Homeowners Claims Process Washington: Step-By-Step to Faster Settlements

Filing a homeowners insurance claim in Washington doesn’t have to be complicated or slow. Most homeowners lose weeks waiting for settlements simply because they don’t know what insurers expect or how the process actually works.

We at Secord Agency – A Trucordia Business have helped countless Washington homeowners navigate their claims and get paid faster. This guide walks you through exactly what happens at each stage, what mistakes to avoid, and how to speed things up.

What Happens When You File Your Claim

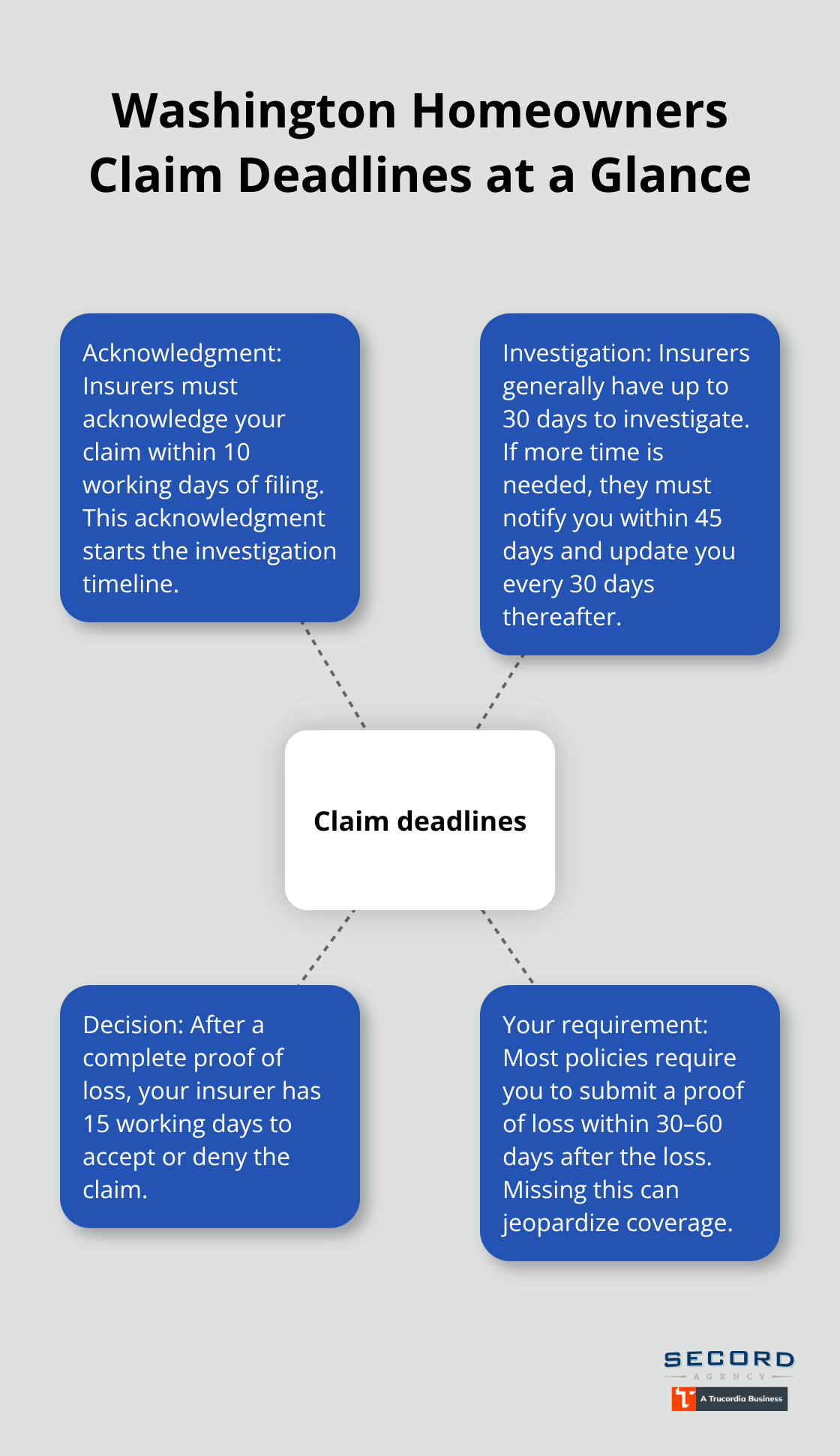

The moment you file a homeowners claim in Washington, a 10-working-day clock starts ticking. According to Washington Department of Insurance regulations, your insurer must acknowledge receipt of your claim within that window. This acknowledgment officially starts the investigation process and locks in your claim date. Call your agent or insurer directly rather than relying on online portals alone; a phone call creates a documented first notice of loss that you can reference later if timelines slip. When you call, have your policy number ready and write down the date, time, and the name of the person who took your information.

This single step prevents disputes about when you actually reported the loss.

What Adjusters Actually Look For

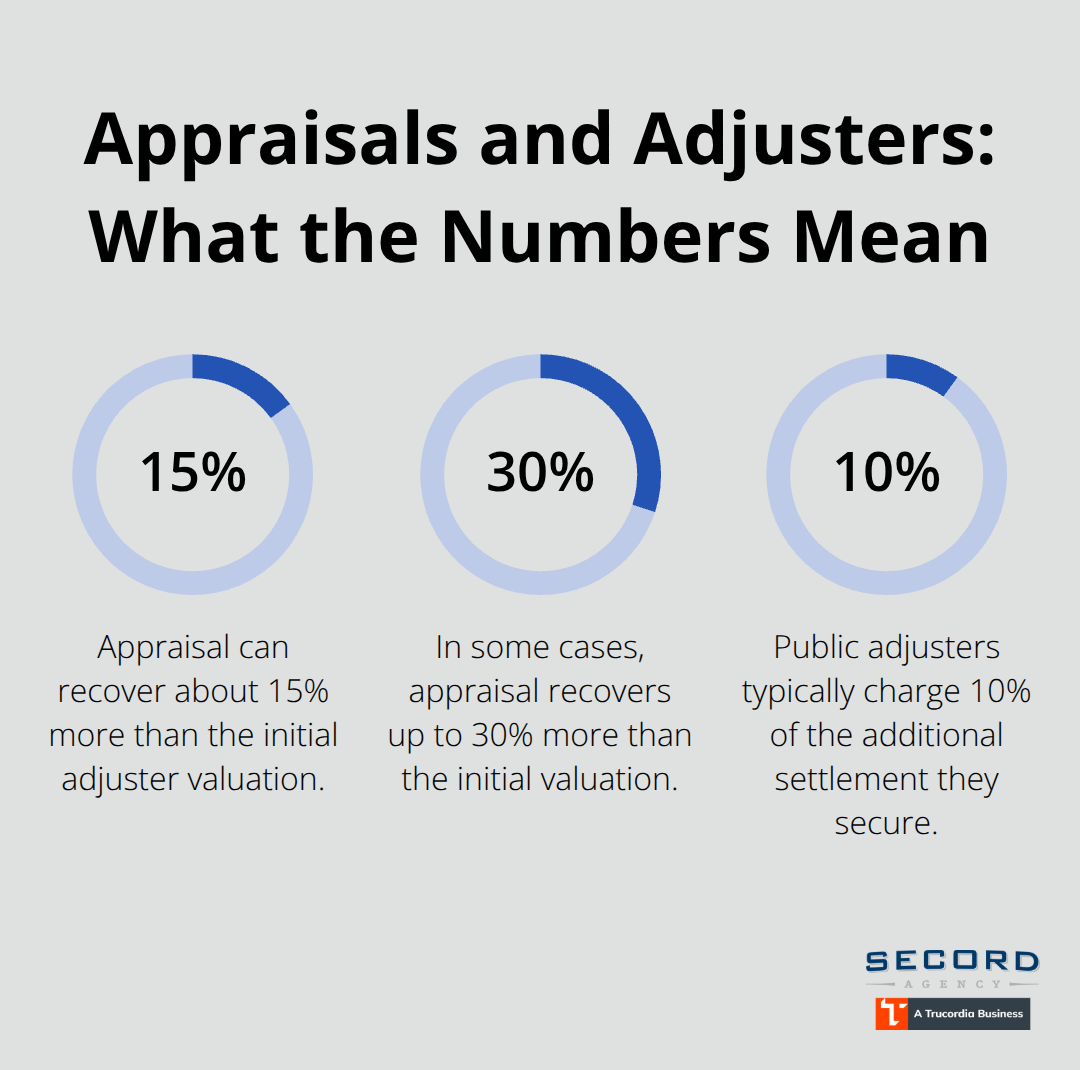

Insurance adjusters don’t just show up and eyeball your damage. They’re trained to match physical evidence against your policy language, which means they look for specific details that either support or limit your payout. An adjuster will photograph damage from multiple angles, check for pre-existing conditions, and verify whether the loss falls under your coverage. Washington Department of Insurance rules give insurers up to 30 days to complete their investigation after you file, though they can request an extension if they notify you within 45 days and continue notifying you every 30 days after that. Don’t wait passively during this period. Collect receipts, repair estimates, and photos of the damage yourself before the adjuster arrives. If you disagree with the adjuster’s assessment, Washington law gives you the right to request an appraisal, which brings in a neutral third party to evaluate the loss amount. Many homeowners skip this step and accept lowball offers, but an appraisal often recovers thousands of dollars in additional coverage.

The Real Timeline You’re Looking At

After your proof of loss is submitted and fully completed, your insurer has 15 working days to accept or deny the claim. If they need more time, they must notify you within 45 days with a specific reason and continue updating you every 30 days. Most settlements take 30 to 60 days total if documentation is complete and there are no disputes. However, this timeline assumes you submit everything promptly and don’t miss deadlines. The biggest delays happen because homeowners submit incomplete proof of loss forms. The insurer then spends weeks asking for missing receipts, contractor estimates, or photos instead of moving toward payment.

How to Submit Documentation That Moves Your Claim Forward

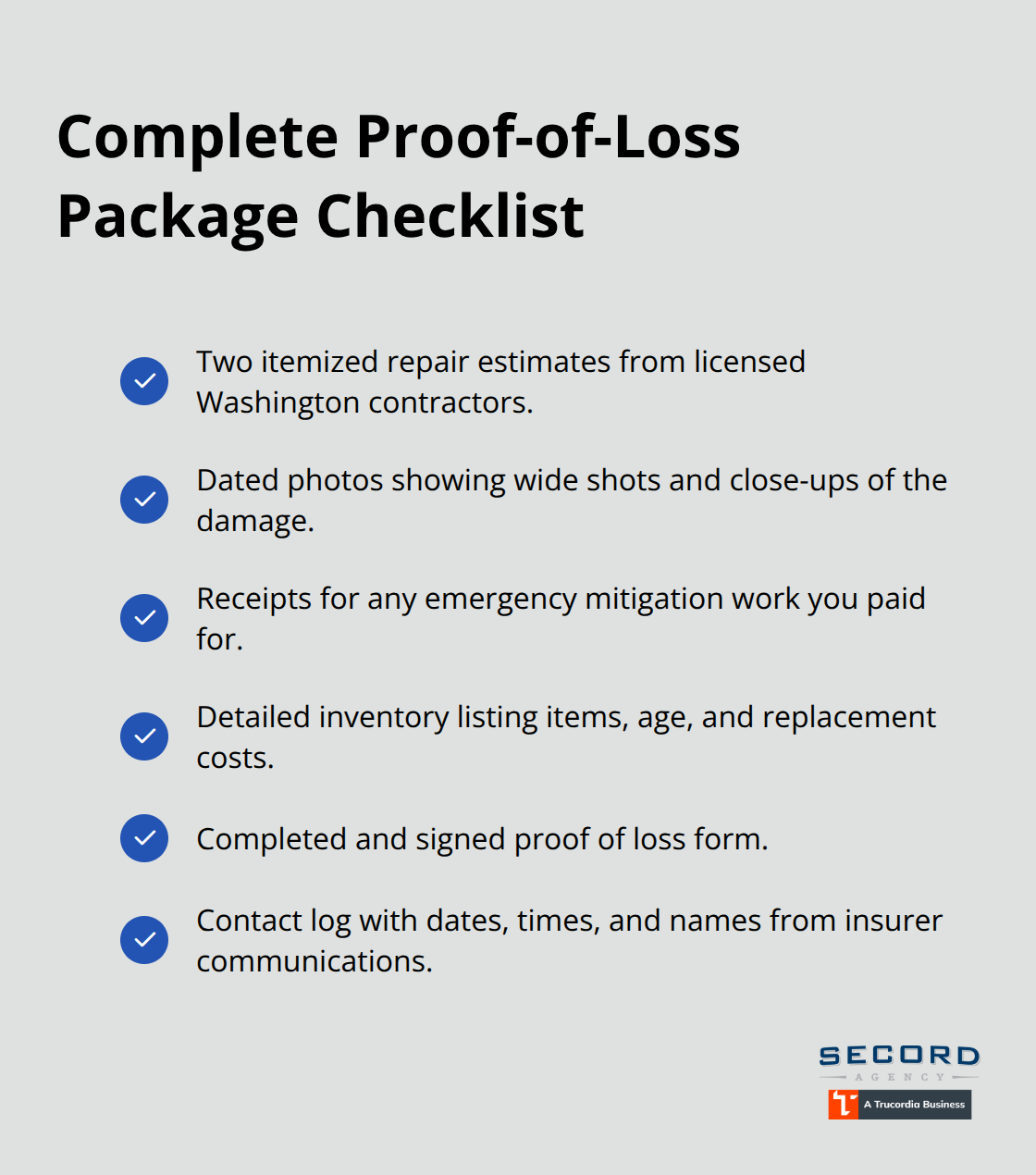

Submit your proof of loss within 30 days of the loss if possible-your policy likely requires this, and speed matters. Organize all supporting documents before you submit: itemized repair estimates from at least two contractors, photos showing before-and-after damage, receipts for any emergency mitigation work, and a detailed inventory of damaged property. When your insurer receives everything at once, they can move straight into settlement discussions rather than playing back-and-forth email tag. This approach (complete documentation submitted upfront) eliminates the most common source of delays in Washington homeowners claims. The faster you compile and submit these materials, the faster your settlement arrives.

Common Mistakes That Slow Down Your Claim

Incomplete Documentation Destroys Your Timeline

Incomplete documentation is the single biggest reason homeowners in Washington experience claim delays. Most insurers require your proof of loss within 30 to 60 days of the loss according to your policy terms, and anything submitted after that window can trigger denial or coverage disputes. Homeowners repeatedly submit partial documentation-a few photos but no contractor estimates, or estimates without receipts for emergency repairs. When your insurer receives incomplete paperwork, they don’t move forward to settlement; instead, they send you a request for missing items and the clock resets. You’re now waiting another week or two for their follow-up, then another week to compile what they asked for. This back-and-forth cycle easily adds 30 to 45 days to your settlement.

The fix is straightforward: gather everything the adjuster will need before you submit anything. That means repair estimates from at least two licensed contractors in Washington, dated photos showing the full extent of damage from multiple angles, receipts for any mitigation work you paid for out of pocket, and a detailed inventory listing damaged items with their replacement costs. Submit all of this in one package. Insurers move fast when they have complete information; they stall when they’re waiting on you.

Missing Deadlines and Policy Requirements

Missing policy deadlines is equally destructive, yet many homeowners don’t realize their policy contains specific timelines they must follow. Washington Department of Insurance regulations require insurers to acknowledge your claim within 10 working days, but your policy sets the deadline for when you must submit your proof of loss-typically 30 to 60 days after the loss. If you miss this deadline, the insurer can deny your claim outright.

Another critical mistake is not understanding what your policy actually covers. Many homeowners assume standard homeowners policies cover everything, then get shocked when the adjuster denies water damage, mold remediation, or code upgrade costs. Your policy language determines what is owed, and exclusions are buried in the fine print. Before filing, request your complete policy documents from your agent and read the coverage limits, exclusions, and endorsements section carefully.

Understanding Your Coverage Limits Before Filing

Look specifically for sub-limits on water damage, which often cap payouts at $5,000 to $10,000 even if your total claim is much higher. Check whether you have law and ordinance coverage, which helps pay for bringing your home up to current building codes after a covered loss-this coverage is optional and many policies don’t include it. If your home is in a flood zone, standard homeowners insurance excludes all flood damage; you must purchase separate flood insurance through the National Flood Insurance Program.

The moment you understand your actual coverage limits, you know exactly what you can claim and what you cannot. This knowledge eliminates disputes with your adjuster down the line and positions you to move into the next phase of your claim with confidence. Your documentation strategy and timeline adherence matter far less if you’re fighting over what your policy actually covers.

How to Speed Up Your Settlement

Prepare Complete Documentation Before Filing

Complete documentation before filing isn’t optional-it’s the fastest path to payment. Contact two or three licensed contractors in Washington and request written repair estimates that itemize labor, materials, and timeline. These estimates must be detailed enough that an adjuster can verify costs; vague estimates stating “roof repair: $8,000” won’t move your claim forward. Photograph your damage from multiple angles in good lighting, capturing wide shots showing the overall scope and close-ups of specific damage.

If you’ve already paid for emergency mitigation work like tarping a roof or removing water, collect those receipts immediately. Create a detailed inventory of damaged items with descriptions, approximate age, and replacement cost for each-this document alone accelerates settlements by weeks because adjusters don’t have to spend time requesting clarification. Package everything into one submission: estimates, photos, receipts, inventory, and your completed proof of loss form.

Complete submissions help move claims through investigation efficiently, while incomplete submissions stretch timelines due to back-and-forth requests for missing information.

Stay Actively Involved Throughout the Investigation

Your next move is to stay actively involved throughout the investigation rather than waiting passively. Call your insurer every 10 days to ask about the adjuster’s timeline and confirm they have all documentation. Record these calls with a note of the date, time, and person’s name-this documentation protects you if deadlines slip or communication breaks down.

If the adjuster’s valuation comes in lower than your contractor estimates, request an appraisal immediately rather than accepting their number. Washington law guarantees you this right, and appraisals frequently recover 15 to 30 percent more than initial adjuster valuations. Push back on any estimate that feels significantly lower than market rates for your area; adjusters sometimes lowball claims hoping homeowners won’t challenge them.

Consider Hiring a Public Adjuster for Complex Claims

If you’re dealing with complex damage like water intrusion, mold remediation, or code upgrade costs, consider hiring a public adjuster licensed in Washington to negotiate on your behalf. Public adjusters typically charge 10 percent of the settlement increase they recover, meaning you only pay if they get you more money. Their involvement signals to insurers that you’re serious about a fair settlement and eliminates delays caused by miscommunication or documentation gaps.

Final Thoughts

The homeowners claims process in Washington rewards those who act with speed and organization. You now understand what insurers expect, what mistakes cost you in wasted time, and how to move your settlement forward efficiently. Submit complete documentation upfront, understand your policy coverage limits before filing, and stay actively involved throughout the investigation-these three actions determine whether your claim closes in 30 to 60 days or stretches into months of frustration.

Washington’s regulations protect you in ways many homeowners never use. You hold the right to request an appraisal if you disagree with an adjuster’s valuation, and you can hire a public adjuster to negotiate on your behalf. An experienced local agent understands Washington’s unique claim environment, knows which contractors deliver reliable estimates, and guides you through policy language that trips up most homeowners. We at Secord Agency – A Trucordia Business have spent years helping Washington homeowners navigate claims and recover fair settlements, and our team stands beside you when you need to file.

Start protecting your home today by reviewing your current policy with a local agent who understands Washington properties. If you face a claim right now, gather your documentation, submit everything at once, and don’t accept a lowball offer without requesting an appraisal. Your settlement depends on how prepared you are and how actively you manage the homeowners claims process in Washington.