Seattle vacation rental liability: Reducing Risks for Hosts

Running a vacation rental in Seattle comes with real financial exposure. Guest injuries, property damage, and legal claims can quickly drain your profits if you’re not properly protected.

At Secord Agency – A Trucordia Business, we help hosts understand their Seattle vacation rental liability risks and build solid defenses against them. This guide walks you through the coverage gaps, insurance solutions, and practical steps that actually reduce your exposure.

What Liability Actually Threatens Seattle Vacation Rental Hosts

Guest Injuries and Your Legal Exposure

Washington State treats most Airbnb and VRBO guests as licensees rather than tenants, which means they don’t have the same legal protections as long-term renters. This distinction matters enormously. If a guest slips on your stairs and breaks their arm, or a guest’s child falls into your hot tub, you face a direct liability claim. Washington courts expect property owners to maintain premises in reasonably safe condition and warn visitors of known hazards. Your duty of care extends to obvious dangers like broken railings, faulty appliances, and slippery surfaces.

A guest who stays 30 days or longer shifts into tenant status under Washington’s Residential Tenancy Act, triggering formal eviction procedures if they refuse to leave. This creates a separate liability exposure: if you fail to follow proper eviction law, you could face wrongful eviction claims.

Property Damage and Insurance Gaps

Property damage claims happen frequently. A guest causes a fire that spreads to the neighbor’s house, water damage from a burst pipe floods the unit below yours, or guests throw a party and someone damages fixtures. Standard homeowners insurance explicitly excludes business activities like short-term rentals, leaving you personally liable for these losses.

Airbnb’s Host Protection Insurance provides limited coverage up to $1 million in some scenarios, but it has significant gaps: it doesn’t cover damage to your own property during a guest stay, it doesn’t reimburse lost rental income if the property becomes uninhabitable, and it excludes intentional damage or violations of Airbnb’s terms.

Seattle’s Regulatory and Compliance Risks

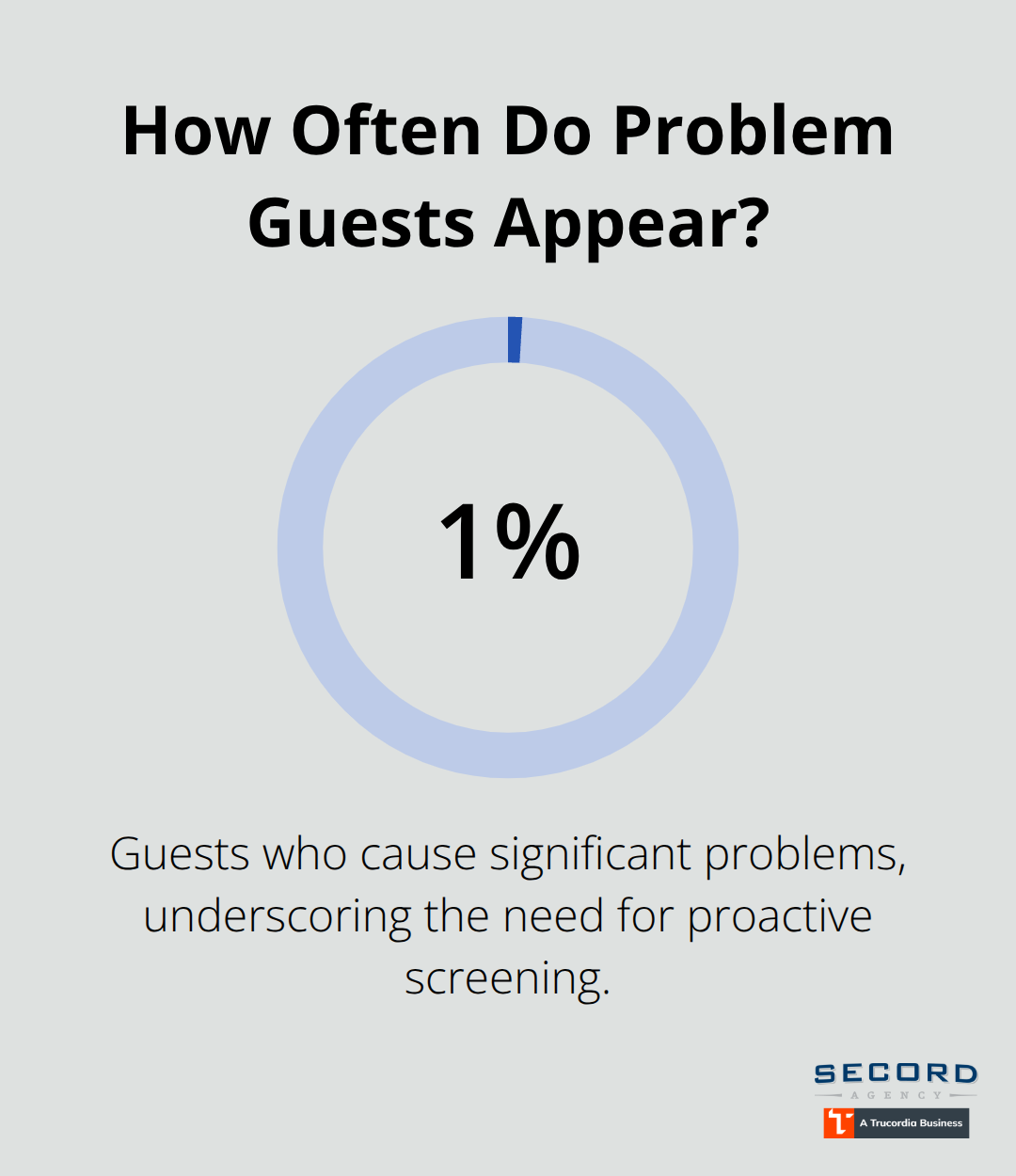

Seattle’s regulatory environment adds another layer of liability exposure. Operating an STR without a regulatory license could subject you to fines and other penalties. Nuisance complaints from neighbors-noise, parties, parking violations-can trigger city enforcement and civil liability if property damage or injuries result. About 1% of guests cause significant problems, making proactive screening essential before they book.

Screening and Maintenance Reduce Real Risk

A detailed screening process catches high-risk bookings before they happen. Red flags include excessive pre-booking questions about early check-in, hot tub temperature, exact toiletries, and thread count of sheets. While meticulous communication doesn’t always signal trouble, large groups or event-focused bookings require stricter scrutiny and clearer house rules.

Property maintenance directly reduces liability. Regular inspections catch hazards before guests arrive. Document all maintenance work and repairs with dates and photos. Keep records of guest communications and incident reports. This documentation protects you in disputes and proves you took reasonable safety precautions. Clear house rules posted in your listing and reinforced at check-in set guest expectations and create legal protection if disputes arise.

Specialized Insurance Closes Coverage Gaps

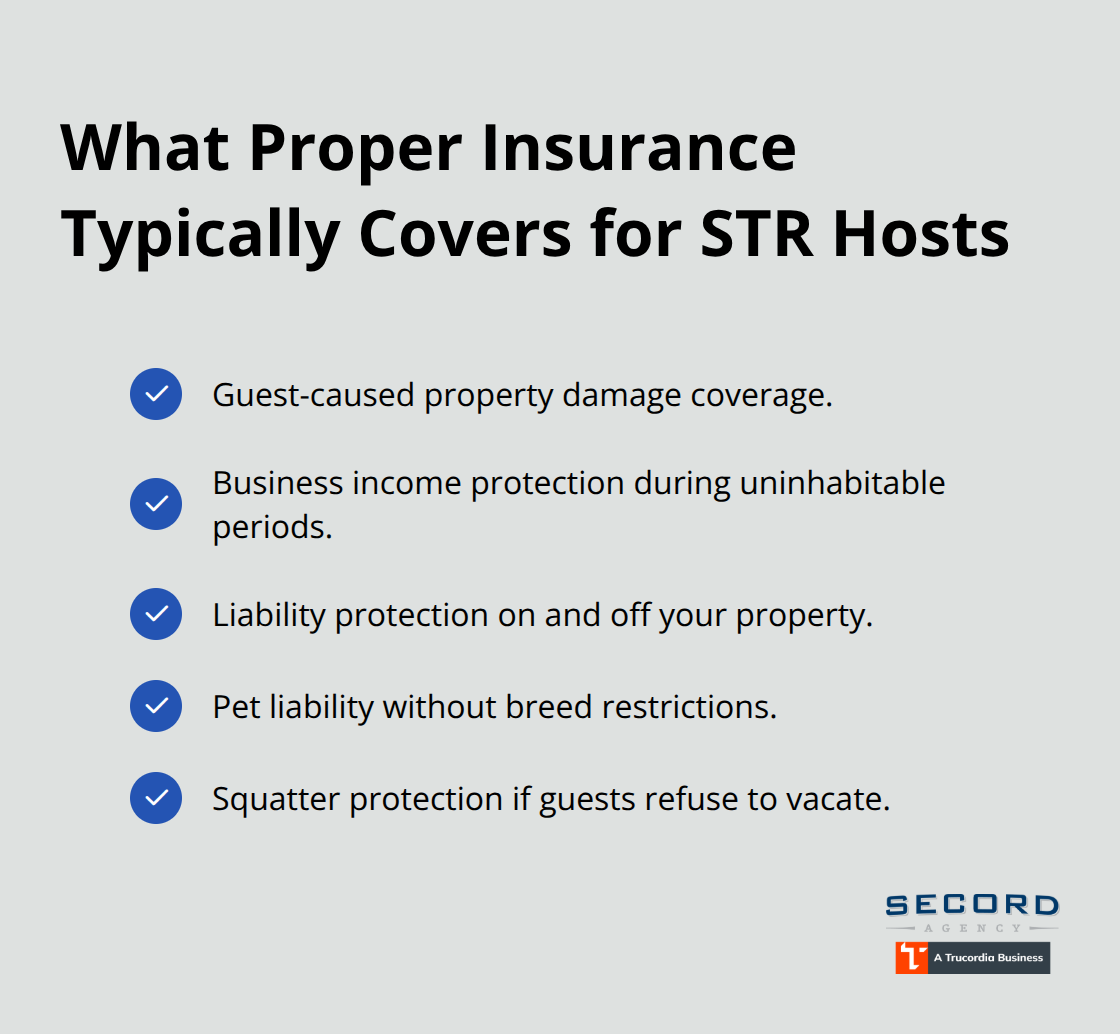

Specialized short-term rental insurance from providers like Proper Insurance addresses exposures that standard policies ignore: guest-caused property damage, loss of rental income during uninhabitable periods, liability for injuries on and off your property, pet liability without breed restrictions, and squatter protection if guests refuse to vacate. Proper’s coverage includes up to $1 million in Commercial General Liability and uses replacement cost coverage for building and contents. Vrbo exclusively endorses Proper as its preferred provider, signaling alignment with major platforms.

The gap between what you think you’re covered for and what you actually are covered for is where financial disaster happens. Understanding these specific liability threats allows you to select the right insurance products and implement the operational safeguards that actually protect your rental business.

What Insurance Actually Covers Your Seattle Rental

Standard Homeowners Policies Exclude Rental Income

Standard homeowners insurance will deny your claim the moment you mention short-term rental income. Most policies explicitly exclude business activities, and insurers actively investigate whether a property generates rental revenue. If you’ve listed your place on Airbnb or VRBO and a guest gets injured or causes damage, your homeowners policy becomes worthless. Airbnb’s Host Protection Insurance sounds comprehensive but covers only specific scenarios: it caps liability at $1 million, excludes damage to your own property during stays, doesn’t reimburse lost income if your unit becomes uninhabitable, and won’t cover intentional damage or guest violations of platform rules. You’re left holding the financial risk for the gaps.

Specialized STR Insurance Fills Critical Coverage Holes

Specialized short-term rental insurance fills these coverage holes with features standard policies ignore entirely. Proper Insurance includes up to $1 million in Commercial General Liability protecting you from guest injuries and third-party claims both on and off your property. Their Building and Contents coverage uses replacement cost valuation with no occupancy restrictions, meaning you’re covered during vacant periods when standard policies would exclude you. Business Revenue Protection reimbarses your actual lost rental income with no time limits if a covered claim makes the property uninhabitable-a critical gap since one water damage incident could cost you thousands in lost bookings. Property Entrustment coverage shields you from guest theft, vandalism, and damage to furnishings that standard homeowners policies specifically exclude. Additional protections include Squatters Protection (providing legal support and lost revenue coverage if a guest refuses to vacate), Pet and Animal Liability without breed restrictions, and Liquor Liability covering alcohol-related incidents. Proper positions itself as the nation’s leading short-term rental insurer with in-house agents trained specifically in vacation rental exposures, backed by Lloyd’s underwriting capacity. The policy covers both short-term nightly stays and longer occupancies, eliminating gaps that plague standard policies when guests transition between booking lengths.

The Real Cost of Inadequate Coverage

The cost difference between inadequate coverage and comprehensive STR insurance is negligible compared to the financial exposure you face. A single guest injury claim can exceed $100,000 in medical costs and legal defense. One water damage incident affecting neighboring units could trigger liability claims exceeding your personal assets. A guest refusing to vacate forces costly eviction proceedings plus lost rental income during the legal process. When you operate a rental business in Seattle’s competitive market where occupancy rates directly determine profitability, losing weeks or months of income from a single incident devastates your returns. Proper’s pricing structure aligns with your actual rental revenue and risk profile rather than charging flat rates that don’t reflect your specific exposure. Lloyd’s backing ensures claims are handled by an insurer with genuine capacity rather than struggling through an underfunded carrier.

Moving Beyond Insurance to Operational Safeguards

Insurance protects your finances after something goes wrong, but the best liability strategy combines coverage with operational practices that prevent problems from happening in the first place. Your insurance policy becomes far more valuable when you’ve already reduced your actual risk through screening, maintenance, and clear communication with guests.

Prevent Liability Before It Starts

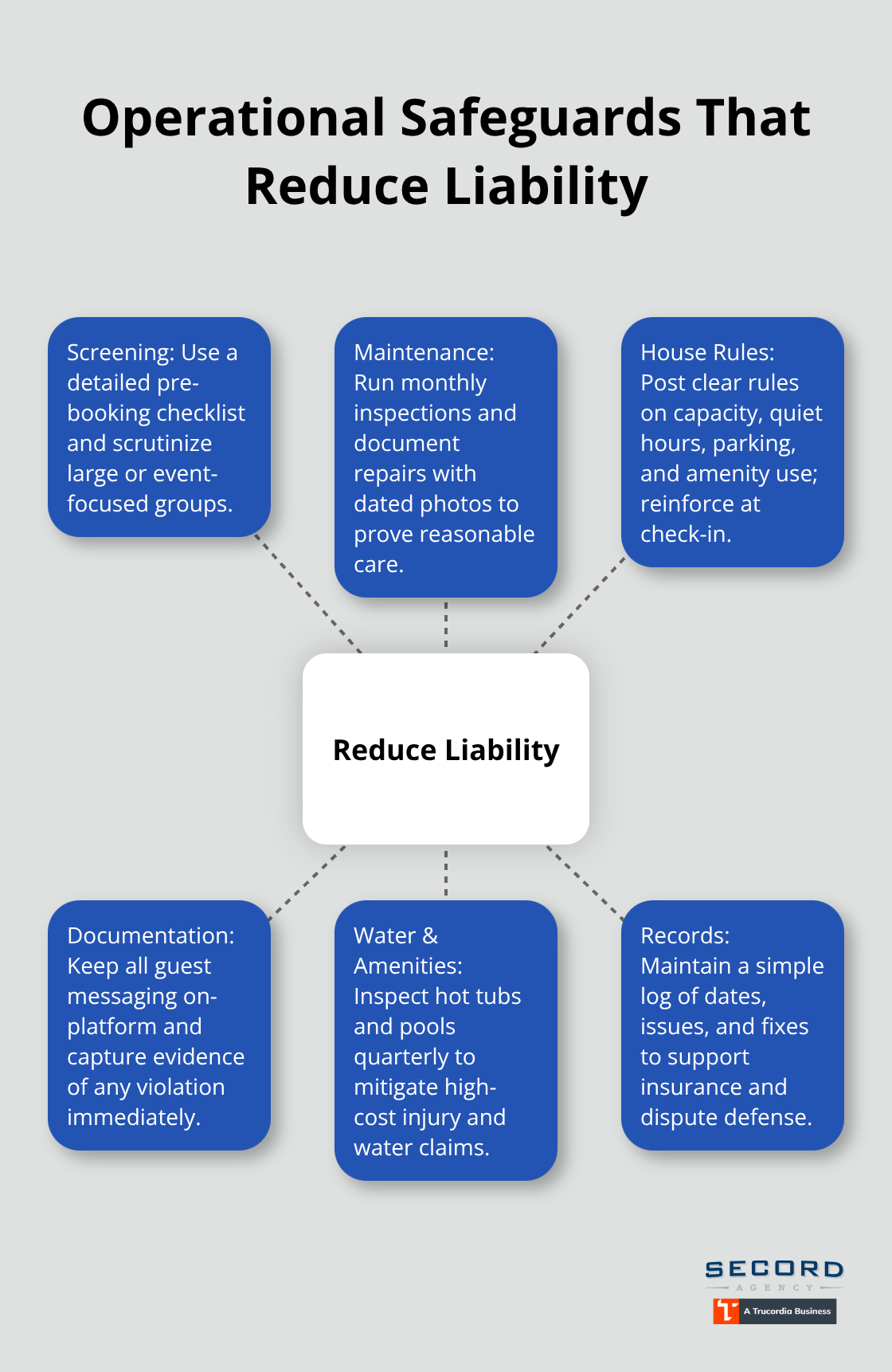

Insurance protects your finances after damage occurs, but operational discipline prevents most problems from happening at all. Property maintenance catches hazards before guests arrive, while clear house rules and documented communication create legal protection if disputes escalate. The hosts who experience the fewest claims aren’t necessarily those with the best insurance-they’re the ones who combine solid coverage with systematic safeguards that reduce actual risk.

Establish a Maintenance Schedule That Catches Hazards Early

Start with a maintenance schedule that inspects critical systems monthly. Check plumbing under sinks for leaks, test smoke and carbon monoxide detectors, examine railings and stairs for loose fasteners, and document everything with photos and dates. A guest injury from a known hazard you failed to address destroys your liability defense in court, regardless of your insurance policy.

Water damage claims in short-term rentals represent some of the costliest incidents, with water damage costing U.S. property owners over $13B annually. Inspect your hot tub or pool equipment quarterly if you offer these amenities, since liability claims from guest injuries at these features frequently exceed $100,000. Keep maintenance records in a simple spreadsheet or property management app showing dates, issues identified, and corrective actions taken-this documentation proves you exercised reasonable care if a claim arises.

Create Clear House Rules That Set Guest Expectations

Clear house rules eliminate misunderstandings that escalate into disputes and liability exposure. Post rules directly in your listing and send them again at check-in, covering guest capacity limits, quiet hours, parking restrictions, pool and hot tub rules, and prohibited activities like smoking or parties. Large groups and event-focused bookings carry significantly higher risk than individual travelers, so your rules should explicitly prohibit events and limit occupancy to the number of beds plus one.

Document Every Guest Interaction and Incident

Document every guest communication in your platform’s messaging system rather than texting or emailing-this creates a timestamped record if disputes arise. If a guest causes damage or violates rules, photograph the damage immediately and document the violation with screenshots of messages. This evidence supports insurance claims and protects you if guests dispute damage charges.

The combination of detailed maintenance records, clear written rules, and documented guest communications significantly strengthens your position in any liability dispute while demonstrating to insurers that you operate with professional standards. Secord Agency, a Trucordia business based in Seattle’s Wallingford neighborhood, helps rental hosts evaluate their coverage gaps and ensure their policies actually protect against the exposures their specific properties face.

Final Thoughts

Running a vacation rental in Seattle means accepting real financial risk, but that risk becomes manageable when you combine the right insurance with operational discipline. Seattle vacation rental liability stems from guest injuries, property damage, regulatory violations, and income loss during uninhabitable periods. Standard homeowners policies won’t cover any of these exposures because they explicitly exclude business activities, while Airbnb’s Host Protection Insurance leaves critical gaps: no coverage for your own property damage, no reimbursement for lost rental income, and no protection against guest refusal to vacate.

Specialized short-term rental insurance from providers like Proper Insurance closes these gaps with Commercial General Liability up to $1 million, Business Revenue Protection that reimburses lost income with no time limits, Property Entrustment coverage for guest-caused damage, and Squatters Protection for guests who refuse to leave. These features address exposures that standard policies ignore entirely. Vrbo’s exclusive endorsement of Proper signals alignment with major platforms and reflects the coverage standards serious hosts need.

Beyond insurance, your best defense is operational discipline: monthly maintenance inspections catch hazards before guests arrive, clear house rules posted in your listing eliminate misunderstandings, and documented guest communications create evidence that protects you in disputes. Contact Secord Agency, an independent insurance agency based in Seattle’s Wallingford neighborhood that shops multiple carriers to deliver tailored coverage for vacation rental hosts. Schedule a policy review this week rather than waiting until after a claim forces the conversation.