Teen Auto Insurance Washington: A Practical Guide for New Drivers

Getting your teen behind the wheel comes with real financial consequences. Teen auto insurance in Washington costs significantly more than coverage for adult drivers, and understanding why helps you find better rates.

We at Secord Agency – A Trucordia Business know that parents need practical strategies to manage these costs without cutting corners on protection. This guide walks you through Washington’s requirements, proven discount opportunities, and smart policy decisions that actually work.

What Washington Requires and Why Teen Premiums Cost So Much

Washington’s Minimum Coverage and Your Real Exposure

Washington state mandates minimum liability coverage of $25,000 per person and $50,000 per accident for bodily injury, plus $10,000 for property damage. These baseline limits sound adequate until a serious crash happens-one collision can easily exceed these thresholds, leaving you financially exposed. If your teen finances or leases a vehicle, the lender requires comprehensive and collision coverage on top of these minimums, which significantly raises the total cost. The reality is that minimum coverage alone leaves most families vulnerable, yet it’s what many parents choose to save money upfront.

Why Teen Drivers Command Higher Premiums

Teen drivers cost more because insurance companies have concrete data showing teen drivers crash at nearly four times the rate of drivers aged 20 and older per mile driven. In Washington specifically, a 16-year-old averages $6,651 per year for full coverage, while a 19-year-old averages $3,838 annually, showing how risk perception drops dramatically with age and experience. Male teen drivers in Washington face even steeper premiums than females-a 16-year-old boy averages $6,947 yearly compared to $6,354 for girls, a gap of roughly $593. The first months after licensure carry the highest crash risk, so insurers price policies accordingly.

How Insurers Assess Your Teen’s Individual Risk

Insurers assess teen risk through several concrete factors: whether the vehicle is financed or owned outright, the specific make and model, your teen’s driving history during the permit phase, their academic performance if they qualify for good student discounts, and their location within Washington (premiums vary significantly by ZIP code). A Honda Accord costs roughly $1,919 annually for full coverage, while a BMW 330i runs about $2,398, showing how vehicle choice directly impacts rates before your teen ever gets behind the wheel.

Getting Accurate Quotes and Comparing Carriers

To get accurate quotes tailored to your situation, you need your teen’s license number, the vehicle’s VIN, driving history details, employment status, and annual mileage estimates-then compare quotes across at least three carriers, since the difference between the cheapest and most expensive options for identical coverage can exceed $2,000 annually. PEMCO offers the lowest average teen rates in Washington at approximately $3,514 yearly, while Travelers averages about $4,100 and Farmers around $4,670 for full coverage. Shopping multiple carriers reveals substantial savings opportunities that most parents miss when they accept the first quote they receive.

Proven Discounts That Actually Reduce Your Teen’s Premium

Defensive Driving Courses and Verified Discounts

Defensive driving courses deliver measurable savings, but only from insurers that recognize them. The Washington Traffic Safety Commission offers accredited courses that many carriers discount, typically saving $50 to $100 annually, though the real value emerges over time as your teen maintains a clean record. You must confirm that your insurer honors this discount before enrollment, since not all carriers participate. The discount matters only if your insurance company accepts it, so contact your agent first.

Good Student Discounts That Compound Over Years

Good student discounts reward a B average or higher and generally reduce premiums by 10 percent or more depending on the carrier. At age 16 in Washington, your teen averages $6,651 yearly for full coverage, so a 10 percent discount saves roughly $665 annually. This discount persists through college if your teen maintains academic performance, making it one of the few discounts that compounds over multiple years. Strong grades translate directly into lower insurance costs, creating a tangible financial incentive for academic success.

Usage-Based Insurance Programs That Track Real Behavior

Usage-based insurance programs like Snapshot or similar telematics offerings track actual driving behavior and reward safe habits with discounts ranging from 10 to 30 percent. Your teen earns discounts by avoiding hard braking, speeding, and late-night driving, with feedback delivered through a smartphone app that shows real-time performance. These programs align your teen’s actual driving with premium reductions, making the connection between safe habits and savings immediate and visible.

Bundling Policies for Maximum Savings

Bundling auto coverage with your home or renters policy cuts combined premiums by 15 to 25 percent, a benefit that often outweighs the hassle of consolidating carriers. When you add your teen to your existing policy, bundling becomes even more powerful since the insurer applies discounts across all lines. Compare bundled quotes from at least two carriers, as some bundle more aggressively than others. PEMCO in Washington averages $3,514 yearly for teen full coverage, significantly lower than the statewide average of $5,244, making rate shopping non-negotiable.

Stacking Discounts for Substantial Savings

Combining a good student discount, a usage-based program, and bundling can reduce your 16-year-old’s premium from $6,651 to roughly $4,500 or lower, a savings of over $2,100 annually that most parents never pursue because they don’t know these options exist or fail to ask. Your teen’s actual premium depends on the specific vehicle, location within Washington, and which discounts your chosen carrier offers. The next step involves deciding whether to add your teen to your existing policy or purchase separate coverage-a choice that significantly impacts both cost and coverage protection.

Adding Your Teen to Your Policy vs. Getting Separate Coverage

Choosing Between Adding Your Teen or Buying Separate Coverage

Adding your teen as a named driver to your existing policy costs substantially less than purchasing them a separate policy, and this difference compounds over multiple years. A 16-year-old added to a parent’s policy runs approximately $4,046 annually, while an 18-year-old on their own policy costs about $6,968 yearly according to Insure.com data. The gap exists because insurers view a teen driving the family vehicle under parental supervision as lower risk than an independent teen driver. However, this advantage disappears if your teen owns a vehicle registered solely in their name or if they live outside Washington as a non-resident permit holder-situations where a separate policy becomes necessary. When deciding between adding your teen or purchasing separate coverage, gather quotes from at least two carriers showing both options, since some insurers price these scenarios differently and the savings opportunity varies.

Informing Your Insurer and Building Coverage History

If your teen will regularly drive the family car, inform your insurer about usage patterns and confirm the policy covers learner’s permit driving before your teen gets behind the wheel, since coverage gaps during the permit phase create serious problems later. Starting insurance coverage during the learner’s permit phase builds a positive driving history that insurers view favorably when your teen transitions to a licensed driver, often resulting in lower premiums compared to teens who delay coverage until licensure. Your insurer needs accurate information about how frequently your teen will operate the vehicle and under what conditions to properly assess risk and apply appropriate coverage.

Controlling Crash Risk Through Active Monitoring

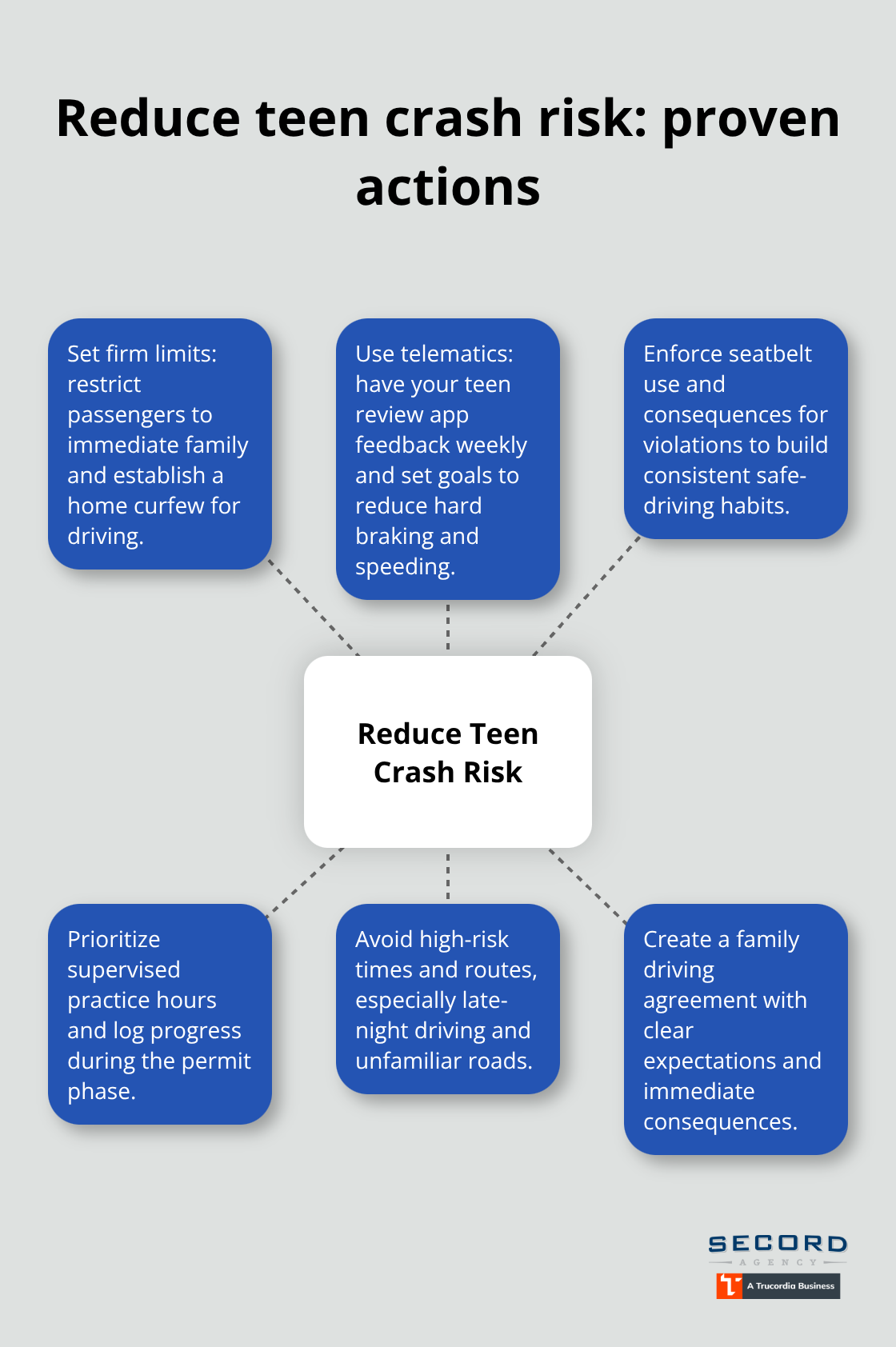

Managing your teen’s actual driving behavior matters far more than any discount or policy structure you choose. In-vehicle monitoring devices combined with feedback shared between your teen and you reduce crash risk substantially, particularly when alerts address speeding and seatbelt use. Usage-based insurance programs accomplish this feedback loop through smartphone apps that show real-time driving performance, but only if your teen engages with the data rather than ignoring the alerts. Enforce restrictions beyond what Washington’s graduated driver licensing requires: limit passengers to immediate family members, prohibit driving between 8 p.m. and 5 a.m., and track supervised practice hours during the permit phase to document safe habits.

Handling Accidents and Maintaining Your Record

When accidents or violations occur, report them to your insurer within the required timeframe (typically 24 to 72 hours), since delayed reporting damages credibility and can complicate claims. After an at-fault accident, expect your premium to increase roughly 48 percent according to Bankrate data, making accident prevention your most powerful cost-control tool. Timely reporting protects your coverage and demonstrates responsibility to your insurer, which matters when your teen transitions to independent driving.

Reviewing Coverage and Shopping Rates Annually

Schedule annual policy reviews with your agent to verify coverage remains adequate as your teen gains experience, confirm all discounts apply, and shop competing carriers since premiums drop as your teen ages and maintains a clean record. Small rate differences compound over years of coverage, so comparing at least two carriers annually identifies savings opportunities that most families overlook. Your teen’s risk profile improves with each year of safe driving, and your policy should reflect that improvement through lower premiums.

Final Thoughts

Teen auto insurance in Washington demands action across multiple fronts, but the payoff justifies the effort. Start by collecting your teen’s license details, the vehicle VIN, driving history, and employment status, then request quotes from at least three carriers to identify the lowest available rates. A 16-year-old averages $6,651 annually for full coverage, yet strategic choices-good student discounts, usage-based programs, and bundling-can reduce this to $4,500 or less, representing real money you control through informed decisions.

Your teen’s actual driving behavior matters more than any discount or policy structure you select. Enforce restrictions stricter than Washington’s graduated driver licensing requires: limit passengers, prohibit nighttime driving, and use in-vehicle monitoring devices that provide real-time feedback on speeding and unsafe habits. Teen drivers crash at nearly four times the rate of drivers aged 20 and older, but this risk drops dramatically when parents actively manage driving conditions and teens face immediate consequences for unsafe behavior.

We at Secord Agency – A Trucordia Business help families navigate teens auto insurance Washington by shopping multiple carriers to deliver competitive rates paired with personalized advice for your specific situation. Contact us at secordagency.com to discuss your teen’s coverage options and identify discounts you may have missed. Schedule annual reviews as your teen gains experience, since premiums drop with each year of safe driving and a clean record.