Washington Homeowners Insurance Quotes: Quick Local Estimates

Getting Washington homeowners insurance quotes shouldn’t feel overwhelming. Your home is likely your biggest investment, and finding the right coverage at the right price matters.

We at Secord Agency – A Trucordia Business help Washington homeowners navigate their insurance options every day. This guide walks you through what affects your rates, how to compare quotes effectively, and why working with a local agent makes a real difference.

What Drives Your Washington Home Insurance Rate

Replacement Cost Sets Your Premium Foundation

Your home’s replacement cost is the single biggest factor determining your premium, and most Washington homeowners underestimate this number significantly. The average Washington home costs over $600,000 to replace, according to Zillow data, yet many policies are written with dwelling coverage far below that figure. When repair and replacement costs spike-as they have due to material shortages and labor constraints following COVID-19-your premium follows. Washington premiums jumped 16.6% in 2023 and 21.7% in 2024, according to the Washington State Office of the Insurance Commissioner, with elevated construction costs cited as the primary driver.

Your home’s market value and its rebuild cost are completely different numbers. A $500,000 home might cost $650,000 to rebuild from scratch. Before getting quotes, measure your home’s square footage, note your roof material, and research local construction costs in your ZIP code. To estimate your replacement cost, multiply your home’s square footage by average building costs per square foot in your area. This gives you a realistic replacement cost figure to share with agents, ensuring your quotes reflect actual coverage needs rather than guesswork.

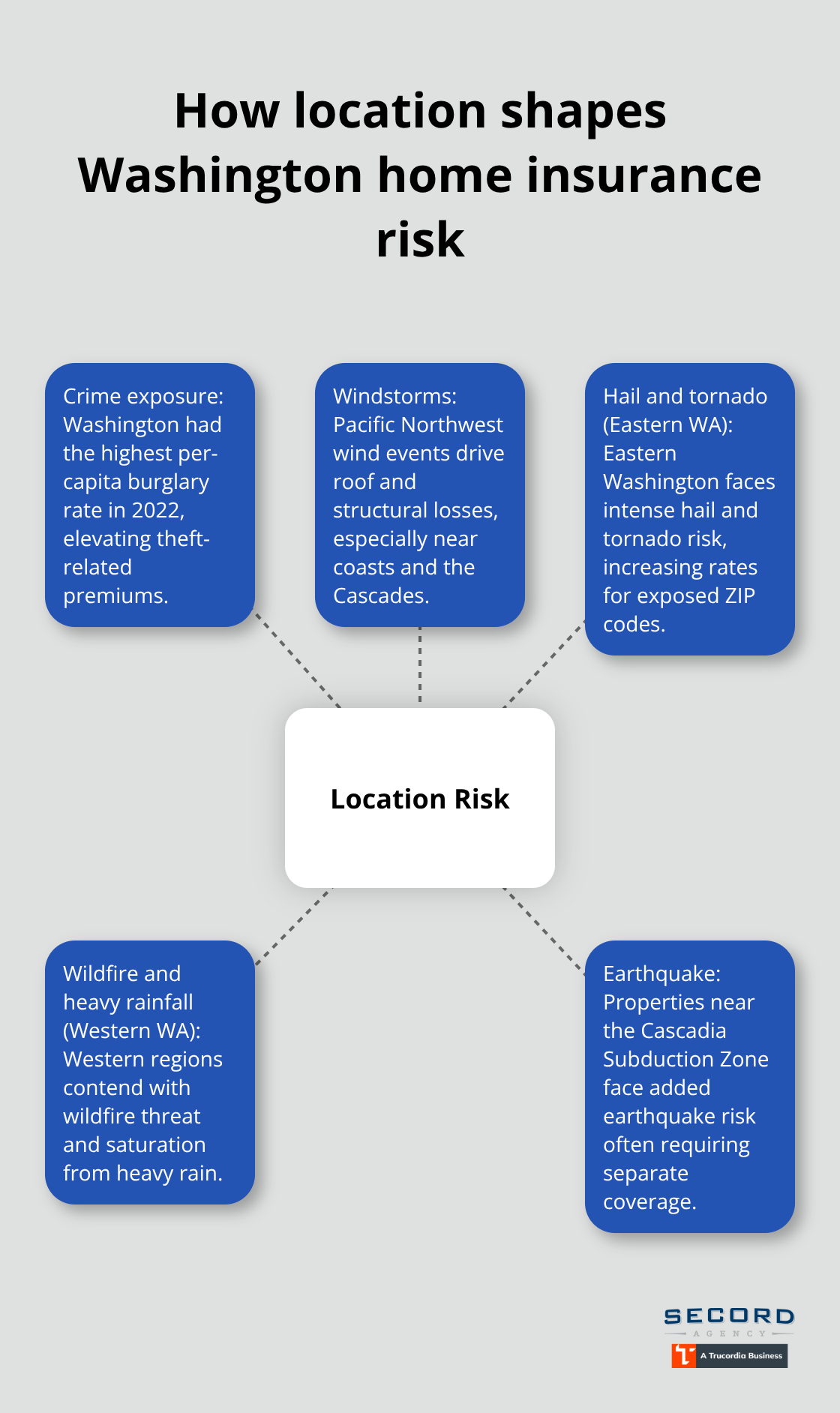

Location Determines Your Rate More Than Almost Any Other Factor

Your ZIP code influences your rate because it reflects local disaster exposure, crime rates, and claims history. In 2022, Newsweek reported Washington had the highest per-capita burglary rate in the nation, pushing theft risk premiums upward statewide. Weather compounds this-the Pacific Northwest’s windstorms cause significant roof and structural damage annually, with coastal areas and properties near the Cascades facing elevated wind exposure.

Eastern Washington faces intense hail and tornado risk, while western regions deal with wildfire threat and saturation from heavy rainfall. Earthquake risk adds another layer, particularly for properties near the Cascadia Subduction Zone. When you request quotes, the agent will ask for your exact address because rates vary dramatically within cities. A Seattle home and a Spokane home of identical construction and value can have premiums differing by hundreds of dollars annually.

Home Age and Construction Type Amplify Location Risk

Wood-frame homes in high-wind zones cost more to insure than brick structures in stable neighborhoods. Safety features like updated electrical systems, reinforced roofs, and functioning sprinklers reduce your rate substantially because they lower claim frequency. If your home was built before 1980, expect higher premiums unless you’ve upgraded the roof, plumbing, or electrical system recently.

These factors (age, materials, and safety upgrades) work together to shape your final quote. An older wood-frame home in a coastal zone will carry a much steeper premium than a newer brick home inland. Conversely, a pre-1980 home with recent major upgrades can compete on price with newer construction. Understanding what your specific property brings to the table helps you anticipate quote ranges and identify which improvements deliver the fastest premium reductions.

What Happens When You Compare Quotes

Getting multiple quotes reveals how different carriers weight these factors. One insurer might prioritize your home’s age heavily, while another focuses on location risk. This variation means shopping around isn’t optional-it’s how you find the rate that matches your property’s actual risk profile. The quotes you receive will show you exactly which factors matter most to each carrier, giving you concrete data to work with as you evaluate your options.

Getting the Right Information Before You Quote

Gathering the right details before contacting insurers saves hours of back-and-forth and produces quotes that actually reflect your coverage needs. Start with your home’s basic specifications: square footage, year built, number of stories, roof material, and foundation type. Next, document your safety features-updated electrical panel, newer roof, functioning sprinklers, deadbolts, and alarm systems all lower premiums. Include any recent renovations, especially roof replacements or major structural work, since these reduce claim risk substantially. You’ll also need your claims history from the past five years, your credit score (which factors into rates in Washington), and details about any prior lapses in coverage. Gather your property tax assessment if you have it, as it often reflects replacement cost estimates. The Washington State Office of the Insurance Commissioner maintains resources explaining how insurers rate policies, which helps you understand what information matters most. When you request quotes online or call agents, having these details prepared means you’ll receive accurate estimates rather than rough ballpark figures that change once underwriters review your complete application.

Three Quotes Reveal Your True Market Position

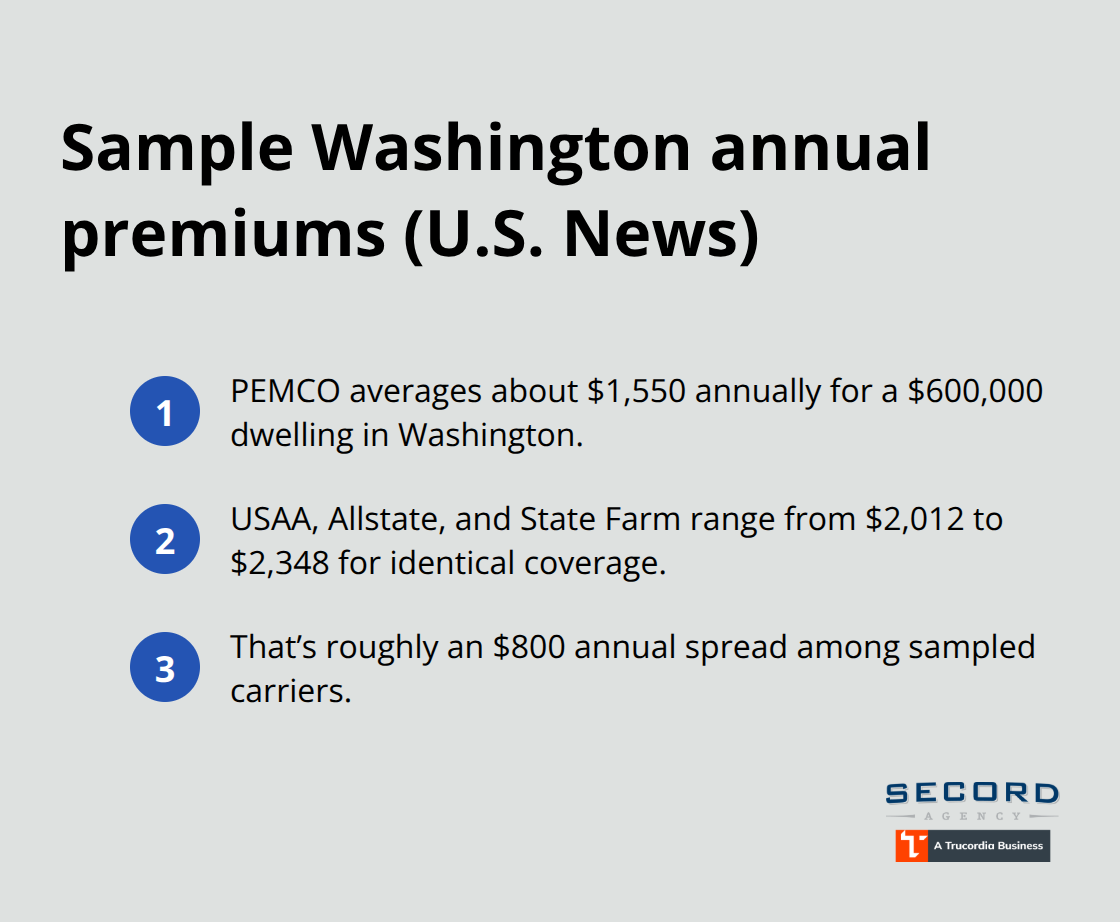

Three quotes minimum gives you a genuine market picture; two quotes might be coincidence, but three shows you where rates cluster and which carriers view your property differently. According to U.S. News rankings, PEMCO averages about $1,550 annually for a $600,000 dwelling in Washington, while other major carriers like USAA, Allstate, and State Farm range from $2,012 to $2,348 for identical coverage. This $800 annual spread matters, but the real value emerges when you examine what each quote includes.

Coverage Details Matter More Than Price Alone

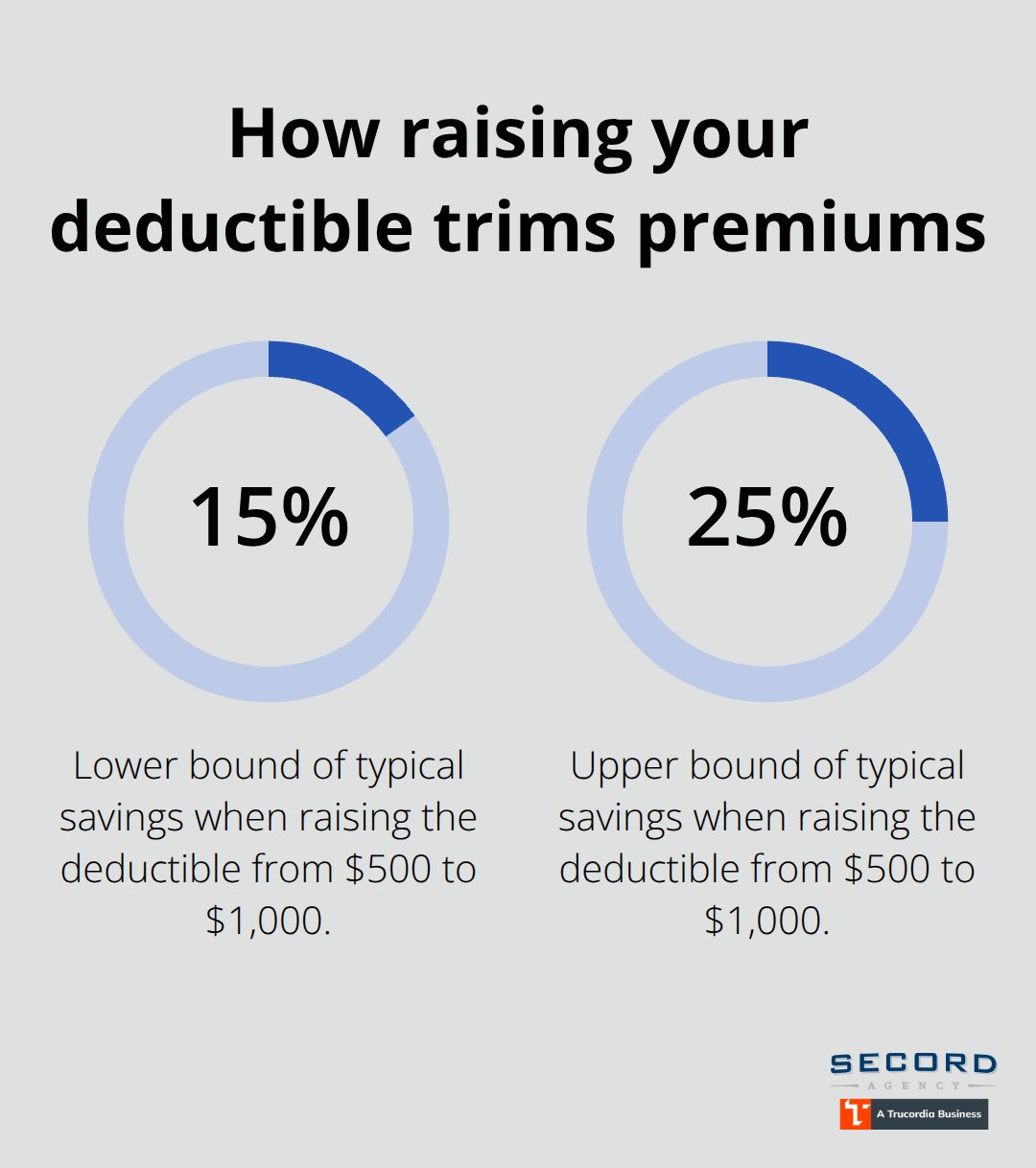

One carrier offers replacement cost coverage on personal property while another charges extra; another includes water backup protection standard while competitors exclude it. Deductible choices dramatically shift your quote-raising your deductible from $500 to $1,000 typically reduces annual premiums by 15 to 25 percent. Understanding coverage gaps matters more than chasing the lowest number.

Standard homeowners policies exclude flood and earthquake damage entirely, yet Washington faces both risks. If you live in a flood-prone area, you need inland flood coverage or a separate policy; if you’re near the Cascadia Subduction Zone, earthquake endorsements become essential. Compare quotes side-by-side using the same deductible and coverage limits across all carriers so you’re genuinely comparing apples to apples, then evaluate which insurer’s additional features and discount options align with your actual risk profile.

Local Agents Help You Navigate These Choices

An independent agent shops multiple carriers simultaneously, presenting you with options that match your specific property and budget. This approach eliminates the need to contact five insurers individually and wait for callbacks. The agent explains what each quote covers, identifies which exclusions matter for your situation, and recommends endorsements based on Washington-specific risks like wildfire or earthquake exposure. This personalized guidance transforms a stack of confusing quotes into a clear decision framework.

Why Your Local Agent Beats Shopping Solo

Independent agents fundamentally change how you approach Washington homeowners insurance because they handle the carrier legwork you’d otherwise manage alone. An independent agency shops multiple carriers simultaneously, which means you receive competitive quotes without contacting five separate insurers and waiting days for callbacks. This efficiency matters when you’re trying to renew coverage before a deadline or need quotes quickly after a life change. PEMCO, USAA, Allstate, State Farm, and Farmers each price risk differently, and an agent familiar with how each carrier weights factors like your home’s age, location, and construction type can predict which companies will offer the best rates for your specific property. Rather than submitting identical information to multiple insurers and comparing quotes yourself, an agent pre-screens carriers based on your situation, eliminating quotes that won’t be competitive before they reach your inbox.

Earthquake and Wildfire Advice Prevents Coverage Gaps

Washington’s specific risks demand knowledge most homeowners lack. Eastern Washington faces intense hail exposure that drives certain carriers to charge premiums 20 to 30 percent higher than western regions, yet many homeowners don’t know this variation exists until quotes arrive. Coastal properties near the Cascadia Subduction Zone need earthquake endorsements, which aren’t included in standard policies and require separate underwriting. Western Washington’s wildfires mean some carriers restrict coverage in fire-prone ZIP codes or exclude wildfire damage unless you add specific endorsements. A local agent knows which carriers maintain appetite in your specific area, which ones have tightened underwriting, and which offer the most comprehensive wildfire or earthquake protection at reasonable rates. This knowledge prevents you from spending hours receiving quotes only to discover the best price comes from a carrier that doesn’t cover your actual risks, or worse, from learning after a loss that a critical exclusion leaves you underprotected.

Claims Support When Disasters Strike

Your relationship with an agent becomes invaluable the moment you file a claim. When a windstorm damages your roof or a water backup floods your basement, you’re stressed and need someone advocating on your behalf immediately. An independent agent files claims alongside you, helps you gather required documentation, and follows up with the carrier to ensure timely processing. An agent familiar with your specific insurer’s claims process knows which adjusters work fastest, which documentation prevents delays, and whether your carrier typically settles quickly or requires additional evidence. After your claim closes, that same agent reviews your policy to identify gaps exposed by the loss and recommends coverage adjustments before renewal, ensuring similar losses don’t leave you underprotected next time.

Ongoing Policy Reviews Adapt to Your Changing Needs

Life changes demand policy adjustments that most homeowners miss on their own. You complete a kitchen renovation, add a deck, or install a new roof-each improvement affects your replacement cost and may qualify you for premium discounts. An agent tracks these changes and recommends coverage updates before renewal, preventing you from paying for outdated limits or missing discounts you’ve earned. Home values in Washington continue to climb, which means your coverage limits need periodic review to stay aligned with actual replacement costs. An agent handles this monitoring automatically, alerting you when inflation or local construction cost increases suggest higher dwelling limits, rather than leaving you to notice the gap years later during a claim.

Final Thoughts

Accurate Washington homeowners insurance quotes require preparation, comparison, and guidance tailored to your specific property. Understanding what drives your rates-replacement cost, location risk, and home characteristics-forms the foundation, and requesting quotes from multiple carriers reveals how different insurers price your risk. This comparison process identifies which carrier fills the coverage gaps you actually need, whether earthquake protection near the Cascadia Subduction Zone or wildfire endorsements in fire-prone areas.

An independent agent transforms this process by shopping multiple carriers simultaneously, presenting genuinely competitive options, and explaining which exclusions matter for your situation. When disaster strikes, that agent becomes your advocate-filing claims alongside you, gathering documentation, and ensuring your carrier processes your loss fairly and quickly. Your policy adapts as your home appreciates, as you complete renovations, or as local construction costs climb, and an agent monitors these changes to recommend adjustments before renewal.

We at Secord Agency – A Trucordia Business understand Washington homeowners’ specific risks and coverage needs. Contact us today to receive competitive Washington homeowners insurance quotes from multiple carriers, paired with personalized advice based on your property’s actual risk profile and your family’s protection priorities.