Airbnb Rental Insurance Washington: Peace of Mind for Hosts and Guests

Running an Airbnb in Washington means opening your home to strangers. Standard homeowners insurance won’t protect you-in fact, most policies explicitly exclude short-term rental activity.

At Secord Agency – A Trucordia Business, we’ve seen hosts face devastating financial losses because they didn’t understand their coverage gaps. The right Airbnb rental insurance in Washington isn’t optional; it’s the difference between a profitable business and a catastrophic liability.

Why Your Homeowners Policy Won’t Protect Your Airbnb

Standard Policies Exclude Rental Activity

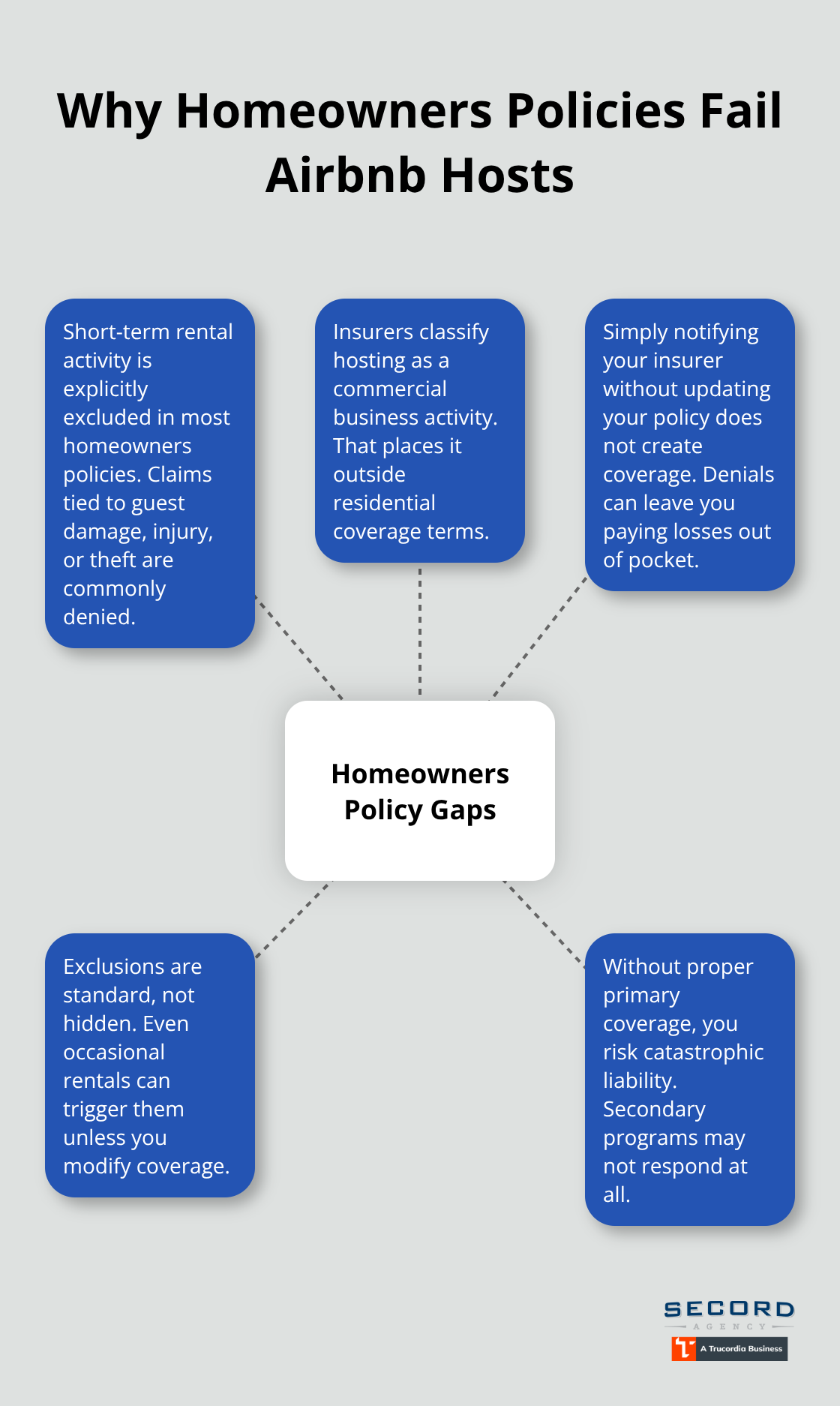

Your standard homeowners insurance policy was designed for one purpose: protecting a primary residence where you and your family live. The moment you list your property on Airbnb, that policy becomes worthless for rental-related claims. Most insurers explicitly exclude short-term rental activity in their policy language. If you file a claim related to guest damage, injury, or theft, your insurer will deny it outright.

Hosts discover this harsh reality only after a guest destroys their kitchen or breaks a leg on the porch. The exclusion isn’t hidden in fine print; it’s a standard clause in nearly every homeowners policy in Washington. Your insurer views short-term rental hosting as a commercial business activity, which falls outside residential coverage. Even occasional rentals-say, just a few weekends per year-trigger exclusions unless you’ve explicitly modified your coverage.

Many hosts assume they can simply notify their insurer of occasional rentals and receive coverage, but this assumption has cost people tens of thousands of dollars in uncompensated damages. Calling your insurer and asking about coverage without formally updating your policy puts you at serious risk. If they deny a claim, you face the financial consequences alone.

Liability Gaps Leave You Exposed

Standard homeowners liability coverage creates a dangerous gap. A guest slips on your wet deck and suffers a broken hip. Your homeowners policy won’t cover their medical bills because the injury occurred during a commercial rental activity. Washington state requires short-term rental hosts to carry at least one million dollars in liability coverage as a minimum standard.

AirCover, Airbnb’s built-in Host Protection Insurance, offers up to one million in liability coverage, but this protection has significant exclusions and acts as secondary coverage. It only pays after your primary insurance exhausts its limits. If you don’t have primary coverage, AirCover may not respond to claims at all.

Property Damage and Lost Income

Property damage presents another critical exposure. A guest throws a party, and your hardwood floors suffer damage, walls are marked, and kitchen appliances break. Standard homeowners insurance won’t cover intentional or reckless guest damage. Specialized short-term rental policies, however, specifically include coverage for guest-caused property damage.

The financial exposure extends to lost rental income during events like wildfires, water damage, or forced evacuations. Washington’s Eastern regions face wildfire season disruptions that eliminate weeks of bookings. Standard homeowners policies don’t cover lost rental income at all. A specialty short-term rental policy covers business income after a waiting period (typically 72 hours), protecting your revenue stream when unexpected events force you offline.

These gaps explain why hosts need dedicated short-term rental insurance-and why understanding your options matters before your first guest arrives.

What Insurance Actually Protects Your Airbnb in Washington

Why AirCover Falls Short

AirCover sounds appealing until you read the fine print. Airbnb’s Host Protection Insurance offers up to one million in liability coverage and three million in property damage protection, but these numbers mask serious gaps. AirCover explicitly excludes wear and tear, mold, infestations, and lost rental income-the exact scenarios that devastate hosts. It also functions as excess coverage, meaning it only pays claims after your primary insurance exhausts its limits. If you have no primary policy, AirCover may not respond at all.

AirCover covers only damage directly caused by guest actions, not weather events, theft outside the listing, or damage to amenities like hot tubs or kayaks stored on your property. Washington state law requires one million in liability coverage as a minimum, and AirCover alone doesn’t reliably meet this requirement because it’s secondary and has exclusions that create coverage gaps. Many hosts discover too late that AirCover won’t pay for the exact loss they’re facing.

Specialty Policies Solve What AirCover Doesn’t

Specialty short-term rental policies address what AirCover leaves unprotected. Proper Insurance, CBIZ Vacation Rental Insurance, and Safely offer policies specifically designed for platforms like Airbnb and VRBO, with premiums in Washington ranging from roughly one thousand eight hundred to four thousand dollars annually depending on property value, location risk, and liability limits.

These policies combine commercial general liability, property damage liability, business income protection, and guest-damage coverage into a single form that replaces or supplements your homeowners policy. Proper Insurance typically costs two thousand to thirty-five hundred dollars yearly for a three-bedroom property and includes amenity liability, bed bug coverage, and squatter protection. CBIZ can run under eighteen hundred for a two-bedroom in Seattle.

How Location and Features Affect Your Premium

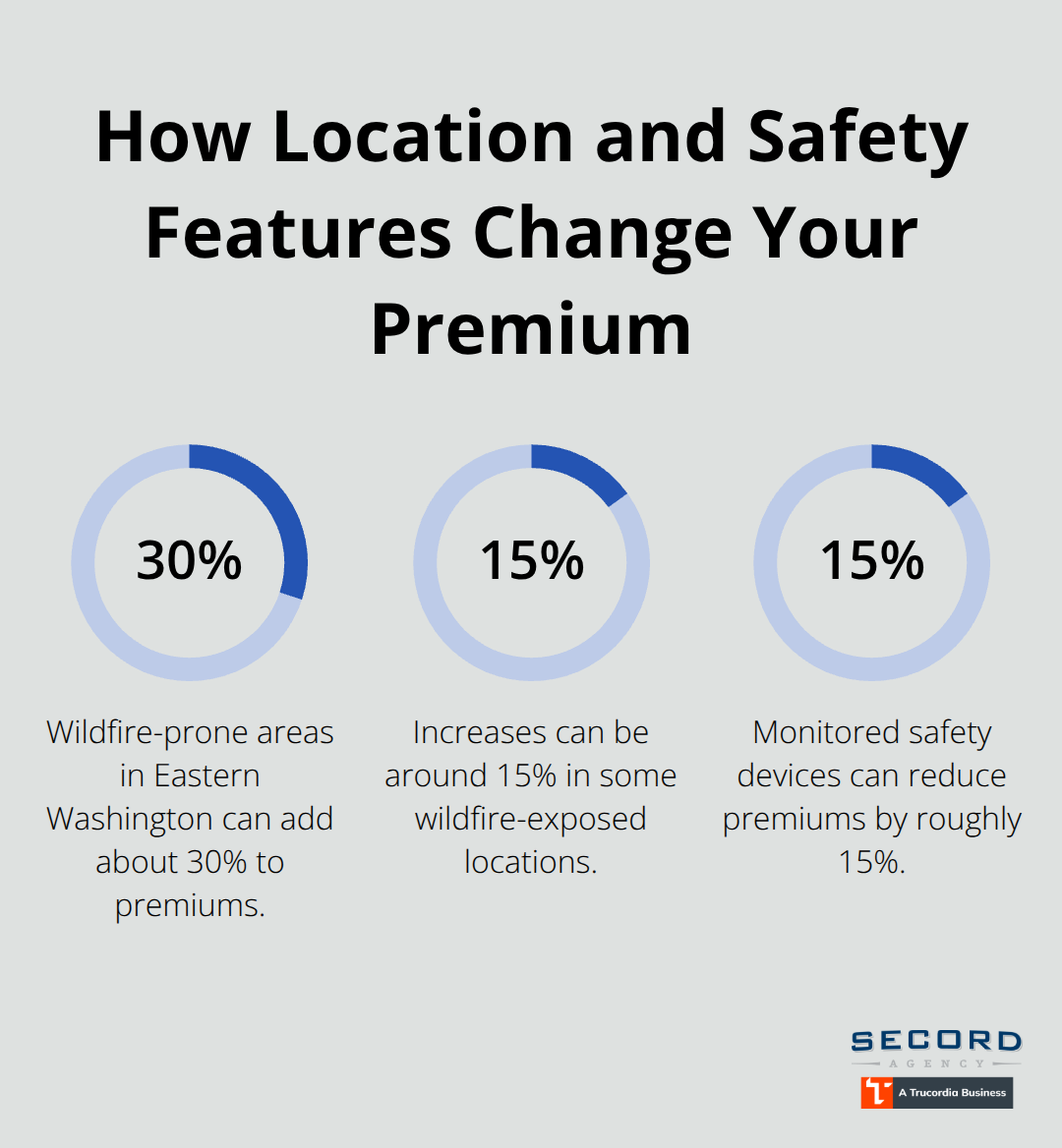

Your property location matters significantly. Wildfire-prone areas in Eastern Washington add fifteen to thirty percent to premiums, while homes near transit or with complex amenities cost more. Safety devices like monitored smoke detectors, water-leak sensors, and security systems reduce premiums by ten to fifteen percent.

Business Income and Primary Coverage Advantages

Specialty policies also cover business income after a seventy-two-hour waiting period, protecting your revenue during forced closures from weather or other covered events. These policies explicitly cover short-term rental activity and respond as primary coverage, eliminating the secondary-coverage trap of AirCover.

Finding the Right Policy for Your Property

An independent agency can shop multiple carriers to compare rates, coverage limits, and exclusions specific to your property, ensuring you pay for protection you actually need rather than overpaying for unnecessary features. This comparison process reveals which carrier offers the best combination of cost and coverage for your situation-information that matters when you’re ready to move forward with actual host responsibilities and legal obligations.

Guest Protection and Host Responsibilities

What Guests Need to Know About Coverage

Guests arriving in Washington short-term rentals often assume Airbnb’s coverage protects them, but this misconception creates serious problems. AirCover for hosts includes guest identity verification, reservation screening, $3M host damage protection, and $1M host liability insurance, but these protections shield hosts from liability claims, not guests. If a guest suffers a slip-and-fall injury or their belongings get stolen, they cannot rely on the host’s Airbnb coverage to recover losses. Guests need their own travel insurance or renters insurance to protect themselves, though most don’t carry it. This gap means hosts field angry guests who expected automatic compensation and didn’t receive it. Setting clear expectations upfront-including a house manual that explains what coverage exists and what doesn’t-prevents conflicts and protects your reputation.

Host Obligations Under Washington Law

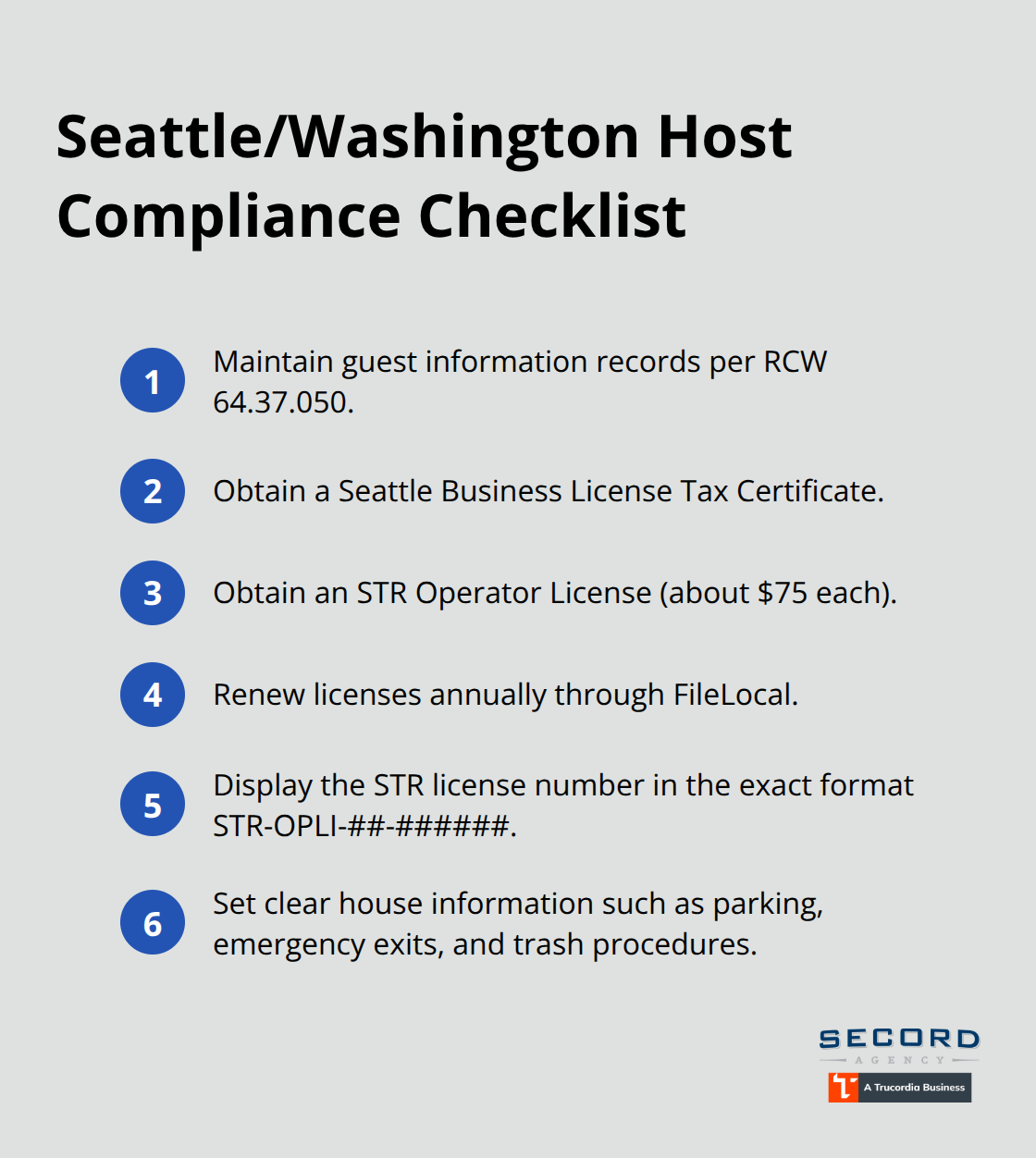

Washington state law requires hosts to maintain guest information records including parking details, emergency exits, and trash procedures under RCW 64.37.050, making documentation part of your legal obligation regardless of insurance. Your host obligations extend far beyond insurance coverage itself. Seattle hosts must obtain two licenses: a Business License Tax Certificate and an STR Operator License, each costing about seventy-five dollars and requiring annual renewal through FileLocal. Every listing must display the official STR license number in the exact format STR-OPLI-##-###### or platforms remove the listing immediately.

Seattle caps most operators at two short-term rental units total, limiting expansion unless you own a primary residence plus one additional property. Chelan County requires one million dollars in liability coverage as a primary policy-umbrella policies don’t satisfy this requirement because they function as excess coverage. Walla Walla imposes a one-hundred-fifty-dollar permit fee and demands proof of property liability coverage plus compliance with fire and safety codes.

Matching Coverage to Your Rental Activity

Selecting the right insurance level means matching your coverage to your actual rental frequency and property characteristics rather than guessing. If you rent occasionally, a homeowners endorsement might suffice, but regular hosting demands a specialty short-term rental policy that explicitly covers your activity. An independent agency can shop multiple carriers to compare which policy meets your specific location requirements, property amenities, and liability exposure-ensuring you pay for protection aligned with real risk rather than overinsuring or underinsuring your operation.

Final Thoughts

Running an Airbnb in Washington requires more than hope and a standard homeowners policy. Standard coverage fails when guests arrive, regulatory requirements demand specific protections, and financial exposure grows with every booking. Airbnb rental insurance in Washington isn’t optional-it’s the foundation of responsible hosting that protects both your investment and your guests.

Contact an independent insurance agency that shops multiple carriers rather than pushing a single option. An agency can compare rates, coverage limits, and exclusions across Proper Insurance, CBIZ, Safely, and other carriers to find what actually fits your property, location, and rental frequency. We at Secord Agency – A Trucordia Business specialize in helping Washington hosts find the right protection through competitive shopping and personalized advice that reveals which policy covers your specific amenities, protects your business income during forced closures, and meets local licensing requirements.

Your property changes over time-you add a hot tub, upgrade amenities, or expand to a second unit. Regulations shift and your rental income grows, each affecting your coverage needs. A quick annual conversation with your agent keeps your policy aligned with your business rather than leaving you exposed to new risks you didn’t anticipate.