Personal Umbrella Policy WA: How Much Protection Do You Need

Your homeowners and auto insurance policies have limits. Once you exceed those limits, you’re personally liable for the rest-and that can mean losing assets you’ve spent years building.

A personal umbrella policy in WA bridges that gap by providing additional liability coverage when accidents happen. We at Secord Agency – A Trucordia Business help Washington residents figure out exactly how much protection they actually need, based on their specific situation and what they own.

How Umbrella Policies Protect Your Assets

When Your Standard Policies Fall Short

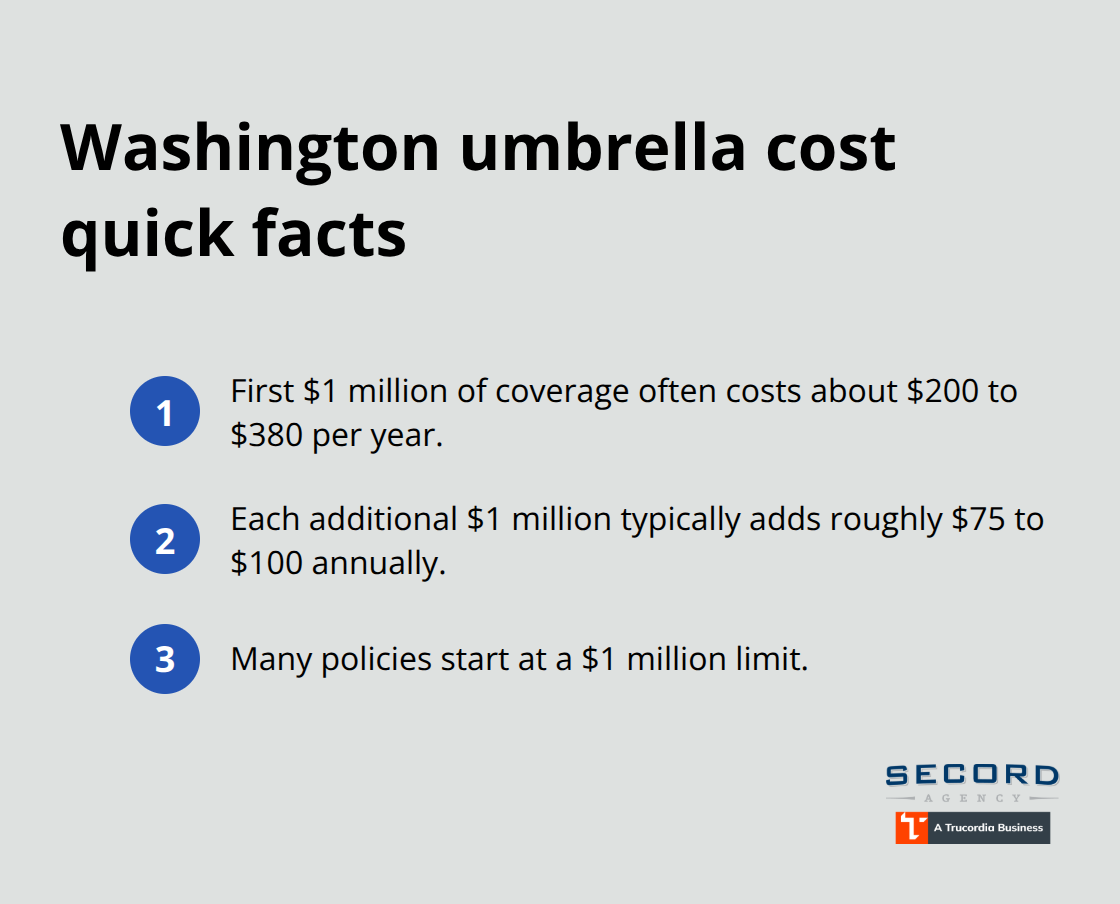

Umbrella insurance activates only after your homeowners and auto policies reach their liability limits. Consider a real scenario: a car accident results in $1.2 million in damages, and your auto policy covers $500,000. Your umbrella policy then covers the remaining $700,000 plus legal defense costs. This layered approach extends your existing coverage rather than replacing it. Most policies in Washington start at $1 million and cost about $200 to $380 annually for that first million, with each additional million adding roughly $75 to $100 per year. If your net worth exceeds $500,000, umbrella coverage becomes economically rational. A single serious accident can generate judgments far beyond standard policy limits, and Washington verdicts in significant injury cases routinely reach multi-million figures.

What Your Umbrella Actually Covers

Your umbrella covers what happens after underlying limits are exhausted across several liability scenarios. It protects you against third-party bodily injury claims, property damage liability, and personal injury claims including defamation, false arrest, and malicious prosecution. If a guest is injured at your home, a dog bite occurs, or someone is hurt in a pool accident you’re responsible for, your umbrella fills the gap once your homeowners policy limit is reached. The same applies to vehicle incidents-if you’re liable for injuries in a multi-car crash, the umbrella activates after your auto policy pays out. Defense costs alone can run into hundreds of thousands of dollars in serious cases.

What Umbrella Insurance Excludes

Your umbrella does not cover your own medical bills, damage to your property, intentional criminal acts, or business liabilities unless you purchase a separate commercial umbrella. Understanding these exclusions prevents surprises when you file a claim. If you own a business or operate from home, you may need additional coverage beyond a standard personal umbrella.

Qualifying for Umbrella Coverage in Washington

To qualify for umbrella coverage in Washington, you need underlying homeowners liability of at least $300,000 and auto bodily injury limits of at least $250,000 per person or $500,000 per accident. A lapse in either underlying policy voids your umbrella protection, so continuous coverage is essential. An independent agent can verify your current limits and recommend adjustments to qualify while keeping total costs reasonable.

Matching Coverage to Your Specific Risks

Your lifestyle and assets determine how much umbrella protection makes sense. High-risk activities like owning a pool, renting property, or driving a teenage driver increase your exposure significantly. The next section walks through specific scenarios where umbrella insurance steps in to protect you when accidents happen.

How Much Umbrella Coverage Fits Your Situation

Calculate Coverage Based on Your Net Worth

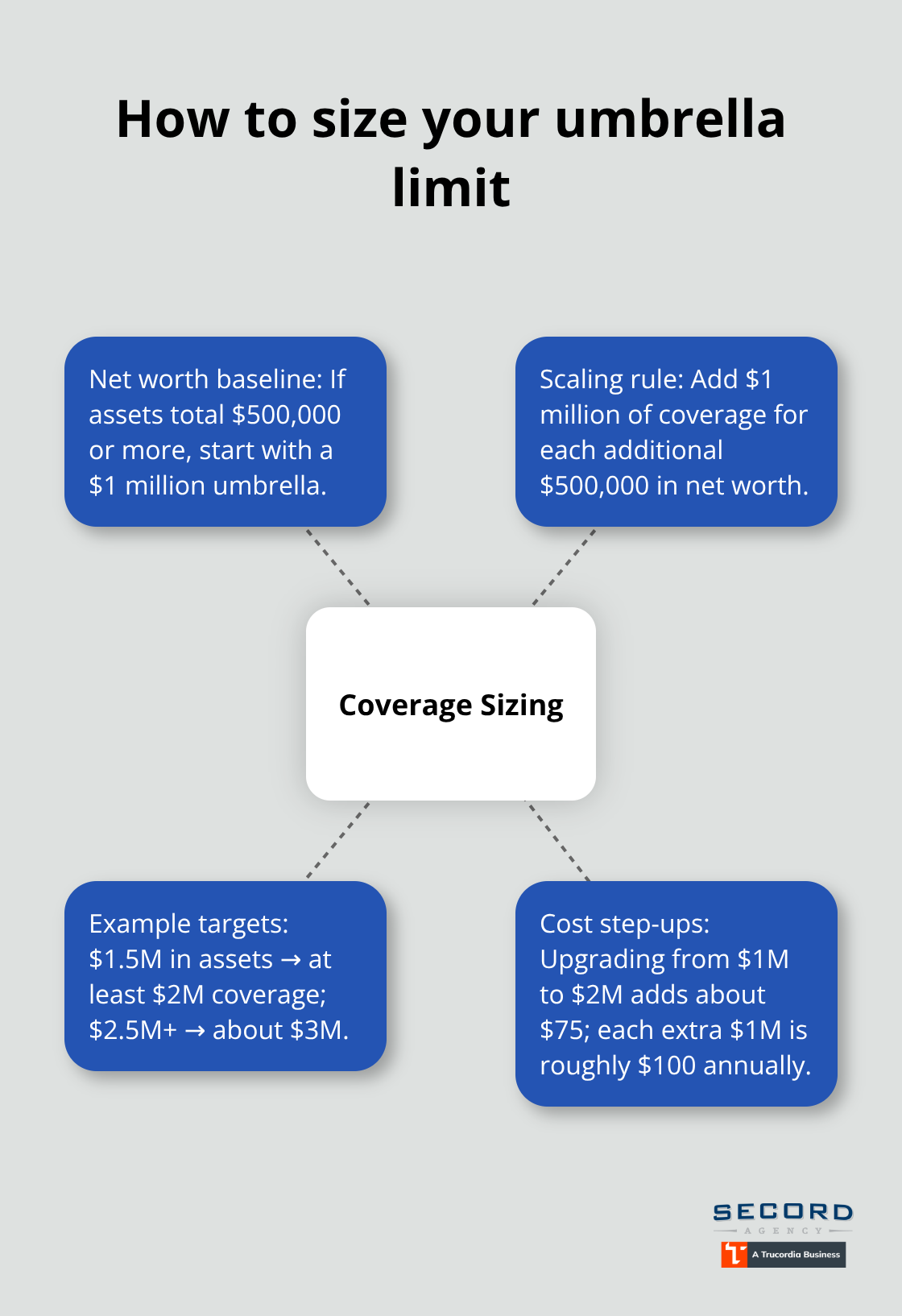

The right umbrella limit depends on three concrete factors: what you own, how you live, and what gaps exist in your current coverage. Start with your net worth. If your assets total $500,000 or more, a $1 million umbrella policy provides economically rational protection. For every $500,000 in additional net worth, add another $1 million in umbrella coverage. Someone with $1.5 million in assets should carry at least $2 million in umbrella protection; at $2.5 million or higher, a $3 million umbrella becomes practical. The incremental cost stays modest-upgrading from $1 million to $2 million typically adds about $75 per year, and each additional million beyond that costs roughly $100 annually. This means protecting significantly more assets costs only slightly more in premium dollars.

Identify Your Lifestyle and Activity Risks

Your lifestyle and activities drive exposure upward quickly. Owning a swimming pool, trampoline, or dog increases liability risk substantially because guest injuries or pet incidents can exceed standard homeowners limits. Rental property ownership multiplies exposure further; tenant injuries or property damage claims can easily surpass $500,000. Teen drivers in your household significantly raise accident risk-younger drivers statistically cause more accidents with higher injury severity. Hosting large gatherings, serving on nonprofit boards, or maintaining a visible social media presence increases lawsuit vulnerability. Real-world scenarios illustrate the stakes: dog bites average around $500,000 in damages, multi-car accidents reach $1 million or more, and serious guest injuries can approach $2 million.

Review Your Current Policy Limits and Gaps

Start by reviewing your current homeowners and auto declarations. Most homeowners policies cap liability at $300,000 to $500,000; auto policies typically max out around $500,000 per incident. A gap analysis is straightforward: subtract your underlying limits from your net worth, then round up to the nearest $1 million umbrella increment. An independent agent can verify your exact limits, calculate worst-case scenarios specific to your property and activities, and quote umbrella coverage across multiple carriers to find the lowest cost for your actual risk profile. This assessment reveals whether your current protection matches your exposure-and what umbrella limit actually makes financial sense for your situation.

Real Claims That Exceed Standard Coverage

Pet Incidents Create Substantial Liability Gaps

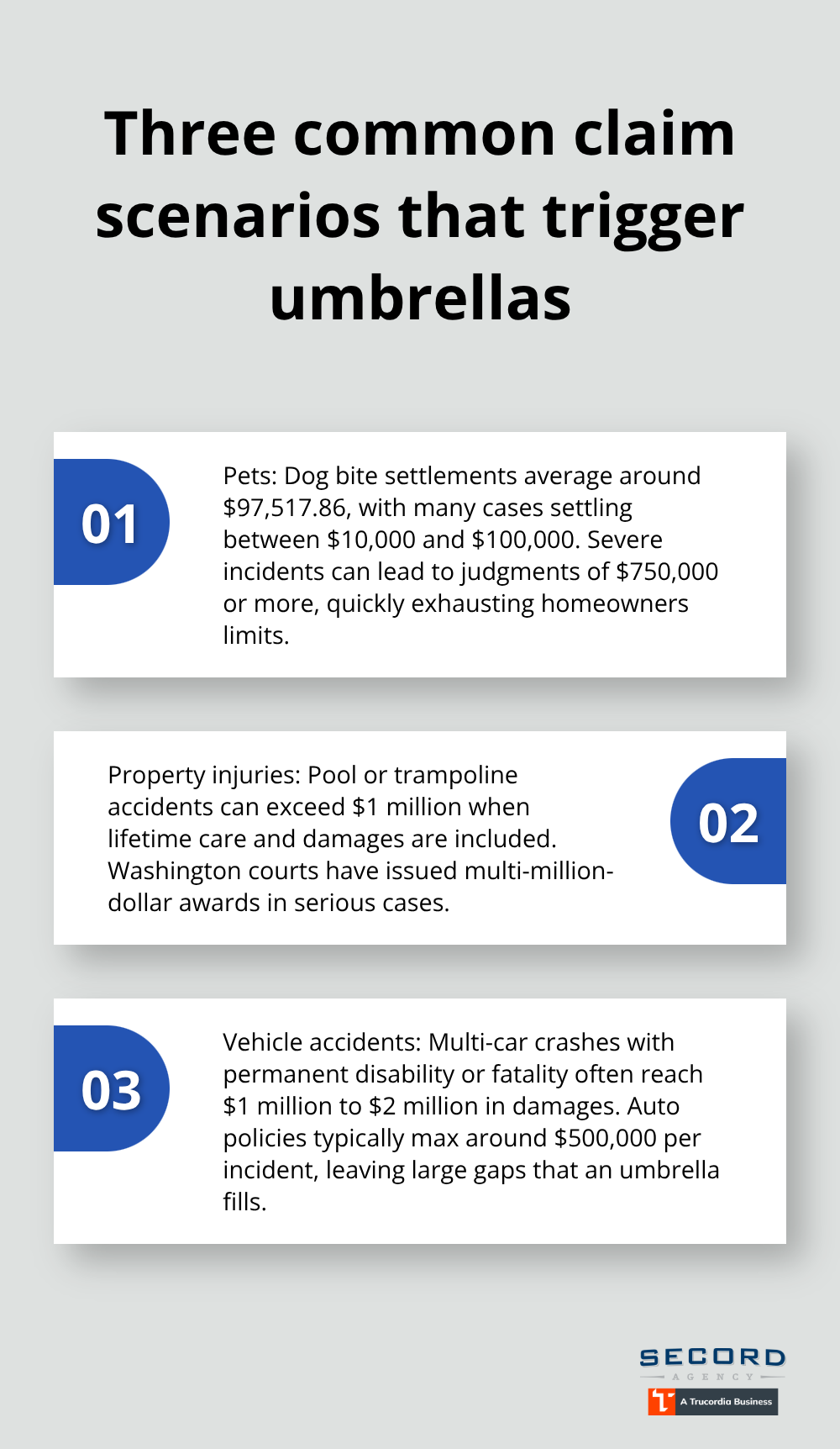

Pet incidents rank among the most common liability claims that drain standard homeowners policies fast. A dog bite settlement averages around $97,517.86 in damages, though cases often settle between $10,000 and $100,000 but can be higher. Your homeowners liability typically caps at $300,000 to $500,000, leaving a substantial gap once medical bills, lost wages, and legal fees accumulate. A single incident can generate judgments for $750,000 or more, especially if a child suffers permanent scarring or disfigurement.

Property-Based Guest Injuries Trigger Major Claims

Swimming pools and trampolines follow the same pattern-guest injuries at your property create liability exposure that standard limits rarely cover fully. A child who breaks their spine on your trampoline or suffers near-drowning complications at your pool can generate claims exceeding $1 million when you factor in lifetime medical care, physical therapy, and pain-and-suffering damages. Washington courts have awarded multi-million-dollar judgments in serious drowning and trampoline injury cases, making pool and trampoline ownership a direct trigger for umbrella coverage.

Vehicle Accidents Activate Umbrella Protection Most Often

Vehicle accidents represent the single most likely scenario to activate umbrella protection because injury severity in multi-car collisions drives damages upward rapidly. A crash involving permanent disability or fatality easily reaches $1 million to $2 million in total damages across medical expenses, lost earning capacity, and legal defense costs. Your auto policy maxes out around $500,000 per incident in most cases, leaving $500,000 to $1.5 million uncovered. Teen drivers multiply this risk substantially-drivers under 20 cause more accidents per mile driven than any other age group according to the National Highway Traffic Safety Administration, and their accidents often involve multiple vehicles and serious injuries. If you’re found liable for injuries to occupants in another vehicle, your umbrella activates immediately after your auto policy exhausts, protecting your savings and home equity from judgment.

Why Standard Policies Leave You Exposed

These three scenarios-pet incidents, property-based guest injuries, and vehicle liability-account for the majority of umbrella claims filed in Washington. Your net worth and current policy limits determine whether you need $1 million or $3 million in coverage, but the reality is that serious accidents happen far more often than most people expect. Standard policies leave gaps that umbrella insurance fills at a cost of just $200 to $380 per year (for the first million in coverage).

Final Thoughts

A personal umbrella policy in WA fills the gaps that homeowners and auto insurance leave behind. Your standard policies have limits, and serious accidents routinely exceed them. The scenarios we covered-pet incidents, pool injuries, and vehicle accidents-happen more often than you might think, and when they do, the financial consequences can be devastating without proper protection.

The right coverage amount depends on what you own and how you live. If your net worth exceeds $500,000, umbrella insurance becomes economically rational because the annual cost of $200 to $380 for the first million in coverage is modest compared to the assets you’re protecting. Someone with $1.5 million in assets should carry at least $2 million in umbrella protection; at $2.5 million or higher, a $3 million umbrella makes practical sense.

We at Secord Agency – A Trucordia Business help Washington residents match their umbrella coverage to their actual circumstances. An independent agent can review your current declarations, calculate worst-case liability scenarios specific to your property and activities, and quote coverage across multiple carriers to find the lowest cost for your risk profile. Contact us today to get a personalized quote and protect what you’ve built.