Vacation Rental Insurance Policy: Clear Coverage for Your Short-Term Property

Your standard homeowners insurance policy won’t protect your vacation rental business. Most traditional policies explicitly exclude short-term rental properties, leaving you exposed to significant financial risk.

At Secord Agency – A Trucordia Business, we’ve seen property owners lose thousands because they assumed their existing coverage applied to guests. A vacation rental insurance policy fills these gaps and protects both your property and your income stream.

Why Your Homeowners Policy Leaves You Unprotected

Standard Policies Exclude Rental Activity

Your homeowners insurance policy was designed for one purpose: protecting a residence where you live. The moment you rent that property to paying guests, your standard coverage becomes worthless. Most standard homeowners insurance policies exclude short-term rental activity, treating it as a commercial business rather than personal property use. This isn’t a loophole or a technicality-it’s a deliberate exclusion built into every major carrier’s underwriting guidelines.

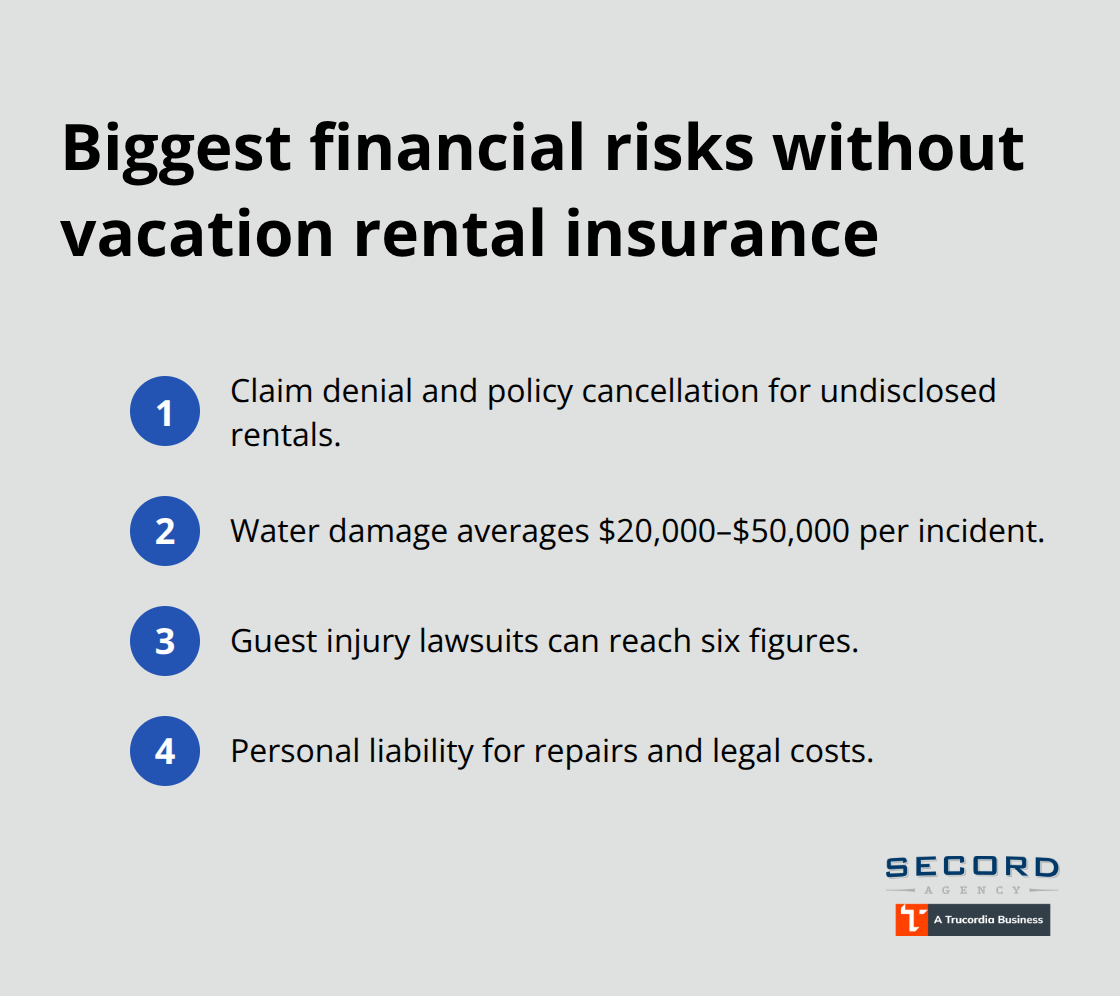

If you file a claim related to guest damage, injury, or lost rental income without disclosing the rental activity, your insurer will deny the claim and potentially cancel your entire policy. Water damage from a burst pipe costs $20,000 to $50,000 on average, especially when it affects multiple floors. A single guest injury lawsuit can easily reach six figures. Without proper vacation rental insurance, you remain personally liable for these costs.

Guest Liability Creates Severe Exposure

The liability exposure is particularly severe because your homeowners policy doesn’t cover injuries or property damage caused by paying guests. If a guest trips on a loose stair and breaks their leg, or if they accidentally start a fire using your kitchen, your standard liability coverage won’t apply. Most homeowners policies limit liability to personal use situations, explicitly excluding business activities.

Guest-related damage also falls outside traditional coverage-theft by guests, intentional vandalism, and accidental property destruction are not covered under standard homeowner’s policies. Your policy simply wasn’t written to handle these commercial risks.

Lost Income During Repairs

Loss of rental income protection represents another critical gap in standard homeowners coverage. If a covered event like fire or water damage makes your property uninhabitable, you lose rental revenue while repairs happen. Depending on your nightly rate and occupancy, this could cost thousands per week. Your guests cancel their reservations, your calendar empties, and your income stops-but your mortgage and property taxes continue.

What Vacation Rental Insurance Provides

A dedicated vacation rental insurance policy fills these gaps with commercial general liability of at least $1 million, property damage coverage at replacement value, and loss of income protection that covers your revenue during repairs. The cost typically ranges from $200 to $600 annually as an endorsement, or higher for standalone policies, but this protection is far cheaper than a single lawsuit or major property loss.

Understanding what your current coverage actually excludes is the first step. The next step is identifying exactly which coverages your specific property needs-and that depends on your guest volume, property type, and the amenities you offer.

What Your Vacation Rental Policy Actually Covers

The Three Core Protections You Need

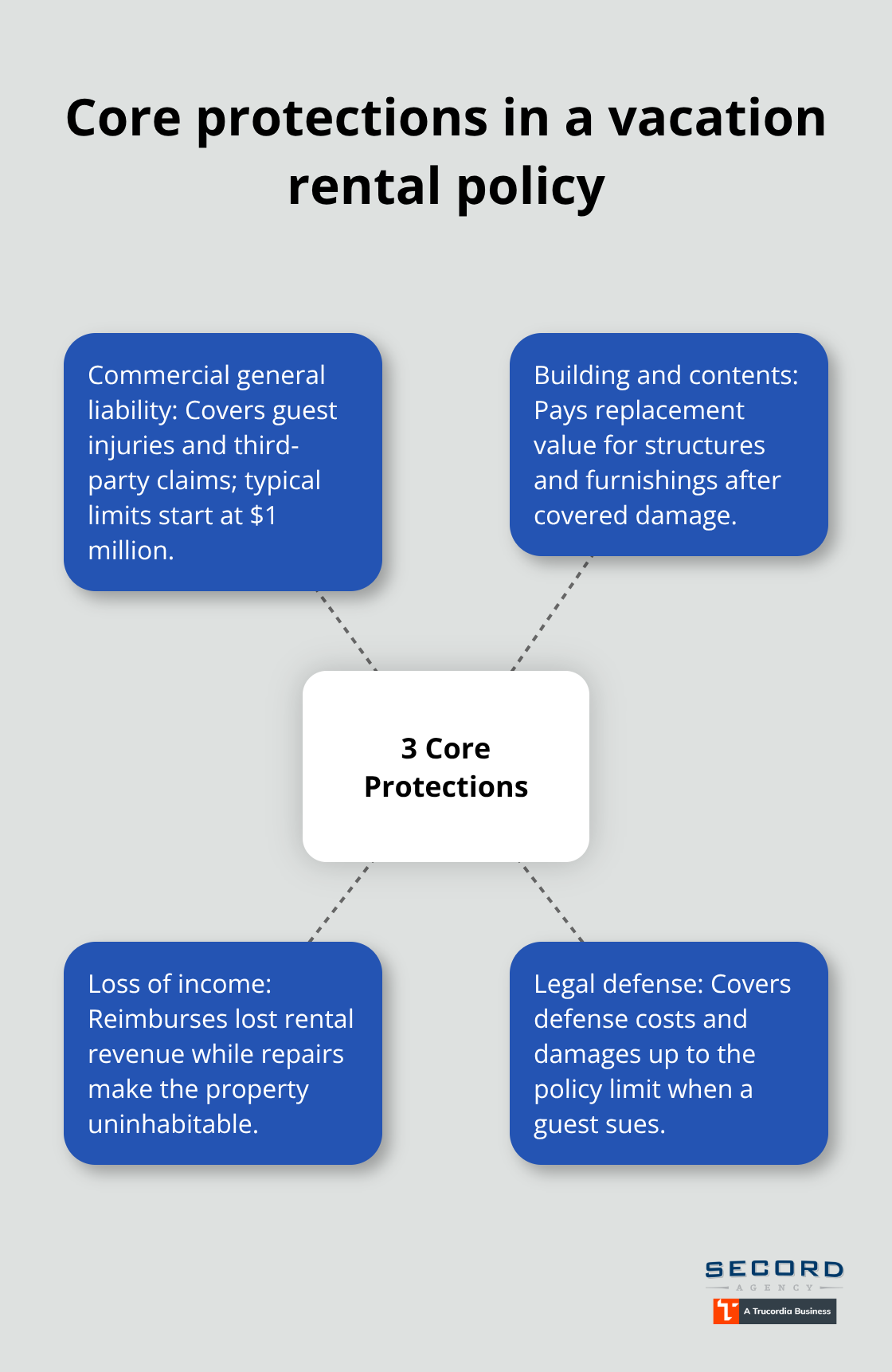

A vacation rental insurance policy provides three core protections that your homeowners policy refuses to offer: commercial general liability coverage, building and contents protection, and loss of income during repairs. This coverage protects against guest injuries and third-party claims, typically starting at $1 million in limits. If a guest is injured on your property and sues, your policy pays legal defense costs and damages up to your coverage limit. Building and contents coverage protects your structure and furnishings at replacement value, not depreciated value-this matters when a guest causes significant damage.

Loss of income protection separates vacation rental insurance from standard policies. If a covered event like water damage or fire makes your property uninhabitable, this coverage reimburses your lost rental revenue while repairs happen. For a property generating $150 per night with 70 percent occupancy, losing even two weeks of income means $2,100 in lost revenue plus cleaning and remediation costs.

Guest Damage and High-Value Item Protection

Property entrustment and guest damage coverage protects against theft and vandalism by guests, with no exclusions for voluntary entrustment. Standard policies explicitly exclude damage caused by people you’ve invited onto your property. If a guest intentionally damages furniture or steals electronics, this coverage applies without the insurer questioning whether you should have trusted that person. High-value items like artwork, jewelry, or electronics often hit coverage limits under standard policies. Ask your insurer about scheduled personal property endorsements that insure specific items at stated values. This targeted approach protects your most valuable possessions without inflating your overall premium.

Water Damage and Specialized Coverage

Water damage deserves special attention because it’s the leading cause of vacation rental claims. Standard vacation rental policies may limit water damage coverage, but specialized carriers offer broader protection for burst pipes, overflow, and guest-related water incidents. Bed bug and pest remediation coverage is increasingly important for short-term rentals. If an infestation forces you to close the property for treatment, this endorsement covers lost income and remediation costs. Some policies also include squatter protection, covering eviction-related legal costs if a guest refuses to leave after their reservation ends.

Endorsements Versus Standalone Policies

The cost structure matters significantly. Endorsements added to your homeowners policy typically cost $200 to $600 annually and cover up to 180 days of rental activity per year. Standalone vacation rental policies have no day limits and work for year-round rentals, making them essential if you rent more than half the year or own the property purely as an investment. When comparing quotes, focus on whether guest intentional damage is covered, whether coverage remains active during vacant periods between guests, and whether the policy distinguishes between personal and commercial liability. These details separate adequate protection from gaps that could cost you thousands. Your specific rental model determines which structure works best for your situation.

How to Choose the Right Vacation Rental Insurance Policy

Match Your Rental Schedule to Your Coverage Type

Start by understanding what you actually rent. A property that hosts guests 200 days per year needs different coverage than one rented 60 days annually. Endorsements capped at 180 days per year work well for occasional hosts, costing $200 to $600 annually and adding coverage to your existing homeowners policy. If you rent year-round or own the property purely as an investment, standalone policies eliminate day limits and provide stronger commercial protections. The distinction matters because an insurer will deny claims if you exceed your endorsement’s rental cap. A property generating $200 nightly with 70 percent occupancy that gets shut down for two weeks loses roughly $2,800 in revenue-far less than the cost difference between endorsements and standalone policies justifies.

Assess Your Property’s Risk Profile

Next, identify your specific risk factors. Properties with wood-burning fireplaces or outdoor grills face underwriting scrutiny from many carriers. In one real-world scenario, Proper Insurance and Farmers Insurance quoted around $2,500 annually for a property with these amenities, while Erie Insurance declined coverage entirely for the same risk profile. This $2,500 figure represents a meaningful premium increase but reveals that coverage availability varies dramatically across insurers. Request quotes from at least three carriers before deciding, and explicitly ask whether guest-use amenities like fireplaces are covered or excluded. Water damage claims on short-term rentals average $20,000 to $50,000 when damage spreads across multiple floors, so confirm that your policy covers burst pipes, overflow, and guest-related water incidents without artificial limits.

Prioritize Coverage Details Over Price Alone

Compare what matters most: whether guest intentional damage is covered without dollar caps, whether coverage stays active during vacant periods between reservations, and whether loss of income protection replaces rent payments you’re unable to collect. Many carriers exclude coverage when properties sit empty, which creates dangerous gaps for turnovers. Ask directly whether the policy covers a guest who refuses to leave after checkout-eviction costs can reach thousands in legal fees and lost revenue. High-value items like electronics, artwork, or jewelry typically hit standard coverage limits, so request a scheduled personal property endorsement for anything worth over $1,000.

For properties in bed bug-prone regions or with frequent turnover, pest remediation and loss-of-income coverage during treatment becomes essential, not optional.

Work With Specialists to Compare Options

Insurance specialists shop multiple carriers and identify coverage gaps quickly-they handle the complexity of comparing coverage structures so you don’t have to. When you receive quotes, the premium difference between carriers often reflects underwriting philosophy more than actual risk. A carrier charging $800 annually might offer broader guest damage coverage with no dollar limits, while another at $600 might cap guest damage claims at $5,000. The cheaper option saves money until you need it, making the coverage gap more expensive than the premium savings. Your guest volume and property characteristics should dictate which structure you choose, not the lowest quote alone.

Final Thoughts

Your vacation rental insurance policy protects your investment where standard homeowners coverage fails. Guest injuries, property damage, and lost income expose you to tens of thousands in personal liability-costs that your homeowners policy explicitly refuses to cover. A dedicated vacation rental policy fills these gaps with commercial general liability, building and contents protection, and loss of income coverage that actually applies to your rental business.

The right policy matches your rental schedule and property risk profile. Endorsements cost $200 to $600 annually for properties rented fewer than 180 days per year, while year-round hosts need standalone policies without day limits. Properties with fireplaces or grills typically cost around $2,500 annually and face stricter underwriting, so confirm coverage applies before you commit. Focus on what matters most: whether guest intentional damage carries no artificial dollar caps, whether coverage stays active during vacant periods, whether loss of income protection fully reimburses your rental revenue, and whether high-value items receive scheduled personal property endorsements.

We at Secord Agency – A Trucordia Business shop multiple carriers to match your specific property and rental model with the right protection. Our team identifies coverage gaps and secures quotes from carriers willing to underwrite your risk profile. Contact us today for a personalized quote that reveals exactly what protection costs for your situation.