Umbrella Liability Insurance In Seattle: Do You Need It?

Your standard homeowners or auto insurance policy has limits. Once you exceed those limits, you’re personally responsible for the rest-and that can mean losing assets you’ve worked years to build.

At Secord Agency – A Trucordia Business, we see Seattle residents overlook umbrella liability Seattle coverage until it’s too late. An umbrella policy sits above your existing insurance and covers the gaps, protecting your savings, home equity, and future earnings when a lawsuit goes beyond your primary policy limits.

What Umbrella Insurance Actually Covers

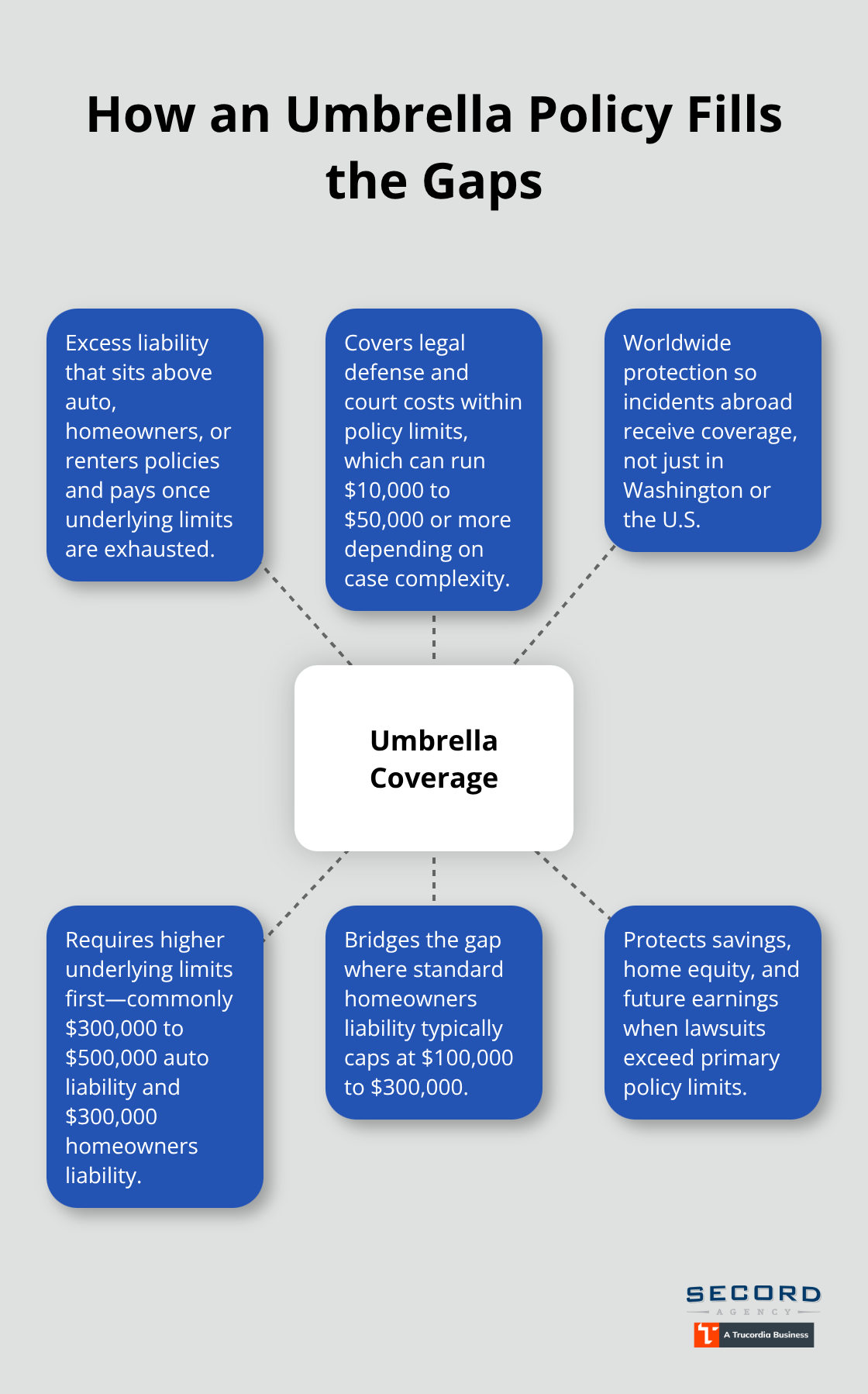

Umbrella liability insurance activates only after your primary policies-auto, homeowners, or renters-exhaust their limits. Washington State sets minimum auto liability at $25,000 per person and $50,000 per accident, according to the Washington State Department of Licensing. A single serious injury claim easily exceeds these thresholds. When your underlying policy hits its limit, your umbrella policy takes over and pays additional damages up to its coverage amount, typically $1 million to $5 million.

Most insurers require you to carry higher underlying limits-commonly $300,000 to $500,000 in auto liability and $300,000 in homeowners liability-before issuing an umbrella policy. This requirement exists because umbrella coverage functions as excess protection, not primary coverage. The policy covers legal defense costs and court expenses within its limits, which can run $10,000 to $50,000 or more depending on case complexity. Umbrella coverage extends worldwide, so incidents abroad receive protection. Many Seattle residents assume their homeowners policy provides sufficient liability protection, but standard homeowners policies typically cap liability at $100,000 to $300,000. With Seattle’s high property values and active lifestyle culture, that gap between your policy limit and potential damages grows quickly.

What Incidents Trigger Umbrella Coverage

A serious car accident where you cause injury represents the most common trigger. If you cause a collision injuring multiple people, medical bills and lost wages can reach $500,000 to $2 million within months. Your auto insurance covers its limit, then your umbrella kicks in for the remainder. Property damage claims also activate umbrella protection-if you damage someone’s expensive vehicle, boat, or home, costs mount fast.

A guest slipping and falling on your Seattle property and suffering a broken hip with ongoing physical therapy can generate $300,000 in medical expenses plus pain-and-suffering damages. Your homeowners liability covers part of it; your umbrella covers the rest. Dog bite incidents fall under umbrella coverage when your pet injures someone and medical costs exceed your homeowners limit. A neighbor’s child injured in your yard, a tree falling on a neighbor’s house during a storm, and water damage to an adjacent property all trigger potential umbrella claims. Personal liability incidents like libel or slander claims also qualify for coverage under most policies, though specific coverage varies by insurer. Seattle’s dense neighborhoods and active social environments create frequent opportunities for liability exposure that standard policies leave unprotected.

Why Standard Limits Fall Short in Seattle

Seattle homeowners carry substantial equity in expensive properties. Median home prices in Seattle neighborhoods exceed $800,000, meaning significant home equity sits unprotected if a liability judgment exhausts your standard policy. A $300,000 homeowners liability limit sounds adequate until you face a $1 million judgment. Your personal assets-savings, investment accounts, future earnings-become vulnerable to garnishment.

High earners in Seattle’s tech, aerospace, and professional services sectors face elevated exposure because larger judgments target those with greater earning potential. A tech professional earning $200,000 annually faces garnishment risk that could impact decades of income if a serious claim occurs. Standard policies also exclude certain liability types that umbrella policies cover, creating unexpected gaps. Your homeowners policy might exclude liability from renting out a guest house or operating a home-based business, but umbrella coverage can extend to these situations depending on the policy.

How Washington’s Legal System Affects Your Risk

Washington’s at-fault insurance system means whoever causes an accident bears full financial responsibility for damages. Unlike no-fault states, you cannot rely on the other party’s insurance to cover excess damages. This legal framework makes umbrella insurance prudent risk management for anyone with assets worth protecting. Understanding your exposure under Washington law helps you determine whether your current coverage leaves you vulnerable-a question that leads directly to calculating how much umbrella protection you actually need.

Who Needs Umbrella Coverage in Seattle

Umbrella insurance isn’t just for the ultra-wealthy, though high net worth certainly increases the case for it. Anyone with meaningful assets, regular liability exposure, or earning potential that could face garnishment needs this protection. Seattle’s real estate values, active lifestyle, and concentration of high earners create conditions where standard policies leave substantial financial gaps. The question isn’t whether umbrella insurance exists for you-it’s whether you can afford the consequences of not having it.

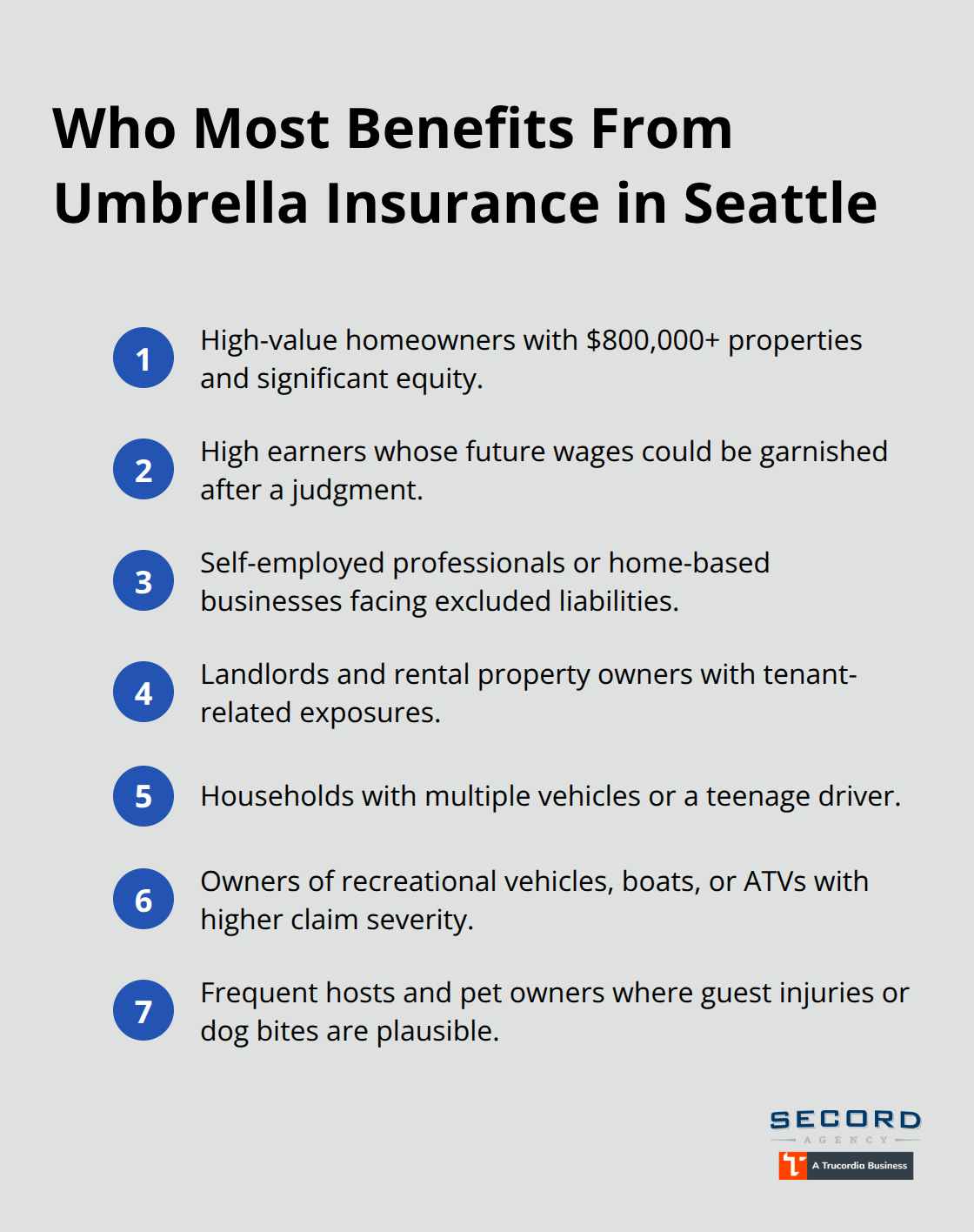

High-Value Homeowners Face the Biggest Exposure

Seattle homeowners sitting on $800,000+ properties absolutely need umbrella coverage. A single liability judgment of $500,000 to $2 million eats directly into home equity that took decades to build. Standard homeowners policies typically max out at $100,000 to $300,000 in liability protection, leaving massive exposure.

If you carry a mortgage on a valuable Seattle property, your lender’s requirements already demand adequate coverage-umbrella insurance completes that picture by protecting equity beyond what basic homeowners policies cover.

High Earners and Self-Employed Professionals

Tech professionals, aerospace engineers, and other high earners in the Seattle area face particular risk because courts consider earning potential when awarding damages. A tech worker earning $250,000 annually faces garnishment that could impact 20+ years of future income if a judgment exceeds policy limits. Self-employed professionals and business owners operating from home or managing rental properties encounter additional liability exposure that standard policies often exclude entirely. A consultant renting out a guest house, a contractor operating a home-based business, or a landlord managing multiple units all face scenarios where homeowners liability either doesn’t apply or caps far below realistic exposure. Umbrella policies fill these gaps effectively.

Vehicle Owners and Recreational Activity Enthusiasts

Vehicle owners with multiple cars, particularly those who drive frequently on Seattle’s congested highways or mountain roads, encounter elevated collision risk. Anyone with a teenage driver in the household faces substantially higher accident likelihood-umbrella coverage protects against the statistical reality that younger drivers cause more serious accidents. Owners of recreational vehicles, boats, or ATVs need umbrella protection because these activities generate disproportionately high liability claims. A jet ski accident or boating incident can easily produce $1 million in damages when multiple parties suffer serious injury.

Pet Owners and Frequent Hosts

Parents with active kids, pet owners with large dogs, and anyone who hosts gatherings regularly should carry umbrella insurance because slip-and-fall incidents, dog bites, and guest injuries represent common liability triggers. You don’t need to be wealthy to face a $500,000+ judgment-you just need one serious incident involving someone else’s injury. These everyday scenarios happen across Seattle neighborhoods, making umbrella protection a practical safeguard that protects your financial future when liability claims exceed what your standard policies cover.

How Much Coverage Protects Your Seattle Assets

Calculate Your Exposed Assets

Start with your net worth, not theoretical risk scenarios. Add up your home equity, investment accounts, retirement savings outside ERISA-protected plans like 401(k)s, and any other liquid assets you’d lose in a major lawsuit. Seattle homeowners with $800,000 properties and $200,000 in savings sit on $1 million in exposed assets. A $1 million umbrella policy covers that exposure directly.

The Washington State Office of the Insurance Commissioner notes that umbrella premiums run roughly $300 to $500 annually for $1 million in coverage, making this protection exceptionally affordable relative to what you’re protecting. High earners in Seattle’s tech sector earning $200,000+ annually should calculate future earning potential too-a judgment could trigger wage garnishment for years, so add 10 to 20 years of after-tax income to your vulnerability calculation.

Exclude ERISA-protected retirement accounts and pensions since creditors cannot touch these assets in most cases. State law varies on IRA protections, so include those conservatively. If your home equity falls below Washington’s homestead exemption threshold, you may skip umbrella coverage for that portion, though few Seattle properties qualify given current valuations.

Match Coverage to Your Actual Exposure

The math becomes straightforward: if your exposed assets total $1.5 million, buy $2 million in coverage. If you own $3 million in unprotected assets, $3 to $5 million in umbrella limits makes financial sense. Most insurers require underlying auto liability of at least $250,000 and homeowners liability of $300,000 before issuing umbrella coverage, so verify your current limits before shopping.

We recommend buying the umbrella limit that fully covers your exposed assets rather than stopping at $1 million simply because it costs less. A $500,000 judgment against your $1 million umbrella leaves you paying $500,000 out-of-pocket-defeating the entire purpose of protection.

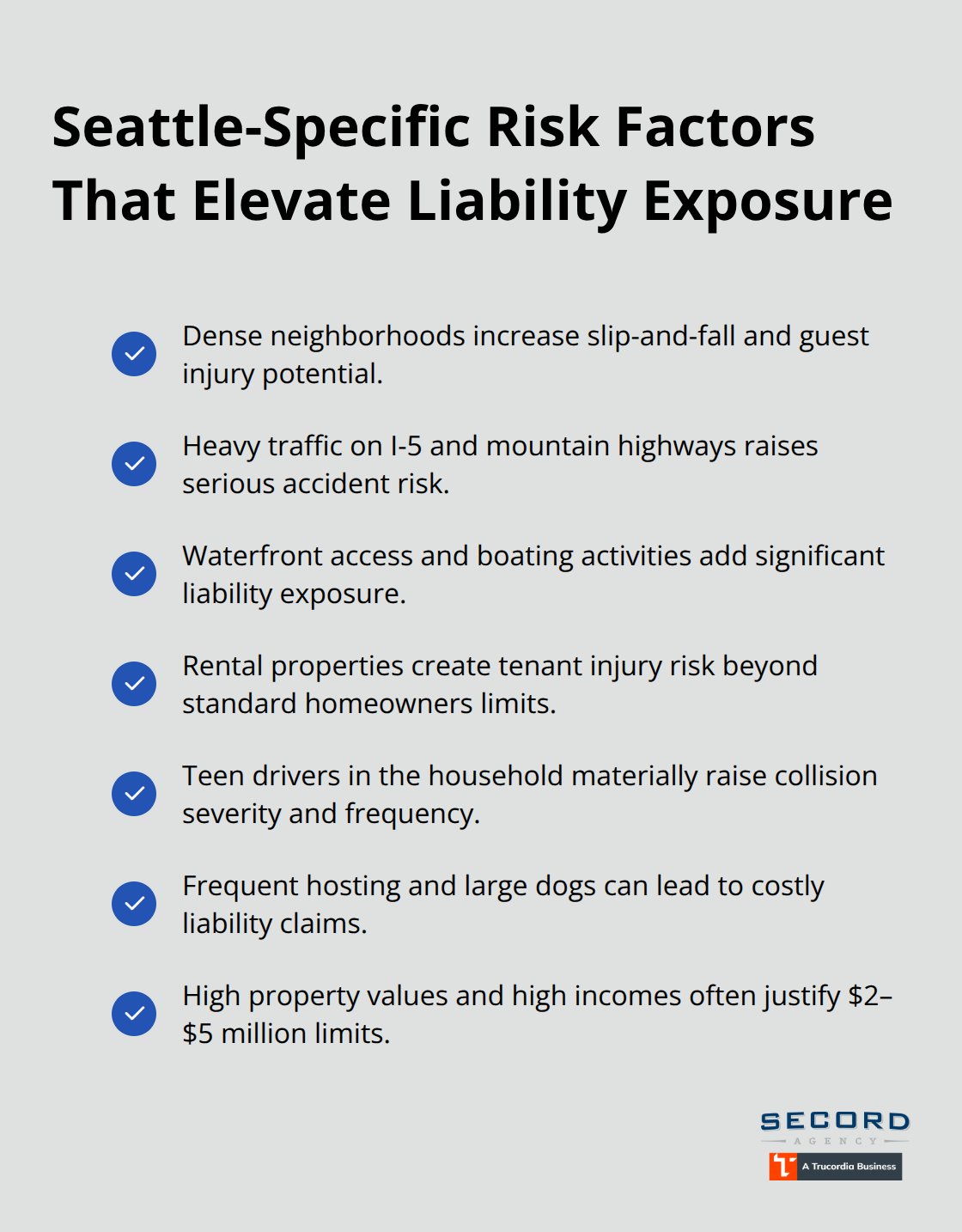

Account for Seattle-Specific Risk Factors

Seattle-specific risk factors push coverage needs higher than national averages. Dense neighborhoods create frequent slip-and-fall exposure, heavy traffic on I-5 and mountain highways increases serious accident likelihood, and waterfront properties add boating liability. Rental property owners face substantially elevated exposure-a tenant injured in your rental unit can pursue claims well above standard homeowners limits.

Multiple vehicle households with teenage drivers dramatically increase accident probability since drivers under 25 cause accidents at rates triple the national average. Pet owners with large dogs, frequent hosts who entertain regularly, and anyone operating a home-based business all face above-average liability exposure. Seattle’s expensive real estate and high-earning population mean asset exposure typically justifies $2 to $5 million in umbrella limits.

Final Thoughts

Umbrella liability Seattle coverage protects what matters most-your home, savings, and future earnings-when a single serious incident creates damages beyond your standard policy limits. We at Secord Agency – A Trucordia Business have watched Seattle residents face devastating financial consequences from liability judgments that exceeded their basic coverage by hundreds of thousands of dollars. A $1 million umbrella policy costs roughly $300 to $500 annually, making this one of the most cost-effective financial decisions you can make.

Contact Secord Agency – A Trucordia Business to discuss your specific situation with a local agent who understands Seattle’s real estate values, traffic patterns, and liability landscape. We shop multiple carriers to find competitive rates and coverage tailored to your actual exposure rather than generic recommendations. Our team reviews your current auto and homeowners limits, calculates your exposed assets, and recommends umbrella coverage that fully protects your financial position.

Seattle property values continue climbing, meaning your home equity exposure increases annually. If you’ve built significant savings, earned promotions, or expanded your real estate holdings over the past few years, your umbrella coverage likely hasn’t kept pace. A quick policy review takes 15 minutes and could reveal substantial gaps in your protection.