Commercial Landlord Insurance Washington: Tailored Coverage for Your Properties

Commercial landlord insurance in Washington protects your rental properties from financial losses that could devastate your business. Tenant disputes, property damage, and liability claims happen more often than most landlords expect.

At Secord Agency – A Trucordia Business, we’ve helped Washington property owners find coverage that actually matches their specific risks. This guide walks you through what you need to know to protect your investment.

What Your Commercial Landlord Policy Actually Covers

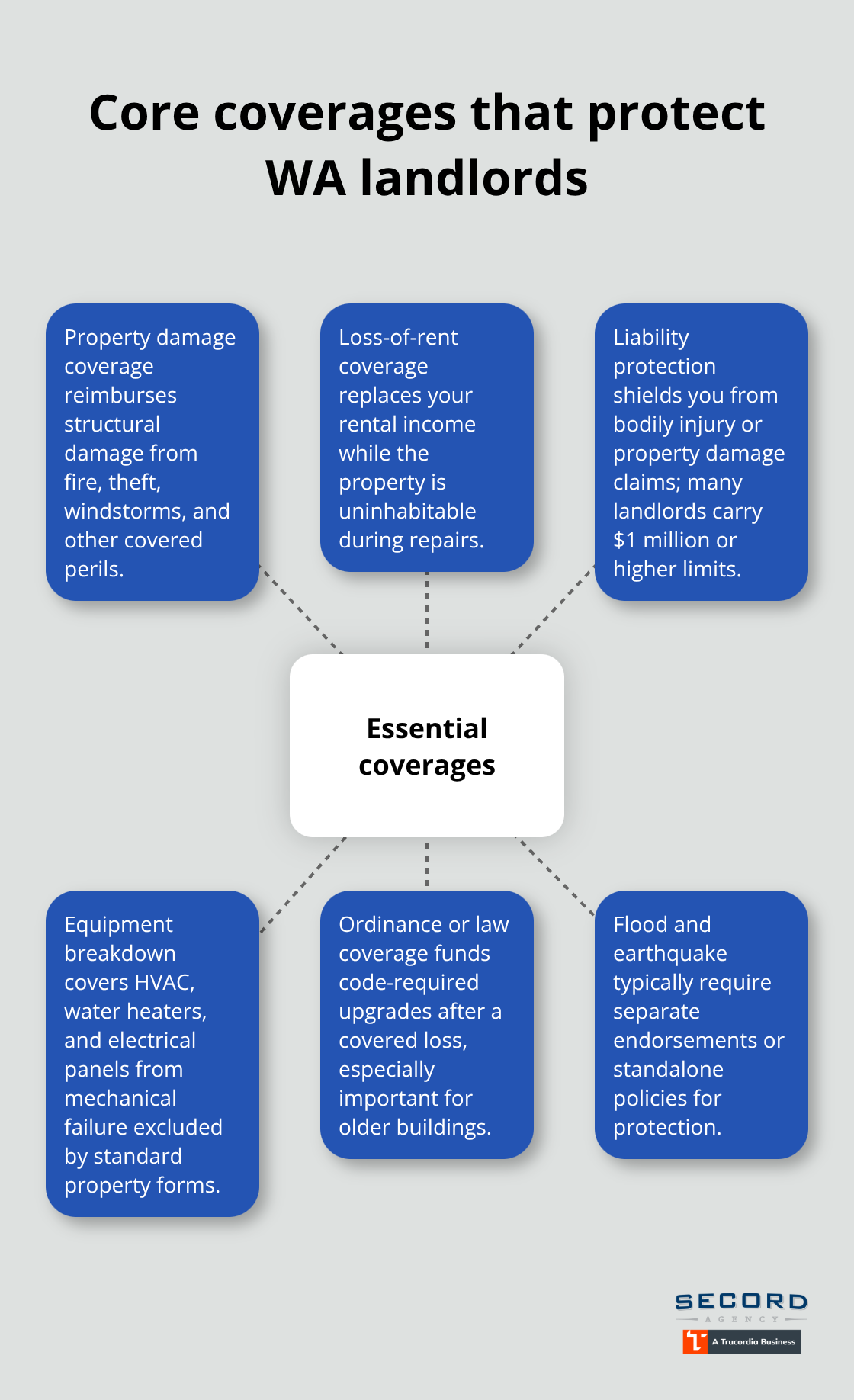

Commercial landlord insurance in Washington covers three core areas that directly protect your rental income and assets. Property damage coverage reimburses you for structural damage from fire, theft, windstorms, and other covered perils-but this is only half the story. The real financial lifeline is loss-of-rent coverage, which replaces your rental income while the property sits uninhabitable during repairs. If a fire forces tenants out for three months, loss-of-rent coverage keeps your cash flow steady instead of forcing you to cover your mortgage and expenses from savings.

Liability Protection Against Major Claims

Liability protection stands equally critical because tenant injuries or third-party claims on your property can result in devastating judgments. Many Washington landlords carry $1 million or higher limits, and some add umbrella policies for additional protection. This coverage shields you from the financial impact of bodily injury or property damage claims that occur on your property.

Equipment Breakdown and Building Systems

Equipment breakdown coverage protects essential building systems like HVAC units, water heaters, and electrical panels from mechanical failure-a peril your standard property coverage excludes. A failed heating system in January can force tenant evacuation and trigger loss-of-rent claims, making this add-on protection valuable. Ordinance or law coverage funds code-required upgrades after a covered loss, which matters especially for older properties in Washington where seismic codes, electrical standards, and fire-safety requirements frequently change during repairs. Without this endorsement, you pay out-of-pocket for code compliance, sometimes adding 15–25% to reconstruction costs.

Weather and Natural Disaster Coverage

Weather-related coverage varies by peril: standard policies cover wind and hail damage, but flood and earthquake require separate endorsements or standalone policies. Flood risk extends beyond mapped floodplains-so even properties on higher ground warrant excess flood coverage if your lender requires it or if you want income protection during water damage.

Understanding these coverage layers helps you identify gaps in your current protection. The next step involves assessing your specific property type and risk exposure to determine which coverage options align with your portfolio.

Why Washington’s Natural Hazards and Tenant Risks Demand Specialized Coverage

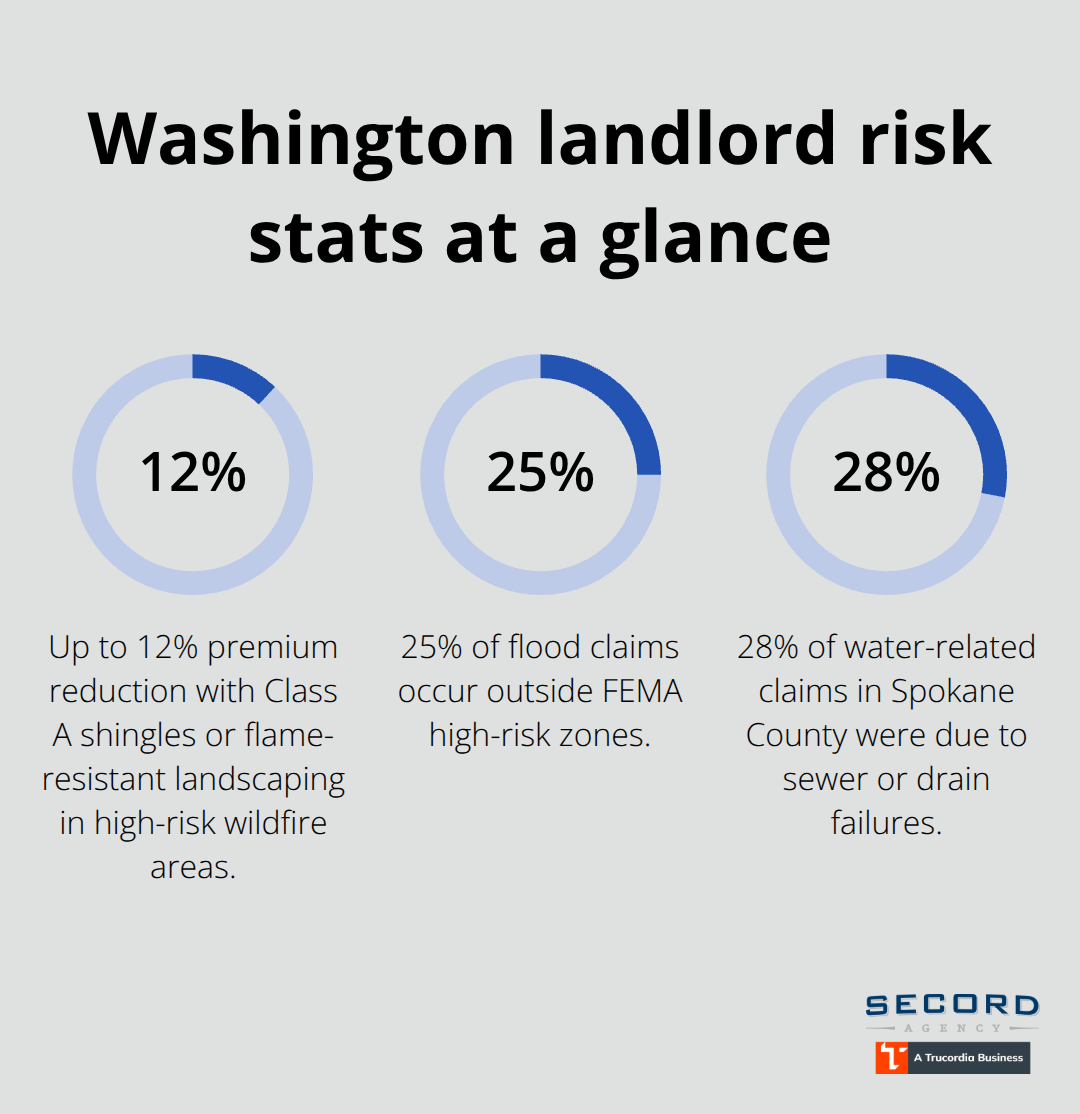

Washington landlords face hazards that standard commercial policies simply don’t address adequately. The Cascadia Subduction Zone poses a significant earthquake risk, yet earthquake damage remains excluded from standard property policies unless you purchase a separate endorsement. Wildfire risk intensifies in Central and Eastern Washington, with smoke damage and defensible-space requirements becoming underwriting standards that can reduce premiums by up to 12% if you upgrade to Class A shingles or flame-resistant landscaping. Flood risk extends far beyond mapped floodplains-FEMA reports 25% of flood claims originate outside high-risk zones, meaning even properties on higher ground warrant excess flood coverage. Standard policies cap residential flood at $250,000 through the National Flood Insurance Program, leaving substantial gaps for investors with larger portfolios. Water backup from sewer or drain failures caused roughly 28% of water-related claims in Spokane County last year, yet this peril requires an optional endorsement that many landlords overlook entirely.

Earthquake and Wildfire Exposure in Washington

These aren’t theoretical risks; they’re documented patterns that directly affect your rental income and asset value. A major earthquake near Seattle could trigger substantial replacement costs statewide, and your standard policy won’t cover structural damage unless you add earthquake protection. Wildfire smoke travels hundreds of miles, affecting properties far from active fire zones, and insurers now require defensible-space inspections and Firewise compliance in high-risk areas. Upgrading your roof to metal or Class A shingles and maintaining flame-resistant landscaping signals risk reduction to carriers and can lower your premiums substantially.

Flood Risk Beyond High-Risk Zones

Properties outside FEMA-mapped floodplains still experience water damage from heavy rainfall, snowmelt, and drainage failures. The Flood Hazard Map identifies more than 175,000 structures in mapped floodplains across Washington, but the remaining properties face equal exposure to localized flooding. Excess flood policies and parametric flood coverage (which pays based on rainfall measurements rather than actual damage assessment) provide faster payouts and broader protection than NFIP coverage alone. Water backup endorsements specifically cover sewer and drain failures, a peril that standard property policies exclude.

Tenant Liability Claims and Rising Verdict Costs

Tenant-related liability claims in Washington have grown more expensive and more frequent. A single slip-and-fall injury or guest accident can exceed your standard $300,000 liability limit within hours of litigation, which is why baseline coverage of at least $500,000 per occurrence makes sense for single properties and $1 million for multi-unit portfolios. Tenant disputes over security deposits, lease violations, or injury claims create exposure that your personal homeowners policy explicitly excludes.

Regulatory Complexity and Income Protection

Washington’s Residential Landlord-Tenant Act adds regulatory complexity-non-compliance triggers fines and legal defense costs that insurance doesn’t cover unless you have proper commercial coverage in place. Loss-of-rent protection becomes critical during tenant disputes or property damage, since your mortgage, property taxes, and maintenance costs don’t pause while repairs happen or tenants relocate. Washington’s rental market has grown substantially, intensifying competition and tenant turnover, which increases the likelihood of damage claims and income interruption during vacancy periods.

Understanding these specific Washington hazards and tenant exposures shapes which coverage options actually protect your portfolio. The next step involves matching your property type and risk profile to the right policy structure.

How to Choose the Right Policy for Your Properties

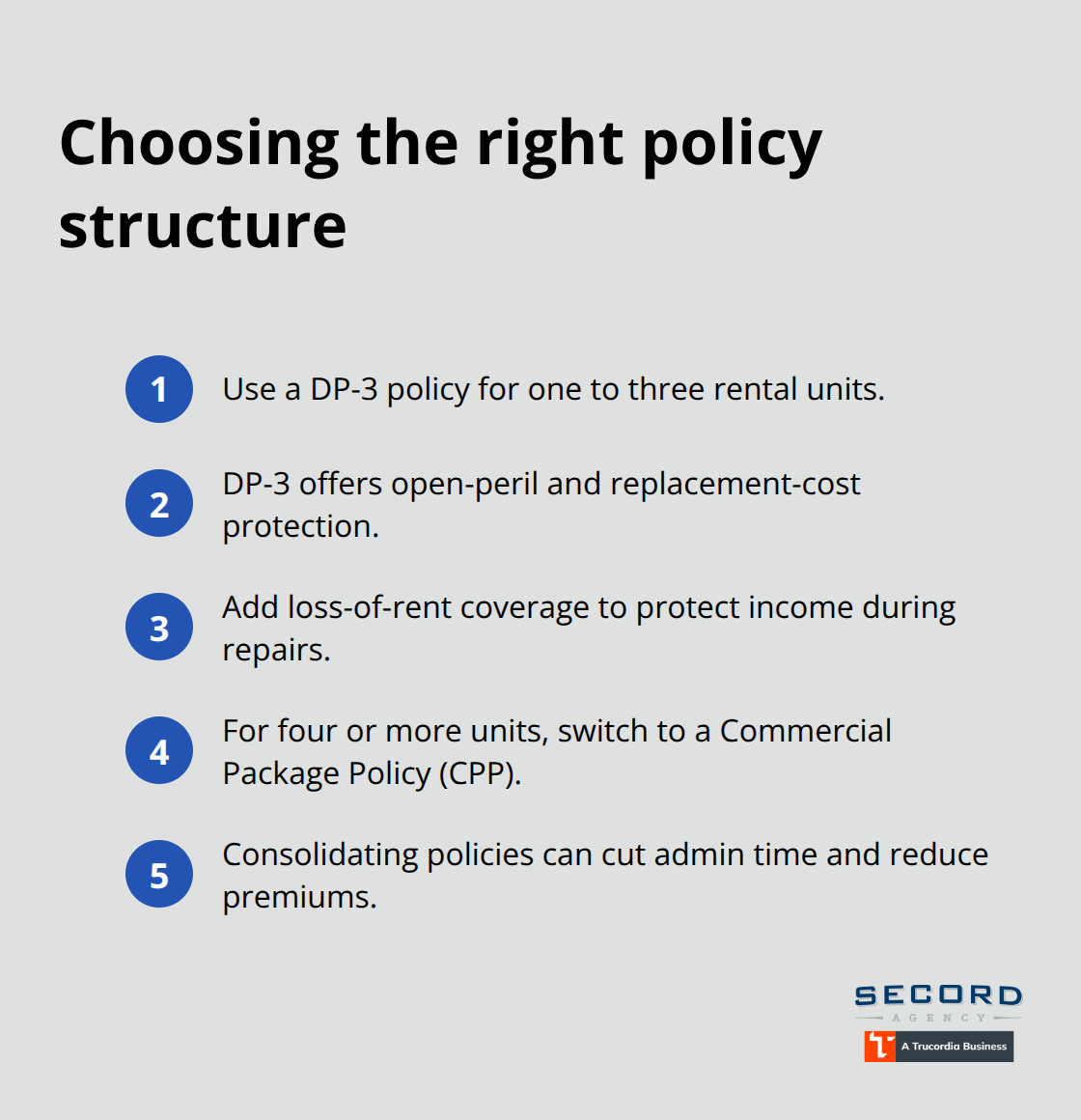

Single-property landlords and portfolio owners need fundamentally different policy structures, and selecting the wrong one leaves you either overpaying or underinsured. If you own one to three rental units, a Dwelling Property 3 (DP-3) policy provides open-peril coverage on the structure with replacement-cost settlement, meaning you receive protection against damage unless the policy explicitly excludes it. DP-3 policies typically cost more upfront than DP-1 or DP-2 options, but they eliminate the guesswork about which perils are covered-everything is in unless excluded. The real financial advantage appears during claims: replacement cost means the insurer pays what it actually costs to rebuild in 2026 dollars, not what the property was worth ten years ago. When you add loss-of-rent coverage to a DP-3, you protect both your asset and your income stream simultaneously.

For properties with four or more units, abandon the residential dwelling forms entirely and move to a Commercial Package Policy (CPP). A CPP bundles property, general liability, equipment breakdown, and optional umbrella coverage under one master policy, which reduces your administrative overhead and often delivers cost savings. One Washington landlord who consolidated eleven separate DP-3 policies into a single CPP saved approximately 40 hours annually on policy management alone, plus achieved measurable premium reductions by consolidating with one carrier.

Deductible Strategy and Premium Optimization

Your deductible strategy matters more than most landlords realize-increasing your deductible from $1,000 to $2,500 typically reduces premiums by 8–15%, but only if you maintain a liquid reserve fund equal to your deductible amount. Some sophisticated investors use schedule deductibles, meaning different properties carry different deductible levels based on their risk profiles; this approach can deliver roughly 14% aggregate premium savings when paired strategically across a mixed portfolio. The key is matching your deductible to your financial capacity-a higher deductible saves money only if you can actually cover it without disrupting operations.

Liability Limits That Match Washington Verdict Reality

Start with a baseline of $500,000 per occurrence for single properties and $1 million for multi-unit portfolios; many Washington landlords then layer an umbrella policy on top for an additional $1–5 million in coverage. Umbrella policies cost far less than you’d expect-often $200–400 annually per $1 million of coverage-and they protect you from the catastrophic judgment that could force you to liquidate property or declare bankruptcy. The verdict environment in Washington has shifted dramatically, and carriers now use granular climate-risk data and historical claim patterns to price premises liability specifically. Properties near transit corridors or in high-foot-traffic areas warrant higher liability limits than isolated rural rentals, yet most landlords apply a one-size-fits-all approach.

Water Backup and Specialized Endorsements

Water backup endorsements deserve specific attention because roughly 28% of water-related claims in Spokane County last year stemmed from sewer or drain failures-a peril that standard policies exclude entirely. Adding this endorsement costs between $50–150 annually but protects against claims that regularly exceed $5,000 in damage. Earthquake and flood coverage require separate decisions based on your property location and lender requirements; if your lender mandates earthquake or flood coverage, refusing it means your policy won’t respond to claims, leaving you personally liable for reconstruction costs.

Selecting an Agent Who Understands Washington

Selecting an agent matters more than most landlords acknowledge because Washington’s regulatory landscape, climate risks, and underwriting standards differ substantially from national norms. An agent who understands the Residential Landlord-Tenant Act, local code requirements, and carrier appetite for earthquake and wildfire risk will identify coverage gaps that online quote tools miss entirely. A local agent conducts an annual policy review after major changes like renovations, new equipment, or tenant transitions, ensuring your coverage limits reflect current replacement costs rather than outdated valuations. When you report a loss, a Washington-licensed agent coordinates with your carrier, tracks claim status, and ensures you receive the documentation lenders require for refinancing or portfolio transactions. Request quotes from at least three carriers, and during those conversations, ask each agent how they handle water backup claims, whether they offer Firewise discount programs, and what happens to your coverage during extended vacancy periods. Many carriers restrict coverage after 30–60 days of vacancy, making this detail essential if you anticipate turnover or seasonal closures. Verify that your insurer carries an A- or higher rating from AM Best, indicating financial stability to pay claims when losses occur. Washington’s Office of the Insurance Commissioner publishes disciplinary actions against carriers, so reviewing those records before placement helps you avoid companies with patterns of claim denials or delayed responses.

Final Thoughts

Commercial landlord insurance in Washington protects far more than your building-it protects your income, your assets, and your ability to weather the unexpected. The coverage gaps that seem minor during underwriting become catastrophic during claims, which is why matching your policy structure to your specific property type and risk profile matters more than chasing the lowest premium. A single-property owner needs different protection than a portfolio investor, and both need coverage that accounts for Washington’s earthquake exposure, wildfire risk, and flood patterns that extend well beyond mapped zones.

When you request quotes, ask each agent directly about water backup coverage, vacancy restrictions, and whether they offer Firewise discounts-these details separate adequate protection from gaps that will cost you thousands during claims. Request quotes from multiple carriers so you can compare not just price but also coverage terms, deductible options, and the agent’s responsiveness to your questions. A carrier with an A- or higher AM Best rating and a track record of fast claims handling in Washington matters more than saving $200 annually on a policy that denies your loss.

We at Secord Agency – A Trucordia Business understand Washington’s landlord landscape because we work across the state every day. Our team shops multiple carriers to find commercial landlord insurance in Washington that actually fits your portfolio, then pairs competitive rates with local service that simplifies both quotes and claims. Contact us for a customized quote and let’s build protection that matches your actual risks rather than templates.