Landlord insurance Washington state: Protecting Rental Homes And Portfolios

Owning rental properties in Washington comes with real financial exposure. A single liability claim or property damage incident can wipe out years of profit, which is why landlord insurance in Washington state isn’t optional-it’s essential.

We at Secord Agency – A Trucordia Business help property owners navigate coverage options that actually match their portfolios. This guide walks you through what you need to know to protect your investment.

What Landlord Insurance Actually Covers

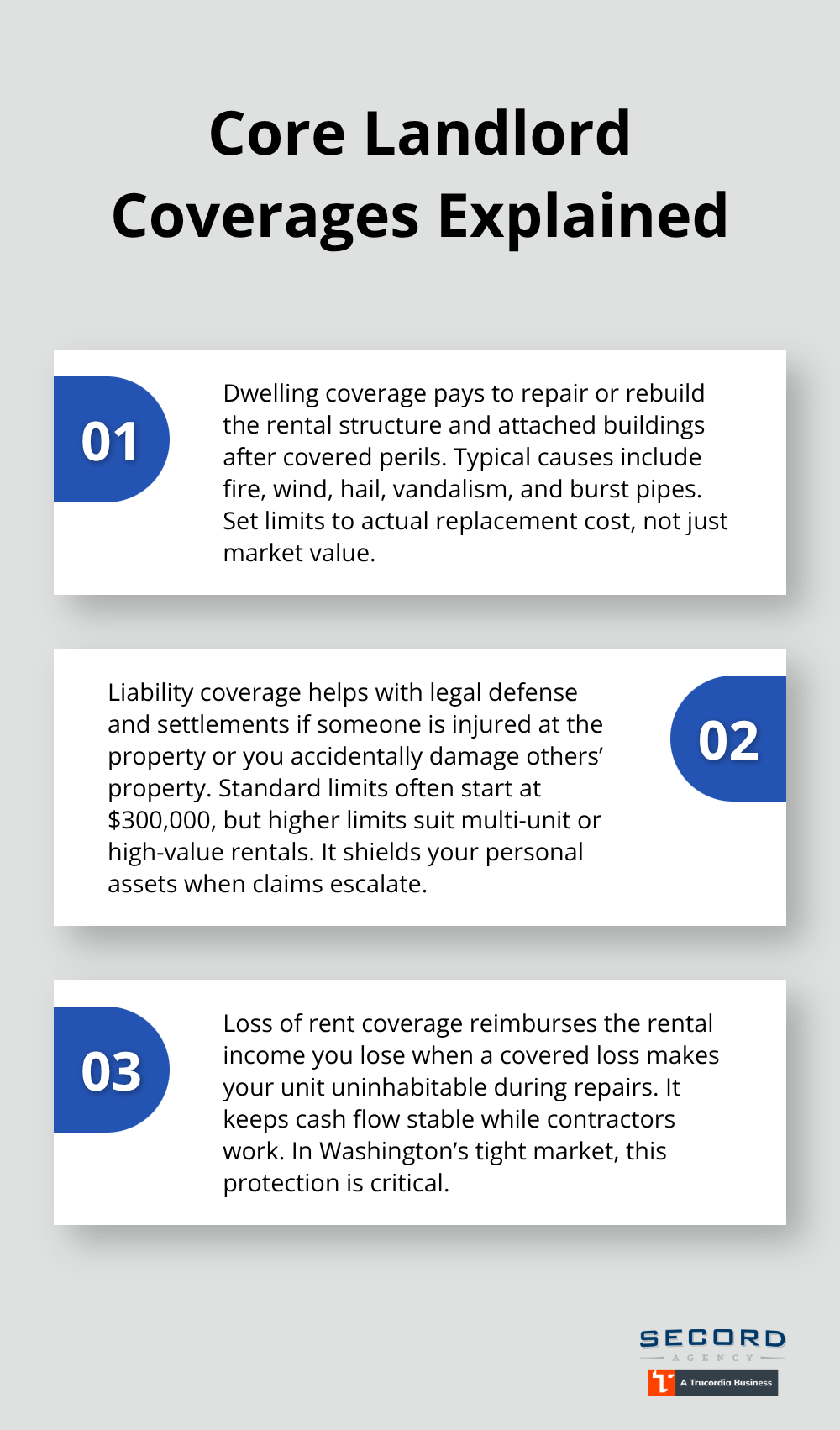

Landlord insurance differs fundamentally from homeowners coverage, and that distinction matters for your bottom line. Standard homeowners policies exclude rental activity entirely, leaving you exposed if a tenant is injured on your property or a fire damages your rental unit. Landlord insurance fills that gap by protecting three critical areas: the physical structure itself, your liability if someone gets hurt at the property, and your rental income when the unit becomes uninhabitable after a covered loss.

Core Coverages That Protect Your Investment

In Washington, the average landlord insurance premium runs about $1,101 annually, though this varies based on property age, location, and whether you’re insuring a single-family home or a multi-unit building. The core coverages you’ll encounter include dwelling protection for the structure and attached buildings, liability coverage typically ranging from $300,000 to $2 million per occurrence, and loss of rent reimbursement that replaces your income during repairs. Fire, wind, hail, water damage from burst pipes, vandalism, and civil unrest are standard perils covered.

Loss of rent coverage is particularly valuable in Washington’s tight rental market, where Spokane County vacancy rates sit below 3.2% and Seattle has over 180,000 rental units-if a covered event makes your unit uninhabitable, this coverage reimburses your lost rental income while you repair the damage.

Why Washington’s Rental Market Demands Real Protection

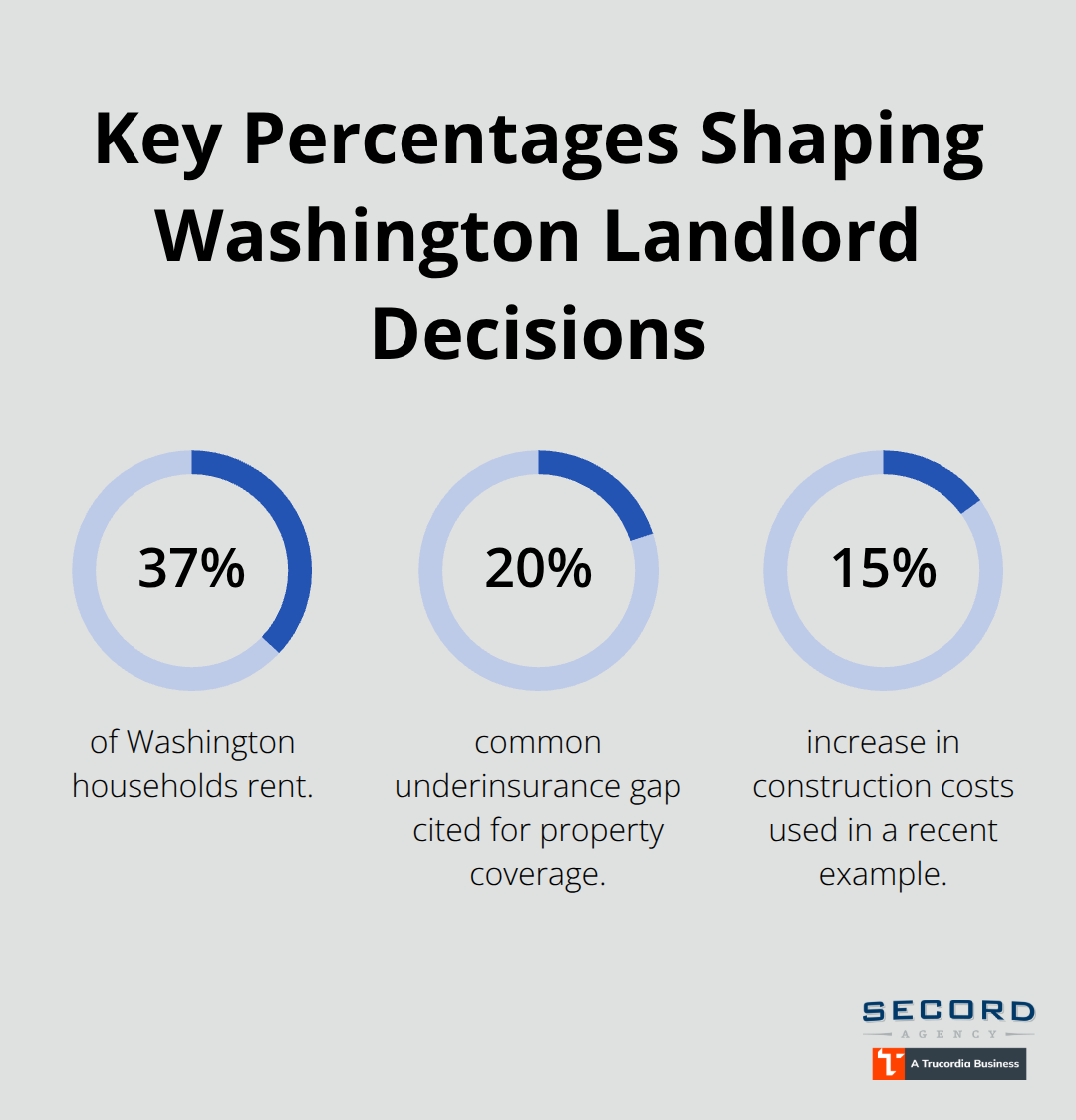

Washington does not legally require landlord insurance, but the state’s rental economics make it practically mandatory. About 37 percent of Washington households rent, with Seattle’s median rent-to-income ratios exceeding national benchmarks by 15 to 20 percent, meaning tenants have less financial cushion and more potential motivation to pursue claims. The Residential Landlord-Tenant Act governs your obligations as a property owner, and Seattle’s just-cause eviction provisions add complexity that increases your liability exposure. A single tenant injury claim or property damage lawsuit can exceed your annual rental income.

Lender Requirements and Regional Risks

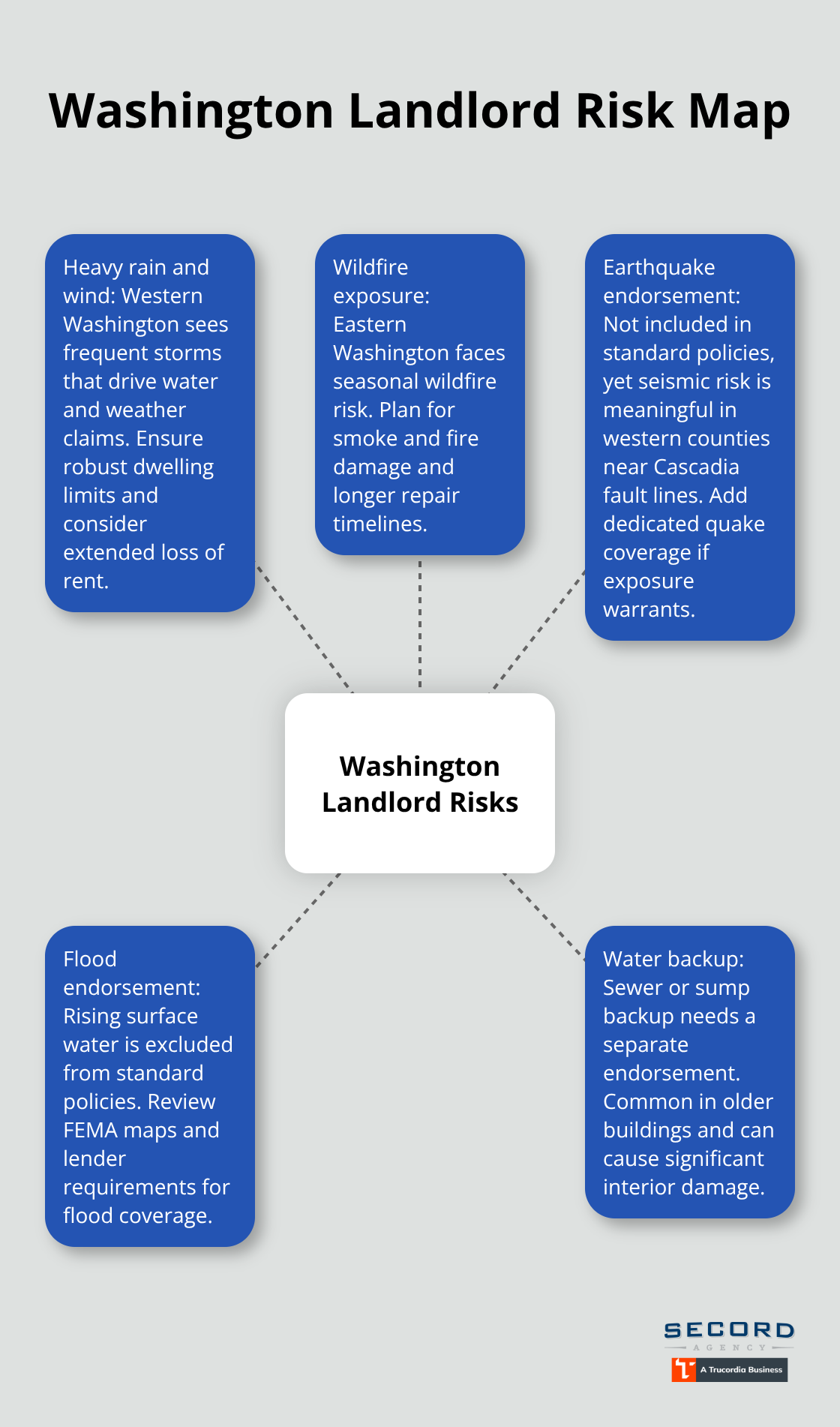

If you financed your property, your lender almost certainly requires landlord insurance as a condition of the loan, making it a practical requirement even where it’s not legally mandated. Western Washington faces heavy rainfall and windstorms that drive water and weather claims, while eastern Washington contends with wildfire risk-both scenarios where loss of rent coverage protects you during extended repairs. Your specific location and property type determine whether standard coverages suffice or whether you need additional endorsements for earthquake, flood, or water backup protection.

Understanding these regional exposures helps you build a policy that matches the real risks your portfolio faces in Washington.

What Coverage Limits Actually Protect Your Rental Portfolio

Liability Coverage That Matches Your Exposure

Liability claims in Washington rental properties run higher than most landlords expect. A tenant slip-and-fall on your stairs, a guest injured at the property, or damage caused by a tenant to a neighbor’s home can trigger lawsuits that exceed $300,000 in damages within months. Standard liability coverage starts at $300,000 per occurrence, but this limit often proves insufficient for multi-unit properties or high-value rentals. Increasing your liability limit to $1 million per occurrence typically adds only $200 to $400 annually to your premium-a small cost relative to the financial exposure you face. If you own multiple rental properties or operate in Seattle’s higher-density neighborhoods where property values and injury claim settlements run steep, push liability coverage to $2 million.

Dwelling Limits That Reflect Real Replacement Costs

Property damage coverage protects the structure itself, but the dwelling limit must reflect current replacement costs, not just the property’s market value. Underinsuring by 20 percent is common and catastrophic-a fire that requires $400,000 in repairs becomes your problem if your dwelling limit sits at $300,000. Washington’s construction costs and labor expenses mean replacement values climb faster than market appreciation, so annual policy reviews catch gaps before a loss exposes them.

Loss of Rent Coverage in Washington’s Tight Market

Loss of rent coverage deserves particular attention in Washington, where tight vacancy rates mean lost income compounds quickly. If your Seattle rental becomes uninhabitable due to a covered loss, loss of rent coverage reimburses what you would have collected from tenants during the repair or rebuild period. This protection separates landlords who recover financially from those who absorb months of lost income while repairs proceed.

Water, Weather, and Specialized Perils

Water damage and weather events dominate claims in Washington, making these coverages non-negotiable. Burst pipes from freezing temperatures, HVAC failures, and plumbing overflows are standard covered perils under water damage provisions, but flood from rising water or sewer backup requires separate endorsements and additional cost. Earthquake coverage is notably absent from standard policies and demands a separate endorsement, particularly critical in western Washington near Cascadia fault lines where seismic risk justifies the extra premium. Vandalism and burglary coverage protects against malicious damage and theft, with most claims requiring police documentation. Civil unrest coverage, sometimes called riot and civil commotion protection, reimburses damage from public disturbances or riots-relevant for properties in urban centers.

Special Situations Demand Explicit Coverage Confirmation

Short-term rentals like Airbnb or VRBO properties require explicit policy confirmation, as standard landlord policies may exclude income from transient occupancy. Vacant or renovation properties need specialized coverage since standard policies exclude uninhabited structures. Your property type and occupancy model determine whether your current policy actually covers what you think it covers, which is why annual reviews with your agent matter more than most landlords realize.

What Mistakes Cost Washington Landlords Real Money

Most Washington landlords discover their coverage gaps only after a loss occurs, and by then the damage is irreversible. The three most expensive mistakes happen repeatedly across the state, and each one stems from a false assumption about how insurance works.

Underinsuring Your Dwelling Destroys Your Financial Recovery

You calculate your property’s market value, set your dwelling limit to that number, and assume you’re protected. This fails because replacement cost far exceeds market value in Washington’s construction market. A single-family home worth $600,000 might cost $750,000 to rebuild after a total loss, accounting for labor inflation, material sourcing, and code upgrades required by current building standards. If your dwelling limit sits at $600,000, you’re short by $150,000 from day one.

The National Association of Insurance Commissioners data shows that underinsurance by 20 percent is disturbingly common, yet most landlords never calculate actual replacement costs. You need a professional replacement cost estimate, not a market appraisal. Annual policy reviews catch this gap before a fire or major weather event exposes it, but most landlords skip reviews entirely and assume their coverage remains adequate as property values and construction costs shift.

Eastern Washington landlords face lower replacement costs than their Seattle counterparts, but the principle remains identical: market value and replacement cost are different numbers. Your policy limit must match the cost to rebuild, not what the property would sell for today.

Confusing Homeowners Insurance with Landlord Coverage Destroys Claims

You own a rental property, apply for homeowners insurance because it’s cheaper, and never mention the rental activity to your agent. When a tenant is injured or causes damage to a neighbor’s property, your claim gets denied because the policy explicitly excludes rental occupancy. Washington’s Residential Landlord-Tenant Act creates specific liability exposures that homeowners policies don’t address, making this mistake financially catastrophic.

Landlord insurance costs roughly $1,101 annually in Washington, while homeowners policies run cheaper for the same property, but that savings evaporates the moment you file a claim on a non-permitted rental use. Independent insurance agents can explain this distinction and quote both policy types side by side, showing the real premium difference and what you actually lose by cutting corners.

Neglecting Regular Policy Reviews Leaves You Exposed

Your rental portfolio changes, market conditions shift, and property values climb, yet your coverage limits stay frozen in place. If you bought a property five years ago with a $400,000 dwelling limit and construction costs have risen 15 percent since then, you’re already underinsured by $60,000. Loss of rent coverage limits matter equally in Washington’s tight rental market.

If your policy covers only 12 months of lost rent and a major fire requires 18 months of repairs, the last six months of income loss becomes your problem.

Review your policy annually, update replacement cost estimates every three years, and adjust liability limits if you’ve added units to your portfolio or moved into higher-density neighborhoods where claim settlements run steeper. This ongoing attention prevents the gaps that turn manageable losses into financial disasters.

Final Thoughts

Landlord insurance in Washington state protects your rental income, your property investment, and your financial stability when unexpected events strike. The three mistakes outlined above-underinsuring your dwelling, confusing homeowners and landlord policies, and skipping annual reviews-cost Washington landlords thousands in unrecovered losses every year. Avoiding these pitfalls requires one straightforward action: obtaining a policy that matches your actual replacement costs, your liability exposure, and your regional risks.

Start by calculating your property’s true replacement cost, not its market value, then contact your lender to confirm their insurance requirements. Request quotes from multiple carriers to compare liability limits, loss of rent coverage, and specialized endorsements like earthquake or flood protection (your policy should reflect current construction costs in Washington and account for the tight rental market’s income protection needs). We at Secord Agency – A Trucordia Business shop multiple carriers to deliver landlord insurance that fits your portfolio and simplifies the process as your rental business grows.

Contact Secord Agency today to review your current coverage or get a quote on landlord insurance that protects your rental portfolio properly.