Contractor insurance quotes WA: How Homeowners Policies Protect Your Projects

Hiring contractors for home projects in Washington comes with real financial risk. Without proper insurance protection, you could face thousands in liability claims or property damage costs.

At Secord Agency – A Trucordia Business, we help homeowners navigate contractor insurance quotes in WA to find coverage that actually protects their investments. This guide walks you through what you need to know before your next project starts.

What Contractor Insurance Actually Protects

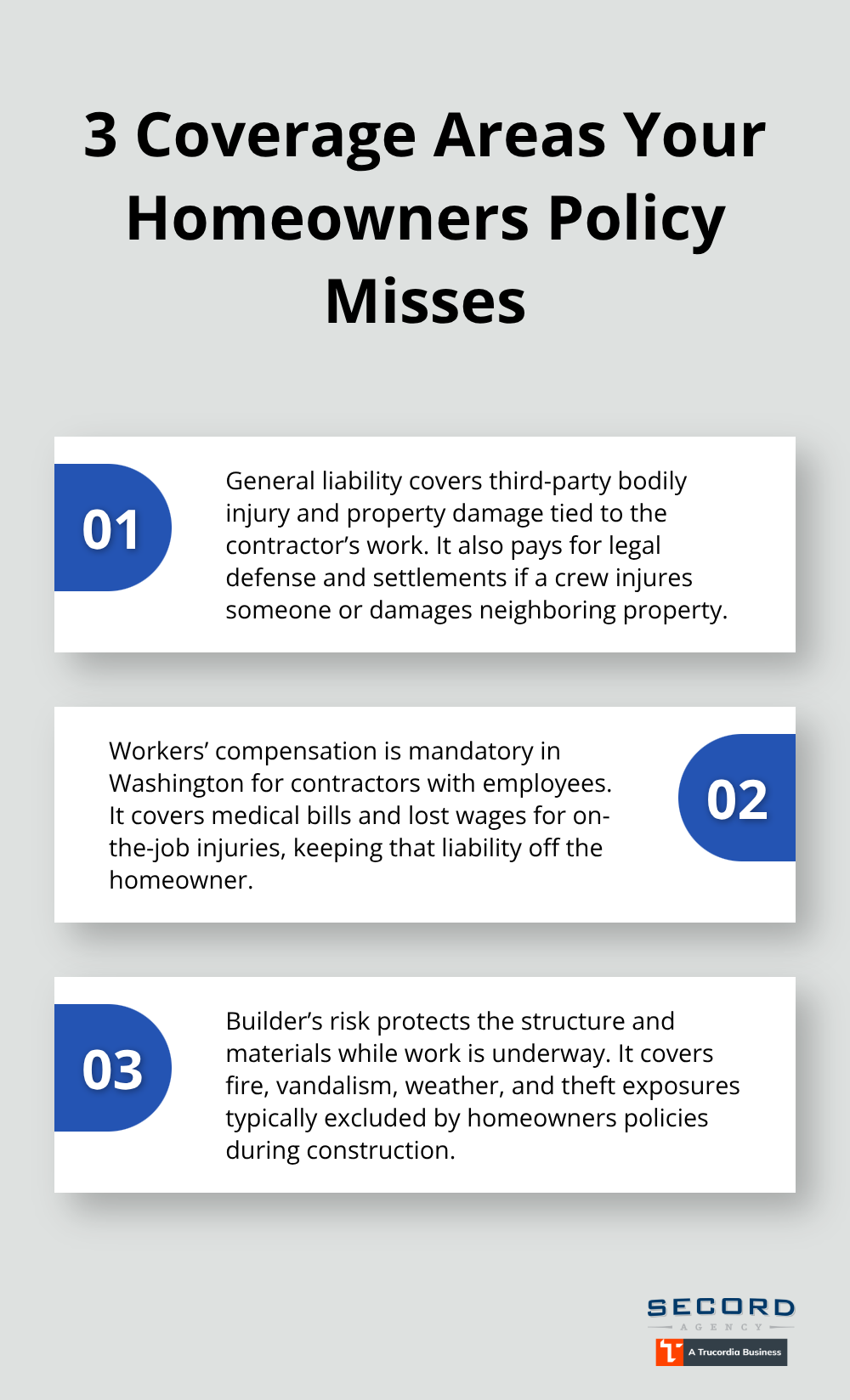

Three Coverage Areas Your Homeowners Policy Misses

Contractor insurance in Washington covers three critical areas that your homeowners policy does not. General liability protects you from third-party bodily injury and property damage claims-if a contractor’s crew damages your neighbor’s fence or a worker gets injured on your property, this coverage handles legal defense and settlement costs. Workers’ compensation is mandatory for contractors with employees in Washington and covers medical expenses and lost wages if someone gets hurt on the job, which keeps liability away from you as the homeowner. Builder’s risk insurance covers the structure itself and materials during construction, protecting against fire, vandalism, and weather damage that standard homeowners policies exclude while work is underway.

Why Your Homeowners Policy Falls Short

Your homeowners policy has significant gaps when contractors are on site. Most homeowners policies suspend or limit coverage once active construction begins, leaving you exposed during the exact period when risk is highest. Washington requires all contractors to carry a minimum of $250,000 in general liability coverage filed with the Department of Labor & Industries, but this is just the baseline-many projects demand higher limits. If a contractor lacks adequate coverage or lets their policy lapse, you become the financial target for any accident or damage claim.

The Additional Insured Endorsement and Completed Operations

The contractor’s certificate of insurance must list you as an additional insured, which extends their coverage to protect you from claims arising from their work. Without this endorsement, you could face out-of-pocket costs even though the contractor was responsible. Completed operations coverage is another critical gap-standard homeowners policies won’t cover defects that emerge weeks or months after the job finishes, like a roof leak from improper installation. Contractors carry this coverage to protect against post-completion claims, but only if their policy explicitly includes it.

Coverage Limits and Verification Steps

Property damage coverage limits matter significantly; the state minimum is either $200,000 public liability and $50,000 property damage or $250,000 combined single limit, according to Washington’s L&I requirements. If your project involves high-value materials or equipment, the contractor’s standard limits may not be enough. Before work starts, request a current certificate of insurance and verify the contractor’s registration status using the L&I verification tool-this confirms their bond is active and coverage is in force, not expired or fraudulent. These verification steps protect you from hiring uninsured or underinsured contractors who could leave you liable for project accidents.

Getting Accurate Contractor Insurance Quotes in Washington

How Project Risk Shapes Your Quote

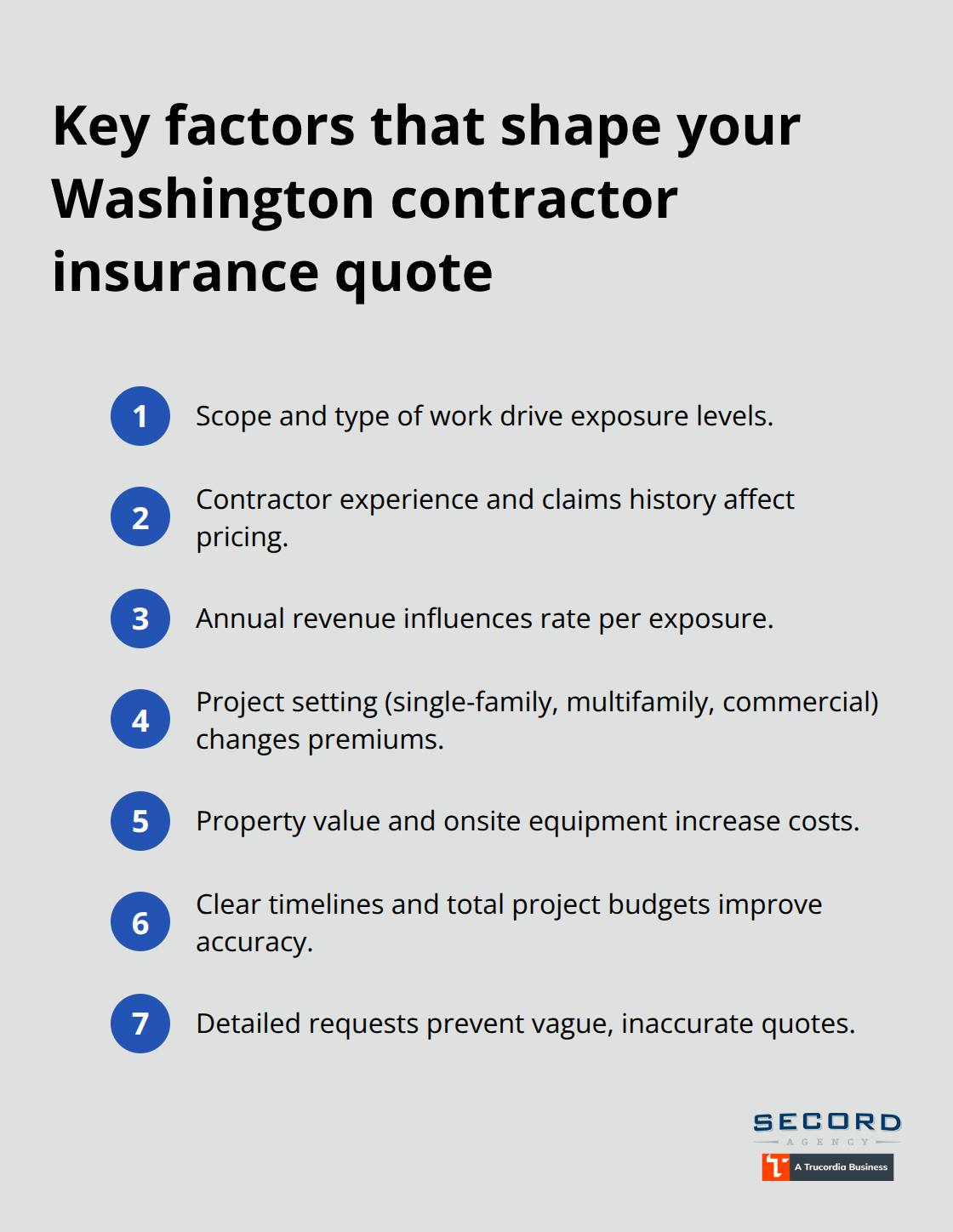

Contractor insurance quotes in Washington vary dramatically based on the specific work being performed and your project’s risk profile. General liability premiums average around $129 per month in Washington, but roofing contractors pay significantly more per dollar of revenue than flooring specialists due to fall hazards and injury risks. The contractor’s years of experience, annual revenue, and claims history all factor into pricing-a contractor with five years of clean history pays less than someone just starting out. Your project type matters equally; renovating a single-family home costs less to insure than a multifamily residential project, and commercial work demands even higher premiums.

Property value and equipment on site also increase quotes, since higher-value projects represent greater financial exposure. When you request quotes, provide detailed scope information about what’s being built or repaired, the timeline, and the total project cost. Vague requests produce vague quotes that won’t reflect your actual risk.

Shopping Multiple Carriers Reveals Real Price Differences

Comparing quotes from multiple carriers reveals significant pricing gaps that justify the effort of shopping around. Contact at least three insurers and request quotes on identical terms so you can see apples-to-apples pricing. Licensed Washington agents can bind coverage within 24 to 48 hours once you apply, so speed isn’t an excuse to accept the first quote.

Red Flags That Signal Coverage Problems

Red flags during quote review include certificates of insurance that look altered or mismatched with the carrier’s records. Contact the insurance company directly to verify the policy actually exists and matches what the contractor showed you, since fraudulent COIs circulate regularly. Quotes that seem unusually cheap compared to competitors warrant skepticism; contractors operating with inadequate coverage create hidden liability for you.

Verify the certificate lists you as an additional insured and includes completed operations coverage. If the COI omits either, the contractor’s policy won’t protect you from post-completion defects. Washington’s L&I verification tool confirms whether a contractor’s registration and bond are current, so cross-reference every quote against the L&I database before proceeding. Missing or lapsed coverage disqualifies a contractor regardless of price, since uninsured work violates state law and leaves your property and finances exposed to claims.

With quotes vetted and coverage verified, the next step involves understanding how your homeowners policy interacts with the contractor’s insurance during active construction.

How Your Homeowners Policy and Contractor Coverage Work Together

The Separate Coverage Lanes During Construction

Your homeowners policy and the contractor’s insurance operate in separate lanes during construction, and understanding this division prevents costly gaps. When a contractor actively works on your property, your homeowners policy typically suspends or severely limits coverage on the area under construction. Insurers intentionally shift liability to the contractor’s general liability policy, which carries a minimum of $250,000 in coverage under Washington’s L&I requirements. The contractor’s policy protects you from third-party claims if their crew injures someone or damages neighboring property. This protection only works if the contractor’s certificate of insurance lists you as an additional insured. Without this endorsement, you remain personally liable for accidents on your property even though the contractor caused them. Request the certificate before work starts and verify it includes additional insured status. If it doesn’t, ask the contractor’s insurance agent to add you immediately-this takes minutes and costs nothing.

Builder’s Risk Covers What Your Homeowners Policy Won’t

Property damage during construction requires a different approach than liability protection. Your homeowners policy will not cover damage to materials, equipment, or the structure itself while work takes place. Builder’s risk insurance fills this gap, and it’s not optional for significant projects. Builder’s risk covers fire, vandalism, weather damage, and theft of materials and equipment on site-exposures that leave homeowners financially vulnerable without it. Washington contractors typically carry this coverage for commercial projects but often skip it on residential work, creating a dangerous assumption that your homeowners policy will step in. It won’t. For renovation projects exceeding $25,000, insist that the contractor either obtain builder’s risk or that you purchase it separately. The cost runs roughly $400 to $800 for a three-month residential project, far less than replacing stolen copper pipes or materials destroyed by fire.

Completed Operations Coverage Protects Against Post-Project Defects

Completed operations coverage protects you from defects that emerge after the contractor leaves, and this protection is widely misunderstood. A roof installed incorrectly may leak months later, or electrical work may cause problems a year down the line. Standard homeowners policies exclude these post-completion failures because they occurred during the contractor’s work. The contractor’s policy must explicitly include completed operations coverage, typically extending one to three years after project completion. Verify this coverage exists on the certificate of insurance before signing any contract. This endorsement shifts responsibility back to the contractor if their work fails after they finish, protecting your investment long after the job site closes.

Final Thoughts

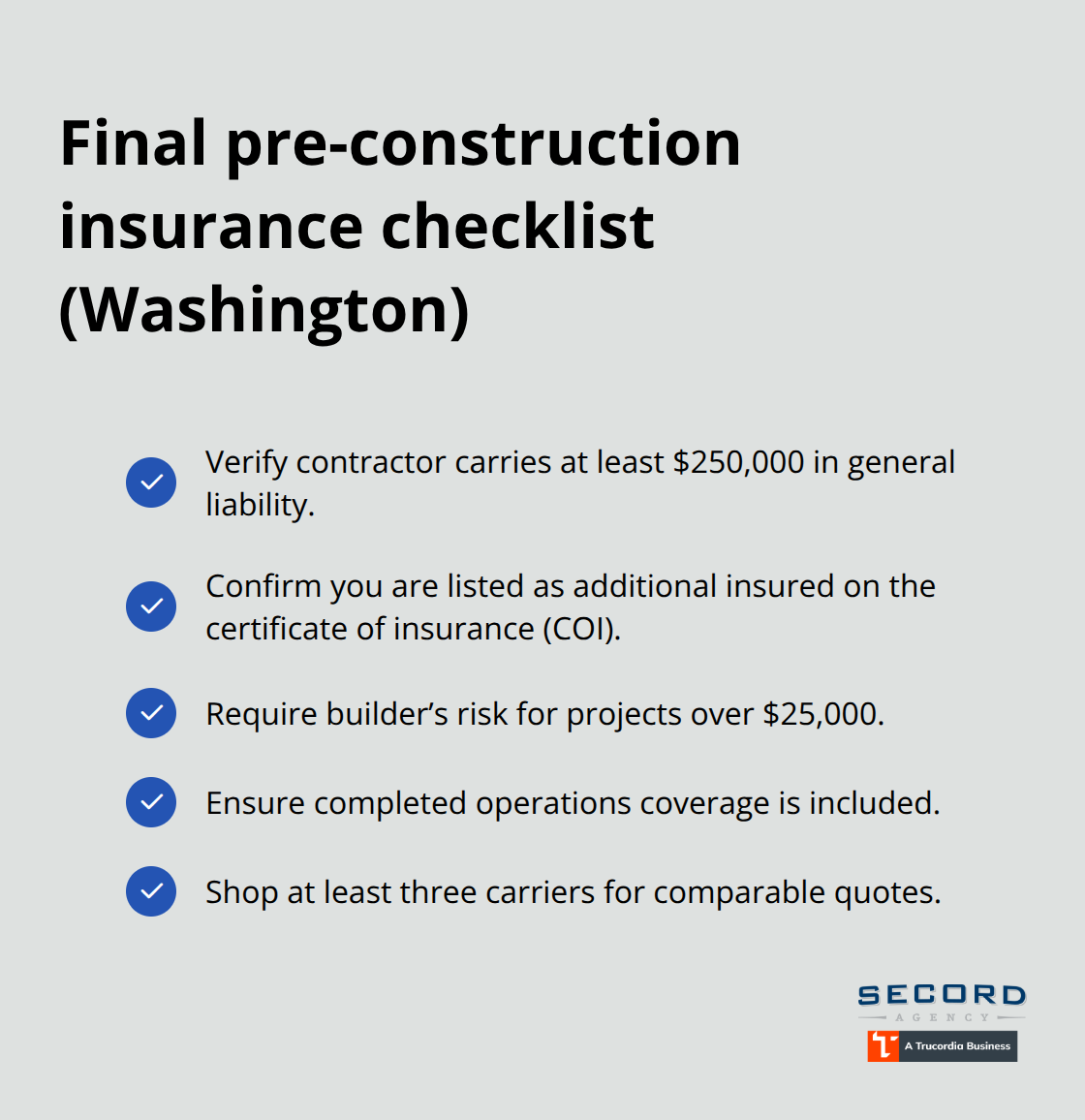

Protecting your construction project in Washington requires three concrete actions: verify your contractor carries a minimum of $250,000 in general liability coverage, confirm you’re listed as an additional insured on their certificate of insurance, and request builder’s risk coverage for any project exceeding $25,000. Your homeowners policy will not protect you during active construction, which is why contractor insurance quotes in WA demand careful attention before work begins. The contractor’s coverage must include completed operations protection to guard against defects that emerge months after the job finishes.

Shopping multiple carriers for contractor insurance quotes reveals real price differences that justify the effort. Licensed agents can bind coverage within 24 to 48 hours, and comparing at least three quotes on identical terms shows you the true cost range for your specific project. General liability premiums vary significantly based on project type, contractor experience, and property value, so accepting the first quote often means overpaying for protection.

We at Secord Agency – A Trucordia Business understand Washington’s contractor insurance landscape and help homeowners find coverage that actually protects their investments. Our team shops multiple carriers to deliver competitive rates paired with personalized advice on policy limits, additional insured endorsements, and builder’s risk options tailored to your specific project. Contact us for a quote and let our local expertise guide you toward the right coverage before your next project starts.