Washington Homeowners Policy Options: A Practical Guide to Coverage

Washington homeowners face unique insurance challenges that most standard policies don’t fully address. From earthquake risks to heavy rainfall, your coverage needs differ significantly from other states.

We at Secord Agency – A Trucordia Business created this guide to help you navigate Washington homeowners policy options with confidence. You’ll learn what coverage is mandatory, how to spot gaps in your protection, and which risks deserve special attention in the Pacific Northwest.

What’s Actually Required for Washington Homeowners

Washington state doesn’t legally mandate homeowners insurance, but your mortgage lender certainly does. If you skip coverage, your lender will purchase lender-placed insurance on your behalf-and you’ll pay significantly more for substantially less protection. Lender-placed policies typically cost 50 to 100 percent higher than standard homeowners policies while offering minimal coverage. That’s the first hard truth: you’re getting insurance either way, so choosing your own policy makes financial sense. Your lender requires you to maintain coverage at all times, and any lapse in protection gives them legal grounds to force their own policy onto your property.

Your Policy Must Cover the Dwelling and Liability

Standard homeowners coverage in Washington includes four core components: dwelling protection, personal property coverage, liability protection, and additional living expenses. Dwelling coverage pays to repair or rebuild your home’s structure after a covered loss, while personal property coverage protects your belongings from fire, theft, wind, and vandalism. Liability coverage is where most homeowners underestimate their exposure. According to the Insurance Information Institute, liability claims can reach six figures when someone is seriously injured on your property. Medical payments coverage, typically included at $1,000 minimum, helps cover immediate medical expenses for guests, but you should strongly consider higher liability limits between $100,000 and $500,000 depending on your assets and neighborhood. Additional living expenses coverage reimburses temporary housing, meals, and other costs if your home becomes uninhabitable after a covered event.

Washington’s Weather and Geology Create Specific Coverage Needs

Wind and hail damage accounts for approximately 39.4 percent of all homeowners insurance claims in Washington, according to the Insurance Information Institute. Freezing and water damage represents another 23.5 percent of claims, primarily from burst pipes during winter months. Lightning strikes and fires make up about 24.8 percent of claims. These aren’t theoretical risks-they’re the actual breakdown of what homeowners file claims for every year. Standard policies cover all three categories, but coverage gaps emerge quickly. Mold remediation, for example, is typically excluded unless the mold results directly from a covered peril like a burst pipe, and even then, many policies cap mold coverage at $5,000 to $10,000. Earthquake coverage is completely absent from standard policies and requires a separate endorsement or rider. Flood damage from rising groundwater or overflowing bodies of water is also excluded, forcing you to purchase separate flood insurance through the National Flood Insurance Program if you’re in a high-risk zone. Landslides, common in parts of Washington, are excluded from standard policies unless you add specific earth movement coverage.

Why You Need a Local Agent to Spot Your Coverage Gaps

Shopping for homeowners insurance online might feel convenient, but Washington’s specific risks demand personalized guidance. An independent agent who understands Pacific Northwest conditions can identify which endorsements matter most for your property and location. A local agent can shop multiple carriers to find coverage that actually fits your home and budget. We help you understand what your standard policy excludes and which add-ons prevent expensive gaps. This personalized approach takes more time than a generic quote, but it protects you from discovering coverage holes after a loss occurs.

Picking the Right Policy Type for Your Washington Home

HO-3 Policies Cover All Perils Except Those Explicitly Excluded

HO-3 policies dominate the Washington market because they cover all perils except those specifically excluded, which means you get broad protection without listing every single covered event. This differs fundamentally from older HO-2 policies that only cover named perils, forcing you to prove that your specific loss falls into a pre-approved category. If your roof sustains damage from an unusual weather event, an HO-3 policy covers it unless explicitly excluded; an HO-2 policy requires you to verify that exact peril was named in your contract. The National Association of Insurance Commissioners data shows HO-3 policies represent the standard across Washington and most of the country for good reason.

However, HO-3 policies still exclude earthquakes, floods, and earth movement, which means you cannot escape those gaps by shopping around-you must add separate coverage. Wind and hail damage, which represents 2.8 percent of Washington claims, is included in all standard HO-3 policies, so this coverage doesn’t differentiate between insurers. Where carriers diverge is in water damage exclusions, mold limits, and how aggressively they enforce maintenance requirements. Some insurers deny claims for frozen pipes if your home lacks adequate heat during winter, while others apply this restriction only to seasonal properties.

Ask Carriers Directly About Their Specific Exclusions

You need to ask each carrier directly about their specific exclusions for water backup, sewer damage, and mold remediation rather than assuming all HO-3 policies work identically. Mold remediation, for example, is typically excluded unless the mold results directly from a covered peril like a burst pipe, and even then, many policies cap mold coverage at $5,000 to $10,000. Landslides, common in parts of Washington, are excluded from standard policies unless you add specific earth movement coverage. This personalized approach to comparing carriers takes more time than collecting generic quotes, but it protects you from discovering coverage holes after a loss occurs.

Match Deductibles and Limits Across All Quotes

Comparing quotes requires more than collecting numbers and picking the lowest premium. Request quotes with identical deductibles, dwelling limits, and liability amounts so you’re actually comparing apples to apples-a $500 deductible quote from one carrier isn’t comparable to a $1,000 deductible quote from another. The Washington State Department of Insurance recommends obtaining at least three quotes before deciding. Deductible selection directly impacts your monthly payment, with higher deductibles typically reducing premiums by 15 to 25 percent, but only choose a higher deductible if you can actually pay it after a loss without financial hardship. A $2,500 deductible saves money monthly but creates real risk if you can’t cover that amount when your roof needs repair.

Set Dwelling Coverage to Match Replacement Cost, Not Market Value

Dwelling coverage should match your home’s replacement cost, not its market value-a home worth $400,000 might cost $550,000 to fully rebuild due to labor and material costs, and underinsuring by even 20 percent can trigger coinsurance penalties that reduce claim payments significantly. Personal property coverage typically runs at 50 to 70 percent of your dwelling limit, but if you own jewelry, art, collectibles, or high-value tools, standard policies cap coverage on those items between $1,500 and $2,500 per category. You’ll need scheduled personal property riders for anything beyond those limits. Liability coverage between $100,000 and $300,000 makes sense for most Washington homeowners, though higher limits cost surprisingly little extra-adding umbrella liability coverage for an additional $1 million in protection typically costs $150 to $300 annually.

Evaluate How Carriers Handle Claims and Local Service

When you receive quotes, ask each carrier how they handle claim disputes and whether they have local adjusters in Washington, because processing speed matters enormously when your home is damaged and you need temporary housing covered immediately under additional living expenses. An independent agent who understands Pacific Northwest conditions can identify which endorsements matter most for your property and location and shop multiple carriers to find coverage that actually fits your home and budget. This local expertise becomes invaluable when you file a claim and need someone who knows Washington’s specific risks and how different insurers respond to them.

Washington-Specific Risks That Standard Policies Leave Exposed

Earthquake Coverage Protects Against the Inevitable Pacific Northwest Threat

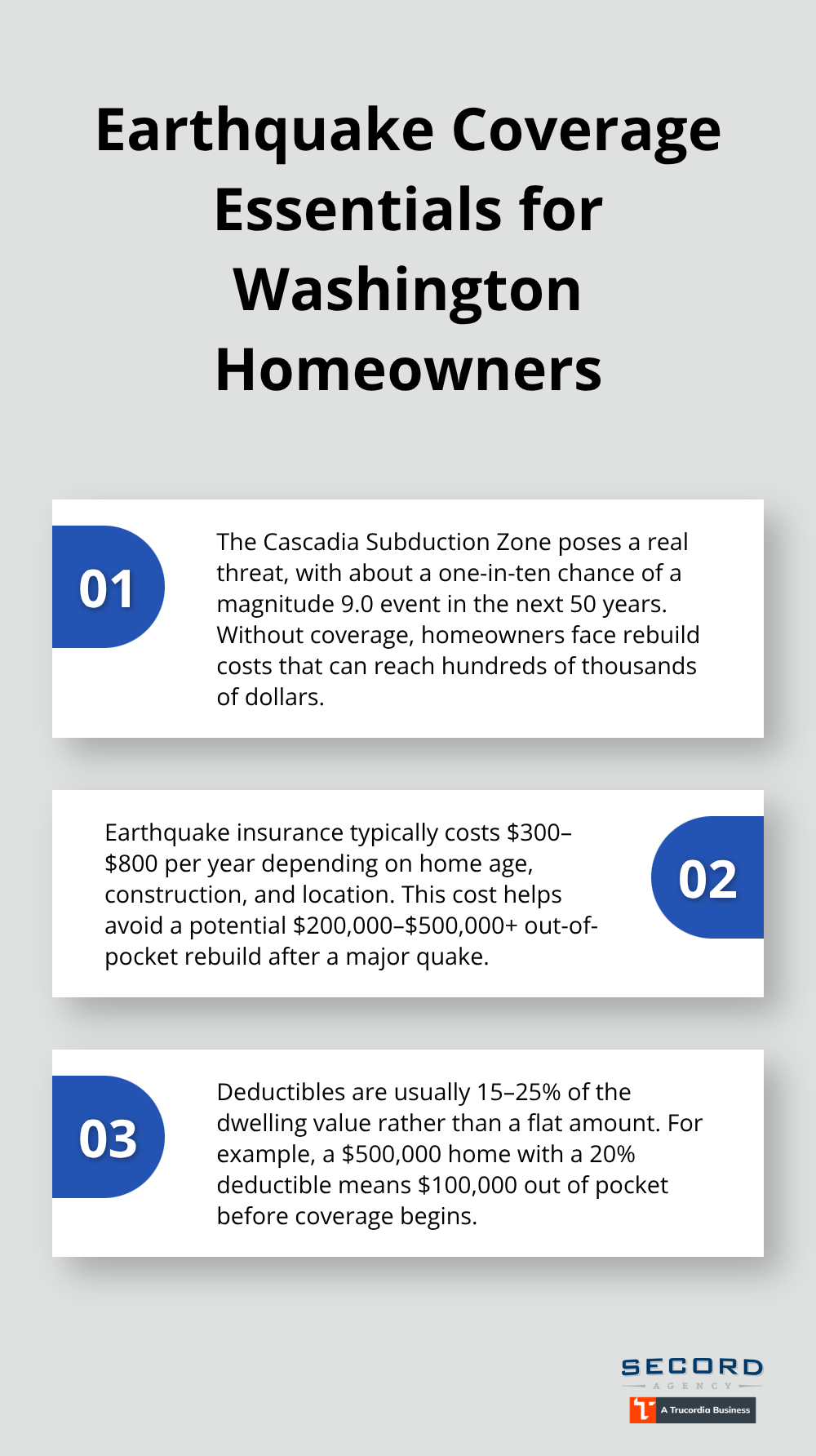

Earthquake damage isn’t covered by any standard HO-3 policy sold in Washington, which means your home sits completely unprotected against the Cascade Subduction Zone threat that seismologists consider inevitable. The chances that an earthquake as large as magnitude 9.0 will occur along the zone within the next 50 years are about one in ten. Adding earthquake insurance costs between $300 and $800 annually depending on your home’s age, construction type, and location, but the alternative is facing a $200,000 to $500,000+ rebuild bill entirely out of pocket.

Earthquake coverage works differently than standard homeowners insurance because it typically includes a 15 to 25 percent deductible rather than a flat dollar amount, meaning you absorb that percentage of damage before coverage kicks in. A home valued at $500,000 with a 20 percent deductible means you pay $100,000 before insurance covers anything, so this coverage only makes financial sense if you can actually afford that deductible when an earthquake strikes.

Flood Insurance Addresses Water Damage That Standard Policies Exclude

Flood insurance requires equally direct thinking. If you’re in a high-risk flood zone according to FEMA maps, your lender will mandate separate flood coverage through the National Flood Insurance Program, but even outside those zones, heavy rainfall and burst pipes create water damage scenarios that standard policies exclude. The distinction matters enormously: sudden internal events like a burst pipe are covered under standard policies, but gradual seepage, long-term leaks, or water intrusion from outside are excluded.

Flooding from rising groundwater or overflowing rivers and streams requires flood insurance, which costs $400 to $1,200 annually for typical Washington homes. Understanding your total insurance cost requires seeing all three pieces together-homeowners, earthquake, and flood-rather than evaluating homeowners coverage in isolation.

Wind and Storm Damage Protection Depends on Your Roof’s Condition

Wind and storm damage protection is already built into standard HO-3 policies since wind and hail account for 39.4 percent of Washington claims according to the Insurance Information Institute, but this coverage gap appears in specific situations. If your roof is over 20 years old or in poor condition, some carriers restrict wind coverage or charge higher premiums, so you need to disclose your roof’s actual age and condition when getting quotes.

Metal roofs and impact-resistant shingles can reduce premiums by 10 to 15 percent because they withstand hail and wind better than standard asphalt shingles. Older homes with wood shake roofs face additional restrictions because insurers view them as fire hazards in wildfire-prone areas, potentially excluding fire coverage entirely unless you upgrade.

Bundle Earthquake and Flood Quotes With Your Homeowners Policy

Getting earthquake and flood quotes at the same time you shop homeowners policies makes financial sense because bundling discounts sometimes apply. An independent agency that shops multiple carriers can identify which combination of coverage and carriers produces the lowest total cost while maintaining adequate protection across all three policy types.

Final Thoughts

Washington homeowners face a straightforward reality: selecting your own policy beats allowing your lender to impose expensive, minimal coverage on your property. The Washington homeowners policy options available to you range from basic HO-3 coverage to fully customized packages with earthquake, flood, and specialized endorsements, but your specific home’s location, age, and financial situation determine the right choice. Start by setting your dwelling coverage at replacement cost rather than market value, then add liability protection between $100,000 and $300,000 based on your assets.

Request quotes with identical deductibles and limits from at least three carriers so you actually compare equivalent policies. Ask each insurer directly about their specific exclusions for water damage, mold, and sewer backup instead of assuming all HO-3 policies work identically. Then add earthquake and flood quotes to see your total annual insurance cost across all three policy types, because evaluating homeowners coverage alone ignores the gaps that will cost you tens of thousands after a loss.

Review your coverage annually, especially after home improvements or renovations, since underinsuring by even 20 percent triggers coinsurance penalties that reduce claim payments significantly. We at Secord Agency – A Trucordia Business shop multiple carriers to find Washington homeowners policy options that fit your home and budget while maintaining adequate protection against Pacific Northwest risks. Contact us for personalized guidance on earthquake coverage, flood insurance, and the homeowners policy that protects your most valuable asset.