Earthquake Protection Homeowners: Strengthen Your Home Insurance in Seismic Zones

Homeowners in seismic zones face a harsh reality: standard insurance policies leave earthquake damage uncovered. At Secord Agency – A Trucordia Business, we’ve seen families discover this gap only after disaster strikes.

Earthquake protection for homeowners requires both physical reinforcement and proper insurance coverage. This guide walks you through identifying your risk, strengthening your property, and selecting insurance that actually protects what matters most.

Know Your Earthquake Risk Before Disaster Strikes

Earthquake risk is not abstract or distant-your exact location and the geological features beneath your property determine it. The Washington Geological Survey maps seismic hazard zones across the state, identifying areas near active faults like the Puget Sound fault zone where homes face significantly higher risk. If you live within a few miles of a mapped fault line, your earthquake insurance premiums will reflect that proximity, sometimes costing substantially more than properties in lower-risk counties. A homeowner in Seattle with a $300,000 home might pay $900–$2,250 annually for earthquake coverage, while the same property in a lower-risk Washington county could run $600–$1,500 per year.

Soil type matters equally-homes built on sandy or loose soil experience greater shaking intensity than those on bedrock, which insurers price accordingly. You can check your specific seismic zone and soil conditions through the Washington Geological Survey maps or ask your insurance agent to run a property risk assessment. This step takes minutes but reveals whether your location demands earthquake protection as a non-negotiable expense rather than an optional add-on.

Standard Insurance Leaves You Exposed

Your homeowners policy covers fire, theft, and weather damage-but earthquake damage sits in a coverage void. Insurers exclude earthquakes because the potential loss from a single major event exceeds their financial capacity, making it impossible to spread risk predictably. California law requires fire damage from earthquakes to be covered under homeowners policies, yet structural damage from the quake itself remains your responsibility. This distinction matters enormously: if an earthquake ruptures your foundation or collapses a wall, you absorb the full cost unless you purchased separate earthquake insurance.

The 2001 Nisqually earthquake near Seattle demonstrated this vulnerability, causing significant damage across the region. Many homeowners discovered afterward that their standard policies paid nothing for their earthquake losses, leaving them to fund repairs through savings, loans, or disaster assistance programs that rarely cover full reconstruction costs. Federal disaster relief typically comes as low-interest loans rather than grants, meaning you rebuild using borrowed money. Separate earthquake insurance closes this gap by covering dwelling damage, personal property, and living expenses if your home becomes uninhabitable.

What New Zealand’s Earthquakes Taught Homeowners

New Zealand’s 2011 Christchurch and 2016 Kaikoura earthquakes revealed how inadequate coverage leaves homeowners facing years of financial uncertainty. Thousands of Christchurch residents had earthquake insurance but discovered their policies contained exclusions for land damage, liquefaction, and other ground-related failures. Others found their coverage limits insufficient for actual reconstruction costs, forcing them to negotiate with insurers over what constituted damage versus normal wear.

The experience taught homeowners that reading policy details before disaster strikes is non-negotiable-waiting until after an earthquake to learn about deductibles, exclusions, and coverage limits is too late. Deductibles on earthquake policies typically range from 10–25% of your coverage amount, meaning a homeowner with a $300,000 dwelling limit and a 15% deductible faces a $45,000 out-of-pocket expense before insurance pays anything. High deductibles lower premiums but shift significant financial risk to you.

The Deductible Trade-Off That Matters

Homeowners who selected lower deductibles despite higher premiums recovered faster and with less personal financial strain after the Christchurch quake. The financial impact of your deductible choice becomes clear only when you calculate the break-even point-the damage amount at which your insurance payout begins. A homeowner paying $200 per month ($2,400 annually) with a 5% deductible on a $300,000 home must incur more than $41,000 in damage to receive any payout. This scenario illustrates why understanding your specific policy terms matters before you sign the contract.

Your next step involves selecting the right coverage limits and deductible structure for your financial situation and risk tolerance. The choices you make now determine how quickly you recover if an earthquake strikes your home.

How to Retrofit Your Foundation and Secure Your Home

Foundation bolting and cripple wall bracing form the backbone of earthquake protection. The difference between a home that survives intact and one that slides off its foundation comes down to these two upgrades. Earthquake Safety, Inc. identifies the primary purpose of retrofitting: keeping your home from being displaced from its concrete foundation, making the building safer and less prone to major structural damage during an earthquake. When an earthquake strikes, your house wants to move independently from the ground beneath it-foundation bolts and bracing prevent that separation.

Expansion bolts cost less upfront but work only in solid concrete, while epoxy-set bolts perform better in older or weaker concrete and can be embedded deeper for superior uplift resistance. If your home was built before 1980, epoxy-set bolts are the smarter choice because aging concrete deteriorates and loses grip strength. Plate washers under anchor hardware must be hot-dipped galvanized 3 by 3 by ¼ inch square washers to clamp the mudsill securely to the foundation and prevent pull-through during earthquakes. When vertical clearance is insufficient for traditional bolts, foundation plates such as Simpson Strong-Tie UFP10 can be used at intervals similar to bolts, providing an effective alternative without requiring deep drilling.

Why Cripple Wall Bracing Stops Collapse

Cripple wall collapse represents a major source of earthquake-related failure, yet this vulnerability remains invisible to most homeowners because it sits in the crawl space beneath living areas. Cripple walls are the short walls that sit between the foundation and the first floor in homes built on raised foundations or piers, and they lack the lateral bracing needed to resist sideways earthquake motion. Structural plywood applied to these walls creates shear walls that resist lateral seismic forces, but you must apply bracing on all sides of the house for comprehensive protection rather than just one wall.

Load transfer is critical-you need a continuous chain from foundations through sill, walls, and into the overhead floor framing so earthquake motions transmit properly without creating weak points. Homes without cripple walls can still be anchored using Simpson UFP10 mudsill plates with L70/L90 clips or direct floor joist anchors; angle iron struts provide another customizable option that offers strong vertical lift and lateral resistance, though they require custom fabrication rather than off-the-shelf components. Retrofit costs typically run about $3,000–$7,000 for older homes needing comprehensive work, and this upfront investment can reduce earthquake insurance premiums by up to 25 percent according to the California Department of Insurance.

Securing Water Heaters and Heavy Furniture

Water heaters become projectiles during earthquakes, rupturing gas lines and causing fires that spread faster than structural damage alone. Strapping your water heater to wall studs with metal bands takes one hour and costs under $50, yet prevents a failure that could ignite your home. Tall furniture, televisions, and computers must be bolted to studs using L-brackets rated for the item’s weight-do not rely on friction or friction pads, which fail under seismic acceleration.

Secure breakables with museum putty, add latches to cabinet doors so dishes do not scatter across your kitchen, and strap down heavy electronics. These actions cost minimal money but prevent injuries and reduce the secondary damage that complicates recovery after a quake. After retrofitting, have your work inspected by a professional to verify that bolts, bracing, and connections meet ABAG Standard Plan A guidelines, which specify acceptable bolt types and installation practices to avoid cracking concrete.

What Comes Next in Your Protection Plan

Your home’s physical strength now stands fortified against seismic forces, but retrofitting alone cannot replace your home after an earthquake. Insurance coverage works alongside these structural improvements to cover the costs that retrofitting cannot prevent-and selecting the right policy requires understanding how deductibles, coverage limits, and additional riders protect your financial recovery.

Choosing Coverage That Matches Your Actual Risk

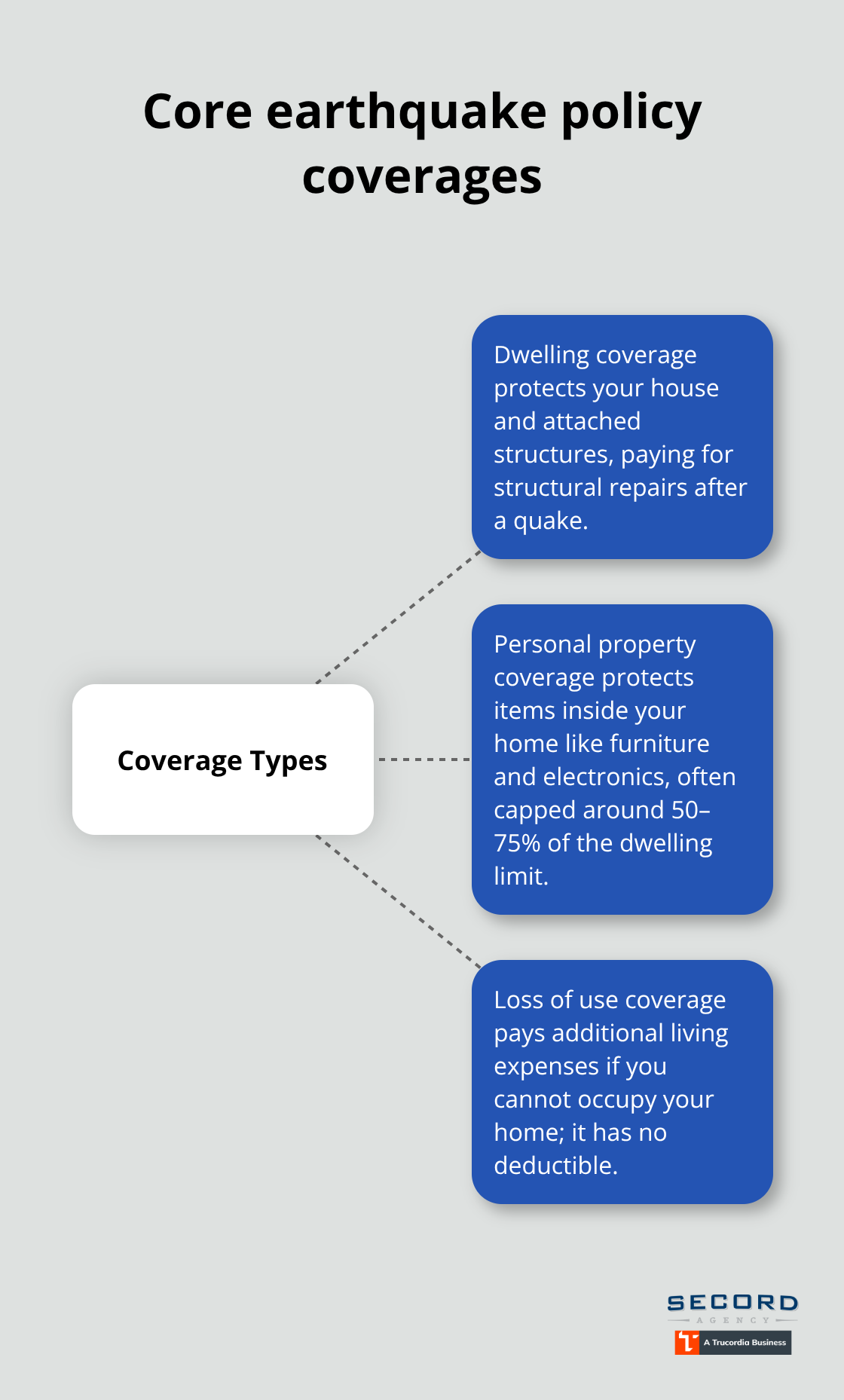

Earthquake insurance policies offer three fundamental coverage types, and the combination you select determines both your premium and what actually gets paid after a quake. The California Earthquake Authority, which provides most earthquake insurance in California, includes dwelling coverage that protects your house and attached structures, personal property coverage for items inside your home like furniture and electronics, and loss of use coverage that pays additional living expenses if you cannot occupy your home. In Washington state, premiums typically range from $3 to $15 per $1,000 of coverage annually, with your deductible choice creating the largest price difference between policies.

How Deductibles Shape Your Out-of-Pocket Costs

Moving from a 10% deductible to a 20% deductible roughly halves your premium, but this savings comes with real financial consequences when an earthquake strikes. A homeowner with a $300,000 dwelling limit and a 10% deductible faces a $30,000 out-of-pocket expense before insurance pays anything, while the same home with a 20% deductible means a $60,000 threshold. The Washington State Department of Insurance recommends calculating your break-even point before selecting a deductible-the damage amount where insurance payout begins-then weighing whether you can afford that out-of-pocket cost if an earthquake causes moderate damage to your home. Most homeowners underestimate how much damage a moderate earthquake causes, which is why understanding your specific financial capacity matters more than chasing the lowest premium.

Replacement Cost and Coverage Limits That Protect You

Replacement cost coverage is the only acceptable option for earthquake policies because actual cash value subtracts depreciation from payouts, leaving you short when rebuilding to current building codes. Your dwelling coverage limit should reflect current reconstruction costs, not the price you paid for your home years ago. If you purchased earthquake insurance five years ago with a $250,000 dwelling limit but construction costs have risen 20%, you now face a $50,000 shortfall that insurance will not cover. The California Earthquake Authority includes building code upgrade coverage in every policy-$10,000 standard, with higher limits available-which helps pay for upgrades needed to obtain reconstruction permits when rebuilding to current standards.

Personal property coverage protects your belongings inside the home and typically maxes out at 50–75% of your dwelling limit, meaning a $300,000 home might include only $150,000–$225,000 in personal property protection. Loss of use coverage has no deductible and pays rent, food, moving, and storage costs if you cannot occupy your home, making this the single most valuable rider after a major quake displaces you for months.

Shopping Multiple Carriers Reveals Real Savings

Obtaining three to five quotes from different insurers for your specific property reveals premium differences that often exceed 30–40% between carriers for identical coverage. Your property inspection may highlight the most impactful retrofits for your home, and these improvements can reduce premiums significantly-a properly retrofitted older home qualifies for substantial discounts, potentially up to 25% according to the California Department of Insurance. Bundling earthquake insurance with your homeowners policy unlocks multi-policy discounts of roughly 10–20%, which also simplifies policy management by keeping multiple lines with one insurer and one renewal date.

Final Thoughts

Earthquake protection for homeowners in seismic zones requires action on two fronts before disaster strikes. Retrofit your home by bolting the foundation, bracing cripple walls, and securing water heaters-these upgrades cost $3,000 to $7,000 but prevent catastrophic structural failure and qualify you for insurance discounts up to 25 percent. Then purchase earthquake insurance with coverage limits reflecting current reconstruction costs, a deductible you can afford if moderate damage occurs, and loss of use coverage that pays your living expenses if you cannot occupy your home.

Federal disaster relief typically provides low-interest loans rather than grants, leaving you to rebuild using borrowed money if you lack proper insurance. Premium differences between insurers often exceed 30 to 40 percent for identical coverage, and bundling earthquake insurance with your homeowners policy unlocks discounts of 10 to 20 percent while simplifying policy management. The 2001 Nisqually earthquake and New Zealand’s Christchurch disaster both proved that homeowners who acted before disaster struck recovered faster and with less personal financial strain.

We at Secord Agency – A Trucordia Business shop multiple carriers to deliver competitive rates paired with fast, local service that simplifies quotes and claims. Contact us today for a no-cost earthquake insurance quote tailored to your home and risk profile-your protection plan starts with understanding your actual costs and coverage options.