Seattle Personal Umbrella Policy: Protecting You with Extra Limits

Your homeowner’s and auto insurance policies have limits. Once you exceed those limits in a lawsuit, you’re personally liable for the rest. A Seattle personal umbrella policy fills that gap with extra protection.

We at Secord Agency – A Trucordia Business help Seattle residents understand when umbrella coverage makes sense and how much protection they actually need.

How Umbrella Insurance Actually Works

The Layering Structure

An umbrella policy sits directly above your existing auto and homeowners coverage, activating only after those underlying limits are exhausted. Your primary policies pay first, and once they hit their limit, your umbrella coverage kicks in to cover additional damages up to its limit. You cannot buy umbrella insurance without maintaining minimum underlying coverage-Washington typically requires at least $250,000 per person and $500,000 per accident in auto liability, plus $300,000 in homeowners liability.

Affordable Protection for Your Assets

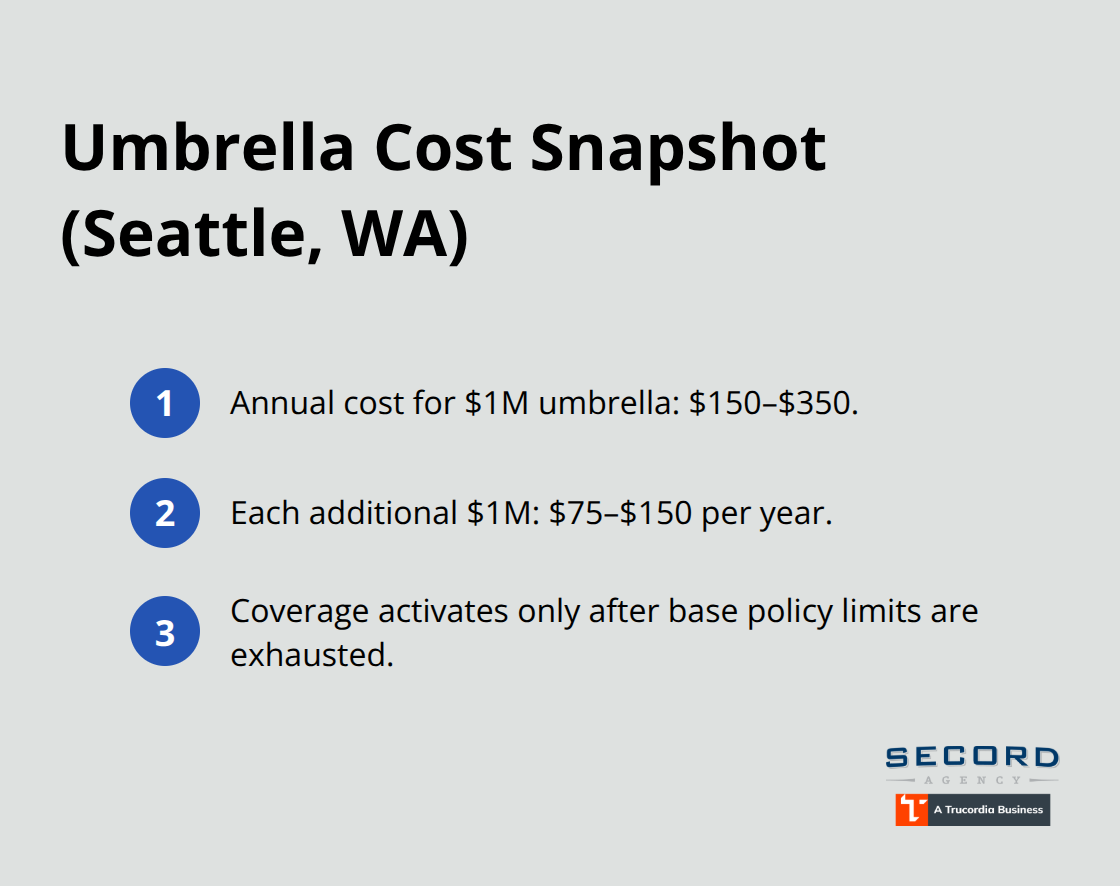

Most insurers charge roughly $150–$350 annually for $1 million in umbrella coverage, making it one of the most cost-effective protections available. Each additional $1 million of coverage typically costs only $75–$150 per year, so jumping from $1 million to $2 million protection remains surprisingly affordable. This pricing structure exists because umbrella policies rarely pay out; they only activate after your base policies are exhausted, which happens in fewer than 1% of claims.

What Your Umbrella Actually Covers

Your umbrella policy covers personal injury claims like defamation and malicious prosecution-areas where standard homeowners policies often leave gaps. It also protects against injuries caused by household members, including your dog, which means a serious dog bite claim reaches your umbrella limit rather than capping at your homeowners liability. The coverage itself extends beyond simple bodily injury and property damage to fill critical protection gaps.

Why Seattle Residents Face Real Exposure

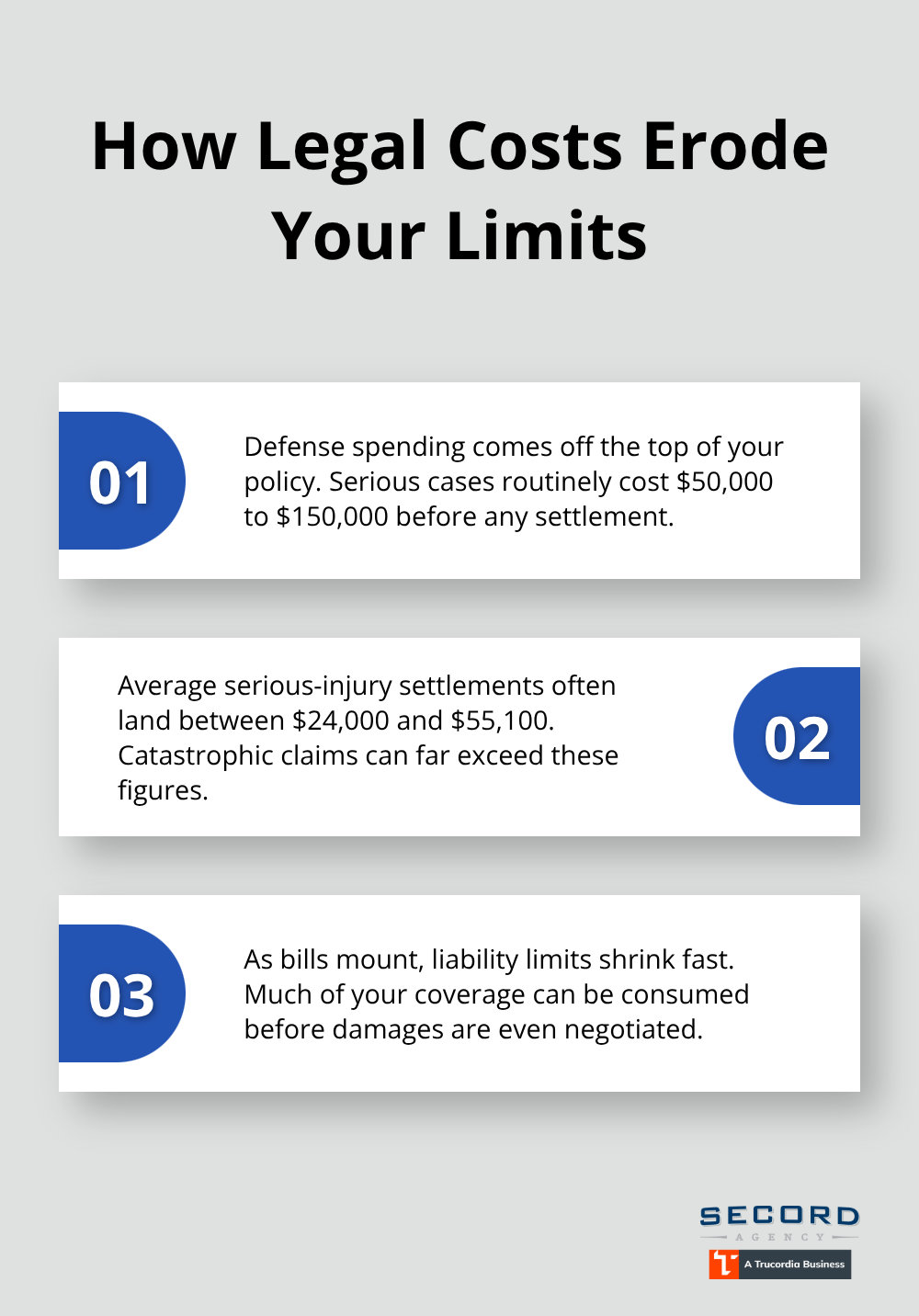

Washington median home prices around $520,000 in 2024 mean most Seattle residents carry substantial assets at risk. A single judgment in a serious accident reaches $400,000 to $600,000; auto judgments in multi-vehicle crashes frequently exceed $500,000. Legal defense costs alone in serious lawsuits run $50,000 to $150,000 before any settlement is reached, which drains your underlying policy limits before the case even concludes.

Bundling Unlocks Hidden Savings

Bundling your auto and homeowners policies with the same carrier qualifies you for multi-policy discounts of 10–15%, which often offsets or exceeds the umbrella premium entirely. This means your extra protection costs little to nothing when you consolidate coverage. Understanding what triggers umbrella claims-and how quickly they happen-shows why this gap protection matters far more than most Seattle residents realize.

Why Seattle’s Assets Face Real Catastrophic Exposure

High Property Values Create Substantial Liability Risk

Seattle’s real estate market generates genuine exposure that most residents underestimate. Washington’s median home price reached $520,000 in 2024, and property values in desirable Seattle neighborhoods often exceed $600,000 to $800,000. When you own significant assets, a single lawsuit threatens everything you’ve built. Home liability judgments typically range from $400,000 to $600,000 when cases proceed to judgment, according to industry data. Auto judgments in serious multi-vehicle crashes frequently exceed $500,000, sometimes reaching into the millions.

The Coverage Gap That Exposes Your Wealth

Your standard homeowners policy caps at $300,000 in liability, and most auto policies max out at $250,000 to $500,000 per accident. The gap between what you’re protected for and what courts actually award creates real financial danger. A guest slipping on your icy Seattle driveway, a dog bite, or a teenage driver causing a multi-vehicle accident can exhaust your primary coverage in weeks.

Legal Defense Costs Drain Your Limits Fast

Legal defense costs amplify this exposure dramatically. A serious lawsuit defense runs $50,000 to $150,000 before any settlement is reached, which means your underlying policy limits get drained before you even reach trial. The Insurance Information Institute reports that average settlements for serious personal injury cases typically range from $24,000 to $55,100, but catastrophic cases far exceed these averages. Defense expenses alone consume a substantial portion of your coverage before damages are even addressed.

What Happens When Your Coverage Runs Out

Without umbrella protection, you face personal liability for amounts beyond your policy limits, potentially forcing asset sales or wage garnishment to satisfy judgments. This isn’t theoretical risk for Seattle residents with substantial net worth-it’s a concrete financial exposure that umbrella coverage directly addresses. The question isn’t whether you’ll face a claim, but whether your current limits will cover it when one arrives.

Real Claims That Drain Your Primary Coverage

Multi-Vehicle Collisions Exhaust Coverage Fast

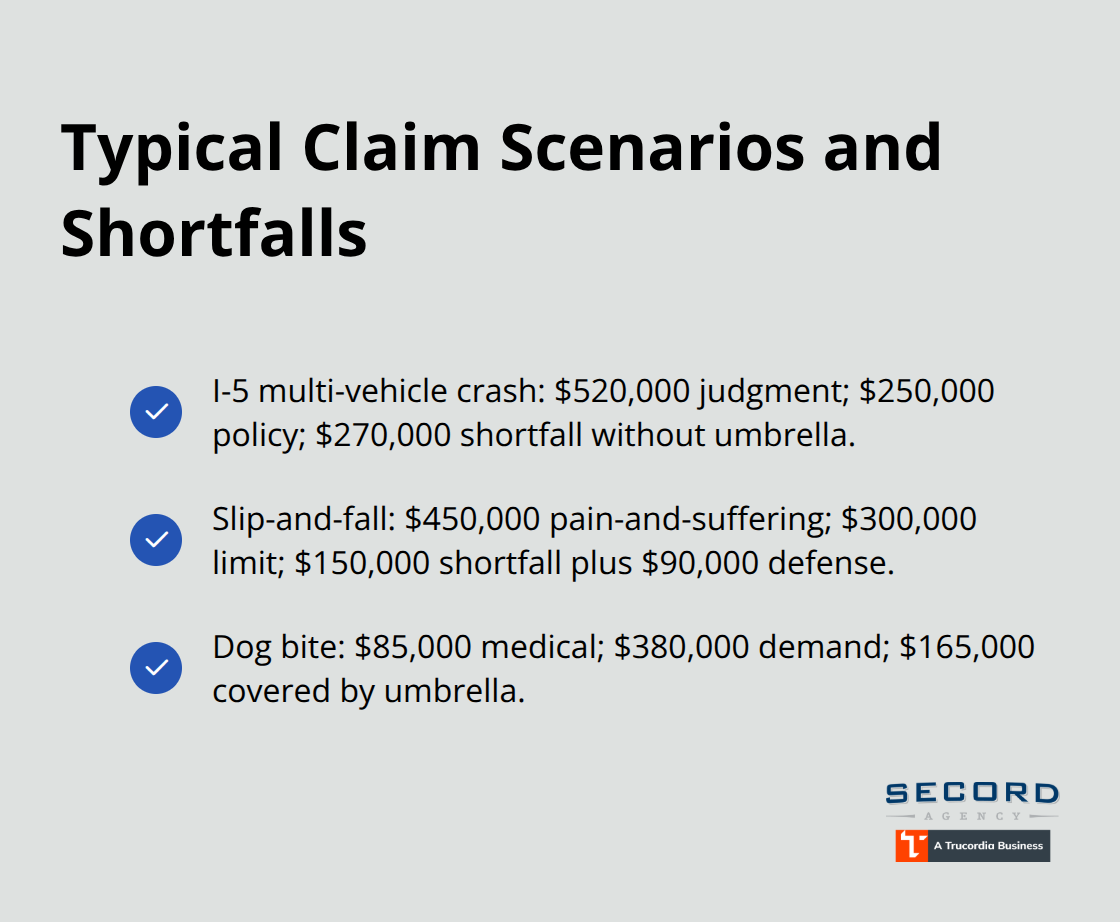

A multi-vehicle highway collision on I-5 near Seattle shows how quickly umbrella coverage becomes necessary. Your teenage driver rear-ends a sedan, which then strikes two additional vehicles, injuring four people across three cars. Medical bills alone reach $380,000 for spinal injuries and ongoing physical therapy. Your auto policy maxes out at $250,000 per accident, leaving a $130,000 gap before anyone’s legal fees are paid. Defense costs run another $75,000, which pulls from your underlying limit and shrinks what’s available for actual damages. The injured parties’ attorneys pursue a judgment that reaches $520,000 total-a realistic figure for multi-vehicle crashes with serious injuries. Without umbrella protection, you’re personally liable for $270,000 after your policy exhausts. With a $1 million umbrella policy costing roughly $200–$300 annually, that protection costs less than a monthly car payment and covers the entire exposure.

Slip and Fall Accidents on Your Property

Slip and fall accidents on your property create similarly devastating claims. A guest slips on ice during a Seattle winter and fractures her hip, requiring surgery and six months of assisted living care. Her medical expenses total $240,000, but her pain-and-suffering claim reaches $450,000 when her attorney calculates lifetime mobility limitations. Your homeowners policy covers $300,000 in liability, leaving a $150,000 shortfall.

Legal defense costs add another $90,000, and your underlying coverage evaporates before damages are addressed. The financial exposure extends far beyond what most Seattle residents anticipate when they review their homeowners limits.

Dog Bite Claims and Permanent Injury Settlements

Dog bite claims follow the same pattern of rapid coverage exhaustion. A neighborhood child suffers facial lacerations requiring reconstructive surgery, with medical costs at $85,000 and a settlement demand of $380,000 for permanent scarring. Your homeowners liability limit covers only $300,000, forcing your umbrella to absorb $165,000 in additional exposure. These scenarios aren’t outlier situations; they’re the exact claims umbrella policies handle routinely. A $1 million umbrella covers all three scenarios completely while costing approximately $250 per year when bundled with your auto and home policies through the same carrier.

Final Thoughts

Seattle residents with substantial assets face real financial exposure from a single lawsuit. Your homeowners and auto policies cap at $300,000 and $250,000 to $500,000 respectively, but judgments regularly exceed $500,000 in serious cases. A Seattle personal umbrella policy fills this gap affordably, costing roughly $200–$300 annually for $1 million in coverage when bundled with your existing policies. Legal defense costs alone drain $50,000 to $150,000 before settlement, and serious injury judgments reach $400,000 to $600,000.

Without umbrella protection, you face personal liability for amounts beyond your policy limits, potentially forcing asset sales or wage garnishment to satisfy judgments. With umbrella coverage, you transfer that risk to your insurer for less than the cost of a monthly car payment. This protection matters far more for Seattle residents who own homes valued at $520,000 or higher and carry retirement savings that courts can pursue.

Start by gathering your auto and homeowners declarations to confirm your current liability limits. Then contact Secord Agency to discuss your exposure and receive quotes from multiple carriers. We’ll explain exactly what your umbrella covers, what it doesn’t, and how bundling discounts reduce your total premium.