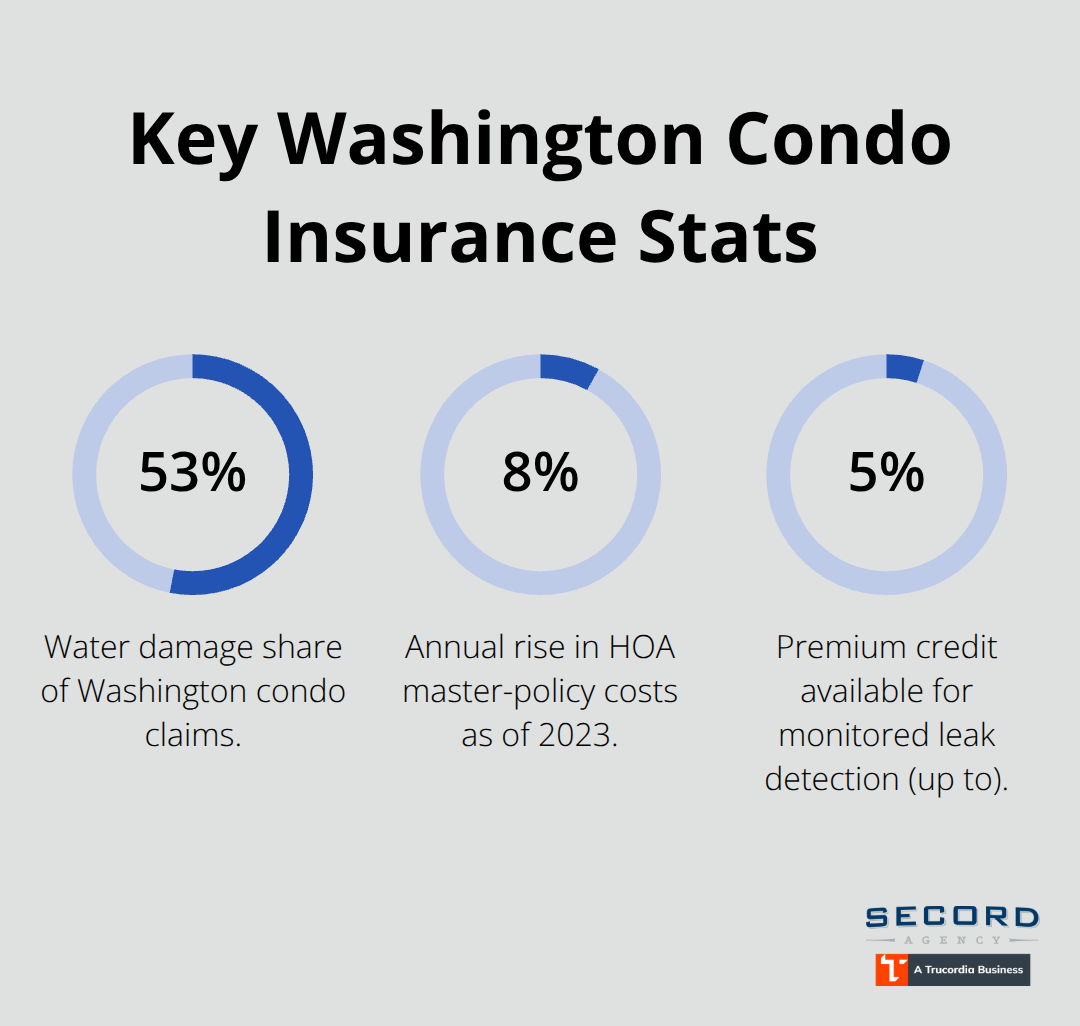

Your HO-6 condo policy covers the interior of your unit-the drywall inward-along with your personal belongings, liability exposure, and additional living expenses if you need temporary housing after a covered loss. Water damage accounts for roughly 53 percent of condo claims in Washington, making it the top loss driver, so understanding what your policy protects against matters far more than general reassurance. The master policy your HOA carries handles the building exterior, roof, common areas, and shared liability, but it stops at your unit’s walls.

This means you own everything inside: kitchen cabinets, bathroom fixtures, flooring, paint, and any upgrades you installed beyond what the builder originally provided. Many owners underestimate this responsibility and face thousands in out-of-pocket costs after a fire or water event.

Your Personal Property Needs Real Protection

Your HO-6 dwelling coverage rebuilds interior damage to your unit, while personal property coverage reimburses stolen or damaged belongings-furniture, electronics, clothing, and everything else you own. The catch is that standard policies typically pay actual cash value, meaning depreciation reduces what you receive; a five-year-old television worth $800 new might only net $300. If you own jewelry, art, or collectibles, request endorsements for replacement cost coverage and higher sublimits, since standard policies often cap jewelry at $1,500 to $2,500 total. Appraisals for items worth more than $5,000 protect you during claims and speed up settlements considerably when you provide copies to your agent. Your liability coverage, starting around $100,000 on most policies, protects you if someone is injured inside your unit and sues-a guest slips on your bathroom floor or your guest’s child sustains an injury. Medical payments coverage, typically $1,000 to $5,000, pays medical bills for injuries on your property regardless of fault, which often prevents lawsuits before they start. If you have significant assets, add an umbrella policy starting at $1 million; Washington average premises-liability settlements reached about $68,000 in 2022, according to state data, so higher limits make financial sense.

Loss Assessment Coverage Protects Against Special Assessments

Loss assessment coverage is the most overlooked protection in Washington condo ownership. When the HOA master policy’s limits are exceeded or claims exhaust reserves, the association bills unit owners for their share of the deductible or shortfall-sometimes $10,000 to $50,000 per unit. Your HO-6 loss assessment coverage, ideally set at $50,000 or higher, pays these special assessments so you aren’t wiped out by one catastrophic event. Additional living expense coverage pays your hotel, meals, and other costs if you must vacate during repairs after a covered loss; most policies include this but often set limits too low at $10,000 to $20,000. If you live in a building where major water damage could displace residents for weeks, request higher limits.

Coordinate with Your HOA to Avoid Coverage Gaps

Washington’s Washington Condominium Act requires associations to maintain master-policy coverage at no less than 80 percent of replacement cost, but this doesn’t mean your unit is fully covered-it protects the structure only. Coordinate with your HOA to obtain a copy of the master policy and the Certificate of Insurance issued at renewal; knowing the master deductible, coverage limits, and what’s included prevents dangerous assumptions. Your individual HO-6 policy fills the gaps that the master policy leaves, but only if you understand what those gaps actually are. The next section explains how condo insurance differs fundamentally from homeowners insurance and why this distinction shapes your coverage strategy.

How Condo Insurance Differs from Homeowners Insurance

The fundamental difference between condo insurance and homeowners insurance lies in what you actually own and what the HOA owns on your behalf. When you buy a house, you own the entire structure-roof, walls, foundation, everything. When you buy a condo, you own only the airspace inside your unit’s walls, while the HOA owns the building envelope, common areas, elevators, and shared systems. This ownership split means homeowners insurance covers the entire dwelling, while condo insurance covers only your interior and personal belongings. The HOA’s master policy handles the building structure and shared liability, but it deliberately excludes your unit’s interior improvements and your personal property.

What the Master Policy Actually Covers

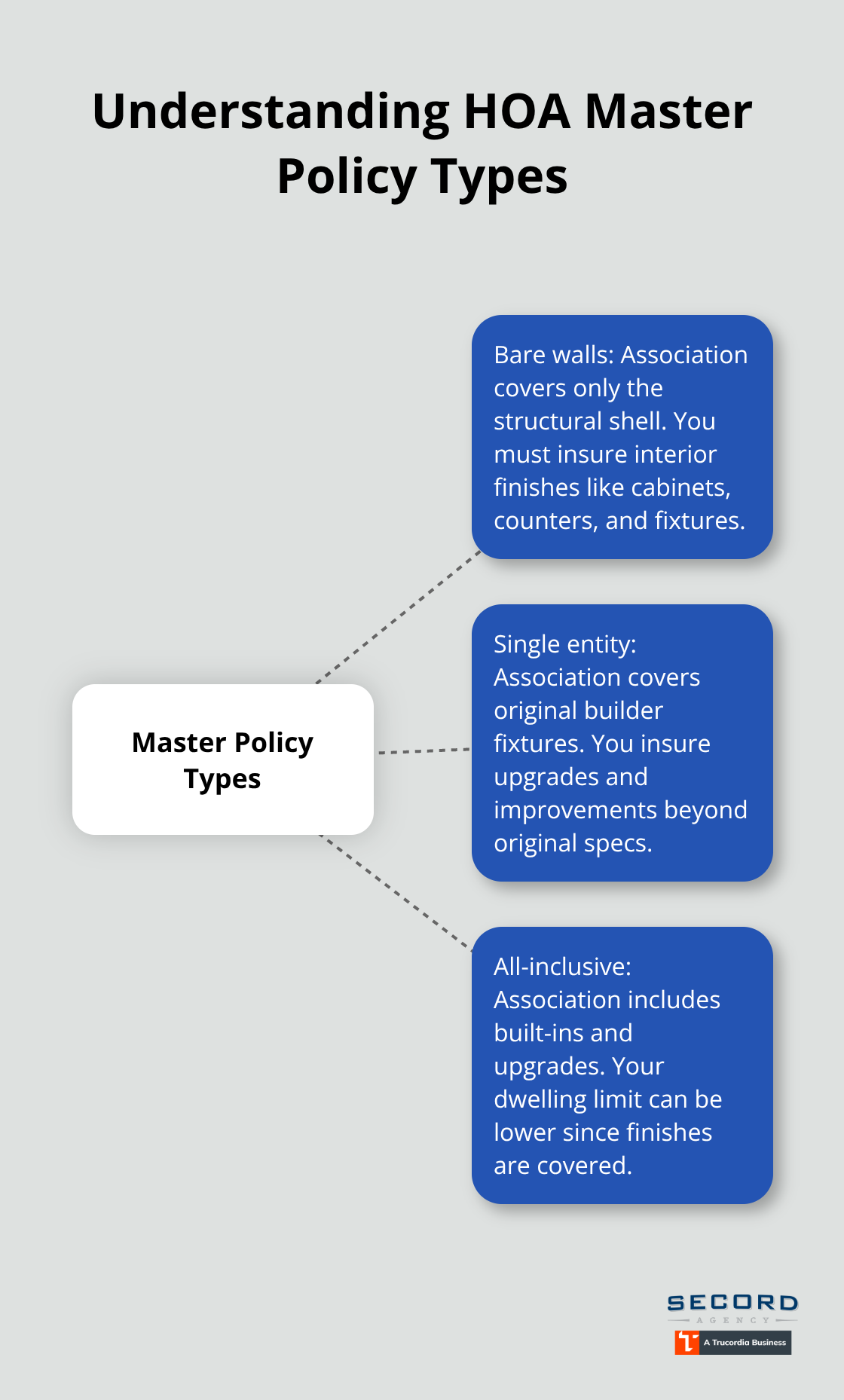

The HOA’s master policy covers the exterior and all interior finishes, such as doors, windows, siding, shower/tub, vanity/cabinets, paint, and baseboards/trim, but it deliberately excludes your unit’s interior improvements beyond original finishes and your personal property. A kitchen fire that damages your cabinets, countertops, and appliances falls on you, not the HOA. Water damage from a burst pipe in your walls becomes your responsibility if the master policy covers only the building’s structural elements. Washington’s master policies typically fall into three categories: bare walls (association covers only structural shell), single entity (association covers original builder fixtures), or all-inclusive (association covers built-in appliances and upgrades). Your dwelling coverage limit must match your master policy type-if you have a bare-walls policy, you need higher dwelling limits to cover kitchen and bathroom finishes; if all-inclusive, you need less.

Why Most Owners Underestimate Their Coverage Needs

Most condo owners never request a copy of the master policy from their HOA, which means they guess at what they need to insure. This guessing costs money through either over-insurance or, more dangerously, under-insurance that leaves massive gaps. Relying solely on the master policy leaves you catastrophically exposed because it protects the structure only, not your interior or belongings.

Cost Differences Reflect Your Reduced Risk

National data suggest condo premiums run two to three times lower than homeowners premiums because you insure far less property-no roof, no foundation, no exterior maintenance. However, Washington condo premiums have risen sharply since 2019, with master-policy costs climbing roughly 8 percent annually as of 2023. Your individual HO-6 policy typically costs $400 to $600 per year in Washington, though location, building age, and your claims history drive significant variation.

The Hidden Financial Risk: Loss Assessment Gaps

The real financial risk in condos comes from loss assessment coverage gaps and insufficient master-policy deductibles. If your HOA carries a $50,000 deductible on the master policy and a major claim exhausts reserves, the association bills each unit owner for their share-potentially $5,000 to $25,000 per unit depending on building size. Standard loss assessment coverage tops out at $1,000 to $5,000 on many policies, which covers almost nothing. Loss assessment limits of at least $50,000 for Washington condos add minimal premium cost but shield you from devastating special assessments. Your homeowners-insured neighbor pays one deductible; you potentially face two-your HO-6 deductible and your share of the master deductible if a claim affects common areas. This dual-deductible reality makes loss assessment coverage non-negotiable, not optional.

Understanding these differences shapes how you approach finding the right policy. The next section walks you through assessing your specific coverage needs and comparing quotes from multiple carriers to build protection that actually matches your situation.

Finding the Right Condo Insurance Policy for Washington

Gather Your Documents First

Start by collecting three documents before you request a single quote: your HOA’s master policy, the Certificate of Insurance issued at renewal, and your building’s governing documents or CC&Rs. These tell you exactly what the master policy covers, what deductible applies, and whether your building is bare walls, single entity, or all-inclusive. Without this information, any quote you receive is essentially a guess. Next, inventory your personal property-furniture, electronics, clothing, jewelry, art-and calculate what it would cost to replace everything at today’s prices, not what you paid years ago. Most owners underestimate this figure by 30 to 50 percent because items in closets, storage, and less-visible areas slip from memory. A detailed inventory also speeds claims processing dramatically if you ever need to file one.

Calculate Your Dwelling and Liability Limits

Your dwelling coverage amount depends entirely on your master policy type; bare-walls policies require higher dwelling limits because you cover kitchen and bathroom finishes, while all-inclusive policies mean lower limits since the association already covers those items. Request quotes with multiple dwelling amounts-typically $25,000 to $100,000 depending on your unit size and finishes-and loss assessment coverage starting at $50,000 minimum. Liability coverage should match your assets; if you have $500,000 in savings and investments, $100,000 in liability leaves you vulnerable, so request $300,000 to $500,000 as a baseline, then add a $1 million umbrella policy if you have significant net worth.

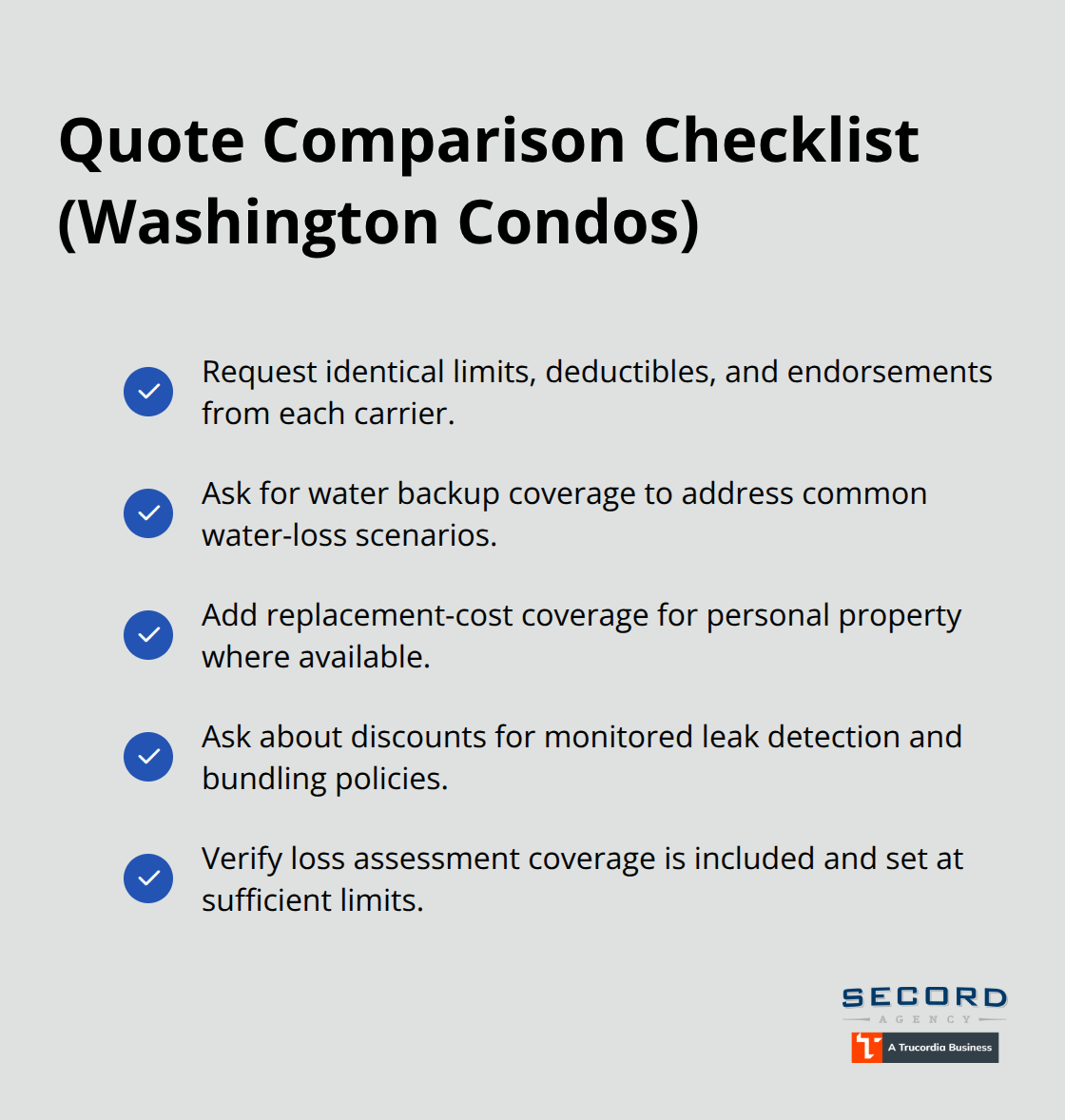

Compare Quotes from Multiple Carriers

Comparing quotes requires more than price alone. Contact at least three carriers and request identical coverage limits, deductibles, and endorsements so you can actually compare apples to apples. Major insurers offering condo policies in Washington include Allstate, Amica, Chubb, Farmers, Liberty Mutual, Nationwide, State Farm, Travelers, and USAA, though availability varies by zip code and building characteristics. Ask each carrier specifically about water backup coverage, replacement-cost endorsements for personal property, and any discounts for bundling auto or installing leak-detection systems-insurers offer up to 5 percent premium credits for monitored leak detection, which also reduces water damage claims. When you receive quotes, verify that loss assessment coverage is included and at sufficient limits; many standard quotes default to $1,000 to $5,000, which is dangerously low.

Work with an Independent Agent

An independent agent who represents multiple carriers rather than one company can shop options and identify the best combination of price, coverage, and service for your specific situation. An independent agent also reviews your master policy alongside your HO-6 to spot coordination gaps that most owners miss entirely. Request a free policy review before you commit; a quality agent invests 30 to 45 minutes understanding your building, your unit’s upgrades, and your assets before recommending coverage. Once you select a policy, review it annually or whenever your master policy renews, since changes to HOA coverage or deductibles should trigger adjustments to your personal limits.

Final Thoughts

Protecting your condo investment in Washington requires understanding what your HOA’s master policy covers and what gaps your personal HO-6 policy must fill. The master policy protects the building structure and common areas, but it deliberately excludes your unit’s interior, personal belongings, and your individual liability exposure. Water damage claims, which account for 53 percent of condo losses in Washington, underscore why comprehensive personal property coverage matters far more than general reassurance.

Your action plan starts with three concrete steps: request your HOA’s master policy and Certificate of Insurance from your property manager, inventory your personal belongings at replacement cost, and secure loss assessment coverage of at least $50,000 to shield yourself from special assessments when master-policy deductibles are triggered. These steps take a few hours but prevent thousands in unexpected costs after a loss. When you shop for condo insurance Washington coverage, compare quotes from multiple carriers using identical limits and endorsements so you can actually compare prices fairly.

Request water backup coverage, replacement-cost endorsements for high-value items, and any available discounts for leak-detection systems or bundled policies. An independent agent who represents multiple carriers can review your master policy alongside your personal coverage to spot coordination gaps that most owners miss. Contact us at Secord Agency – A Trucordia Business for a free policy review to ensure your condo insurance protection matches your actual situation and assets.