Tenant liability insurance WA: Safeguarding Landlords And Their Tenants

Tenant liability insurance in Washington protects both landlords and renters when accidents happen on the property. A single incident-like a guest’s injury or accidental damage-can lead to costly lawsuits that neither party is prepared for.

At Secord Agency – A Trucordia Business, we’ve seen how the right coverage transforms a stressful situation into manageable protection. This guide walks you through what tenant liability insurance WA actually covers and how to choose a policy that works for your situation.

What Tenant Liability Insurance Actually Covers

Liability Protection for Injuries and Property Damage

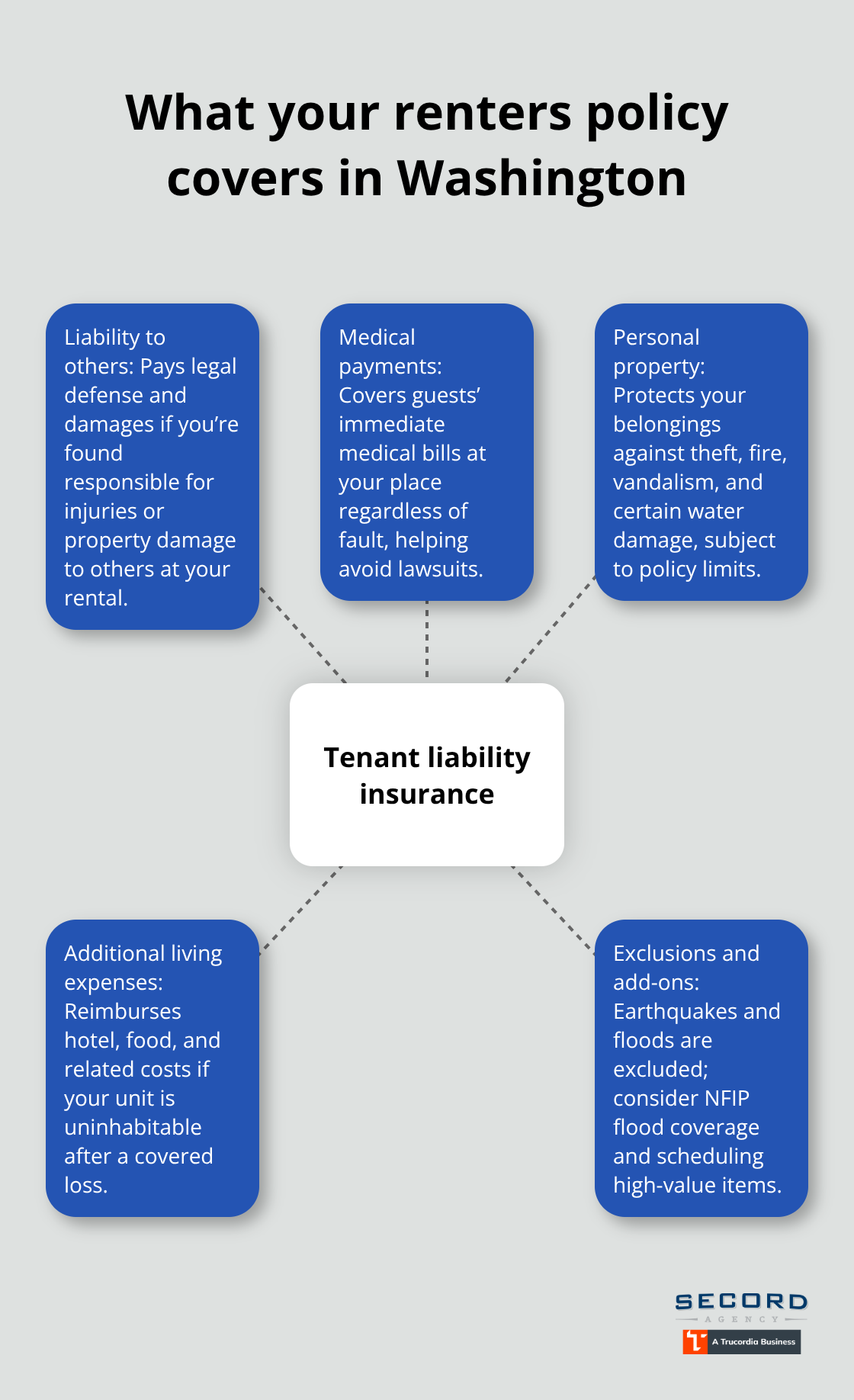

Tenant liability insurance in Washington protects you when someone gets injured at your rental or when you accidentally damage someone else’s property. This coverage differs fundamentally from landlord’s insurance, which covers only the building structure and the landlord’s own liability. Your landlord’s policy will not protect your personal belongings or cover you if a guest trips on your rug and breaks an arm. According to the National Association of Insurance Commissioners, personal liability coverage pays legal defense costs and damages if you’re found responsible for injuries or property damage to others on your rental unit. In Washington, this coverage typically starts at liability limits of $10,000, though many landlords now require $100,000 in liability protection as a lease condition.

You must verify your lease terms in writing, not just verbally, because a mismatch between what you carry and what your lease demands can put you in breach.

Affordability and Lease Requirements

The average cost of renters insurance in Washington runs about $120–$216 annually, or roughly $10–$18 per month according to state data, making adequate liability protection genuinely affordable. Washington state does not legally require renters insurance, but that legal freedom shouldn’t mislead you into skipping coverage. Many property managers and landlords now mandate it in lease agreements, and even when it’s optional, the financial exposure from a single injury claim far exceeds annual premiums.

Medical Payments and Additional Protections

Your policy also covers premises medical payments, which pays medical expenses for guests injured at your place regardless of fault-this coverage remains separate from your liability protection and typically ranges from $1,000 to $5,000. Personal property coverage rounds out the package by protecting your belongings against theft, fire, vandalism, and water damage. Standard policies exclude earthquakes, floods, and landslides, so you’ll need separate flood insurance through the National Flood Insurance Program if you’re in a high-risk area. Additional living expenses coverage reimburses hotel stays and food costs if your rental becomes uninhabitable after a covered loss.

Matching Coverage to Your Actual Needs

The key is matching your coverage limits to the actual value of what you own and understanding exactly what your policy excludes before you need it. High-value items like jewelry, cameras, or musical instruments may require scheduled personal property endorsements to maintain adequate coverage beyond standard policy caps. When you assess your belongings and liability exposure, you’ll be ready to compare policies from multiple carriers and find the right fit for your situation.

Why Tenant Liability Insurance Protects Both Renters and Landlords

How Liability Coverage Stops Financial Disasters

Tenant liability insurance eliminates a dangerous gap that leaves both parties exposed. Without it, a single accident creates financial devastation that neither the renter nor the landlord anticipated. When a guest slips on wet flooring and suffers a serious injury, or when you accidentally damage a neighbor’s property, your personal liability coverage steps in to cover legal fees and damages if you’re found responsible for injuries to others or damage to someone else’s property. In Washington, where average renters insurance costs only $10–$18 monthly, the financial protection far outweighs the minimal premium.

Why Landlords Benefit from Tenant Coverage

Landlords benefit equally because when tenants carry adequate liability coverage, the landlord’s own insurance stays out of disputes over tenant-caused injuries. This separation of coverage means landlords face fewer claims against their policies and maintain cleaner underwriting records. Many property managers now require $100,000 in liability limits specifically because they’ve seen how inadequate coverage creates legal complications and delays in claims resolution.

Medical Payments and Property Protection

Premises medical payments coverage adds another layer of protection by covering immediate medical expenses for guests injured at your rental, regardless of fault. This prevents minor incidents from escalating into lawsuits. For renters with high-value belongings, the personal property protection component guards against theft, fire, and water damage-which Lemonade data identifies as the two most common claim reasons in Washington. Additional living expenses coverage handles hotel stays and food costs if your rental becomes temporarily uninhabitable after a covered loss.

Converting Risk Into Predictable Costs

The practical reality is that tenant liability insurance transforms an unpredictable financial exposure into a predictable, manageable cost. Renters who skip this coverage gamble with their financial future, while landlords who don’t require it create unnecessary legal risk. Understanding what your policy actually covers-and what it excludes-becomes the next critical step in securing the right protection for your situation.

How to Pick Coverage Limits That Match Your Liability Risk

Start With Your Lease Agreement

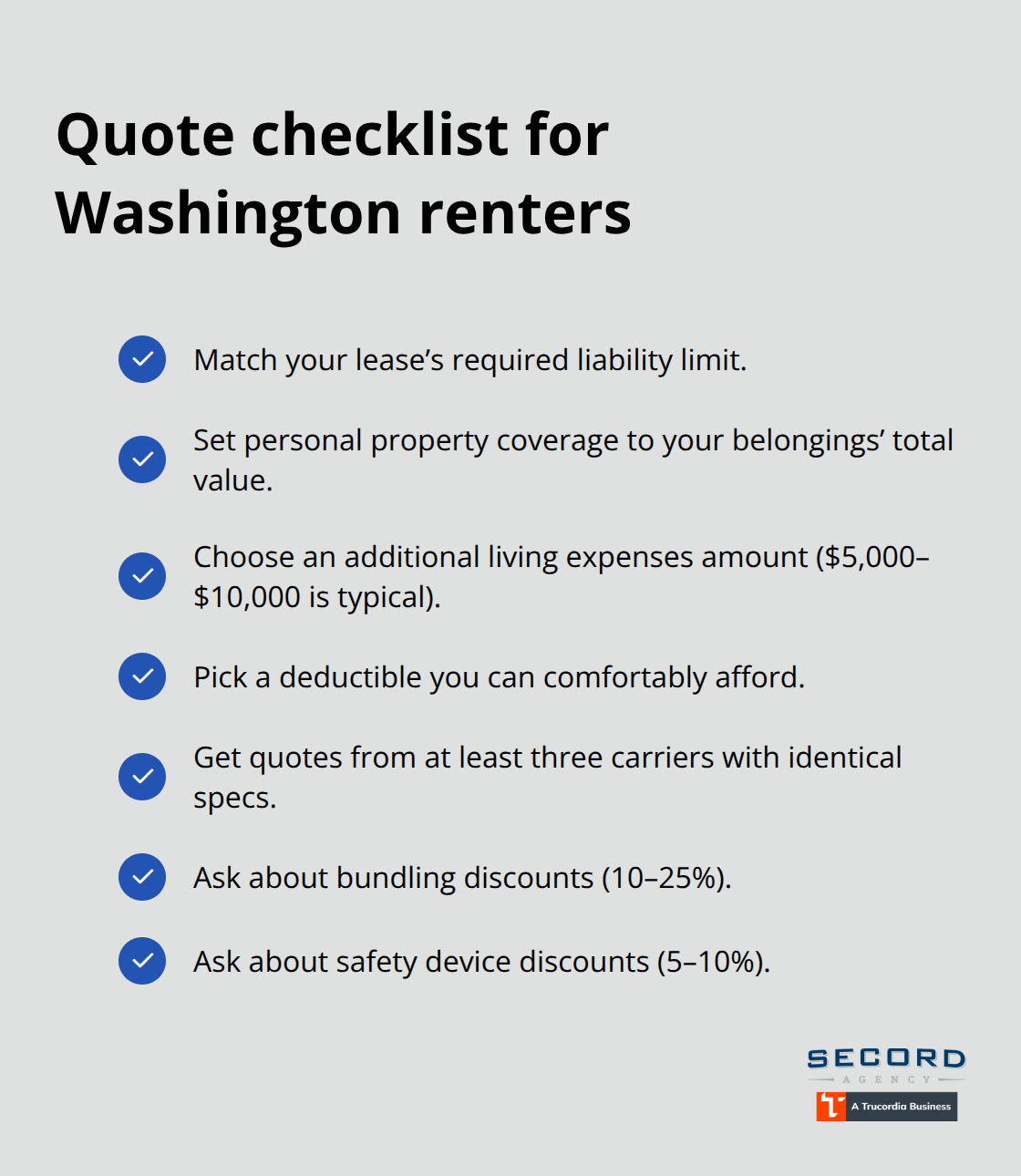

Pull your lease agreement and confirm the exact liability requirement in writing-not a verbal promise from a property manager. Washington landlords increasingly demand $100,000 in liability coverage, yet many tenants still carry only the standard $10,000 limit. If your lease specifies $100,000, that’s your floor, not a suggestion. The cost difference between $10,000 and $100,000 in liability coverage is minimal; most carriers typically charge only a few dollars more monthly for the higher limit. Once you know your lease requirement, assess your actual exposure. If you host frequent gatherings, have a dog, or live in a multi-unit building where guest injuries are more likely, $100,000 makes financial sense regardless of lease terms. If you live alone and rarely entertain, $25,000 to $50,000 may suffice, though erring toward higher limits costs so little that it’s usually worth it.

Choose Your Deductible Strategically

Deductibles work differently than liability limits and deserve separate attention. A $500 deductible saves roughly $3–5 monthly compared to a $250 deductible according to typical Washington pricing. A $1,000 deductible cuts premiums further but means you’ll pay that amount out-of-pocket before coverage kicks in. Most renters choose $500 as the sweet spot-low enough to avoid catastrophic out-of-pocket costs but high enough to justify meaningful savings. Avoid the temptation to raise deductibles just to lower premiums; a water damage claim or theft loss at $1,000 deductible can wipe out years of premium savings.

Compare Quotes With Identical Specifications

Comparing quotes demands specificity because coverage varies dramatically between carriers. When you request quotes, specify the exact coverage you need: liability limit (matching your lease), personal property coverage amount (total value of belongings), additional living expenses (typically $5,000–$10,000), and deductible preference. Lemonade, Liberty Mutual, and State Farm all operate in Washington, but their pricing and add-on options differ. Lemonade emphasizes online discounts and modern claims handling; Liberty Mutual offers traditional agent support; State Farm combines both. Request quotes from at least three carriers using identical coverage specifications so you’re genuinely comparing apples to apples.

Washington allows bundling discounts when you combine renters with auto or other policies, sometimes saving 10–25% on your total premium. Ask each carrier about safety device discounts (fire alarms, burglar alarms) because these typically reduce rates by 5–10%.

Understand Exclusions and Special Coverage Options

Before finalizing any policy, read the exclusions section carefully. Standard policies exclude earthquakes, floods, and landslides-three events that actually happen in Washington. The National Flood Insurance Program covers flood damage and requires a 30-day waiting period, so don’t wait until flood season to purchase coverage. For high-value items like jewelry, engagement rings, or musical instruments, scheduled personal property endorsements extend coverage beyond standard caps, which typically max out at $2,500 for jewelry. Verify whether your chosen policy offers replacement cost coverage (pays to replace with new items) or actual cash value (pays depreciated price), as replacement cost costs more but pays significantly more when you claim.

Work With Local Expertise

Secord Agency, a Trucordia business based in Seattle’s Wallingford neighborhood, helps renters navigate these decisions by shopping multiple carriers and explaining exactly what each option means for your situation. The goal isn’t the cheapest policy-it’s the right coverage at a fair price.

Final Thoughts

Tenant liability insurance in Washington protects you from financial devastation when accidents happen on your rental property. A single incident-a guest’s injury or accidental damage to a neighbor’s belongings-can trigger lawsuits costing tens of thousands of dollars, but your policy handles the legal fees and damages instead. Without coverage, you absorb these costs personally; with it, you transfer that risk to your insurer for just $10–$18 monthly.

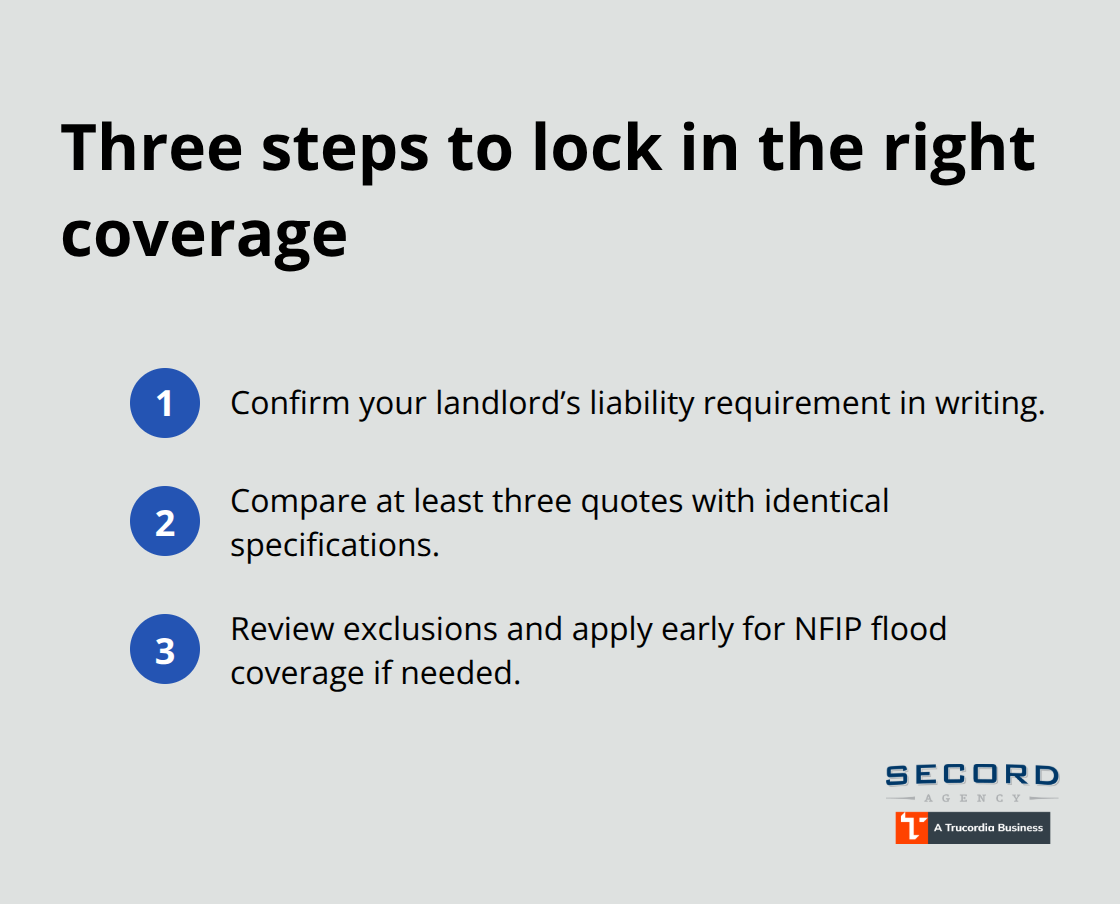

The path to adequate protection requires three concrete actions. First, pull your lease and confirm your landlord’s exact liability requirement in writing, since many now demand $100,000 instead of the standard $10,000 limit.

Second, request quotes from at least three carriers using identical coverage specifications so you compare apples to apples, and ask about bundling discounts (which save 10–25% when combined with auto insurance) and safety device discounts (which typically reduce rates by 5–10%). Third, read the exclusions carefully because standard policies exclude earthquakes, floods, and landslides-events that actually occur in Washington-and apply for flood coverage through the National Flood Insurance Program well before flood season arrives.

We at Secord Agency – A Trucordia Business help renters navigate tenant liability insurance WA by shopping multiple carriers and explaining what each option means for your situation. Contact us today to secure the right coverage for your rental.