Washington Personal Umbrella Coverage: Do You Have Adequate Protection?

A single lawsuit or accident can wipe out years of financial progress. Most homeowners and car owners in Washington rely on standard insurance policies that simply don’t provide enough protection when liability claims exceed those limits.

Washington personal umbrella coverage fills that gap. At Secord Agency – A Trucordia Business, we help residents understand whether their current protection is actually adequate for their situation.

How Umbrella Coverage Actually Works

Personal umbrella insurance sits directly on top of your existing auto and homeowners policies, activating only after those underlying limits are exhausted. This is not a replacement policy-it’s an additional layer of protection. You must maintain active homeowners and auto coverage to qualify, and in Washington, insurers typically require minimum underlying limits of $300,000 on homeowners liability and $250,000 per person on auto bodily injury. The moment your base policy pays out its maximum, the umbrella kicks in and covers the remaining damages plus legal defense costs.

The Mechanics of Coverage Activation

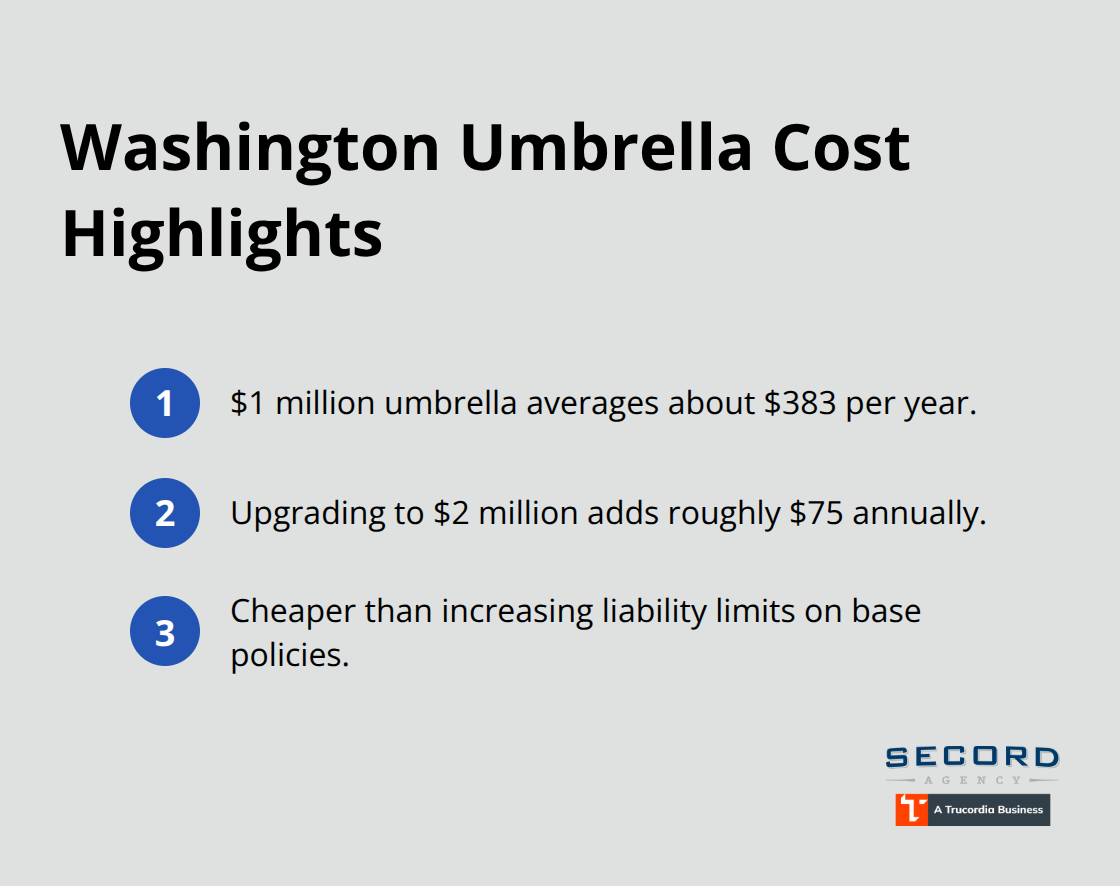

A multi-car accident illustrates how this works in practice. You cause a collision with $1.2 million in total damages. Your auto policy covers $500,000. Your umbrella policy then covers the remaining $700,000 plus attorney fees and court expenses. This structure makes umbrella coverage far more affordable than simply raising liability limits on your base policies. A typical $1 million umbrella policy in Washington costs around $383 per year according to ACE Private Risk Services data. Upgrading from $1 million to $2 million adds roughly $75 annually according to Money.com pricing data.

Coverage Limits and Geographic Scope

Washington umbrella policies typically start at $1 million and extend up to $5 million or higher depending on your risk profile and net worth. The coverage applies worldwide with no geographic restrictions, protecting you whether the incident happens in Seattle, rural Washington, or abroad. This global protection matters for residents who travel frequently or maintain property outside the state.

What Umbrella Policies Actually Cover

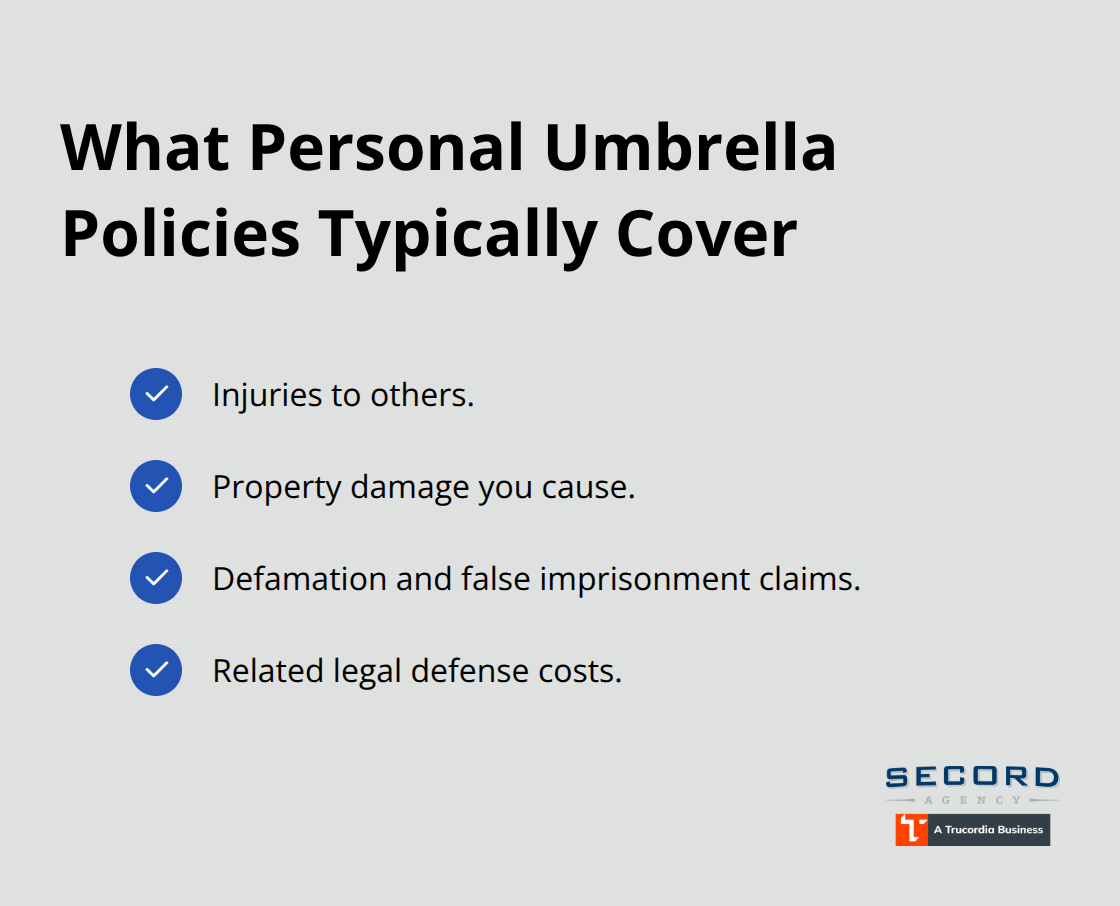

Umbrella policies cover injuries to others, property damage caused by you, defamation claims, false imprisonment, and related legal expenses-essentially any liability claim that exceeds your underlying policy limits. However, umbrella coverage explicitly excludes your own medical bills, damage to your own property, intentional criminal acts, and business liabilities unless you carry a commercial umbrella policy.

Real Washington Verdicts Show the Need

Washington verdicts and settlements illustrate why this protection matters. A 2023 wrongful death settlement reached $3.7 million. A 2022 pedestrian injury verdict totaled $1.85 million. A 2021 birth-injury case resulted in a $6 million verdict. These are not hypothetical scenarios-they represent actual Washington cases where victims received substantial awards that far exceeded standard policy limits. Understanding your actual exposure to these kinds of claims helps you determine whether your current coverage leaves you vulnerable.

Why Your Standard Policies Leave You Exposed

Washington liability claims regularly exceed what standard homeowners and auto policies cover. The 2021 Washington Medical Malpractice Annual Report documents total plaintiff compensation of $151 million across 120 claims, with average settlements around $1.3 million and verdicts averaging $730,000. Beyond medical malpractice, auto accidents involving pedestrians and cyclists generate substantial awards. A 2022 pedestrian injury verdict reached $1.85 million for injuries including concussion and brain contusions. A 2021 birth-injury case produced a $6 million verdict due to airway injuries and prolonged hospitalization. These figures represent actual Washington cases, not hypothetical scenarios.

Most homeowners carry $300,000 to $500,000 in underlying liability coverage. Most drivers carry $250,000 per person in bodily injury limits. When a single claim reaches $800,000 or $1.2 million, your base policies stop paying immediately, and you become personally responsible for the remaining balance. Washington does not cap damages in personal injury or medical malpractice cases, meaning awards can grow substantially larger than your policy limits.

Who Faces the Highest Liability Risk

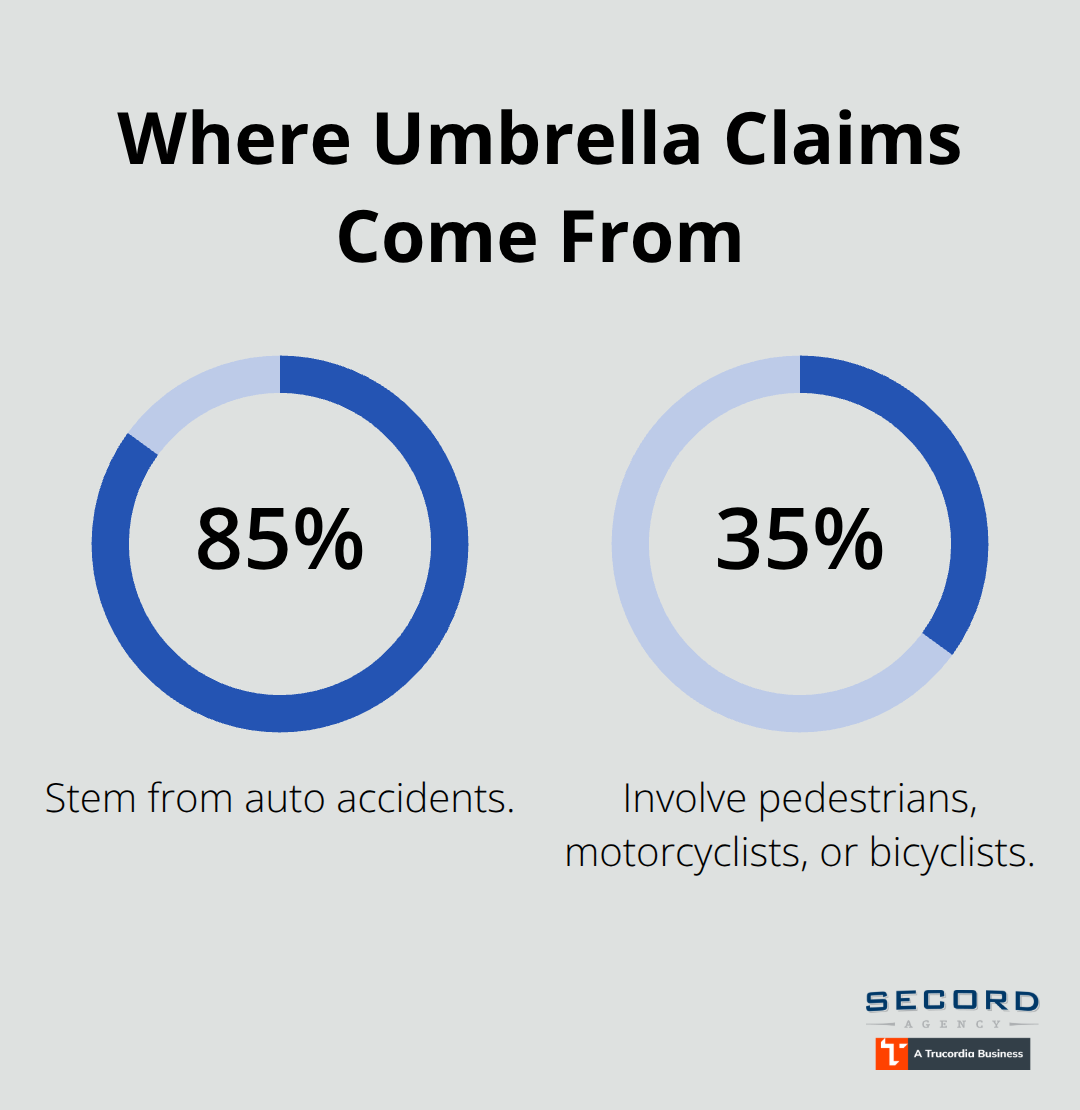

Landlords, pool owners, and parents of teenage drivers face elevated exposure. Safeco Insurance data shows that roughly 85% of umbrella claim payments stem from auto accidents, with approximately 35% of those involving pedestrians, motorcyclists, or bicyclists. A teen driver who causes a serious accident involving multiple injured parties can trigger damages that dwarf standard coverage.

If you rent out a property and a tenant or visitor suffers a major injury on your premises, your homeowners policy maxes out quickly. Hosting events where guests are injured, maintaining a trampoline, or having a dog that injures someone all create realistic pathways to six-figure or seven-figure liability claims. Your assets and future earnings remain at risk unless umbrella coverage protects them.

The Affordability Factor Changes Everything

A $1 million umbrella costs approximately $383 annually, making it far cheaper to add than to face a judgment that decimates your savings or forces wage garnishment. For net worth exceeding $500,000, umbrella insurance becomes economically essential because the annual cost represents a fraction of what you stand to lose. Upgrading to $2 million coverage adds only about $75 per year.

What Happens Without Adequate Protection

Without adequate protection, you pay damages out of pocket once underlying limits exhaust. A driver with $250,000 in auto liability who causes an $800,000 accident faces a $550,000 shortfall. Creditors can pursue bank accounts, investment accounts, and future earnings.

In Washington, primary residences receive some exemption protection under state law, but investment properties, rental income, vehicles, and other assets remain exposed. A $1 million umbrella covering that same accident costs roughly $383 annually and eliminates the personal liability. The decision becomes straightforward: spend a few hundred dollars annually or risk losing hundreds of thousands.

Matching Coverage to Your Actual Exposure

Your specific risk profile determines how much umbrella protection you actually need. Someone with significant rental properties faces different exposure than a homeowner with no tenants. A parent with a teenage driver needs different limits than a retiree with adult children. Evaluating your assets, your lifestyle, and your potential liability sources reveals whether your current coverage leaves dangerous gaps that umbrella insurance can fill.

How Much Umbrella Coverage Do You Actually Need

Calculate Your Net Worth First

Determining your umbrella limit requires honest assessment of three concrete factors: what you own, what your current policies cover, and what a realistic worst-case scenario would cost. Start by calculating your net worth-add up your home value, investment accounts, vehicles, retirement savings, and any other significant assets. This number drives everything. If your net worth sits below $500,000, basic umbrella coverage may not be economically necessary since your underlying policy limits might suffice for most scenarios. However, if your net worth exceeds $500,000, umbrella insurance becomes essential protection. For those in the $500,000 to $1 million range, starting with $1 million in umbrella coverage is standard practice. For net worth above $2 million, many advisors recommend $3 million as a practical minimum to shield future earnings and investments.

The cost difference is minimal-upgrading from $1 million to $2 million adds roughly $75 annually, making it illogical to under-insure simply to save a small premium.

Review Your Current Policy Limits

Pull your declarations pages from your auto and homeowners policies and write down your exact liability limits. Most Washington homeowners carry $300,000 to $500,000 in underlying liability. Most drivers carry $250,000 per person in bodily injury limits. These numbers matter because umbrella policies activate only after underlying limits exhaust, and insurers require minimum underlying coverage of typically $250,000 per person and $500,000 per accident before qualifying for umbrella protection. Your combined underlying limits should ideally reach $500,000 to $750,000-this creates a solid foundation for umbrella protection.

If your auto bodily injury limit sits at $250,000 and your homeowners liability at $300,000, your total underlying protection is only $550,000. A $1 million umbrella on top of this provides reasonable coverage, but gaps remain if damages reach $1.5 million. Align your umbrella limit with your underlying totals rather than purchasing umbrella coverage in isolation.

Assess Your Specific Liability Exposures

Evaluate your specific liability exposures next. Do you rent out property? Roughly 85 percent of umbrella claims stem from auto accidents, with approximately 35 percent involving pedestrians, motorcyclists, or bicyclists-exposures that spike significantly if you drive a teen or operate a vehicle frequently in urban areas. Do you host events regularly, maintain a pool, or own a dog with any history of aggression? These factors increase claim likelihood substantially.

A realistic worst-case scenario for a serious auto accident with multiple injured parties could easily reach $800,000 to $1.2 million in damages. Washington verdicts demonstrate this repeatedly-the 2021 birth-injury case that resulted in a $6 million verdict and the 2023 wrongful death settlement reaching $3.7 million show that single incidents can generate damages far exceeding standard coverage.

Match Coverage to Your Worst-Case Exposure

Match your umbrella limit to your net worth rather than purchasing arbitrary amounts. Your specific risk profile determines how much umbrella protection you actually need. Someone with significant rental properties faces different exposure than a homeowner with no tenants. A parent with a teenage driver needs different limits than a retiree with adult children. Evaluating your assets, your lifestyle, and your potential liability sources reveals whether your current coverage leaves dangerous gaps that umbrella insurance can fill.

Final Thoughts

Washington personal umbrella coverage protects what you’ve built when a single accident threatens to destroy it. The math is undeniable: a $1 million umbrella costs roughly $383 annually, yet a serious liability claim can reach $1.2 million, $3.7 million, or higher based on actual Washington verdicts. Standard homeowners and auto policies max out at $300,000 to $500,000, leaving you personally liable for everything beyond that threshold.

Start by pulling your current policy declarations and confirming your exact liability limits on both auto and homeowners coverage. Write down your net worth, including your home, investments, vehicles, and retirement accounts. If that number exceeds $500,000, umbrella insurance is not optional-it’s the most cost-effective financial decision you can make.

We at Secord Agency – A Trucordia Business help Washington residents determine exactly how much protection they actually need. Our independent agency shops multiple carriers to deliver tailored coverage paired with fast, local service. Contact us for a free coverage assessment and find out whether your current protection leaves dangerous gaps that umbrella insurance can fill.