Seattle auto insurance options: Finding The Best Rate In The Emerald City

Seattle auto insurance options vary widely, and finding the right rate requires understanding what drives your premiums. At Secord Agency – A Trucordia Business, we help drivers navigate local factors that impact their costs.

This guide walks you through the key elements affecting your rates, how to compare providers, and practical steps to secure the best coverage for your situation.

What Really Drives Your Seattle Auto Insurance Costs

Location Shapes Your Rate More Than You Realize

Your Seattle neighborhood determines a significant portion of your premium before any other factor enters the calculation. Drivers in ZIP code 98118 pay around $3,340 annually for full coverage, while those in 98115 pay $2,788, according to NerdWallet’s analysis using Quadrant Information Services data. The difference stems from local accident frequency, traffic density, and theft rates in your specific area. This geographic variation means two drivers with identical records, vehicles, and ages can face vastly different quotes simply based on where they park at night. Shopping around becomes essential because rates shift dramatically across Seattle’s neighborhoods.

Your Driving Record Controls Your Future Costs

Your driving record represents a major factor in how insurers calculate your premium. Insurers set your auto premiums by starting with the base rate and adjusting it based on factors specific to you and your policy. A clean five-year record qualifies you for accident-free discounts that reduce premiums by up to 10 percent. One at-fault accident changes everything-drivers with a single accident on record see quotes ranging from $1,902 with Kemper to $4,060 with National General. A DUI creates far steeper consequences; the same driver profile shows rates jumping to $2,088 with Progressive and $4,285 with Allstate. Even a speeding ticket adds $200 to $800 annually depending on your insurer. These numbers demonstrate why maintaining a clean record matters more than any other action you take.

Vehicle Choice and Age Impact Your Premium Directly

The car you drive affects cost immediately. Newer vehicles with advanced safety features and expensive repair components cost more to insure, while older paid-off vehicles let you drop collision coverage entirely if you have emergency savings. The 2023 Toyota Camry LE baseline used in rate comparisons reflects how insurers price common vehicles, but luxury sedans, sports cars, and trucks carry higher premiums. Your vehicle’s repair costs, safety ratings, and theft likelihood all factor into what carriers charge you each month.

Personal Factors Beyond Your Control Still Matter

Age, credit history, and annual mileage shape your rates significantly. A 20-year-old in Seattle averages $6,108 annually versus $2,897 for a 35-year-old with identical coverage. Poor credit bumps rates up across every carrier; Kemper charges $1,357 for good credit but $2,409 for poor credit on the same profile. If you drive under 3,000 miles yearly, pay-per-mile plans like Metromile can cost around $60 monthly, making mileage-based insurance worth comparing against standard unlimited plans. These factors operate independently of your driving behavior, yet they substantially affect what you pay.

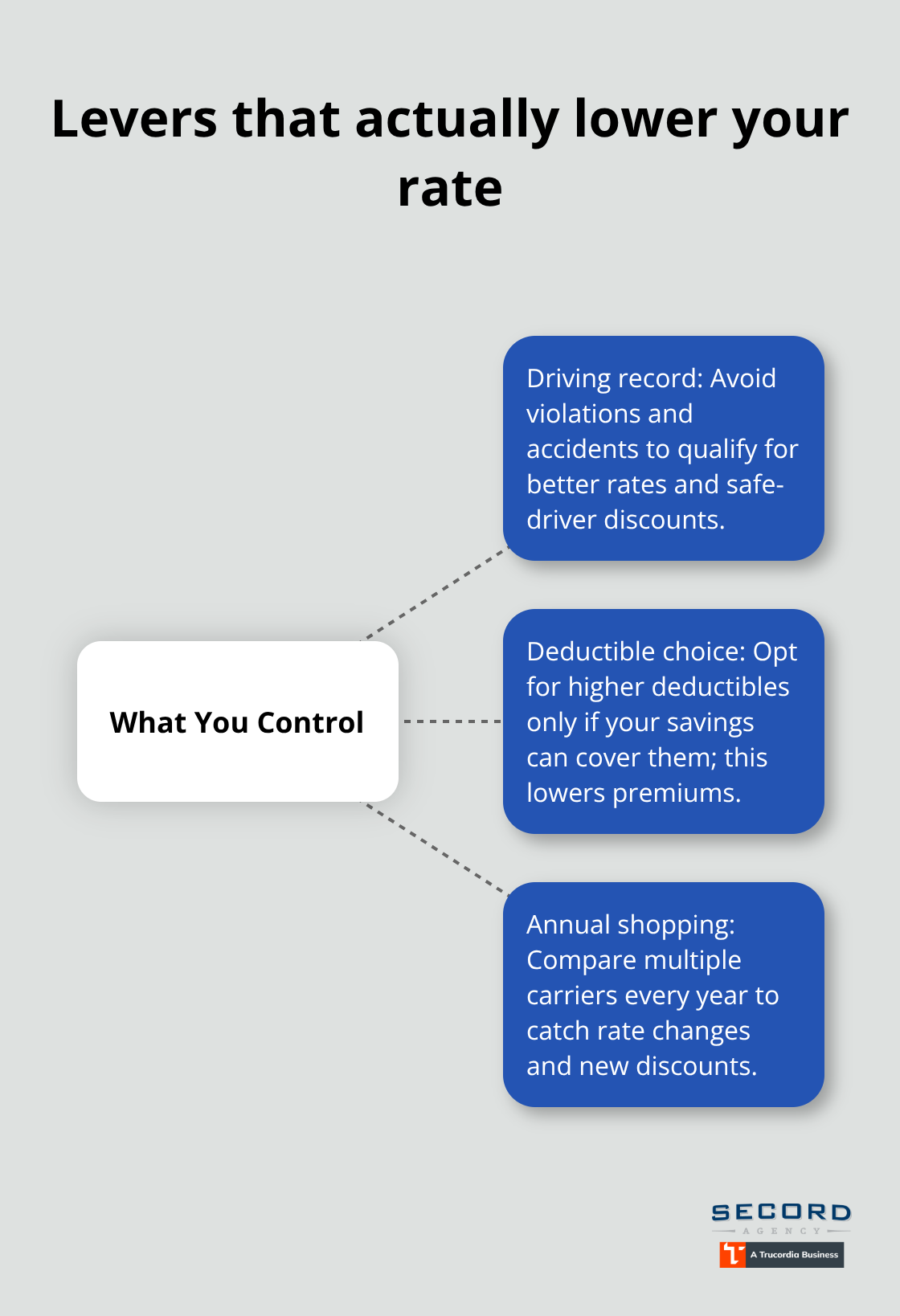

Focus Your Energy on What You Control

Weather and seasonal risks in Seattle matter less than you’d think-rates don’t spike seasonally the way they do in states with extreme winters. Instead, concentrate on the elements within your power: your driving record, your deductible choice, and your annual shopping habits. Raising your deductible lowers your premium, but only if you have enough savings to cover the higher amount when a claim occurs. Shopping multiple carriers annually reveals rate changes and new discounts you may qualify for.

These actions produce measurable savings, while worrying about Seattle traffic or weather you cannot change wastes your attention. Understanding these cost drivers positions you to make smarter decisions when comparing coverage options and selecting the right policy for your needs.

Which Carriers Actually Deliver Value in Seattle

National Carriers Optimize for Volume, Not Your Situation

National carriers dominate Seattle’s insurance market, but their size creates a fundamental problem: they optimize for volume over individual outcomes. Geico, Progressive, and State Farm process millions of policies nationwide using standardized algorithms, which means your Seattle-specific risks get filtered through national pricing models that miss local nuances. Kemper charges the lowest rates in Seattle for a 35-year-old with good credit at $1,357 annually, followed by Travelers at $1,556 and CIG at $1,658 according to NerdWallet’s analysis. However, cheapest doesn’t equal best when claims processing delays or poor customer service cost you weeks of frustration. USAA offers $1,421 annually for military families, but eligibility restrictions lock out most Seattle drivers entirely. Progressive ($1,861) and Geico ($1,959) fall in the mid-range for clean records, yet both show rate increases after policy adjustments or renewals that catch drivers off guard.

Independent Agencies Shop Multiple Carriers Simultaneously

Independent agencies operate differently because they aren’t bound to a single carrier’s playbook. They shop multiple carriers simultaneously, comparing real quotes across different underwriters rather than presenting you with one company’s take-it-or-leave-it offer. This approach matters when your circumstances don’t fit standard profiles-multiple accidents, poor credit, or unusual mileage patterns. Coverage flexibility becomes critical here: national carriers offer boilerplate policies designed for average drivers, while independent agencies can negotiate specific deductible combinations, higher liability limits, and bundling arrangements that actually fit your household.

Claims Advocacy Makes a Real Difference

When you need to file a claim, independent agencies advocate directly with carriers on your behalf instead of routing you through automated phone systems. Quick settlements prevent disputes over coverage interpretation and allow carriers to manage outgoing funds effectively. Local agencies understand Seattle’s specific claim patterns and carrier preferences, which translates to faster resolution and fewer complications throughout the process.

Annual Shopping Reveals Hidden Rate Gaps

Shopping around annually isn’t optional in Seattle because rates shift unpredictably. Drivers who stayed loyal to one carrier reported paying 20-50% more than competitors offering identical coverage. Comparing quotes from different carriers reveals these gaps immediately. The Washington Department of Insurance requires insurers to explain any premium changes, but most drivers never request this explanation. You have leverage here: call your current insurer, ask why your rate changed, and tell them you’re comparing alternatives. This simple action often triggers retention discounts or policy adjustments that lower your cost without switching companies. These rate variations mean your next best option could save you hundreds annually-a gap that widens every year you delay comparison shopping.

Getting the Right Rate Without Wasting Hours

Collect Quotes That Actually Compare

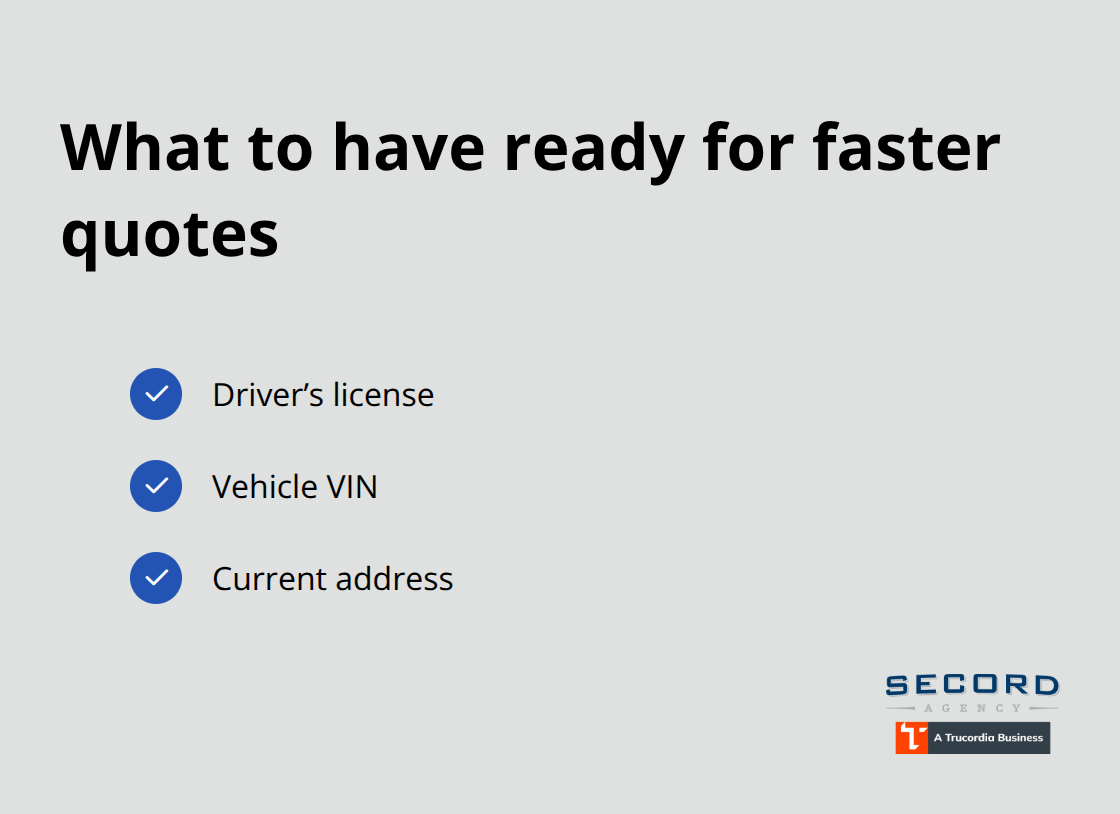

Gathering five to ten quotes from different carriers takes about two hours and reveals price gaps that often exceed $1,000 annually. Start with online quote tools from Geico, Progressive, and USAA if you’re military-eligible, then add regional carriers like Kemper and Travelers. Have your driver’s license, vehicle VIN, and current address ready so the process moves quickly.

The critical step most drivers skip: ensure every quote includes identical coverage limits and deductibles across all carriers. Comparing a $500 deductible collision policy against a $1,000 deductible policy produces meaningless numbers. Set your target coverage first-Washington requires $25,000 bodily injury per person, $50,000 per accident, and $10,000 property damage minimum, but consider higher limits if you have assets to protect-then lock those specifications while requesting quotes.

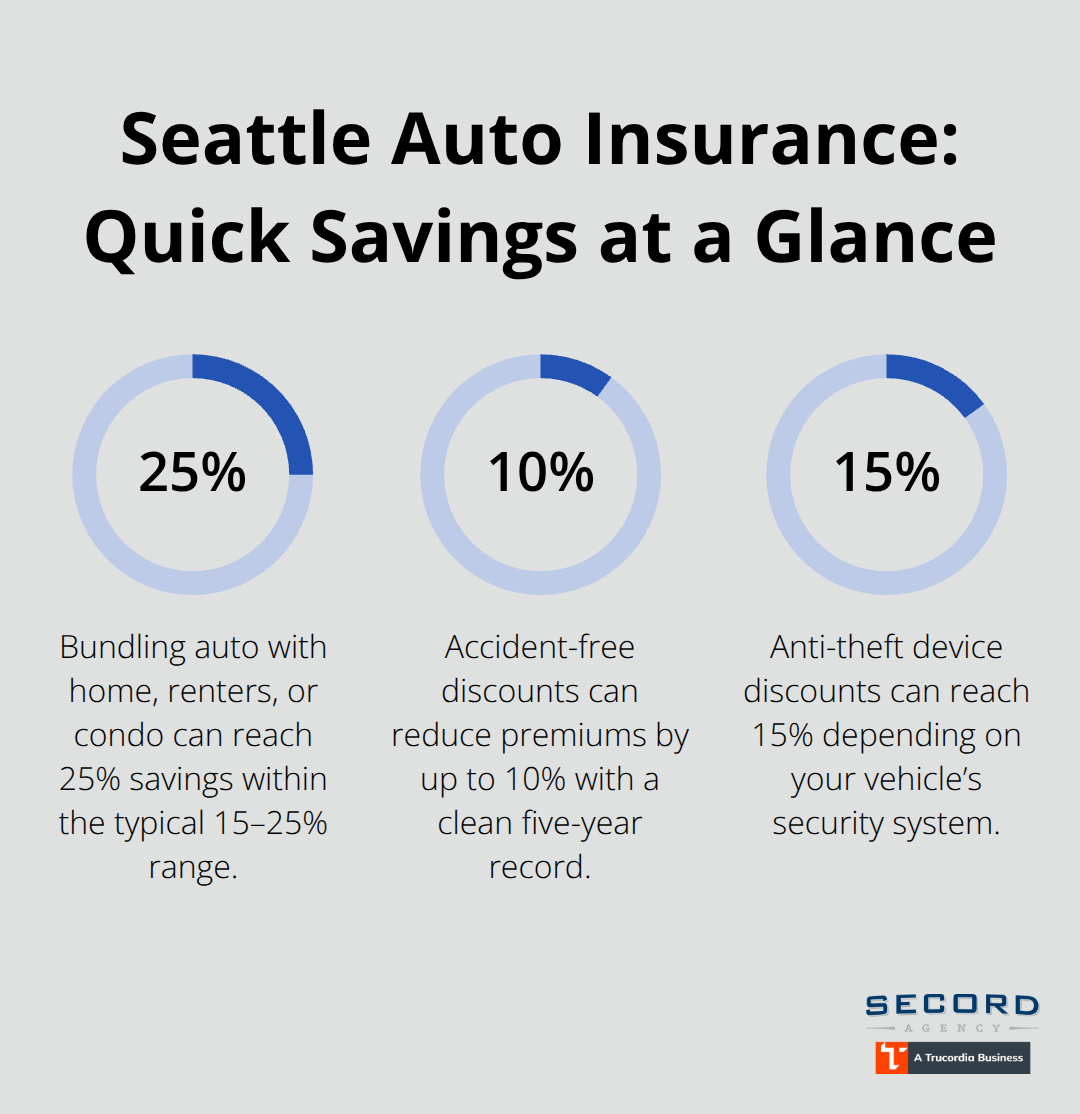

After collecting quotes, rank them by total premium and cross-reference complaint data through the Washington Department of Insurance before selecting your top three options. Call each carrier and ask directly: what discounts do I qualify for? Safe driver discounts reward five years accident-free driving, good student discounts apply to drivers aged 16–24 with B averages or better, and defensive driving discounts benefit drivers 55 and older who complete state-approved courses. Anti-theft device discounts range from 5–15 percent depending on your vehicle’s security system. These discounts often don’t appear in online quotes, so verbal requests unlock savings that reduce your final cost substantially.

Leverage Your Current Insurer’s Retention Department

If your current insurer’s rate increased, call and tell them you’re shopping alternatives. Retention departments frequently offer discounts or policy adjustments to keep your business, sometimes matching or beating competitor quotes without requiring you to switch. This single tactic often produces immediate savings without the hassle of switching carriers.

Stack Discounts Through Bundling

Bundling auto insurance with home, renters, or condo coverage typically saves 15–25 percent on your auto premium, making it worth evaluating even if you’re satisfied with your current homeowners policy. If you own multiple vehicles, insuring them all under one policy further reduces per-vehicle costs. Conduct a full household insurance review annually because life changes-marriage, home purchase, vehicle replacement, or relocation within Seattle-create opportunities to restructure coverage and eliminate overlapping protection that wastes money.

Schedule this review each year around your policy renewal date rather than waiting for a rate increase to force action.

Adjust Deductibles to Match Your Financial Reality

During your annual review, assess whether your deductibles still align with your emergency savings. If you’ve built additional reserves, raising your collision and comprehensive deductibles from $500 to $1,000 or $1,500 lowers premiums without creating financial risk. For vehicles worth less than $5,000, collision and comprehensive coverage often costs more annually than the vehicle’s replacement value, making these coverages unnecessary if you can absorb the loss. Conversely, maintaining higher liability limits-$100,000 per person and $300,000 per accident instead of state minimums-protects your income and assets if you cause a serious accident (a protection that costs only $15–30 monthly but prevents catastrophic financial exposure).

Shop Annually to Stay Competitive

Annual shopping reveals whether your current carrier remains competitive or whether a switch saves hundreds. Drivers who shop annually report average savings of $200–400 per year compared to those who stay with one insurer for five years without comparison shopping. Rate variations mean your next best option could save you hundreds annually-a gap that widens every year you delay comparison shopping.

Final Thoughts

Seattle auto insurance options require active management, not passive acceptance of whatever rate your current carrier quotes. Location determines baseline pricing, your driving history controls future adjustments, and annual shopping habits reveal whether you overpay compared to available alternatives. These elements combine to create rate variations exceeding $1,500 annually for identical coverage, making comparison shopping a financial necessity rather than an optional task.

We at Secord Agency – A Trucordia Business operate differently than national carriers because we shop multiple underwriters simultaneously on your behalf. Rather than presenting you with one company’s standard offer, we compare real quotes across different carriers and negotiate coverage combinations tailored to your specific situation. When claims arise, local advocacy means direct communication with carriers instead of automated phone systems, translating to faster resolution and fewer disputes over coverage interpretation.

Start by contacting Secord Agency – A Trucordia Business for a personalized quote that compares multiple carriers at once. We handle the comparison work so you don’t have to, delivering competitive rates paired with local service that actually advocates for you when you need it most. Your next step takes just one phone call to access Seattle auto insurance options that fit your household instead of forcing you into generic templates designed for average drivers nationwide.