Condo Homeowners Coverage Washington: Essential Tips for Your Unit

Condo homeowners coverage in Washington protects your unit and personal belongings, but many owners don’t realize what their policy actually covers. The gap between what your HOA master policy covers and what you need to protect yourself can be significant.

We at Secord Agency – A Trucordia Business help condo owners navigate these coverage gaps and build policies that match their actual needs. This guide walks you through the essentials so you can protect your investment properly.

What Your Condo Policy Actually Covers in Washington

How the Two-Policy System Works

Your HO-6 condo policy covers the interior of your unit, but the specifics depend on what the HOA master policy leaves uncovered. In Washington, condo insurance splits responsibility between two policies: the association’s master policy handles the building exterior and common areas, while your personal policy protects what’s inside your walls. Many owners skip reading the master policy before buying coverage, so they either over-insure or under-insure critical areas. Your HO-6 should cover dwelling protection for interior walls and finishes, personal property inside your unit, liability if someone gets injured in your space, medical payments for guest injuries, and additional living expenses if your unit becomes uninhabitable.

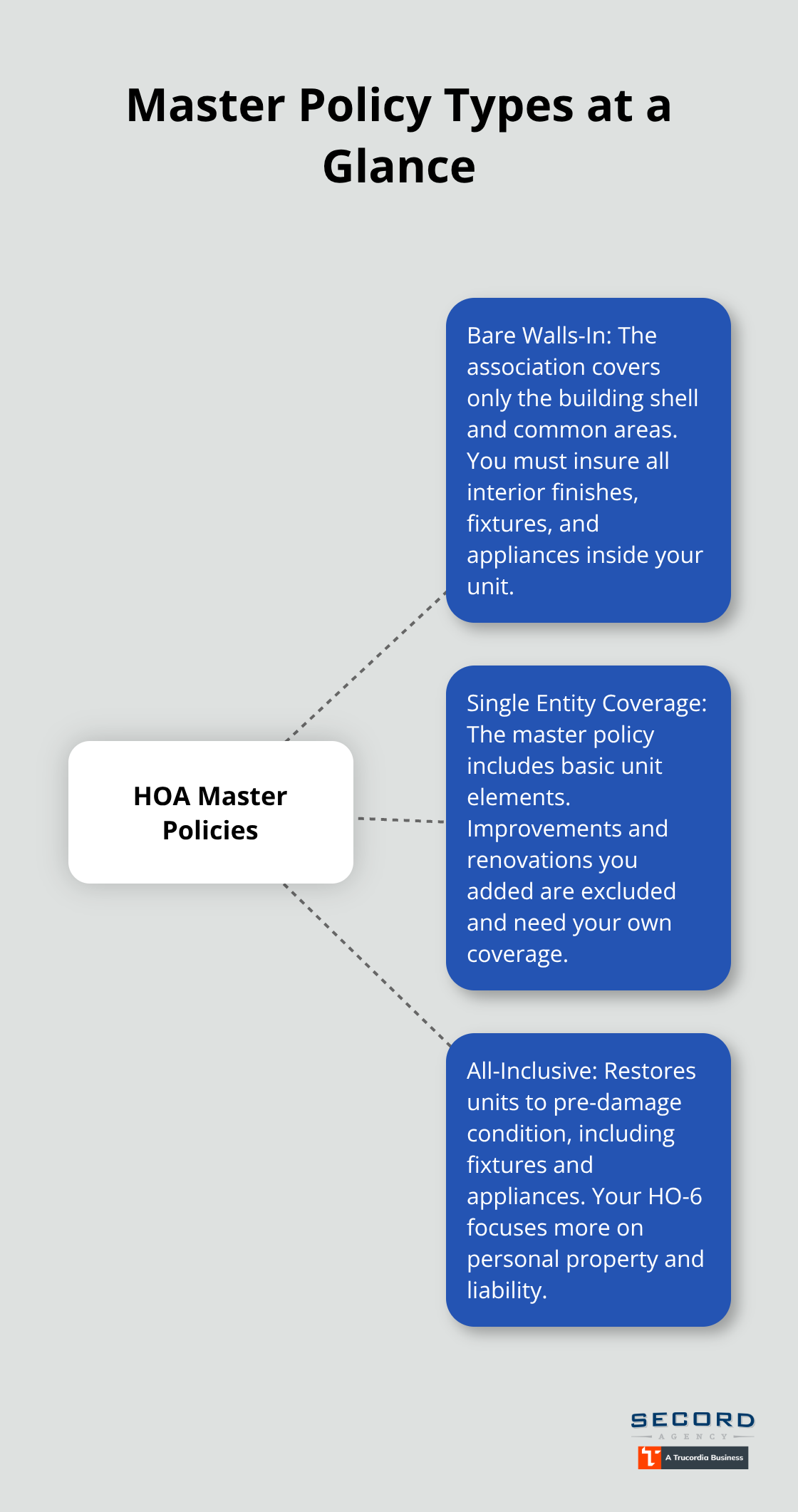

Master Policy Types Shape Your Coverage Needs

The master policy type determines what you actually need to buy. If your building has a Bare Walls-In policy, the association covers only the exterior framing and common areas, leaving you responsible for all interior finishes, appliances, and fixtures. A Single Entity Coverage policy adds unit coverage but excludes improvements and renovations you’ve made. An All-Inclusive policy covers restoration to pre-damage condition, including fixtures and appliances, which means your personal policy focuses more on personal property and liability rather than structural repairs.

Understanding Costs and Deductibles

Washington state condo insurance averaged about $555 per year according to NerdWallet’s 2026 rate analysis, based on a standard two-bedroom policy with typical coverage and a $1,000 deductible, though Seattle runs slightly higher at around $570 annually. Before you compare quotes, obtain and read your HOA’s master policy document and Certificate of Insurance to understand the deductible amount and what’s actually covered. The master deductible can reach $25,000 or higher, which means if a loss occurs, you pay that amount out of pocket before the master policy responds.

Critical Endorsements You Need

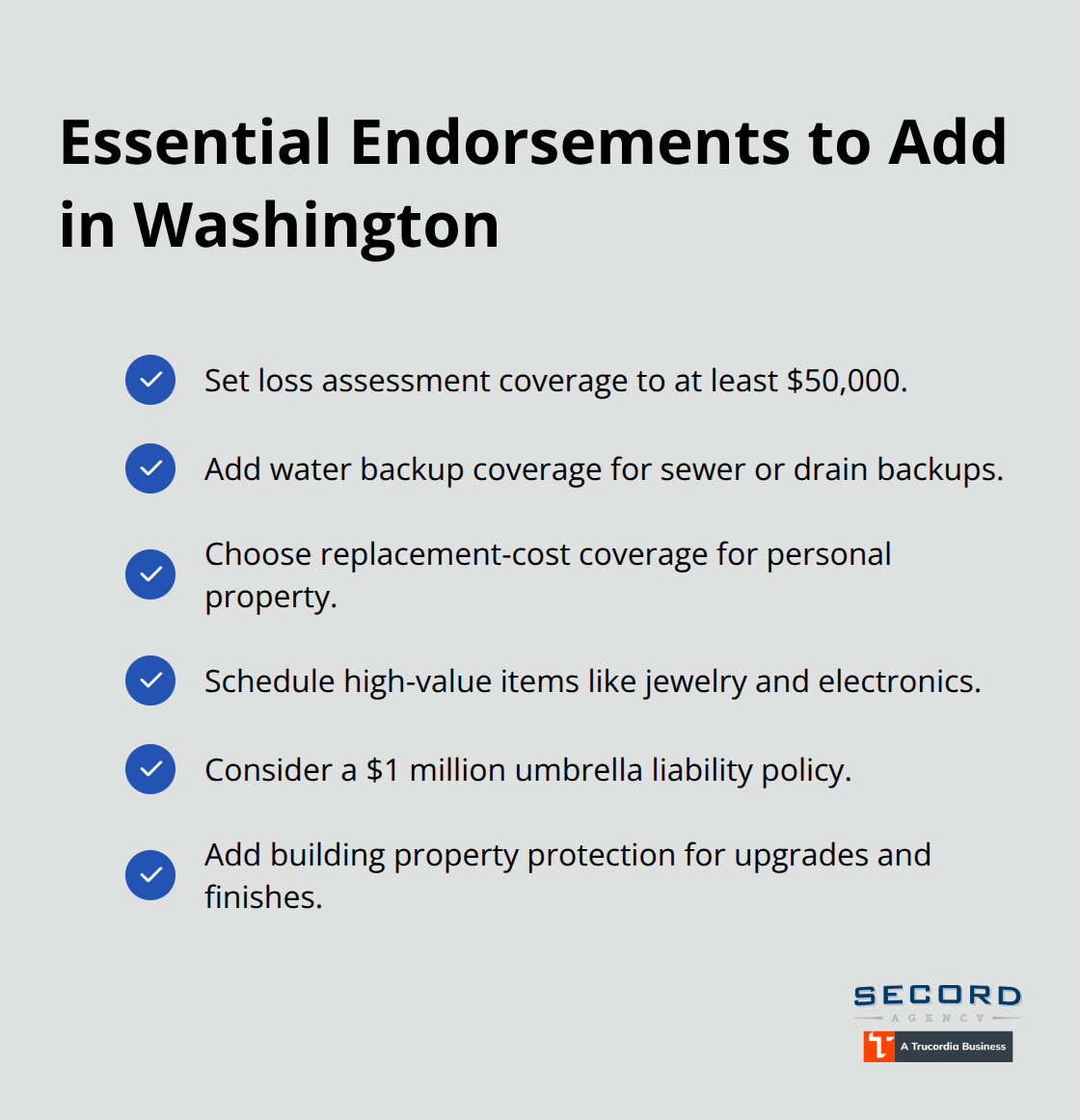

Loss assessment coverage on your HO-6 protects you from costs if your condo association issues an assessment to cover expenses for shared areas damaged. Set loss assessment coverage to at least $50,000 because HOA deductibles and coverage gaps create substantial out-of-pocket costs. Water backup coverage is another critical addition that most standard policies exclude; sewer or drain backups cause real damage in condos and can cost thousands to repair. Personal property coverage in Washington typically pays actual cash value rather than replacement cost, so discuss replacement-cost endorsements with your agent if you own valuable jewelry, heirlooms, or electronics.

Getting Ready to Shop for Quotes

Once you know your master policy type and deductible, shop quotes from at least three carriers with identical coverage limits and deductibles so you can compare apples to apples. This comparison reveals which insurers offer the best rates for your specific situation and helps you identify available discounts. With this foundation in place, you’re ready to evaluate which gaps in your master policy pose the biggest risks to your unit and finances.

What You’re Actually Missing in Your Condo Coverage

Water Damage Exposes Your Finances

Most condo owners in Washington face coverage gaps only after a loss occurs, which is too late. Standard HO-6 policies exclude specific perils that cause real damage in condos, and the master policy often leaves gaps that neither policy covers. Water damage from sewer backups represents one of the largest blind spots because standard policies exclude backup coverage entirely, yet sewer line failures and drain backups happen regularly in older Seattle and Tacoma buildings. If your unit floods from an internal drain backup, you pay out of pocket unless you added water backup coverage as an endorsement. This single exclusion costs thousands in repairs when it strikes, making it one of the most expensive gaps to ignore.

Liability Limits Fall Short in Real Claims

Your HO-6 covers injuries inside your unit, but the coverage limits on standard policies often max out at $300,000, which falls short if a guest suffers a major injury and sues. Medical payment coverage under your policy typically covers only minor injuries up to $1,000 or $5,000, leaving significant liability exposure if someone requires hospitalization or ongoing care. A serious injury claim can exceed these limits quickly, leaving you personally responsible for the difference. Umbrella liability coverage starting at $1 million protects your assets when standard limits prove inadequate.

High-Value Items Receive Depreciated Payouts

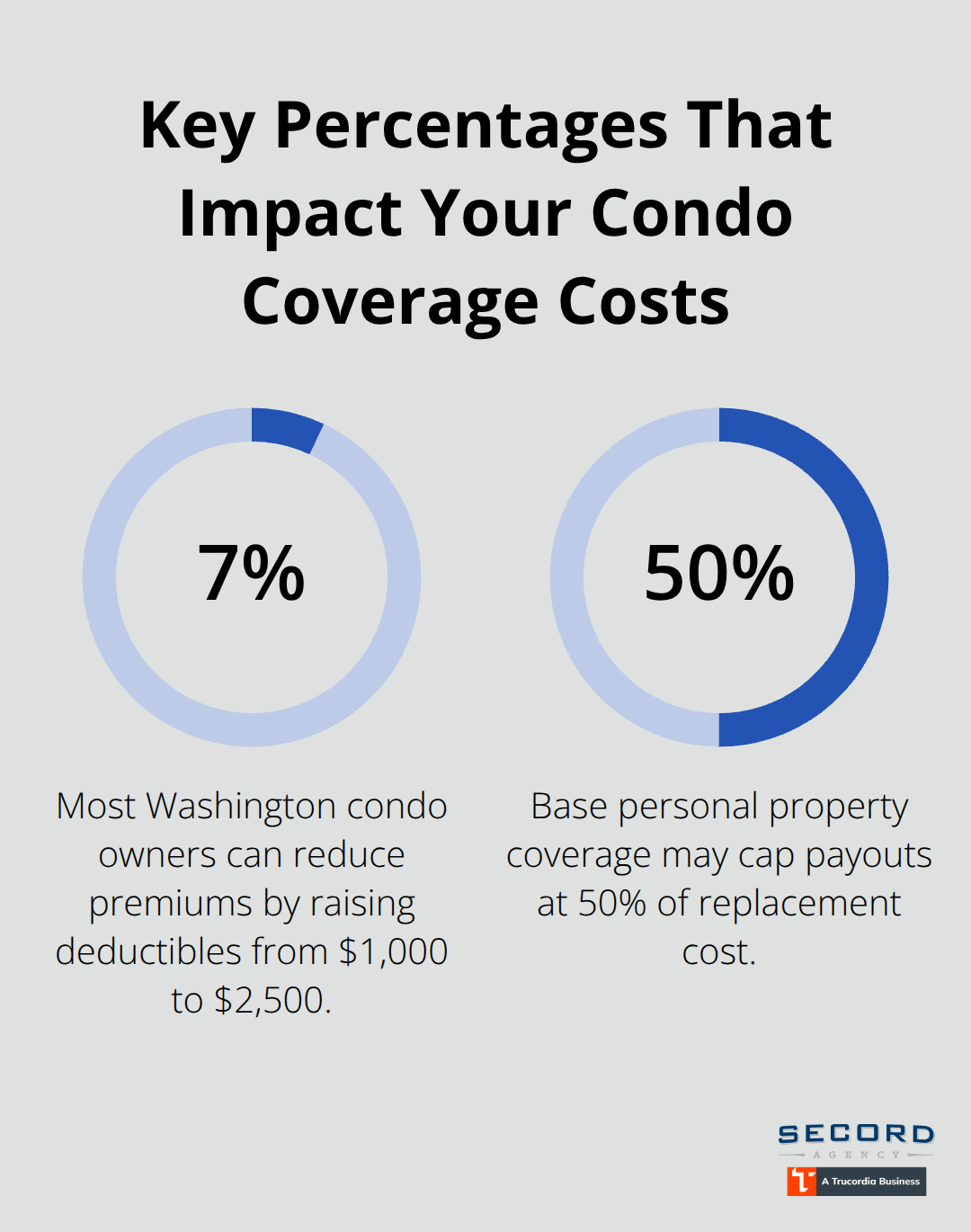

High-value personal items like jewelry, artwork, electronics, or inherited goods are typically covered under standard personal property limits at actual cash value, meaning you receive depreciated payouts rather than replacement cost. If you own jewelry worth $10,000 or electronics worth $8,000, your base personal property coverage may cap payouts at 50% of replacement cost, leaving you substantially underinsured. Scheduled personal property endorsements for items over $5,000 each lock in replacement cost coverage and eliminate depreciation concerns entirely.

Loss Assessment Coverage Protects Against HOA Costs

Loss assessment coverage on your HO-6 protects you from costs if your condo association issues an assessment to cover expenses for shared areas damaged. Set loss assessment coverage to at least $50,000 because HOA deductibles regularly hit $25,000 or higher, and coverage gaps create substantial out-of-pocket costs. The master deductible can reach $25,000 or more, which means a single loss triggers significant assessments passed to unit owners.

Building Your Complete Protection Strategy

Adding water backup coverage if your building was constructed before 1980 or sits in a flood-prone area closes one of your biggest exposure gaps. Consider umbrella liability coverage starting at $1 million if you have meaningful assets or income, because condo injury claims exceed standard policy limits quickly. These additions transform your coverage from incomplete to comprehensive, positioning you to handle the losses that actually occur in Washington condos. With these gaps identified and addressed, you can now evaluate which specific policy features and carriers offer the best combination of protection and value for your situation.

Choosing the Right Policy for Your Situation

Start with your HOA master policy document, not with insurance quotes. Most condo owners reverse this order and waste time comparing policies that don’t match their actual needs. Request the Certificate of Insurance from your property manager and ask for the full master policy if available. The certificate tells you the deductible amount and basic coverage limits, but the full policy reveals exactly what your association covers and what gaps exist. A $25,000 master deductible means you need loss assessment coverage of at least $50,000 to absorb that hit if the association issues an assessment. If your building uses a Bare Walls-In policy, you’re responsible for all interior finishes and appliances, so your dwelling coverage needs to be substantially higher than in an All-Inclusive building where the association covers restoration to pre-damage condition. This single document shapes every other decision you make about your personal policy.

Shop Multiple Carriers with Identical Coverage

Once you understand your master policy, shop quotes from at least three carriers using identical coverage limits and deductibles to see which insurer offers the best rate for your exact situation. Most Washington condo owners can reduce premiums by 7% by increasing the deductible from $1,000 to $2,500, but only if you have the cash reserves to cover that higher deductible when a loss occurs.

Ask every carrier about discounts specific to your situation: bundling condo with auto or other policies, installing smoke alarms or security systems, setting up autopay, maintaining a claims-free history, and living in a gated community can each reduce costs. Credit-based insurance scores also affect your rates substantially, so checking your credit report before shopping helps you understand what you’ll pay. Independent brokers in Washington can access regional carriers offering competitive rates or discounts not visible from national brands, making local expertise genuinely valuable when comparing options.

Match Coverage Limits to Replacement Cost

Coverage limits should reflect your building’s replacement cost, not its sale price. If your two-bedroom unit would cost $400,000 to rebuild in Seattle today, your dwelling coverage should approach that amount, not the $350,000 you paid for the unit five years ago. Construction costs in Washington have risen significantly, and your coverage needs to reflect current replacement value. Personal property coverage works differently: the standard limit of $50,000 on many policies covers actual cash value, so a five-year-old television worth $2,000 new might pay out only $800 after depreciation. If you own jewelry, artwork, or electronics totaling more than $30,000, you need scheduled personal property endorsements that lock in replacement cost and eliminate depreciation penalties.

Protect Against Liability and Water Damage

Liability coverage of $300,000 on a standard HO-6 sounds adequate until a guest suffers a serious injury and your medical bills exceed $500,000, which happens in real claims. Try starting with at least $500,000 in liability coverage, and consider a $1 million umbrella policy if you have meaningful assets or future earning potential. Water backup coverage costs roughly $50 to $150 annually depending on your building’s age and location, yet it prevents thousands in uninsured losses from sewer backups that standard policies explicitly exclude. Building property protection endorsements covering appliances, cabinetry, and flooring upgrades you’ve installed cost far less than replacing those items out of pocket after a fire or water damage. These adjustments transform a generic policy into one that actually protects your specific situation rather than leaving you with expensive gaps when a loss occurs.

Final Thoughts

Protecting your condo investment in Washington requires understanding two separate policies, identifying coverage gaps, and building a strategy that matches your actual risks. The master policy covers common areas and building structure, but your HO-6 fills the gaps for your unit’s interior, personal belongings, and liability exposure. Most owners discover these gaps only after a loss occurs, which is why reviewing your master policy before shopping for quotes saves thousands in unnecessary coverage or dangerous underinsurance.

Your condo homeowners coverage Washington strategy should start with three concrete steps: obtain your HOA’s Certificate of Insurance and master policy to understand the deductible amount and what’s actually covered, identify your building’s master policy type since this determines whether you need higher dwelling coverage or can focus on personal property and liability, and add critical endorsements like loss assessment coverage of at least $50,000 and water backup coverage if your building predates 1980. Shopping multiple carriers with identical coverage limits reveals which insurers offer competitive rates for your situation, and increasing your deductible from $1,000 to $2,500 typically reduces premiums by about 7%. Washington condo insurance averaged $555 annually in 2026, but your actual cost depends on your building’s age, location, master deductible, and the endorsements you add.

Working with a local agent matters because they understand Washington’s specific condo insurance landscape and can access regional carriers offering rates or discounts invisible in online quote tools. We at Secord Agency – A Trucordia Business shop multiple carriers to deliver tailored coverage that matches your actual needs, not generic templates. Contact Secord Agency to review your current coverage and build a strategy that protects your condo investment properly.