Homeowners Insurance Overview Seattle: What You Need to Know

Homeowners insurance in Seattle protects your most valuable asset, but understanding your coverage options can feel overwhelming. We at Secord Agency – A Trucordia Business have helped countless Seattle homeowners navigate their policies and find the right protection for their needs.

This homeowners insurance overview Seattle covers the coverage types you need to know about, the factors that impact your rates, and how to select a policy that actually fits your situation.

What Does Your Homeowners Policy Actually Cover

Dwelling Coverage and Structural Protection

Your standard homeowners policy in Seattle covers four essential areas, and understanding what’s protected prevents costly surprises when you file a claim. Dwelling coverage pays to repair or rebuild your home’s structure at current replacement costs, not the market value you paid-this matters because rebuilding a Seattle home typically costs significantly more than the purchase price. Wind and hail account for the largest share of homeowners claims, so your dwelling coverage must reflect actual rebuilding expenses in today’s market. For a 2,500-square-foot Seattle home, expect dwelling costs around $1,600 annually for basic coverage, though this varies by ZIP code, construction materials, and home age.

Personal Property and Liability Protection

Personal property coverage protects your furnishings, electronics, and belongings inside the home, usually set at 50 to 70% of your dwelling limit. Most policies apply actual cash value to personal property, meaning your $1,200 television receives payment at depreciated value, not replacement cost-you’ll need a scheduled personal property endorsement to cover high-value items like jewelry or art at agreed values. Liability protection shields you when someone is injured on your property or you accidentally damage someone else’s property, with standard limits starting at $100,000 for bodily injury and property damage combined. Medical payments coverage typically covers at least $1,000 in medical expenses for guests injured at your home, regardless of fault. Most Seattle homeowners underestimate liability exposure and should carry at least $300,000 in coverage; a $1 million umbrella policy costs only $150 to $300 annually and provides critical protection if a serious injury occurs on your property.

What Your Policy Excludes

Your standard policy does not cover flood damage from rising groundwater or overflowing bodies of water, and with spring snowmelt and heavy rain common in Washington, you need separate flood insurance-the National Flood Insurance Program takes up to 30 days to activate, so don’t wait until storm season arrives. Earthquake coverage is also excluded and requires a separate endorsement or standalone policy, despite the Pacific Northwest’s significant seismic risk. Water backup from municipal sewers or sump pump failure is typically excluded or heavily capped, yet accounts for substantial damage in older Seattle homes; add a water backup endorsement to protect against this common loss.

Common Claims and Prevention Strategies

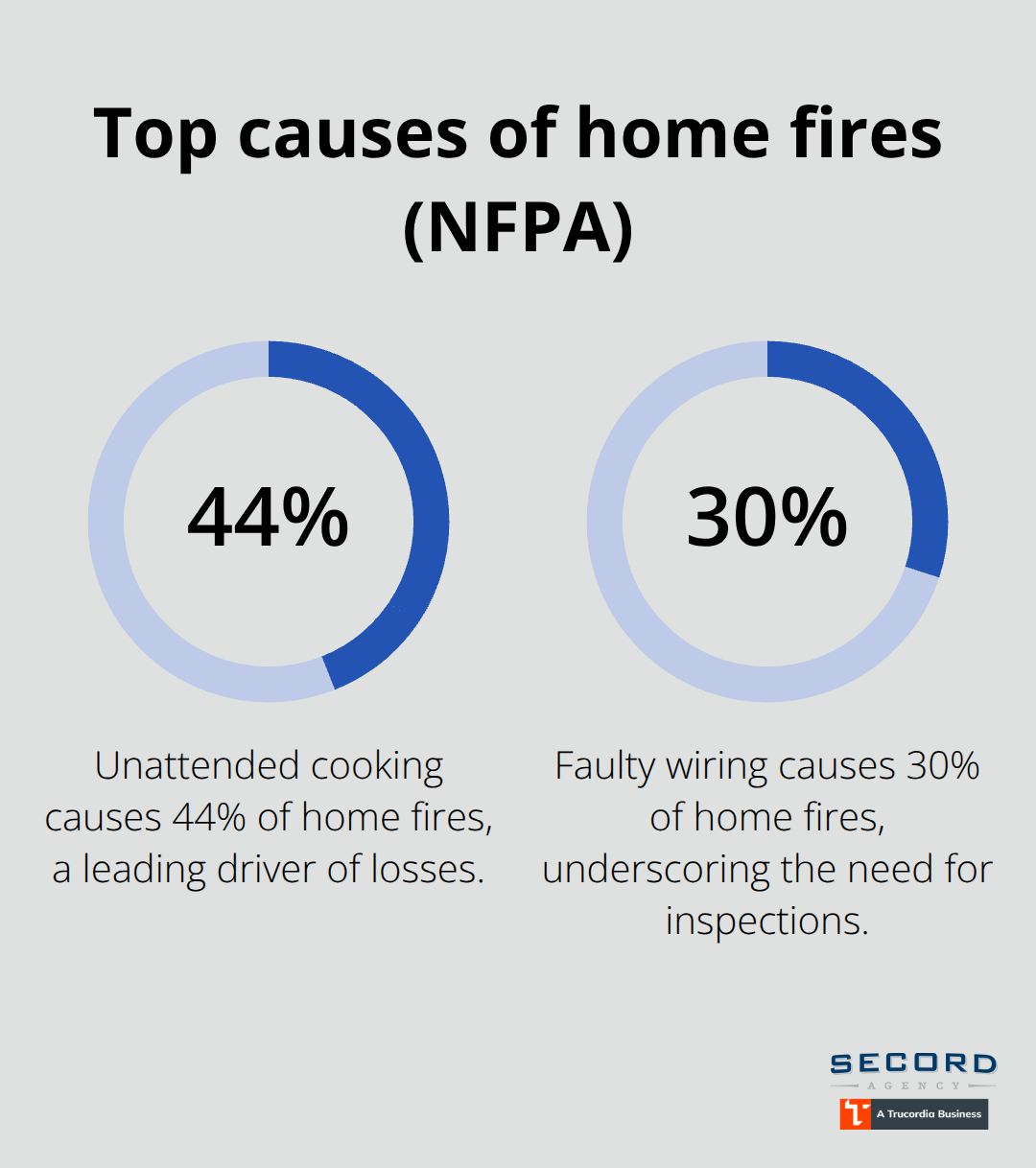

Water damage and freezing are significant concerns in Washington, so insulate exterior pipes, install frost-free hose bibs, and use heat tape in crawlspaces to prevent burst pipes during winter. Fire and electrical hazards cause substantial losses, with the National Fire Protection Association noting that 30% of home fires start from faulty wiring and 44% from unattended cooking-these losses are covered, but prevention through electrical inspections and kitchen safety habits keeps premiums lower.

Dog bite liability is a hidden risk: about 4.5 million incidents occur annually in the US, and many insurers exclude or restrict coverage for certain breeds like Pit Bulls, Rottweilers, and Chow Chows, so verify breed coverage in writing with your carrier.

Moving Forward With Your Coverage

Understanding these coverage boundaries means you can add endorsements strategically and avoid gaps that leave you exposed. The factors that shape your rates-from your home’s age and location to your claims history-play an equally important role in determining what you pay and what protection you actually receive.

What Drives Your Seattle Insurance Rate

Home Age, Size, and Construction Materials Shape Your Premium

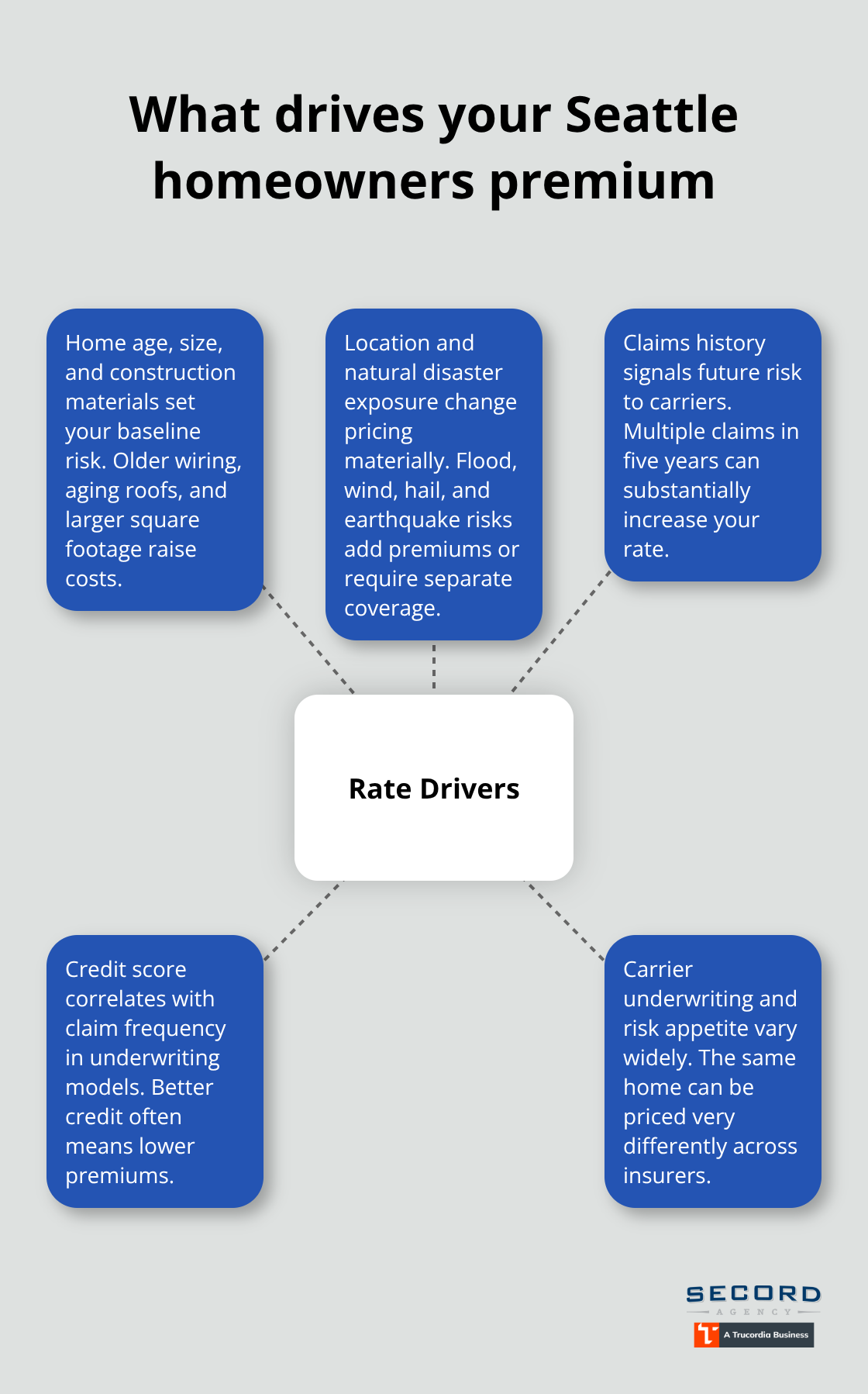

Your home’s age, size, and construction materials form the foundation of how insurers price your policy, and these factors matter far more than most homeowners realize. A 1955 Seattle home like the one quoted at $1,600 annually carries different risk than a newly constructed property because older homes often have outdated electrical wiring, plumbing systems prone to freezing, and roofing materials nearing end-of-life. Insurers charge more for homes built before 1980 because they’re statistically linked to higher fire and water damage claims, particularly when the electrical system hasn’t been updated.

A 2,500-square-foot home costs substantially more to insure than a 1,500-square-foot home simply because there’s more structure to rebuild and more personal property to protect.

Construction materials shift your rate significantly: homes with wood siding and composition roofs pay more than those with brick exteriors and impact-resistant roofing, which can withstand the wind and hail damage that affects Washington homeowners claims according to the Insurance Information Institute. If you’ve upgraded your roof to hail and wind-resistant materials, inform your insurer immediately because many carriers offer discounts of 10 to 15% for this type of protective investment.

Location and Natural Disaster Exposure

Your ZIP code and exposure to natural disaster risk create the second major pricing lever, and this is where Seattle homeowners face real cost variation. Spring snowmelt and heavy rainfall put your property at flood risk, yet standard policies exclude flood damage entirely, forcing you to purchase separate coverage through the National Flood Insurance Program at an additional $400 to $1,200 annually depending on your flood zone. Earthquake risk in the Pacific Northwest adds another $300 to $800 per year for endorsement coverage. Wind and hail storms hit Seattle regularly, making storm-resistant construction a genuine money saver.

Claims History and Credit Score Impact Rates

Your claims history and credit score round out the pricing equation: insurers view past claims as predictors of future losses, so a homeowner with two claims in five years pays substantially more than one with a clean record. Credit scores influence rates because studies show a correlation between credit management and insurance claim frequency. PEMCO, the cheapest homeowners insurer in Washington at around $1,550 annually for $600,000 dwelling coverage, explicitly rewards claim-free history and offers educator discounts. Other carriers like Allstate and State Farm charge significantly more in Washington, with State Farm averaging $2,348 for comparable coverage.

Shopping Multiple Carriers Reveals Your True Cost

Shopping three to five carriers simultaneously is the only way to see how your specific home profile affects pricing across the market, since the same 2,500-square-foot home can cost $1,600 with one carrier and $3,000 with another based purely on underwriting criteria and risk appetite. An independent agency like Secord Agency-a Trucordia business based in Seattle’s Wallingford neighborhood-can shop multiple carriers at once to compare how different insurers rate your property and identify the best value for your coverage needs. The variation across carriers means that comparing quotes from at least three providers before you commit to a policy protects you from overpaying and helps you understand which coverage options matter most for your specific situation.

How to Choose the Right Homeowners Insurance Policy

Calculate Your Home’s True Replacement Cost

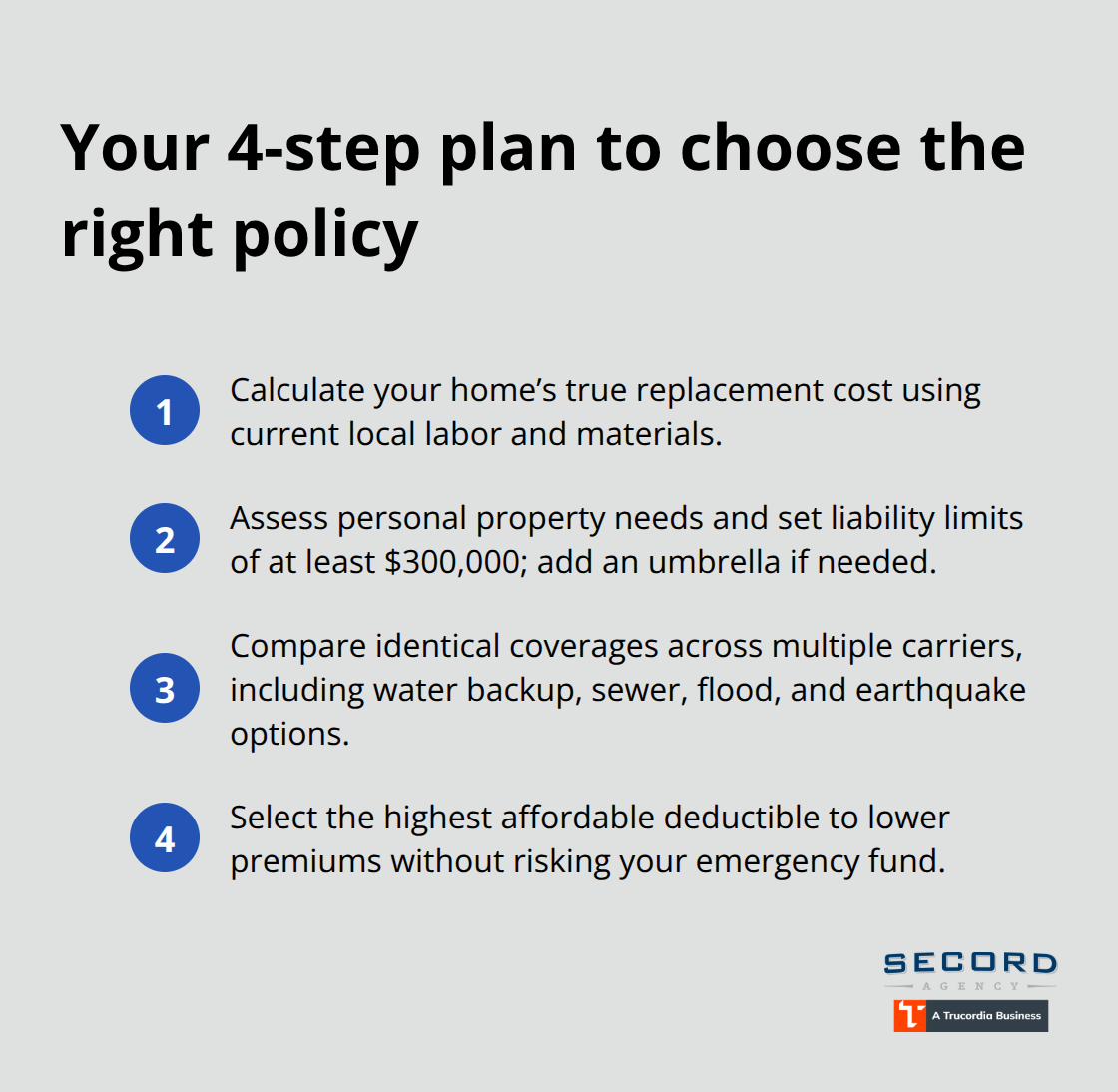

Start by calculating your home’s true replacement cost, not its market value or what you paid for it years ago. Contact three local contractors and ask what it would cost to rebuild your home from the ground up using current materials and labor rates. Most Seattle homeowners discover their dwelling limit is too low because they anchor to outdated purchase prices or tax assessments.

Once you have that number, add 10 to 15 percent as a buffer for cost inflation and unforeseen structural issues that contractors find during reconstruction.

Assess Your Personal Property and Liability Needs

Your personal property limit should reflect what you actually own-count your furniture, electronics, clothing, and appliances, then add scheduled coverage riders for jewelry, art, or collectibles worth more than $2,500 each. Liability limits demand serious attention: standard $100,000 coverage is dangerously low for a Seattle homeowner. A single lawsuit from a guest who slips on your icy driveway or a dog bite incident can easily exceed that amount. Carry at least $300,000 in liability protection, and an umbrella policy costs only $150 to $300 annually-one of the smartest investments you can make. Write down these numbers and use them as your baseline when requesting quotes.

Compare Quotes Across Multiple Carriers

Request quotes from PEMCO, Allstate, USAA (if you qualify as military or federal employee), State Farm, and Farmers using the exact same dwelling limit, deductible, and coverage options across all five carriers. When comparing quotes, pay attention to what’s excluded: some carriers cap water backup coverage at $5,000 while others offer $25,000, and flood or earthquake endorsements vary dramatically in cost and sub-limits. Request quotes that include water backup, sewer backup, and earthquake coverage so you’re comparing apples to apples.

Optimize Your Deductible and Coverage Details

Deductible selection directly impacts your monthly cost-raising your deductible from $500 to $1,000 typically saves 15 to 25 percent on premiums. Try the highest deductible you can afford to pay out of pocket if a loss occurs, since you’re self-insuring that amount anyway. An independent agency can shop all these carriers simultaneously and highlight which offers the best combination of price and coverage for your specific situation, saving you hours of phone calls and ensuring you don’t miss critical endorsements or discounts.

Final Thoughts

Your homeowners insurance overview Seattle protects your most valuable asset when you match your coverage limits to actual rebuilding costs, not outdated purchase prices or market value. Wind and hail cause the majority of Washington claims, so your dwelling limit must reflect current construction expenses in your area, and a $1 million umbrella policy costs only $150 to $300 annually for critical liability protection that standard coverage cannot provide. Water damage from freezing pipes and excluded flood risk demand separate attention through endorsements or standalone policies before spring arrives, since the National Flood Insurance Program takes up to 30 days to activate.

The same 2,500-square-foot home costs $1,600 with one insurer and $3,000 with another, which means comparing quotes across multiple carriers reveals your true cost and prevents overpaying for identical coverage. PEMCO offers the lowest average premiums in Washington at around $1,550 for $600,000 dwelling coverage, but the cheapest option may not fit your specific situation if it excludes water backup or earthquake coverage you need. Raising your deductible to $1,000 saves 15 to 25 percent on premiums, and you should review your policy annually after home improvements or life changes to confirm your dwelling limit still reflects current rebuilding costs.

We at Secord Agency, a Trucordia business based in Seattle’s Wallingford neighborhood, shop multiple carriers simultaneously to find you competitive rates paired with coverage tailored to your actual needs. Our independent agency approach means we compare how different insurers rate your specific property and identify the best combination of price and protection for Seattle’s unique risks. Contact us today to get quotes that account for your home’s true replacement cost.