Landlord Property Policy Washington: Comprehensive Coverage for Landlords

Owning rental property in Washington comes with real financial exposure. A standard homeowners policy won’t protect your rental income or shield you from tenant liability claims.

We at Secord Agency – A Trucordia Business help landlords understand what a landlord property policy in Washington actually covers and why it matters for your bottom line.

What Landlord Property Insurance Actually Covers

How Landlord Insurance Differs from Homeowners Policies

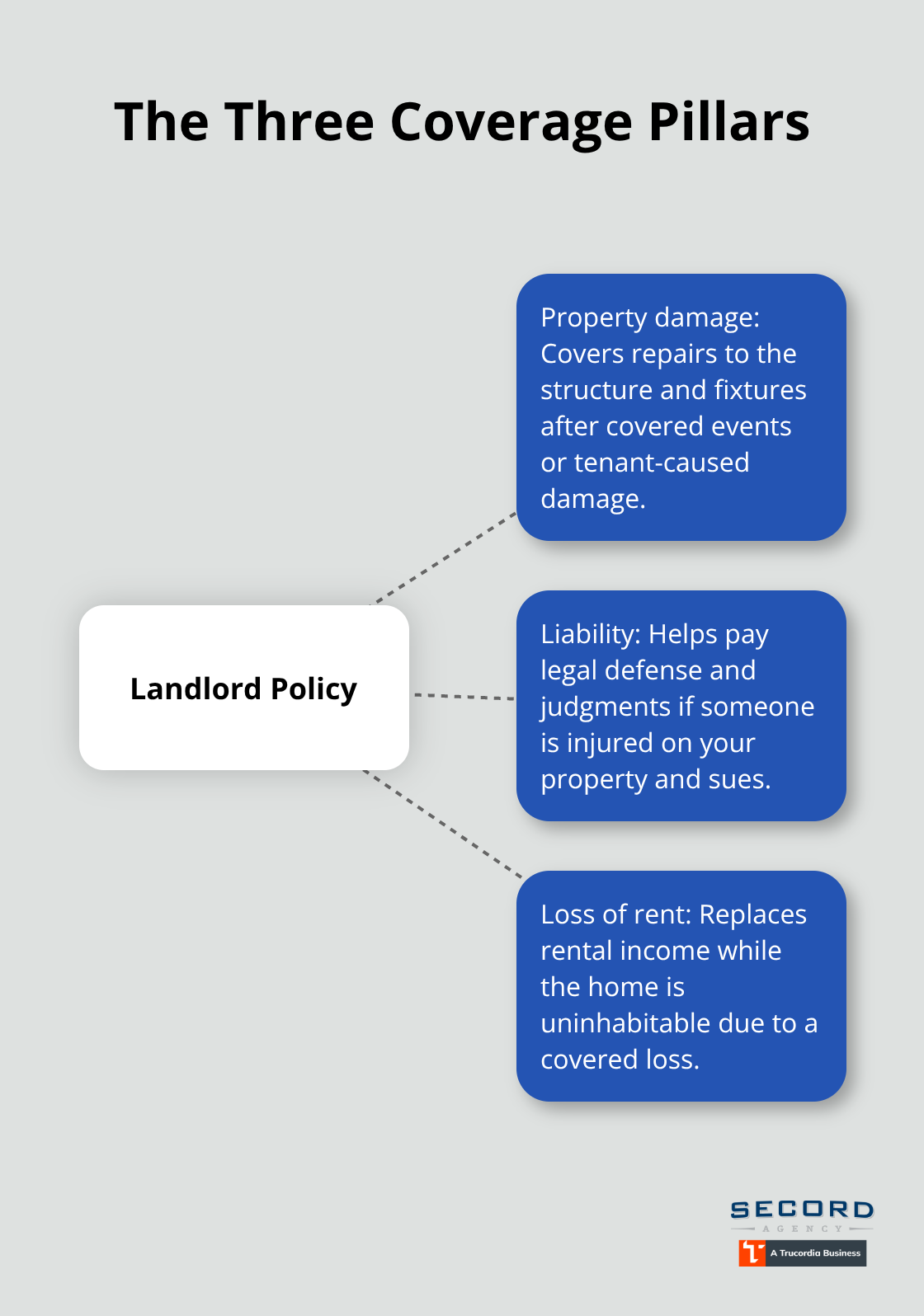

Landlord property insurance in Washington protects something fundamentally different than a standard homeowners policy. A homeowners policy assumes you live in the property and covers your personal possessions. Landlord insurance protects the building itself, your liability exposure as a property owner, and your rental income stream. These three protection areas-property damage, liability, and lost rent-form the backbone of any solid landlord policy.

The Three Main Coverage Pillars

Property damage protection covers repairs to the building and fixtures when a tenant causes damage or a covered event occurs. Liability coverage protects you financially if someone is injured on your property and files a lawsuit. Loss of rental income coverage reimburses you for rent you cannot collect while the property sits uninhabitable due to a covered loss. Together, these three pillars address the specific risks that rental property owners face.

Understanding DP-1, DP-2, and DP-3 Policy Forms

Washington landlords with one to four rental units can choose from three primary policy forms. DP-1 is the most basic option, covering only named perils like fire, lightning, wind, hail, and riots. It excludes vandalism and theft and typically pays out at current cash value rather than replacement cost. DP-2 expands coverage to 18 types of damage including falling objects, burglary, frozen pipes, electrical damage, and vandalism-a practical middle ground for most Washington landlords. DP-3 offers open-perils coverage, meaning nearly all damage is covered unless specifically excluded, and it becomes the right choice if your roof is older than 10 years or you want maximum flexibility.

Why Washington Landlords Cannot Ignore This Coverage

Washington does not legally require landlord insurance, but your mortgage lender almost certainly does. The Rental Housing Association of Washington recommends it regardless of lender requirements. The state’s specific hazards (earthquakes, floods, and wind damage) make dedicated landlord coverage essential because standard homeowners policies often exclude or severely limit these perils. Additionally, Washington’s tenant-protection laws have become stricter, with landlords needing to provide at least 90 days advance written notice before raising rent. When you carry landlord insurance, you transfer certain financial risks to the carrier, which allows you to focus on compliance and property management rather than absorbing unexpected losses.

Scaling Up: Commercial Policies for Larger Portfolios

Properties in high-risk areas or with older construction should prioritize DP-2 or DP-3 coverage. If you own more than four rental units, a commercial landlord policy becomes appropriate, offering broader protections including loss of income coverage, equipment breakdown, and building ordinance insurance to help cover code upgrades after a loss. The right policy form depends on your specific property characteristics, location, and risk tolerance. Understanding which coverage option fits your situation sets the stage for evaluating the specific gaps that standard homeowners policies leave unprotected.

Three Essential Coverage Pillars for Washington Rental Properties

Structure Protection for Your Building and Fixtures

Dwelling fire insurance protects the physical structure of your rental property, but most Washington landlords misunderstand what this coverage actually includes. Structure protection covers damage to the building itself, permanent fixtures like cabinets and appliances, and attached structures such as garages or decks. This coverage applies regardless of who caused the damage-whether a tenant punched a hole in the wall, a storm damaged the roof, or a fire destroyed the kitchen. DP-2 policies, which work well for most Washington landlords, cover 18 named perils including falling objects, frozen pipes, electrical damage, and vandalism. If your roof is older than 10 years, DP-3 open-perils coverage becomes the smarter choice because it covers nearly all damage unless explicitly excluded, protecting you against unexpected scenarios that named-perils policies miss.

Comparing DP-2 and DP-3 Costs and Benefits

The difference in premium between DP-2 and DP-3 typically ranges from 10–20%, but that extra cost pays for itself if you face a single claim involving damage outside the standard 18 perils. DP-2 offers a practical middle ground for landlords who want solid protection without the highest premium. DP-3 makes sense if you own an older property or operate in a high-risk area where unexpected damage types become more likely. Your property’s age, location, and construction materials should drive this decision.

Liability Coverage: Protecting Against Tenant and Guest Injuries

Liability coverage reimburses legal fees and settlements if a tenant or guest is injured on your property and sues you-something that happens more frequently than landlords expect, especially in high-traffic rental areas. Standard homeowners policies exclude liability claims tied to rental activities, leaving you personally exposed to lawsuit costs. A solid landlord liability policy covers your legal defense and any judgment against you, up to your policy limit. This protection matters in Washington where tenant-related disputes have increased significantly in recent years.

Loss of Rent Coverage: Your Income Safety Net

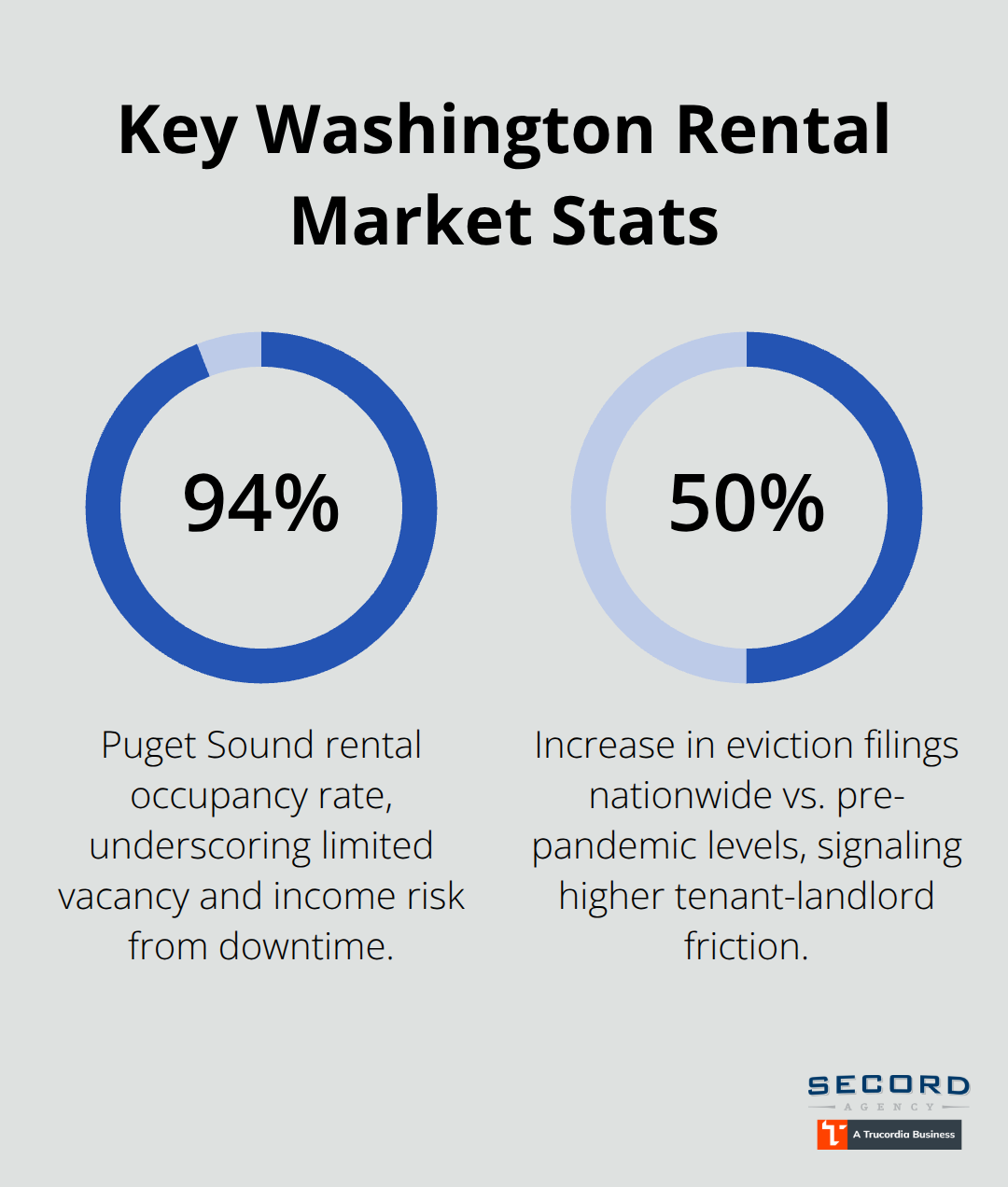

Loss of rent coverage reimburses you for income you cannot collect while the property sits uninhabitable due to a covered loss, and this matters enormously in Washington’s tight rental market where 94% occupancy in the Puget Sound means every vacant day costs you money. If your property becomes unlivable after fire, water damage, or another covered event, loss of rent typically covers your actual rental income until repairs are complete or a maximum of 12 months-whichever is shortest. Without this coverage, you absorb the full income loss yourself while still paying property taxes, mortgage payments, and insurance premiums. For properties generating $2,100 per month in rent-the Washington statewide average-a month-long repair period means $2,100 in uncompensated income loss.

Commercial landlord policies for properties with more than four units include loss of income as standard, making them essential if you own a multi-unit building.

Multi-Unit Properties and Commercial Coverage

Properties with five or more units require a commercial landlord policy rather than a dwelling fire form. Commercial policies offer broader protections including loss of income coverage, equipment breakdown, and building ordinance insurance to help cover code upgrades after a loss. These policies address the complexity of managing multiple tenants and the higher liability exposure that comes with larger rental operations. The right policy form depends on your specific property characteristics, location, and risk tolerance-factors that become more complex as your portfolio grows.

Why Your Homeowners Policy Won’t Protect Your Rental

Standard Homeowners Policies Exclude Rental Activities

A standard homeowners policy is built for owner-occupied properties, not investment real estate. Insurance companies design these policies assuming you live in the home, maintain it personally, and control who enters the building. The moment you rent that property to tenants, your risk profile changes fundamentally, and your homeowners policy becomes inadequate or outright void. Many Washington landlords discover this gap only after filing a claim and watching the insurer deny coverage based on the rental use exclusion buried in the policy language. Your mortgage lender may have accepted the homeowners policy initially, but a rental property requires landlord-specific coverage because the liability exposure and income considerations are entirely different.

Liability Claims Fall Outside Homeowners Coverage

Standard policies exclude liability claims arising from rental activities, meaning if a tenant’s guest slips on a staircase you own, your homeowners carrier will likely deny the claim. Property damage coverage under a homeowners policy also assumes you control maintenance and occupancy patterns, which doesn’t apply when tenants live there. Additionally, homeowners policies contain no loss of rental income protection because the insurer assumes you have no rental income to protect. In Washington’s tight rental market, that income gap becomes catastrophic if a covered loss forces you to vacate tenants temporarily.

Three Financial Risks You Face Without Landlord Coverage

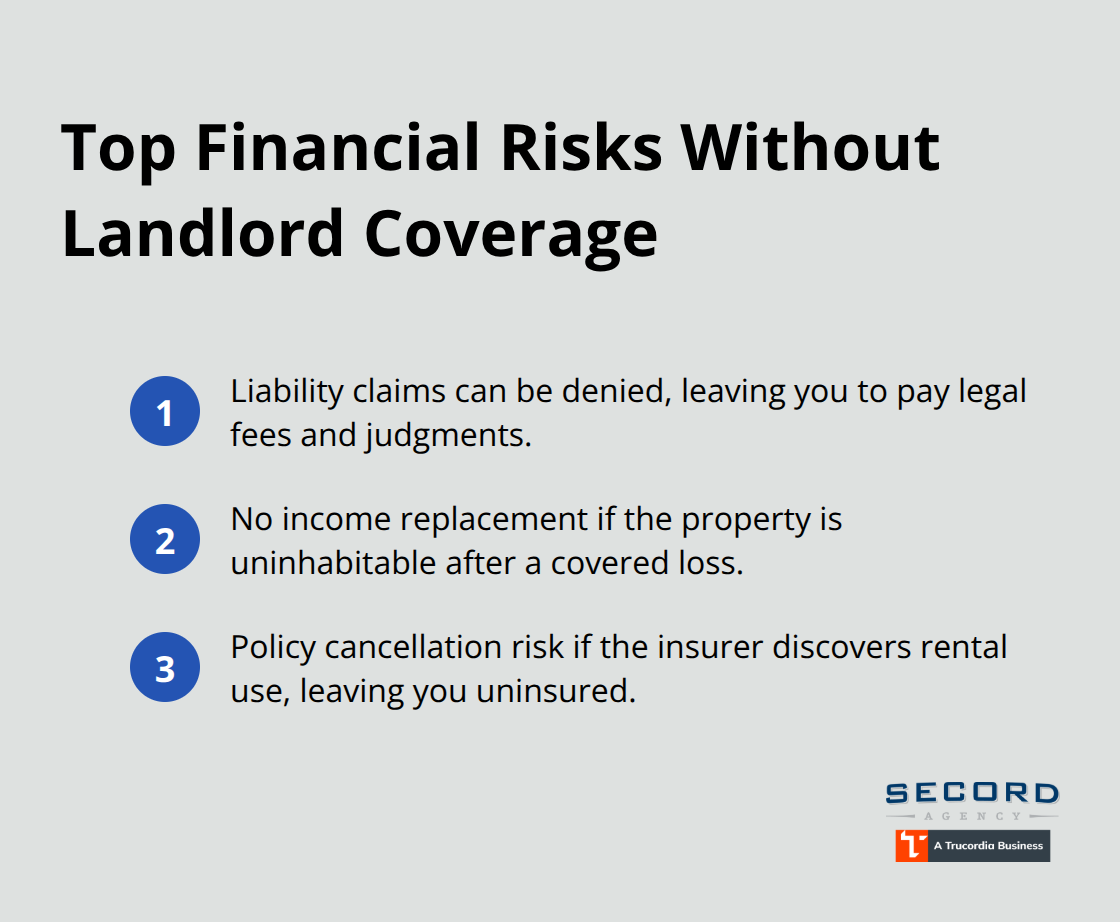

Relying on a homeowners policy for rental property protection exposes you to three serious financial risks. First, your homeowners insurer can deny liability claims from tenants or guests, leaving you personally responsible for legal fees and judgments-a scenario that becomes more likely given that eviction filings across the country have risen roughly 50% higher than pre-pandemic levels according to the Urban Institute’s December 2024 analysis, suggesting increased tenant-landlord friction.

Second, you have zero income replacement if the property becomes uninhabitable, forcing you to absorb lost rent while still paying your mortgage, property taxes, and utilities. Third, your policy may lapse or be canceled retroactively if the insurer discovers the rental use, leaving you uninsured at the worst possible moment.

Transition to Landlord-Specific Coverage Now

Washington landlords facing these gaps should transition to a DP-2 or DP-3 landlord policy immediately, ensuring liability coverage extends to tenant-related claims and that loss of rent protection covers actual rental income during repairs. A landlord property policy flips the standard homeowners assumptions entirely, acknowledging that your building generates income, that tenants create liability exposure you cannot control, and that property damage directly threatens your cash flow. Secord Agency, an independent insurance agency based in Seattle’s Wallingford neighborhood, shops multiple carriers to deliver tailored landlord coverage paired with fast, local service and personalized advice to help you understand exactly which exposures remain unprotected and structure a policy that addresses your specific property and income needs without overpaying for unnecessary coverage.

Final Thoughts

A landlord property policy in Washington protects three critical areas that standard homeowners policies ignore: your building, your liability exposure, and your rental income stream. Without dedicated landlord coverage, you absorb the full financial impact of tenant injuries, property damage, and lost rent during repairs. Washington’s 94% occupancy rate in the Puget Sound means every vacant day costs real money, making loss of rent coverage essential for properties generating the statewide average of $2,100 monthly.

Start by confirming your current coverage with your insurer-most carriers deny claims tied to rental activities, leaving you personally liable for legal fees and settlements. DP-2 works well for most Washington landlords, covering 18 named perils including vandalism and frozen pipes at a reasonable premium. If your roof exceeds 10 years or your property sits in a high-risk area, DP-3 open-perils coverage becomes the smarter choice despite the higher cost.

We at Secord Agency help Washington landlords navigate these decisions by shopping multiple carriers to find coverage that matches your property and income needs. As an independent agency based in Seattle’s Wallingford neighborhood, we pair competitive rates with fast, local service and personalized advice tailored to your specific exposure. Contact Secord Agency to discuss your landlord property policy options and receive a quote that reflects your actual situation.