Washington Vacation Rental Insurance: What Hosts Should Know

Running a vacation rental in Washington means navigating permits, taxes, and regulations that most homeowners never encounter. Your standard homeowners policy won’t protect you from the unique risks that come with hosting guests.

At Secord Agency – A Trucordia Business, we’ve seen hosts lose thousands because their WA vacation rental policy didn’t cover guest injuries or property damage. This guide walks you through what you actually need to know.

Understanding Washington’s Vacation Rental Regulations

State-Level Requirements Every Host Must Meet

Washington State treats short-term rentals as commercial lodging operations, not hobby income. Under RCW 64.37, any stay under 30 nights triggers state-level obligations that go far beyond what most hosts realize. You need a Washington State Business License and a Unified Business Identifier (UBI) registered with the Department of Revenue. That’s the baseline. The state applies a 6.5% statewide lodging tax on stays under 30 nights, with local jurisdictions adding up to 2% basic lodging tax and up to 2% special lodging taxes on top. You must register for a Lodging Tax ID and collect and remit taxes on every booking.

The Permit Patchwork: No Single Statewide License

Here’s where it gets complicated: there is no single statewide vacation rental permit. Instead, each city and county issues its own licenses, zoning permits, and enforcement rules. Seattle requires two separate permits-a Business License Tax Certificate and a Short Term Rental Operator License from the Department of Construction and Inspections-each costing about $75. Your listing must display a license number in the exact format STR-OPLI-##-###### or you risk removal from major platforms and daily fines. Spokane tightened rules in 2026 with stricter administrative permits and zoning compliance. Vancouver, WA implemented a 24-month pilot requiring a city STR permit tied to zoning and capping the number of units you can operate. Walla Walla demands a city-issued permit, a local contact person, fire safety compliance with a working fire extinguisher, and adequate parking-with a $150 initial fee and annual renewal. Leavenworth uses a dense-permit system with a “one in, one out” rule, and permits may become non-transferable after September 2026, which could tank resale value. Bellingham limits rentals to primary residences only, requiring 270 days of primary use and only 95 days of rental annually.

Enforcement and Financial Penalties

The penalty for noncompliance is steep: Washington hosts face $500 per day fines for violations. This regulatory patchwork means two properties just miles apart face completely different rules. Operating an unlicensed STR in Seattle can incur heavy daily fines, and listings get removed by major platforms for missing license numbers.

The $1 Million Liability Insurance Mandate

Washington law mandates at least $1,000,000 in primary liability insurance per claim under RCW 64.37.050. That’s not optional-it’s the law. Your standard homeowners policy will not cover this because it excludes commercial short-term rental activity. Many hosts discover this only after a guest injury claim gets denied. If you list on platforms like Airbnb or Vrbo, the platform’s liability insurance can substitute for your own policy if it meets the $1,000,000 primary liability threshold, but you must verify this coverage exists and covers your specific property. Umbrella policies do not count as primary coverage and often sit on top of insufficient underlying policies, leaving gaps.

Market Opportunity and Increased Scrutiny

Seattle’s projected World Cup impact shows nightly rates could spike from around $200 to about $380, but that higher revenue also means higher tax obligations and increased scrutiny from local authorities. Working with a professional manager or tax specialist who understands Washington’s county-by-county rules is not a luxury-it’s essential risk management. The regulatory landscape continues to shift as cities reshape STR policies around housing affordability, making compliance a moving target that requires constant attention.

Why Standard Homeowners Insurance Fails Vacation Rental Hosts

The Commercial Reality Your Policy Doesn’t Cover

Your homeowners insurance policy protects you from risks like theft, fire, or a guest slipping on your front porch once a year. It was never designed for the commercial reality of vacation rental hosting, where strangers occupy your property for days at a time, multiple times per month. The moment you list your property on Airbnb or Vrbo, your standard homeowners policy becomes nearly worthless for the actual risks you face.

Most homeowners policies explicitly exclude coverage for short-term rental activity. This isn’t a gray area or a loophole-insurers write it directly into the exclusions section. Insurance companies treat a vacation rental as a commercial operation, which sits outside the scope of residential coverage. When a guest files an injury claim, your homeowners insurer can deny coverage outright because you failed to disclose the rental activity.

What Happens When Claims Get Denied

Hosts lose significant amounts in legal fees and settlements because they believed their homeowners policy covered guest injuries. It doesn’t. The gap between what hosts believe they’re covered for and what they actually have coverage for is staggering.

Your homeowners policy offers almost no protection for rental-specific risks. Guest-caused damage, theft by guests, bed bugs, fleas, and squatter situations fall outside standard homeowners coverage entirely. If a guest damages your furniture, steals your kitchen equipment, or leaves bed bugs in your mattresses, your homeowners policy won’t pay for repairs or replacement.

Revenue Loss and Hidden Costs

Revenue loss from cancellations due to pest infestations or property damage also isn’t covered. A single infestation forces you to close for weeks, costing thousands in lost bookings while you treat and verify the problem is resolved. Your standard policy leaves you absorbing these losses alone.

Specialized short-term rental coverage addresses these exact gaps, including guest-caused theft and damage, amenity liability for items like hot tubs or kayaks, and bed bug and flea coverage. The cost of adding proper vacation rental insurance typically runs $40 to $80 per month, depending on your property value and location. Compared to a single liability claim or revenue loss from property damage, that cost is trivial.

The Legal and Financial Risk

Washington hosts operating without the right insurance violate state law under RCW 64.37.050 while gambling with their most valuable asset. The regulatory requirements demand at least $1 million in liability insurance-a threshold that standard homeowners policies simply cannot meet. Understanding what types of coverage actually protect your rental operation requires examining the specific policies designed for this business model.

Getting the Right Coverage for Your Washington Vacation Rental

Match Your Policy to Your Actual Risks

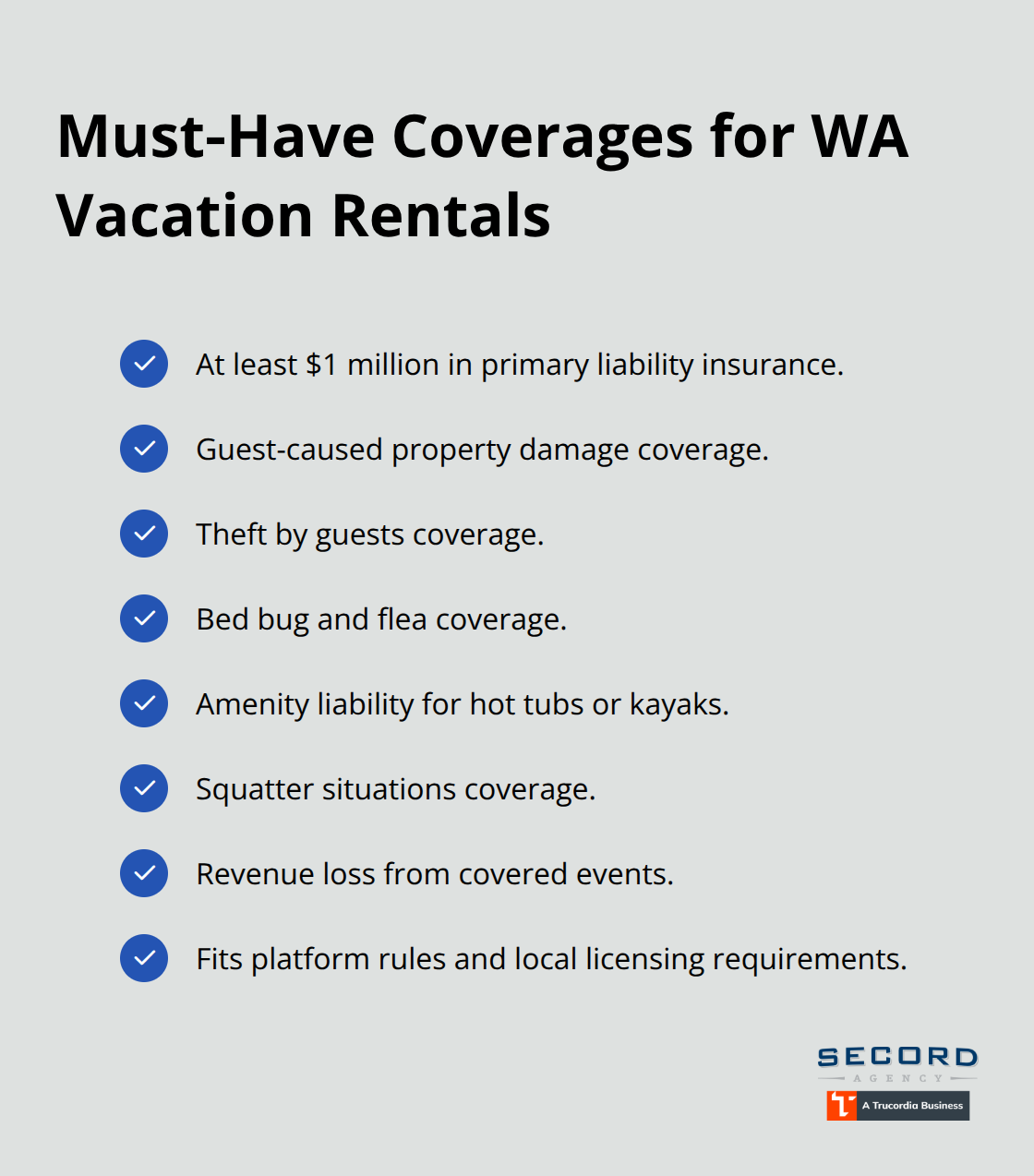

Choosing vacation rental insurance means understanding what specific risks your property faces and matching them to actual policy language, not marketing promises. Washington hosts need short-term rental insurance that covers at least $1 million in primary liability insurance, guest-caused property damage, theft by guests, and revenue loss from covered events like bed bug infestations or squatter situations. Standard short-term rental policies from carriers like Proper Insurance, endorsed by Vrbo as their preferred provider, typically bundle these coverages together rather than forcing you to piece together multiple policies.

Understand What Platform Coverage Actually Covers

Many hosts assume platform coverage like AirCover substitutes for their own policy, but AirCover has documented gaps and covers only specific claim types. Washington law allows platform-provided liability insurance to satisfy the $1 million requirement if it meets the primary liability threshold, but you must verify this in writing with the platform and understand what events it excludes. If you operate across multiple platforms, each platform must provide at least $1 million in primary liability coverage or you must carry your own policy that covers all properties.

Request Specific Coverage Details and Compare Quotes

When comparing providers, request a 3-minute quote and ask directly whether the policy covers guest-caused theft, amenity liability for items like hot tubs or kayaks, bed bugs and fleas, and squatter situations. The $40 to $80 monthly cost varies based on property value, location, number of rental units, and whether your property is your primary residence. Hosts in Seattle or other regulated cities should prioritize compliance-focused policies that verify you meet local licensing requirements, since operating without proper permits creates insurance gaps anyway.

Reduce Costs Through Smart Risk Management

Cost savings come from bundling coverages rather than purchasing à la carte, maintaining a clean claims history, and installing loss-prevention measures like security cameras or noise-monitoring technology that reduce your risk profile. A quick 15-minute policy review with a licensed agent reveals whether your current coverage actually covers short-term rental activity or contains exclusions that would leave you exposed during a claim. This verification step protects you from discovering gaps only after a claim gets denied.

Verify Your Coverage Meets State Requirements

Washington law mandates at least $1 million in primary liability insurance per claim under RCW 64.37.050-a threshold that standard homeowners policies simply cannot meet. Operating without compliant coverage exposes you to regulatory fines while leaving your property and income unprotected. A licensed agent can help you verify your protection aligns with state regulations and platform requirements, offering personalized advice tailored to your specific rental configuration and local zoning rules.

Final Thoughts

Running a vacation rental in Washington requires protection that goes far beyond what your homeowners policy provides. The state’s $1 million liability insurance mandate, combined with city-specific permit requirements and lodging tax obligations, creates a legal and financial landscape that demands real coverage. Standard homeowners policies explicitly exclude short-term rental activity, leaving hosts exposed to claim denials, regulatory fines, and revenue loss from property damage or pest infestations.

Your WA vacation rental policy must address the specific risks your property faces: guest-caused damage and theft, amenity liability for hot tubs or kayaks, bed bug and flea coverage, and squatter situations. These gaps don’t exist in traditional homeowners coverage because insurers never designed those policies for commercial rental operations. A specialized short-term rental policy costs $40 to $80 monthly and covers exactly what your business needs.

Start by verifying your current coverage actually includes short-term rental activity rather than discovering exclusions after a claim gets denied. Request a 3-minute quote from a provider and ask directly about guest-caused theft, amenity liability, and pest coverage. Contact us for personalized guidance on your specific rental configuration and local zoning rules, and we’ll help you verify that your protection aligns with Washington’s state requirements and your local city’s specific rules.