Vacation Rental Liability Insurance: Guarding Your Short-Term Property

Your standard homeowners insurance policy wasn’t designed for guests paying to stay in your home. That gap between personal coverage and rental activity creates real financial risk.

At Secord Agency – A Trucordia Business, we see property owners lose thousands because their policies exclude rental income and guest injuries. Vacation rental liability insurance fills those gaps and protects what you’ve built.

Why Your Homeowners Policy Won’t Cover Your Rental Business

The Business Activity Exclusion

Homeowners insurance explicitly excludes income from short-term rentals. When you rent your property on Airbnb, Vrbo, or Booking.com, you operate a business, not a personal residence. Your standard policy treats this as commercial activity and denies claims tied to guest injuries, property damage caused by renters, or lost rental income. This isn’t a gray area-it’s a direct violation of your policy terms. If a guest breaks a window, slips on your stairs, or damages furniture, your homeowners insurer will reject the claim outright.

The Real Cost of Coverage Gaps

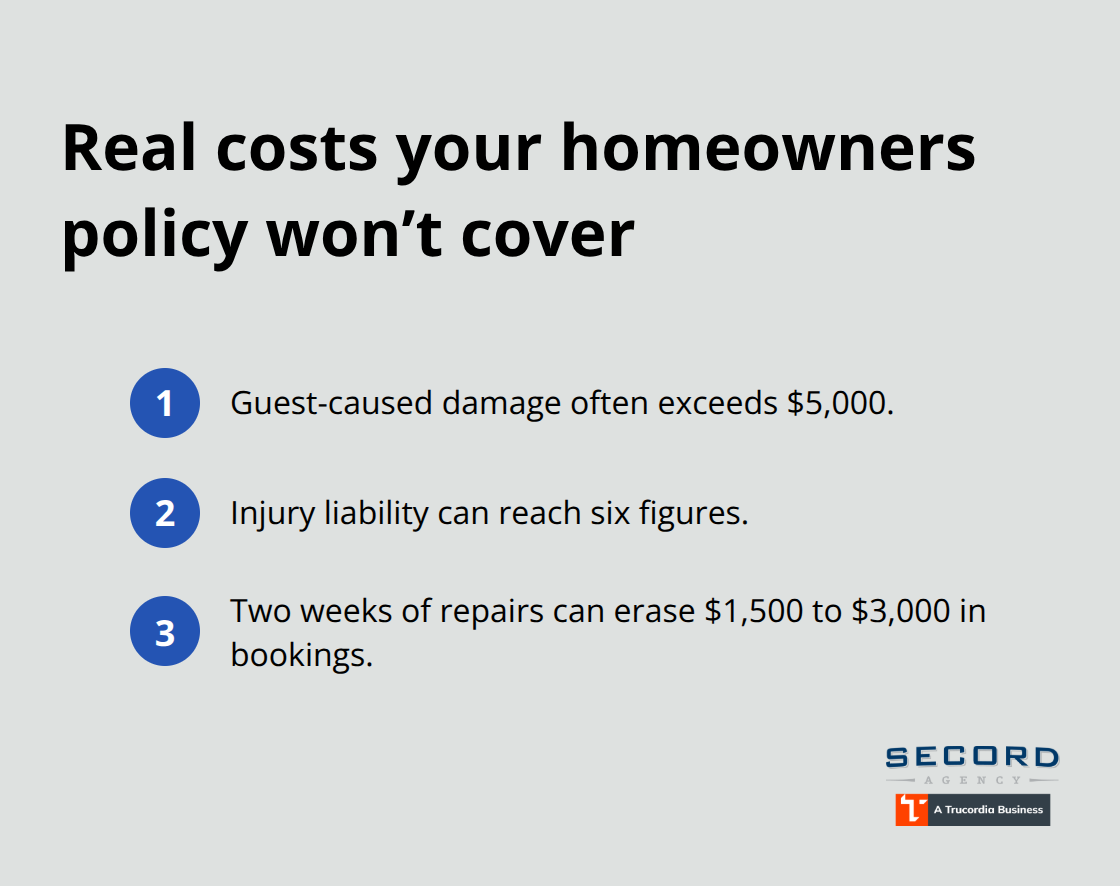

The financial exposure runs deep. Guest-caused property damage claims frequently exceed $5,000, and liability claims from injuries can reach six figures. Without proper coverage, you absorb these costs directly from your own pocket. Additionally, if a covered loss like a fire makes your property uninhabitable, homeowners insurance won’t compensate you for the rental income you lose while repairs happen.

A two-week renovation could cost you $1,500 to $3,000 in lost bookings, depending on your nightly rate.

Rental-Specific Risks Your Policy Ignores

Standard policies also don’t cover liability scenarios specific to rentals-bed bug infestations, communicable diseases from shared amenities like hot tubs, or injuries that occur because you failed to disclose hazards to guests. These gaps exist because homeowners policies assume you’re the only occupant managing the property. Your insurer never anticipated the liability exposure that comes with rotating guests, shared spaces, and commercial operations.

Why Vacation Rental Insurance Matters

Vacation rental insurance addresses these exact risks with commercial general liability coverage, property damage protection, and loss of income coverage designed for rental operations. The Global Vacation Rental Platform Liability Insurance market is projected to grow at a CAGR of 11.2% between 2025 and 2033, reaching an estimated value of USD 6.51 billion by 2033, reflecting how essential specialized coverage has become. Property owners who continue relying on homeowners insurance are betting against themselves-and losing that bet costs real money.

The types of liability coverage available for vacation rentals go far beyond what homeowners policies offer, and understanding these options helps you build protection that actually matches your rental operation.

Types of Liability Coverage for Vacation Rentals

Commercial General Liability: The Foundation of Your Protection

Commercial general liability coverage stands as the foundation of vacation rental protection, and it operates differently than the personal liability included in homeowners policies. When a guest injures themselves on your property or damages your furnishings, commercial liability covers medical expenses, legal defense costs, and settlements up to your policy limits. Most vacation rental insurers recommend a minimum of at least $1 million in liability coverage, though $2 million offers stronger protection if your budget allows. The difference matters significantly: a guest slip-and-fall with a broken arm might cost $15,000 to $30,000 in medical bills and legal fees, while a more severe injury claim can exceed $100,000. Your coverage limit determines how much of that burden falls on you versus your insurance carrier.

Property damage liability specifically protects you when guests break windows, damage walls, or destroy furniture. This coverage reimburses repair or replacement costs without depleting your personal savings. Unlike homeowners insurance, vacation rental policies treat guest-caused damage as a covered loss, not a business exclusion.

Specialized Add-Ons That Prevent Financial Disaster

Beyond standard liability, specialized add-ons prevent the financial disasters that standard policies ignore. Bed bug and flea liability coverage warrants the extra premium because infestations lead to six-figure settlements when guests claim health problems or sue over spreading infestations to their own homes. Communicable disease coverage protects you if a guest contracts Legionnaires’ disease from a hot tub or similar amenity on your property-without this coverage, you face significant exposure.

Loss of income coverage compensates you for rental revenue lost when a covered event like fire or water damage makes your property uninhabitable during repairs. This protection shields your cash flow during downtime. Assault and battery coverage, including sexual assault claims, often gets excluded from standard policies, so verify your vacation rental policy includes it before signing.

Invasion of privacy coverage addresses liability from improper guest access, unauthorized entry by cleaners, or camera placement concerns that trigger lawsuits.

How Platform Protections Fit Into Your Coverage Strategy

Platform-provided protections like Airbnb AirCover offer up to $3 million in damage protection and $1 million in liability, but these serve as supplemental layers, not replacements for your own policy. Vrbo and Booking.com provide up to $1 million in liability coverage as additional protection, yet gaps remain between what platforms cover and what your business actually needs. Treating platform protections as bonus coverage while building your standalone policy to match your property’s specific risks and revenue profile creates the strongest defense. Understanding which specific liability scenarios your platform covers-and which ones fall to you-determines whether your protection strategy actually works when a claim happens.

Finding the Right Vacation Rental Insurance Policy

Coverage Limits That Protect Your Financial Future

Coverage limits vary dramatically across vacation rental policies, and the difference between coverage limits between $1 million and $2 million in liability protection determines whether a serious claim bankrupts you or gets handled by insurance. North America accounts for over 38% of the global vacation rental insurance market, roughly $930 million in 2024, driven partly by property owners learning the hard way that underinsurance costs more than adequate premiums. When you compare policies, focus on three measurable factors: the liability ceiling, whether loss of income coverage includes sub-limits that cap payouts, and how guest property damage allocates between your policy and the guest’s insurance. A $1 million limit sounds substantial until a guest suffers a spinal injury requiring surgery and ongoing care, which can easily exceed $500,000 in medical costs plus legal fees.

How Property Features and Rental Frequency Affect Your Costs

Location and property amenities directly impact your premium costs. A rental with a hot tub, pool, or trampoline carries higher risk than a basic apartment, so insurers charge 20–40% more for these features. Your rental frequency matters too-occasional rentals cost less than full-time operations. If you rent your property 90 days annually versus 300 days, you’ll see a significant premium difference. Deductibles range from $500 to $2,500, and a higher deductible lowers your monthly cost but increases your out-of-pocket expense when you file a claim. Installing water sensors, temperature monitors, and smoke detectors can lower premiums by 5–15% because these devices reduce claim frequency and allow faster emergency response. Request quotes from at least three providers and compare not just the premium but the specific exclusions each policy includes.

Working with an Agent to Verify Your Coverage

An insurance agent who understands vacation rental operations prevents costly oversights that self-service online quotes miss. An agent verifies whether you can rent on multiple platforms under the same policy, confirms that loss of income coverage applies during your specific booking patterns, and ensures assault and battery coverage is included rather than excluded. Many property owners discover too late that their policy excludes bed bug liability or that communicable disease coverage doesn’t apply to their hot tub setup. When you contact an agent, bring your property details: square footage, amenities, annual rental days, platforms you use, and your target coverage limits. This information allows the agent to identify which carriers offer the best rates and features for your situation.

Ask whether your current homeowners policy can be modified or whether a standalone vacation rental policy makes more sense-sometimes a commercial homeowners policy designed specifically for short-term rentals costs less than layering a rider onto your existing policy. Request written confirmation from the underwriter for the specific scenarios you’re relying on, and keep that documentation in case you need to reference it during a claim. The agent should also explain what happens if your property becomes uninhabitable: does loss of income coverage begin immediately, or is there a waiting period? Does it cover your actual lost bookings or a predetermined daily amount? These details determine whether your policy actually protects your cash flow when disaster strikes.

Final Thoughts

Your vacation rental operates in a liability landscape that standard homeowners insurance simply doesn’t address. The coverage gaps we’ve outlined-from guest injuries to lost rental income to bed bug infestations-represent real financial exposure that grows with every booking. Vacation rental liability insurance protects you from absorbing a $50,000 claim yourself and instead transfers that risk to your insurer.

Start by gathering your property details: square footage, amenities like pools or hot tubs, annual rental days, and the platforms you use. Contact an insurance agent who understands vacation rental operations and can compare policies from multiple carriers rather than steering you toward a single option. Request written confirmation from your underwriter about the specific scenarios you’re relying on-guest injuries, property damage, loss of income during repairs-and keep that documentation accessible.

We at Secord Agency – A Trucordia Business work with property owners across Washington to build vacation rental coverage that matches your operations. Contact Secord Agency today to discuss your vacation rental liability insurance needs and receive a quote that reflects your specific property and risk profile.

As a local insurance agency, we strive to provide answers to all your insurance queries. When it comes to renters insurance, there’s a common misconception that your landlord’s insurance policy will cover any unfortunate incidents that may occur while renting an apartment, home, or condo.

As a local insurance agency, we strive to provide answers to all your insurance queries. When it comes to renters insurance, there’s a common misconception that your landlord’s insurance policy will cover any unfortunate incidents that may occur while renting an apartment, home, or condo.