Seattle Auto Insurance Quotes: Get Fast Local Estimates

Getting Seattle auto insurance quotes shouldn’t mean spending hours comparing dozens of options. The right coverage at the right price depends on understanding what insurers actually look at and knowing which discounts apply to your situation.

At Secord Agency – A Trucordia Business, we help drivers cut through the noise and find policies that match their needs and budget. This guide walks you through the quote process, shows you how to spot real savings, and explains why local expertise matters.

How Seattle Auto Insurance Quotes Really Work

Coverage Types Define What You’re Buying

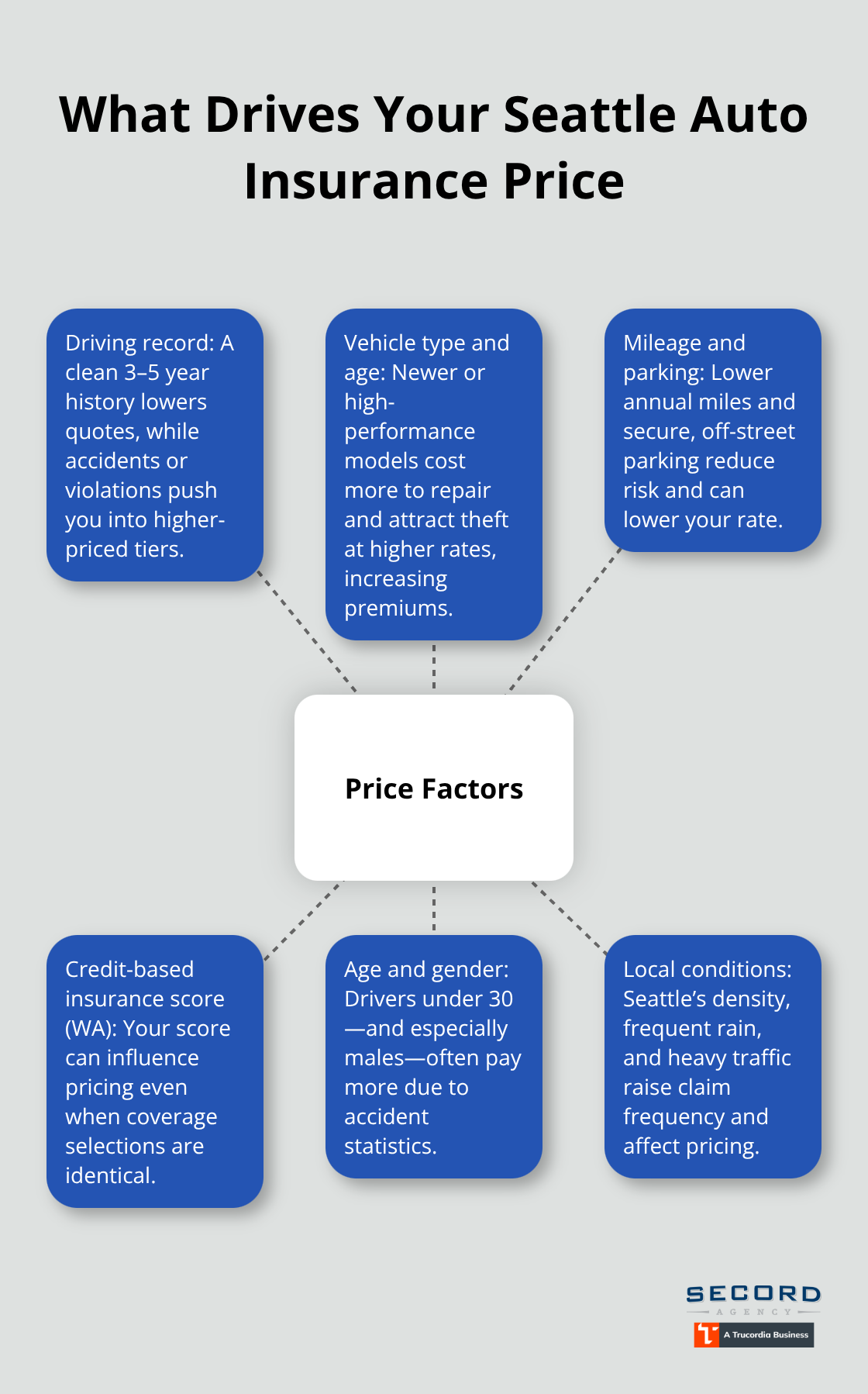

Seattle auto insurance quotes reflect three core elements insurers measure, and understanding each one helps you anticipate what your quote will show. First, coverage types define what you actually purchase. Washington requires minimum liability limits of $25,000 per person and $50,000 per accident for bodily injury, plus $10,000 for property damage. However, these minimums leave you exposed after a serious accident. Most drivers need higher limits, and then you layer on optional coverage like collision, comprehensive, medical payments, and uninsured motorist protection. Each coverage type carries its own limit and deductible, and changing either one shifts your quote immediately. When you request a quote online, insurers ask about these coverage choices because liability alone does not protect your vehicle if you cause an accident or hit an uninsured driver.

Risk Factors That Shape Your Price

The second element is the risk factors unique to your situation. Seattle’s urban density, frequent rain, and dense traffic create higher claim frequency, which insurers price accordingly. Your driving record matters intensely; a clean history over the last 3 to 5 years produces meaningfully lower quotes than one with accidents or violations. Vehicle type and age heavily influence cost too, since newer high-performance cars cost far more to repair and attract theft at higher rates. Your annual mileage, where you park, and even your credit-based insurance score in Washington all feed into the calculation. Younger drivers under 30 pay substantially higher rates due to accident statistics, and males in that age group typically pay more than females. When you shop quotes, provide identical information across carriers to ensure you compare apples to apples, not differences caused by missing details.

Local Agents Uncover What Online Tools Miss

The third element separates fast local estimates from generic online results. Online quote tools deliver speed, often producing estimates within minutes across multiple carriers. However, online systems apply standardized pricing without context for Seattle-specific discounts or your personal circumstances. A local agent shops multiple carriers and identifies discounts you might miss alone, such as bundling auto with home or renters insurance, telematics programs that monitor safe driving, good student status, and safety features like anti-lock brakes or anti-theft devices. Local agents also explain what each quote actually covers and catch hidden fees or exclusions before you commit. They know which insurers handle claims fastest in the Seattle area and which ones excel at customer service, information you will not find in an online quote form. If you drive for rideshare services, a local agent flags coverage gaps and endorsements you need. Raising your deductible from $500 to $1,000 lowers your premium, but an agent helps you understand whether you can actually cover that deductible if a claim happens. Shopping every 6 to 12 months captures rate changes and new discounts, and a local agent reminds you when it is time to review. Online quotes give you a starting point; local expertise transforms that into a decision you can actually stand behind.

What Really Matters When Comparing Quotes

Standardize Coverage Before You Compare Prices

Most drivers compare auto insurance quotes by staring at the monthly premium number, which is exactly backward. The premium is the last thing to evaluate, not the first. Start instead by confirming that each quote covers the same liability limits, deductibles, and optional coverages across all carriers. If one quote shows $25,000 bodily injury liability and another shows $100,000, the prices are meaningless until you standardize them.

Washington’s minimum is $25,000 per person and $50,000 per accident for bodily injury plus $10,000 for property damage, but these minimums are dangerously low. Most drivers need at least $100,000 per person and $300,000 per accident, with higher limits if you have significant assets. When you request quotes, specify identical coverage across all carriers: the same liability limits, the same deductible amounts for collision and comprehensive, and the same optional coverages like uninsured motorist protection and medical payments.

Online quote tools often default to different settings, so this takes discipline. It is the only way to compare fairly. Most carriers deliver quotes within minutes online, so there is no excuse for shopping only one or two options. Get quotes from at least three to five major insurers.

Check Complaint Data and Claims Performance

Next, look at what discounts each quote actually includes. The Washington Office of the Insurance Commissioner publishes complaint data for each insurer, and you can check which carriers have fewer complaints relative to their market share. J.D. Power and Consumer Reports both rank insurers on customer satisfaction and claims handling speed, which matters far more than saving $20 a month with a company that takes three months to pay a claim.

Rates in Washington vary widely across carriers for identical drivers and vehicles. This variation means your shopping effort directly translates to real savings. A carrier with strong claims performance in the Seattle area may cost slightly more upfront but pays claims faster and with less friction when you actually need them.

Calculate Total Annual Cost, Not Monthly Payment

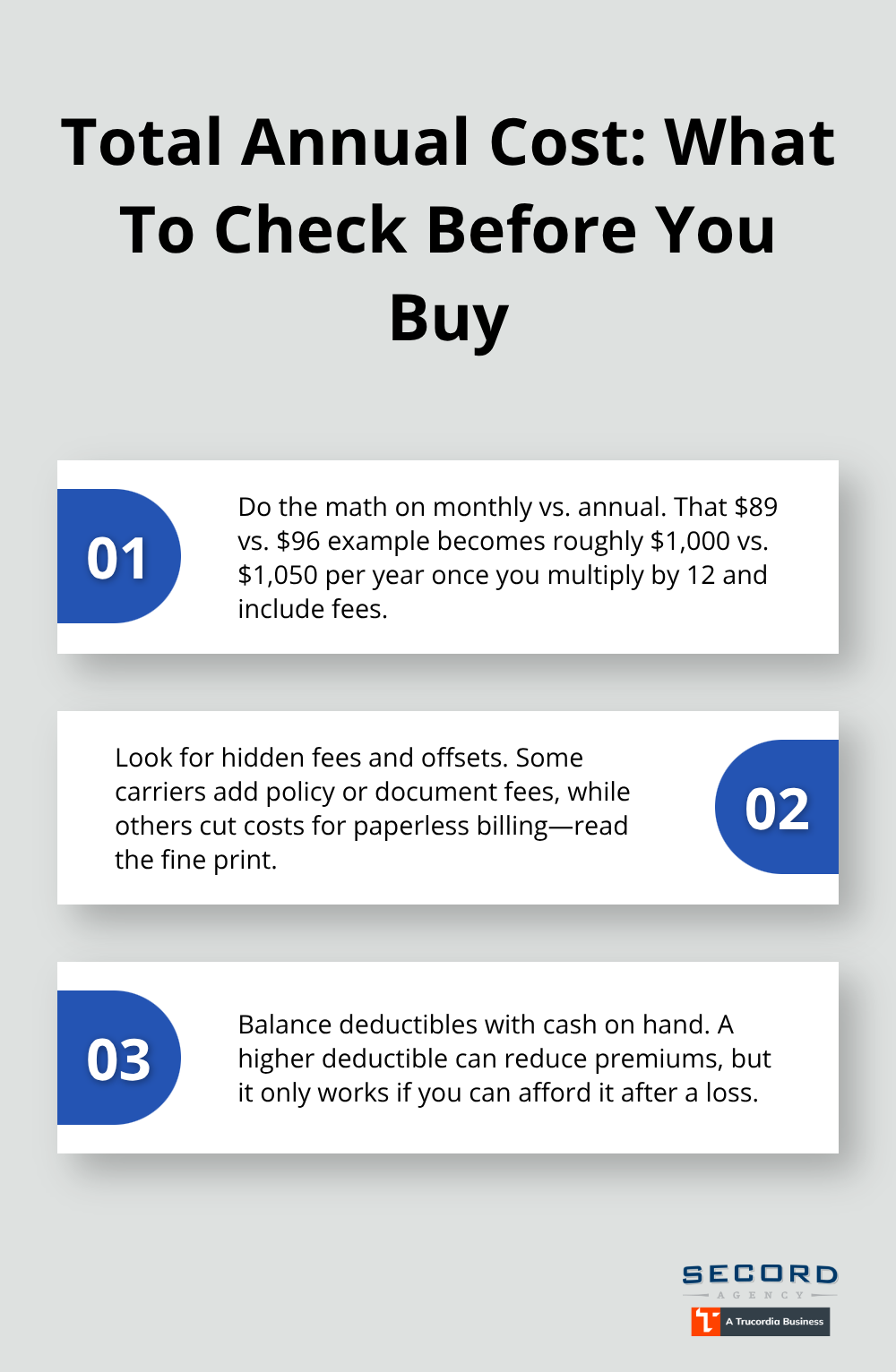

The biggest mistake drivers make is ignoring the total annual cost and fixating on the monthly payment. A quote showing $89 per month sounds better than $96 per month, but if you multiply by 12 months and add all fees and surcharges, the actual difference might be $1,000 versus $1,050 annually. Always confirm the total cost before comparing.

Hidden fees appear in different places: some insurers charge policy fees, some charge document delivery fees, and some add surcharges for electronic payment or paperless billing. A few carriers actually reduce your premium for going paperless, so read the fine print carefully. Deductibles hide enormous cost differences too. Raising your deductible from $500 to $1,000 typically lowers your annual premium by 10 to 15 percent, but only if you can actually afford to pay $1,000 out of pocket when a claim happens.

If you cannot cover that deductible, choosing it to save money creates a false economy.

Stack Discounts to Uncover Real Savings

Discounts are where most drivers leave money on the table. Bundling auto with home or renters insurance saves 15 to 25 percent at many carriers. Telematics programs that track safe driving through your phone can reduce premiums by 10 to 30 percent depending on the carrier. Good student discounts, safety feature discounts for anti-lock brakes or anti-theft devices, and low-mileage discounts all stack up, but you must ask about them explicitly because quote tools do not always apply them automatically.

Some carriers offer these discounts only if you call an agent rather than buying online. An independent agent shops multiple carriers and identifies every discount you qualify for, which often saves more time and money than shopping around alone. This approach transforms a quote from a static number into a tailored policy that reflects your actual situation and eligibility.

Maximize Savings Through Discounts and Smart Choices

Stack Discounts to Cut Your Premium

Discounts represent where most Seattle drivers leave substantial money on the table, and carriers do not advertise all of them equally. Bundling auto with home or renters insurance saves 15 to 25 percent at many carriers according to the National Association of Insurance Commissioners, which represents one of the largest savings opportunities available. Telematics programs that monitor safe driving through your phone can reduce premiums by 10 to 30 percent depending on the carrier, though you must opt in and allow data collection. Good student discounts apply if you maintain a 3.0 GPA or higher, safety feature discounts reward vehicles with anti-lock brakes or anti-theft devices, and low-mileage discounts help drivers who commute less than 7,500 miles annually. Online quote tools frequently fail to apply these discounts automatically, so you must ask about them directly when comparing carriers.

An independent agent shops multiple insurers simultaneously and identifies every discount you qualify for, which typically saves more time and money than requesting quotes alone. This approach transforms a quote from a static number into a tailored policy that reflects your actual situation and eligibility.

Age and Gender Impact Your Base Rate

Drivers under 30 pay substantially higher rates due to accident statistics, with males in that age group paying approximately 15 to 20 percent more than females for identical coverage. This age-based pricing is not negotiable, but maximizing discounts becomes even more critical when your base rate is already elevated. The higher your starting premium, the more valuable each discount percentage becomes in absolute dollar terms.

Your Driving Record Determines Your Tier

Your driving record and vehicle type shape your quote far more than most drivers realize, and these factors determine whether you qualify for the lowest tier pricing at each carrier. A clean driving history over the last 3 to 5 years produces meaningfully lower quotes than records with accidents or violations, while a single at-fault accident can raise your premium by 20 to 40 percent depending on the carrier. Vehicle age, make, and model matter intensely because newer high-performance cars cost far more to repair and experience higher theft rates, which drives up premiums substantially.

Make Smart Choices Before You Buy

Before purchasing a car, request quotes from multiple insurers on that specific model and check Consumer Reports for its accident and theft rates. This step prevents the costly mistake of buying a vehicle that costs far more to insure than you anticipated. A modest sedan typically costs 30 to 50 percent less to insure than a sports car, and that difference compounds over years of ownership.

Review Your Policy Annually

Review your policy every 6 to 12 months because rates change annually and new discounts emerge regularly. When your circumstances shift-you move, reduce your annual mileage, or complete a defensive driving course-contact your agent immediately because these changes often produce savings you did not anticipate. Secord Agency, a Trucordia business based in Seattle’s Wallingford neighborhood, helps clients review policies annually and catch rate changes or new discounts before renewal dates arrive, which prevents the costly mistake of paying outdated premiums for months longer than necessary.

Final Thoughts

Getting Seattle auto insurance quotes fast means understanding what insurers measure, comparing coverage standardized across carriers, and stacking every discount available to your situation. The process takes discipline but saves hundreds or thousands annually. Start by requesting quotes from at least three to five major carriers with identical coverage limits and deductibles, then check complaint data and claims performance before fixating on the monthly premium.

Working with a local Seattle insurance agency transforms this process from a frustrating solo effort into a partnership with someone who knows your market and your options. An independent agent shops multiple carriers simultaneously, identifies discounts you would miss alone, explains what each quote actually covers, and catches hidden fees before you commit. They know which insurers handle claims fastest in the Seattle area and which ones excel at customer service (information you will not find in an online quote form).

We at Secord Agency – A Trucordia Business help Seattle drivers cut through the noise and find policies that match their needs and budget. Contact us today to get your Seattle auto insurance quotes and discover how much you can actually save with the right coverage and the right partner.