Flood Insurance Homeowners Washington: A Practical Guide to Coverage

Floods cause more property damage than any other natural disaster in the United States, yet most homeowners don’t realize their standard insurance won’t cover it. If you live in Washington, understanding flood insurance for homeowners is essential-especially since the state experiences significant flooding in certain regions.

We at Secord Agency – A Trucordia Business help homeowners navigate these coverage gaps. This guide walks you through your options and shows you exactly how to protect your home.

Why Your Standard Homeowners Policy Won’t Protect Your Home From Floods

Standard Policies Explicitly Exclude Flood Damage

Standard homeowners insurance policies contain explicit flood exclusions, which means your insurer will deny any claim related to flood damage-no matter how catastrophic the loss. This isn’t a loophole or a misunderstanding; it’s written directly into the policy language. The distinction matters because floods are defined specifically as overflow from bodies of water, heavy rainfall, dam failures, or rapid snowmelt. Water that backs up through your sewers, leaks from your plumbing, or seeps through your basement walls from ground saturation doesn’t technically qualify as flood damage under standard policies, though these scenarios often occur during flood events and cause similar destruction.

The Federal Government Created NFIP Because Private Insurers Refused

Washington homeowners must purchase separate flood insurance to close this gap, and the National Flood Insurance Program (NFIP) exists precisely because private insurers refused to offer flood coverage at any price. The federal government created NFIP in 1968 when private insurance companies simply would not underwrite flood risk. NFIP policies are available through licensed agents across Washington and offer two distinct coverage types: building coverage protects your home’s structure and foundation along with permanently installed systems like electrical wiring, plumbing, HVAC equipment, and built-in appliances, while contents coverage protects your personal belongings such as furniture, clothing, electronics, and portable appliances.

How NFIP Rates Work in Washington

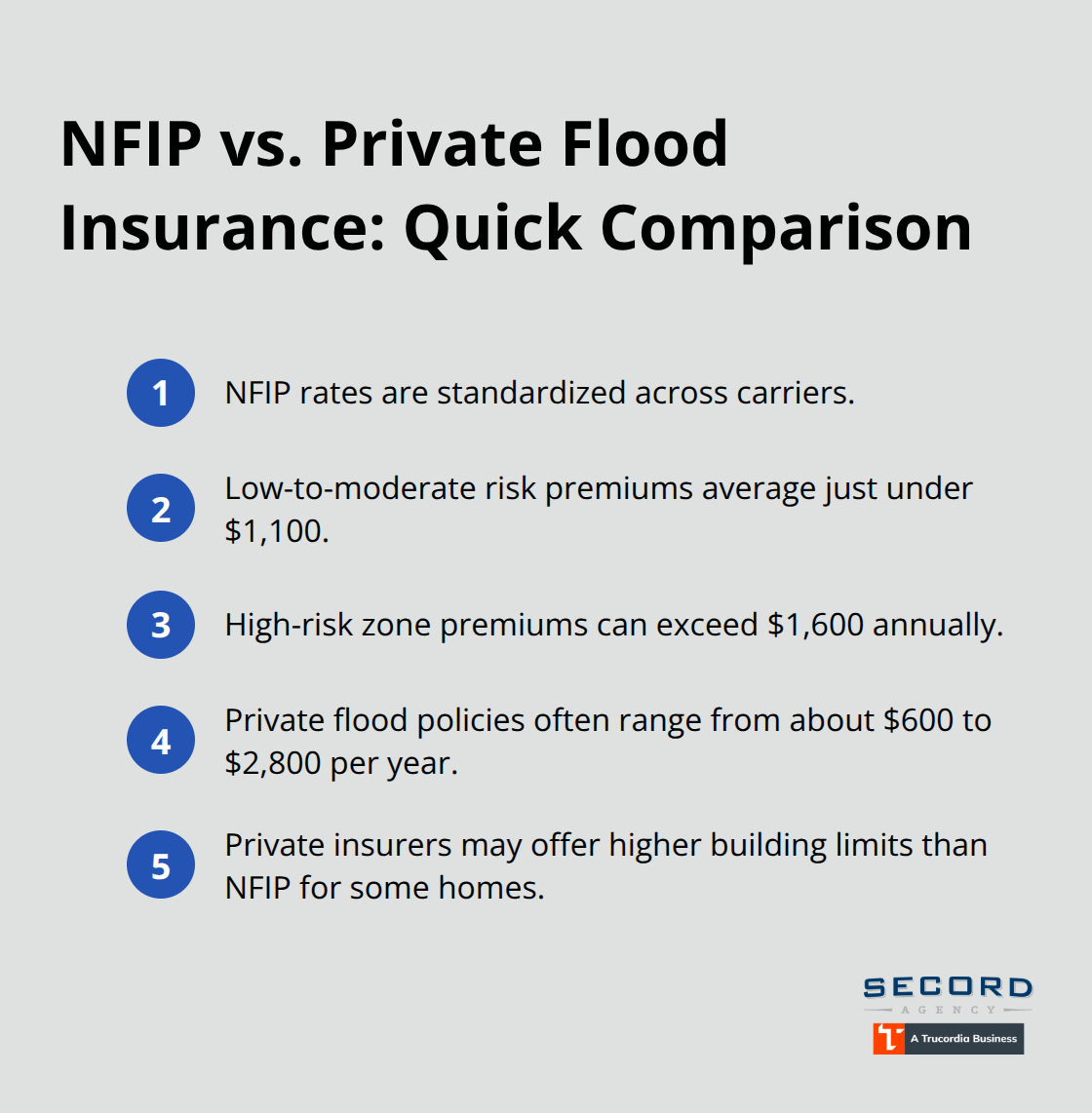

Rates are standardized across all carriers, meaning you won’t find cheaper NFIP premiums by shopping around-the price depends entirely on your flood zone designation and replacement cost. In low to moderate risk areas, annual NFIP premiums average just under $1,100, but homes in high-risk zones can exceed $1,600 yearly. Washington’s flood risk extends beyond obvious coastal areas; nearly one-third of all NFIP claims nationwide from 2014 to 2024 came from properties outside officially designated high-risk zones, demonstrating that flooding threatens homes across the state regardless of their perceived vulnerability.

Private Flood Insurance Offers Another Path

Private flood insurance has emerged as an alternative for some homeowners, typically costing between $600 and $2,800 annually depending on coverage limits and property specifics. These policies can offer higher building limits than NFIP’s $500,000 cap for commercial properties, though residential limits vary by insurer. Understanding your flood zone and comparing both NFIP and private options will help you determine which coverage best fits your Washington home’s specific risk profile and budget.

What Coverage Do You Actually Get From NFIP and Private Flood Insurance

Building and Contents Coverage Explained

NFIP building coverage protects your home’s structure, foundation, electrical systems, plumbing, HVAC equipment, water heaters, and permanently installed appliances like refrigerators and stoves. Contents coverage shields personal belongings including furniture, clothing, electronics, and portable appliances. The critical limitation: NFIP caps building coverage at $250,000 for residential properties and contents at $100,000, which falls short for many Washington homes. If your home’s replacement cost exceeds these limits, you’ll face an uninsured gap. Private flood policies typically offer higher limits, and some insurers provide building limits exceeding $500,000. However, private policies come with varied terms and conditions, so comparing specific coverage details matters more than chasing the lowest price.

What NFIP and Private Policies Don’t Cover

Neither NFIP nor private flood insurance covers vehicle damage-you need comprehensive auto coverage for that protection. Both exclude mold and mildew damage unless you purchase specific endorsements, a common oversight that leaves homeowners exposed after water intrusion occurs. This gap means you should review your policy language carefully and ask your agent whether endorsements make sense for your situation.

How Your Deductible Affects Your Costs

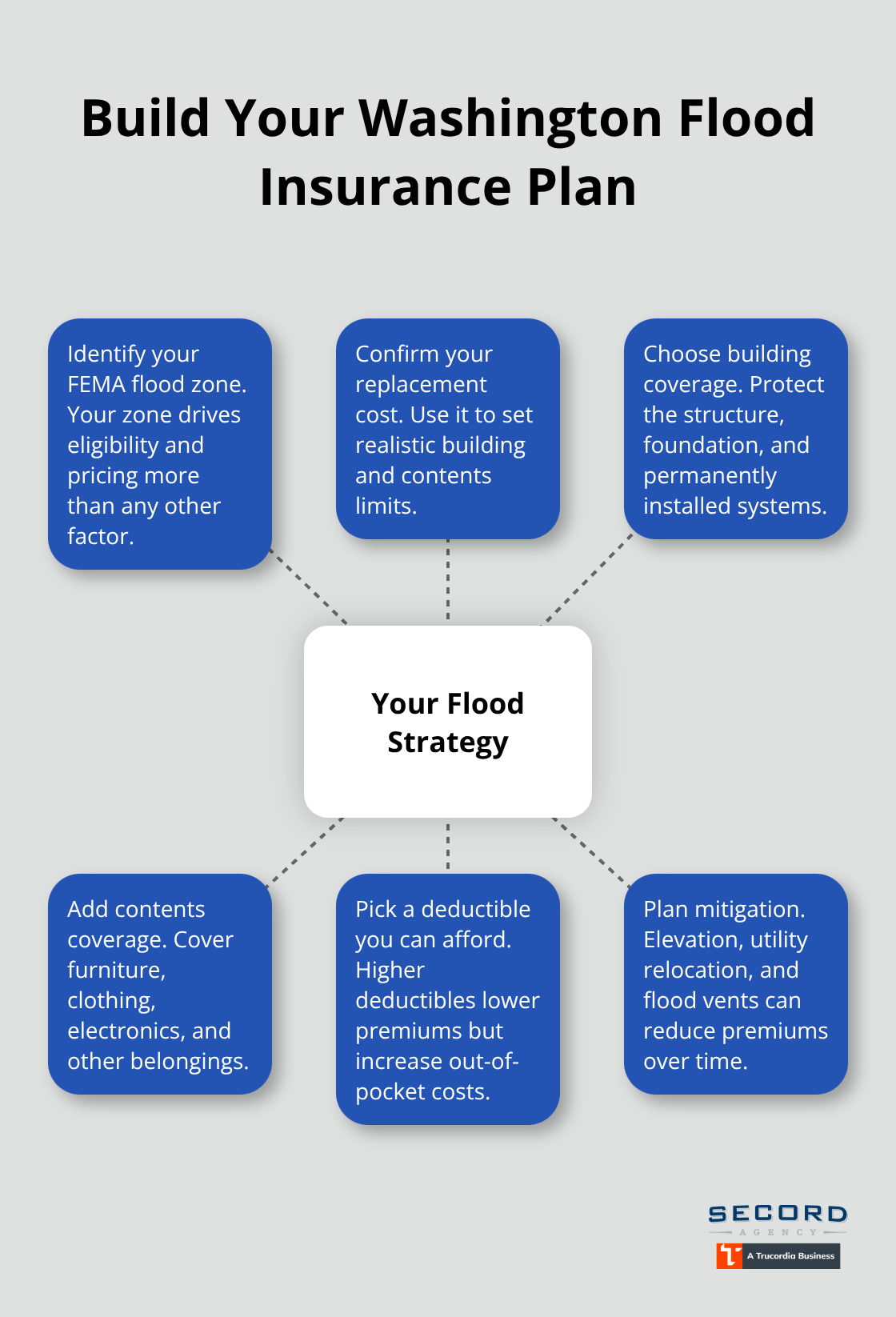

Your deductible choice directly impacts your out-of-pocket costs after a flood. NFIP offers deductible options of $1,000, $2,500, $5,000, or $10,000; selecting a higher deductible lowers your annual premium, sometimes by hundreds of dollars. NFIP policies cost just over $1,100 per year on average, and you could reduce that with a higher deductible. The trade-off requires honest assessment: if you have emergency savings exceeding your deductible, a higher deductible makes financial sense. If unexpected expenses would strain your finances, the lower premium isn’t worth the risk. Private insurers offer similar flexibility, and some allow deductibles as low as $500. One actionable step: use the NFIP’s quote tool to run scenarios with different deductibles and compare total five-year costs, not just annual premiums.

Elevation Reduces Your Premiums Substantially

Building elevation-raising your home’s lowest floor above the base flood elevation-reduces premiums substantially. FEMA data shows each foot of elevation can lower your premium by hundreds of dollars annually, making elevation certificates valuable investments if you’re considering this mitigation strategy. Homeowners who elevate utilities (HVAC and electrical panels) or install flood vents also qualify for premium reductions. These physical improvements transform your property’s flood risk profile and can pay for themselves through premium savings over time.

Next Steps: Comparing Your Options

The combination of coverage limits, deductibles, and mitigation steps creates multiple pathways to protect your Washington property. Your specific risk level, home value, and financial situation determine which approach works best. We at Secord Agency – A Trucordia Business shop multiple carriers to help you identify coverage that matches both your needs and budget, then guide you through the application process. Understanding these coverage options positions you to make informed decisions before you need to file a claim.

Getting Flood Insurance in Washington

Identify Your Flood Zone First

Your flood zone determines everything about your coverage and cost. Washington has designated flood zones mapped by FEMA flood zone maps, and your property falls into one of these categories: high-risk areas (Special Flood Hazard Areas where lenders require flood insurance), moderate-risk zones, or low-risk areas. Use NFIP’s interactive “What is My Flood Zone?” map to find your specific designation, or contact a local agent who can pull this information immediately. Your flood zone drives your premium more than any other factor-a home in a high-risk coastal area will cost significantly more than an identical property in a low-risk zone.

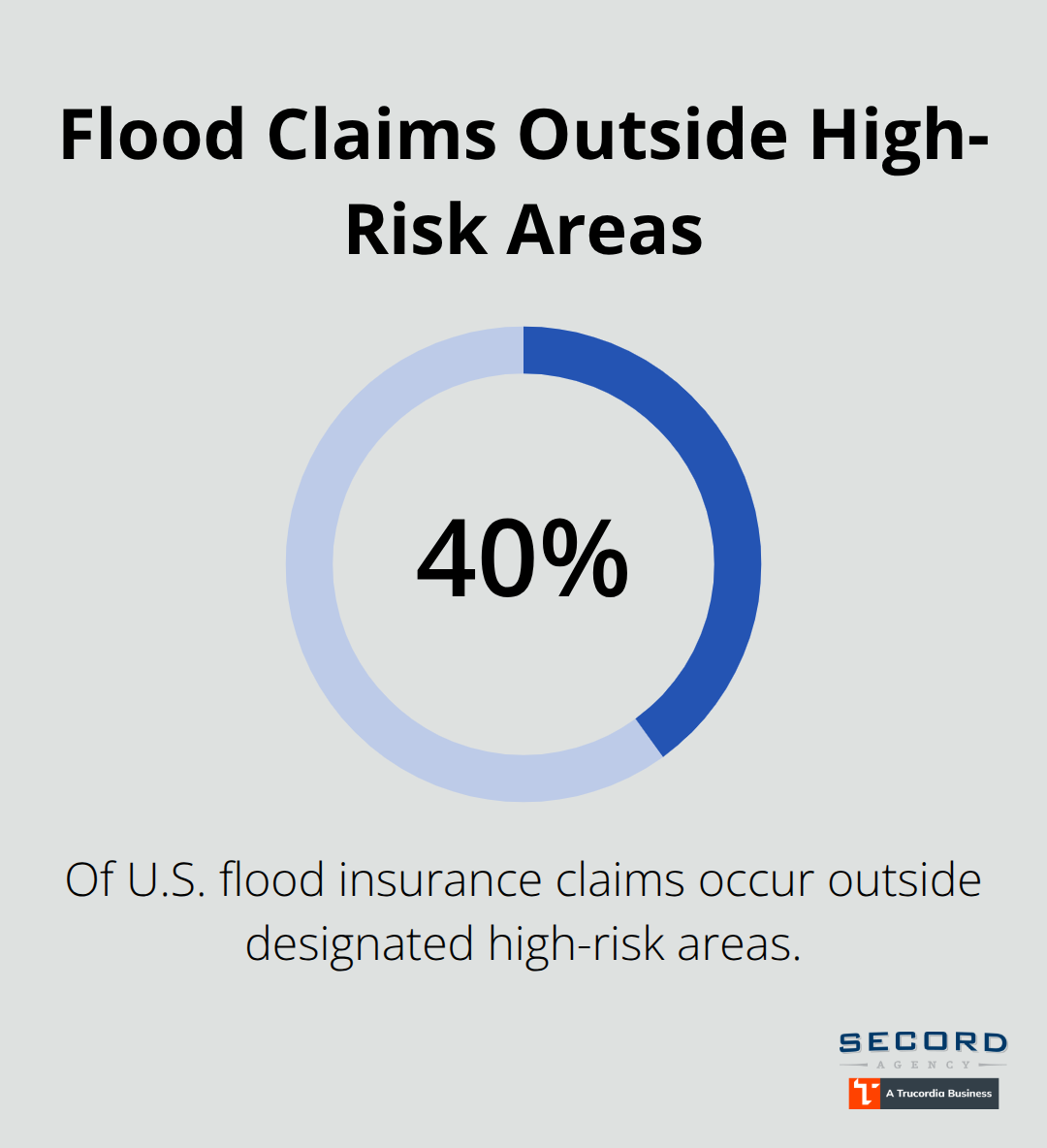

Washington’s geography creates pockets of serious flood exposure. The state experienced notable flooding events in December that left many renters and homeowners scrambling because they lacked adequate coverage. Don’t assume your location is safe just because it hasn’t flooded recently-nearly 40% of flood insurance claims nationally occur outside designated high-risk areas, meaning your Washington neighborhood could face unexpected water damage regardless of historical patterns.

Gather Your Home Information and Coverage Needs

Once you know your zone, collect your home’s replacement cost estimate and decide whether you need building coverage, contents coverage, or both. Building coverage protects your structure and permanently installed systems, while contents coverage shields your personal belongings. This foundation makes everything that follows straightforward.

Your replacement cost estimate helps you select appropriate limits that actually match your property’s value, preventing underinsurance that could leave you exposed after a flood event.

Compare NFIP and Private Flood Insurance Options

Finding the right carrier requires comparing both NFIP options and private flood insurance since they offer different advantages. Washington has approximately 50 NFIP-participating insurers, so you’ll have genuine choices even within the federal program-use the NFIP’s “Find a Flood Insurance Provider” tool to see carriers operating in your area. Because NFIP rates are standardized, you won’t save money by shopping rates, but private insurers do compete aggressively on price and coverage limits.

Request quotes from at least three carriers and specifically ask whether each offers the endorsements you need (mold coverage and sewer backup protection are common gaps). When you compare policies, look beyond the annual premium and examine what each policy actually covers. Private policies sometimes offer higher limits than NFIP’s $250,000 building cap for residential properties, which matters if your home’s replacement cost exceeds that threshold.

Document Damage and File Your Claim Properly

When a flood occurs, act immediately-contact your insurer before making permanent repairs, document all damage with photos and video, and avoid discarding damaged items until your adjuster assesses them. Photograph high-water marks on walls, list all damaged items with descriptions, and save receipts for any temporary repairs or emergency supplies you purchase.

File your proof of loss within 60 days for commercial properties and follow your policy’s timeline for residential claims. If your insurer denies or underpays your claim, you have the right to appeal and can request advances for urgent recovery needs while the full claim processes. Your adjuster will assess the damage and determine what your policy covers, but you control the documentation that supports your claim’s value.

Final Thoughts

Flood insurance for homeowners in Washington isn’t optional if you want genuine financial protection. Standard homeowners policies won’t cover flood damage, and waiting until after a flood event to purchase coverage leaves you completely exposed. The average NFIP claim from 2020 to 2024 exceeded $82,000, and just one inch of floodwater causes roughly $25,000 in damage-these represent real losses that devastate unprepared homeowners across Washington.

Acting now delivers concrete advantages over waiting. Your flood insurance homeowners Washington premium depends on your flood zone and replacement cost, not on when you purchase the policy, but NFIP policies typically begin coverage 30 days after purchase (surplus line policies start immediately). Homeowners who implement elevation improvements can reduce premiums by hundreds of dollars annually, and these mitigation steps take time to plan and execute. Starting now means you’ll benefit from premium reductions sooner rather than later.

Your next step is identifying your specific flood zone using FEMA’s interactive maps, then contacting an agent who can explain your coverage options. We at Secord Agency – A Trucordia Business shop multiple carriers to help you find flood insurance that matches your actual risk and budget, and our team handles the comparison work so you can make informed decisions without getting lost in policy language. Contact us today to discuss your flood protection strategy.