Non-Owner Auto Insurance Explained: Do You Need It?

You don’t have a car, but you drive regularly. Maybe you rent vehicles for business trips or borrow your friend’s sedan on weekends. That’s where non-owner auto insurance comes in-it fills the gap when you need coverage without owning a vehicle.

At Secord Agency – A Trucordia Business, we help drivers understand their insurance options. This guide breaks down what non-owner auto insurance covers, when you actually need it, and how it stacks up against other choices.

What Non-Owner Coverage Actually Protects

Non-owner auto insurance covers liability when you cause an accident in a vehicle you don’t own. If you hit another car, injure someone, or damage property while driving a borrowed sedan or rental, your policy pays for the other person’s medical bills, lost wages, and property repairs up to your coverage limits. Bodily injury liability covers medical expenses and related costs for injured parties, while property damage liability handles repair or replacement of damaged vehicles and other property.

Understanding Your Coverage Limits

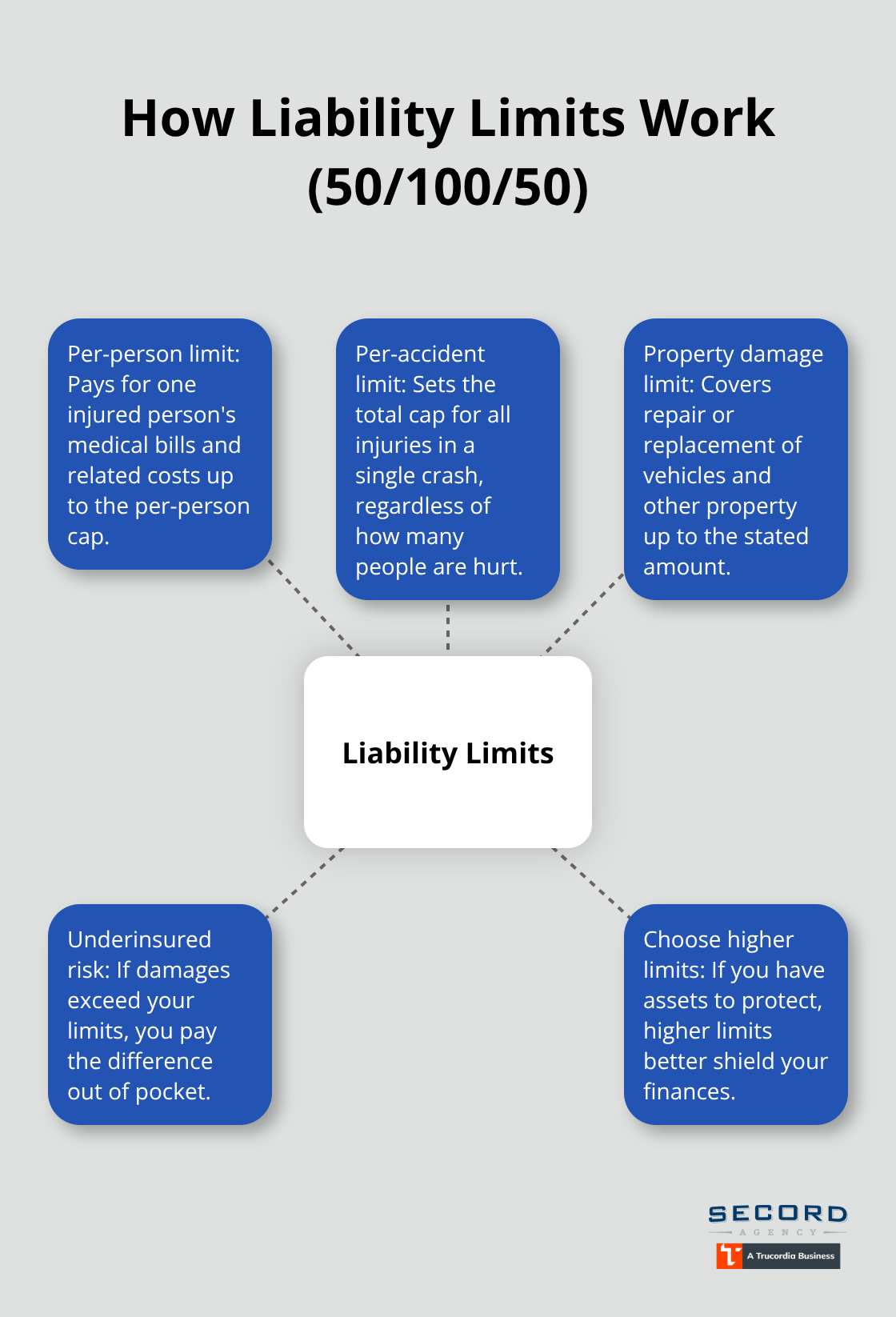

The coverage limits you choose directly determine your financial protection. A 50/100/50 limit means $50,000 per person for injuries, $100,000 total per accident, and $50,000 for property damage. These aren’t arbitrary numbers; they reflect how much you’re willing to risk personally.

If you cause an accident with $200,000 in damages and your limit is only $50,000, you’re personally liable for the remaining $150,000. This is why higher limits matter, especially if you have assets to protect.

What Your Policy Won’t Cover

Non-owner insurance explicitly excludes damage to the vehicle you’re driving. If you rent a car and cause an accident, your non-owner policy covers the other driver’s injuries and property damage, but not the rental car itself. You’ll need the rental company’s collision damage waiver or your credit card’s rental coverage to handle that. The policy also doesn’t cover your own medical bills unless you add Medical Payments coverage, which typically costs $10–20 more monthly.

Business-related driving is another major exclusion. If you use a borrowed car for work deliveries or client meetings, you’re not covered. Your personal belongings inside the car, theft, vandalism, and weather damage all fall outside the scope. Some insurers extend coverage to spouses listed on the policy, but most won’t cover other household members or drivers unless specifically named, so verify this before lending someone your borrowed vehicle.

Why Coverage Limits Matter More Than Price

The national average for non-owner insurance runs around $748 annually according to Quadrant Information Services, but prices vary dramatically by insurer. Auto-Owners quotes at roughly $202 per year while Progressive reaches $1,189. This wide range tempts drivers toward cheaper options, but selecting limits based on price rather than protection creates real financial exposure.

If you frequently borrow or rent vehicles, try carrying at least 100/300/100 limits-$100,000 per person, $300,000 per accident, and $100,000 for property damage. This protects your assets from lawsuit judgments that regularly exceed $500,000 in serious injury cases. Adding uninsured motorist coverage protects you if hit by a driver with insufficient insurance, and medical payments coverage ensures your medical bills get paid regardless of fault. These add-ons increase your premium but eliminate coverage gaps that could cost far more later. Understanding when you actually need non-owner coverage requires honest assessment of your driving habits and the vehicles you access most often.

When You Actually Need Non-Owner Coverage

Frequency Determines Your Coverage Decision

Renting a car twice a year for vacation doesn’t justify non-owner insurance. Grabbing a rental every month for business trips does. The dividing line between needing this coverage and skipping it comes down to frequency and financial exposure. If you rent vehicles more than four times annually or regularly borrow cars from friends and family, non-owner insurance makes financial sense. A single accident while driving a borrowed vehicle could expose you to liability claims that exceed the vehicle owner’s policy limits, leaving you personally responsible for the excess.

The Math Behind Monthly Premiums

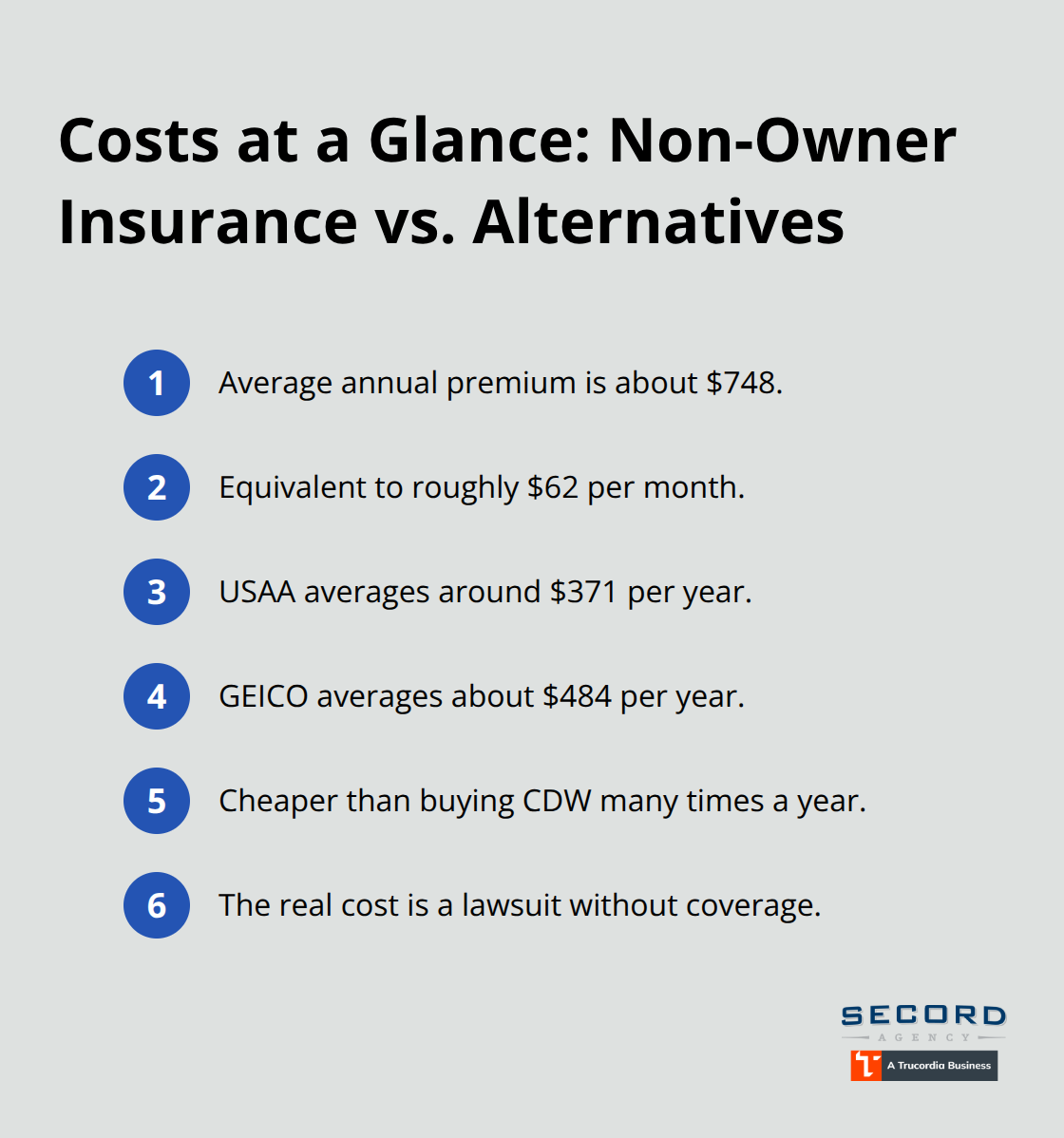

When you rent frequently, carrying your own liability policy costs roughly $748 annually on average according to Quadrant Information Services, which breaks down to about $62 monthly. That’s cheaper than buying collision damage waiver protection from rental agencies multiple times per year, and it provides consistent coverage across different rental companies and borrowed vehicles. USAA customers pay around $371 annually while GEICO averages $484, so shopping quotes from multiple carriers matters.

The real expense isn’t the premium; it’s the lawsuit judgment you’d face without coverage.

SR-22 Requirements and Legal Obligations

State mandatory insurance laws create a harder requirement in some situations. If you’ve had your driver’s license suspended or received multiple violations, your state likely requires proof of insurance through an SR-22 filing, and non-owner policies satisfy this requirement in most states. This applies whether you own a vehicle or not.

Maintaining Coverage History Between Vehicles

Maintaining continuous coverage after losing your own policy serves a practical purpose beyond legal compliance. Insurance companies review your coverage history when you apply for new policies, and gaps in coverage raise your rates. If you sell your car and won’t own another for six months, carrying non-owner insurance for that period keeps your record clean and prevents rate increases when you eventually buy a replacement vehicle. Some insurers offer temporary non-owner policies lasting just a few months, which costs less than permanent coverage but maintains your continuous insurance history. This approach costs roughly $200–300 for a three-month period, protecting both your driving record and your future premiums.

Understanding your specific situation helps you decide whether non-owner coverage fits your needs. The next section compares how non-owner policies stack up against other insurance options available to drivers without vehicles.

How Non-Owner Policies Stack Up Against Your Other Options

Named Driver vs. Non-Owner Coverage

Non-owner insurance differs fundamentally from adding yourself as a named driver to someone else’s policy, and the distinction matters for your wallet and your protection. When you’re added as a named driver to a vehicle owner’s policy, their policy limits apply to you, which means you depend on their coverage choices and their insurer’s willingness to pay claims. If the owner carries minimal limits and you cause a serious accident, you’re personally liable for amounts exceeding their policy. Non-owner policies flip this dynamic-you control your own coverage limits rather than depending on someone else’s choices, making you the primary insured rather than a secondary driver. This independence costs more than being named on someone else’s policy but provides substantially better protection. If you frequently borrow from multiple people or rent different vehicles, being named on individual policies becomes impractical and impossible. Non-owner coverage follows you as the driver rather than tying coverage to specific vehicles or owners.

The Real Cost Comparison

A standard auto policy for vehicle owners averages $1,500–2,000 annually depending on driving history and location, while non-owner coverage runs roughly $748 per year according to Quadrant Information Services data. This comparison misleads because you’re not comparing equivalent coverage. If you rent four times yearly at $35–50 per day for collision damage waiver protection, you spend $560–800 annually just on rental coverage, plus you lack liability protection between rentals. Non-owner insurance at $62 monthly covers you across unlimited rentals and borrowed vehicles simultaneously.

For occasional drivers who rent fewer than three times yearly, skipping non-owner insurance and purchasing collision damage waiver at each rental makes financial sense-you’d spend roughly $420–600 annually on rental waivers while avoiding the monthly premium. But for anyone renting monthly or borrowing regularly, the math shifts decisively toward non-owner coverage. The real alternative to non-owner policies isn’t traditional auto insurance-it’s accepting uninsured liability exposure or relying on other drivers’ policies, both of which create dangerous financial gaps.

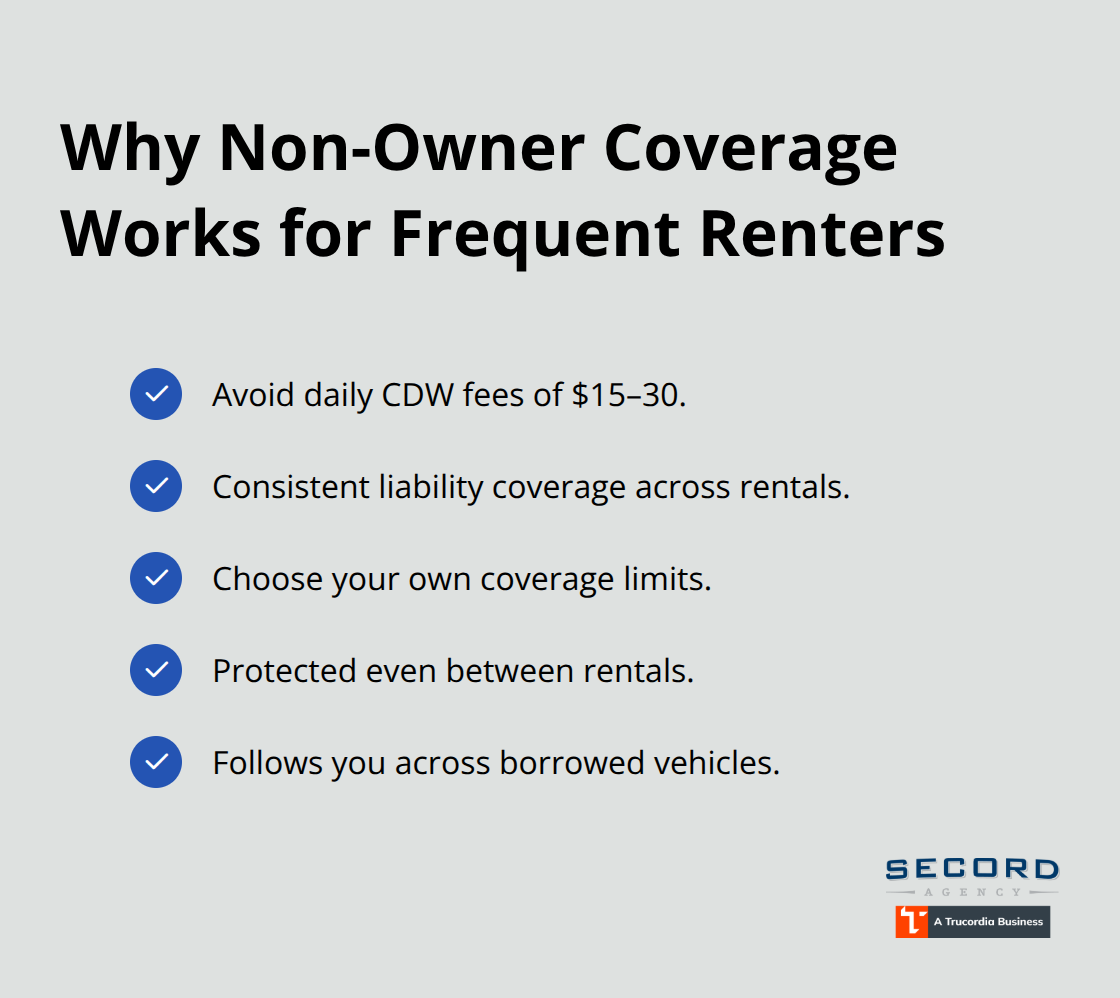

Why Non-Owner Coverage Wins for Frequent Renters

Rental agencies charge $15–30 daily for collision damage waiver protection, which adds up fast when you rent multiple times per year. Non-owner insurance provides consistent liability coverage across all rentals and borrowed vehicles without per-rental fees. You control your coverage limits rather than accepting whatever the rental company offers, and you maintain protection even when you’re not actively renting. This consistency matters because coverage gaps between rentals leave you exposed to liability claims. A single accident during an uninsured period could cost far more than years of non-owner premiums.

Final Thoughts

Non-owner auto insurance solves a specific problem: you drive regularly but don’t own a vehicle. The coverage protects others from your liability while you rent or borrow cars, and it costs substantially less than traditional auto policies. Whether this protection makes sense for your situation depends on three concrete factors: your driving frequency, your asset protection needs, and any legal requirements in your state.

Assess your driving frequency first. If you rent vehicles more than four times annually or regularly borrow from friends and family, non-owner auto insurance pays for itself compared to purchasing collision damage waivers at each rental. The national average of $748 yearly breaks down to roughly $62 monthly, which undercuts the $15–30 daily rental fees most agencies charge. For occasional drivers renting fewer than three times per year, skipping the policy and buying per-rental protection remains cheaper.

Consider your asset protection second. Coverage limits directly determine your personal financial exposure after an accident, and carrying 100/300/100 limits protects you from lawsuit judgments that regularly exceed $500,000 in serious injury cases. Adding uninsured motorist and medical payments coverage eliminates additional exposure for roughly $10–20 monthly. Contact Secord Agency – A Trucordia Business for a free quote and personalized guidance on whether non-owner auto insurance fits your situation.