Cheap Auto Insurance Washington: How to Save Without Sacrificing Coverage

Finding cheap auto insurance in Washington doesn’t mean settling for inadequate protection. Most drivers overpay simply because they don’t know what factors insurers consider or which discounts apply to their situation.

We at Secord Agency – A Trucordia Business help Washington residents cut their premiums while maintaining solid coverage. This guide walks you through the rate factors you can’t control, the strategies that actually work, and the costly mistakes to avoid.

What Drives Your Washington Auto Insurance Rate

Your insurance rate isn’t random. Washington insurers measure specific factors to predict risk, and understanding which ones matters most helps you make smarter decisions about coverage and cost.

Driving History Sets the Foundation

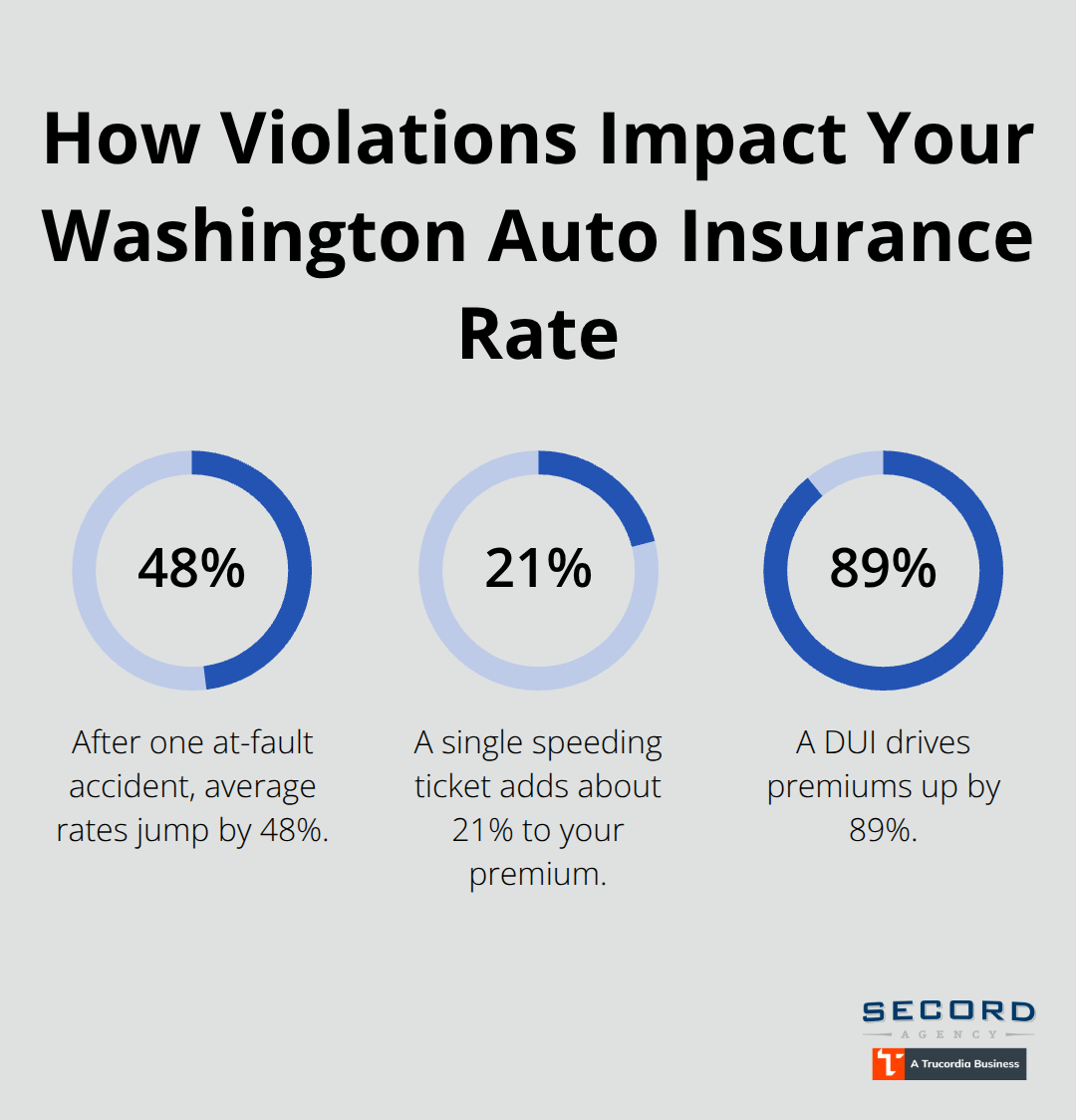

A clean driving record cuts your premium significantly. Drivers with no accidents average around $1,919 annually according to Bankrate data, while a single at-fault accident pushes rates up 48% higher. One speeding ticket adds roughly 21% to your costs, and a DUI increases premiums by 89%.

This means your past behavior on the road directly controls whether you pay $1,919 or substantially more. The good news: every year without an incident lowers your rate, so safe driving pays off immediately and compounds over time.

Vehicle Type Affects Your Premium as Much as Your Driving History

The car you drive shapes your premium significantly. A BMW 330i costs about $2,398 annually to insure in Washington, while a Honda Odyssey runs around $1,749 per year, according to Bankrate. Sports cars and luxury vehicles carry higher repair costs and theft risk, making insurers charge more. Before you buy any car, ask your insurer for estimated premiums on each model you’re considering-this step alone can save hundreds annually. Consumer Reports publishes accident and theft rates for every model, helping you spot cheaper-to-insure options before purchase. Safety features like anti-lock brakes, airbags, and anti-theft devices lower your premium, so prioritize these when comparing vehicles. Older vehicles with lower values might not need collision or comprehensive coverage, which can cut your bill significantly if you’re willing to accept higher out-of-pocket costs after a total loss.

Age, Location, and Credit History Shape Your Final Rate

Washington’s insurance costs vary dramatically by location and personal circumstances. Seattle drivers pay around $2,154 annually for full coverage, while Port Townsend averages $1,562-a difference of nearly $600 for identical coverage. Teen drivers face the steepest rates: a 16-year-old on a parent’s policy costs about $4,046 per year, while an 18-year-old on their own policy reaches $6,968 annually. Rates drop steadily as drivers age; a 55-year-old averages $124 monthly across carriers, and seniors aged 65–70 pay roughly $134 monthly. Credit history also affects your rate in Washington-poor credit raises costs by approximately 48%, while excellent credit reduces them by 13%, according to Bankrate. Male drivers under 30 historically pay more than females because accident data shows higher incident rates in that group. These factors combine to create your individual rate, which is why shopping multiple carriers is essential-USAA, Travelers, PEMCO, and Encompass often offer competitive pricing in Washington, but savings vary by profile.

Now that you understand what insurers charge for, the next section reveals which strategies actually lower your premiums without leaving you underprotected.

How to Cut Your Premium Without Dropping Coverage

Bundle Your Home and Auto Policies Strategically

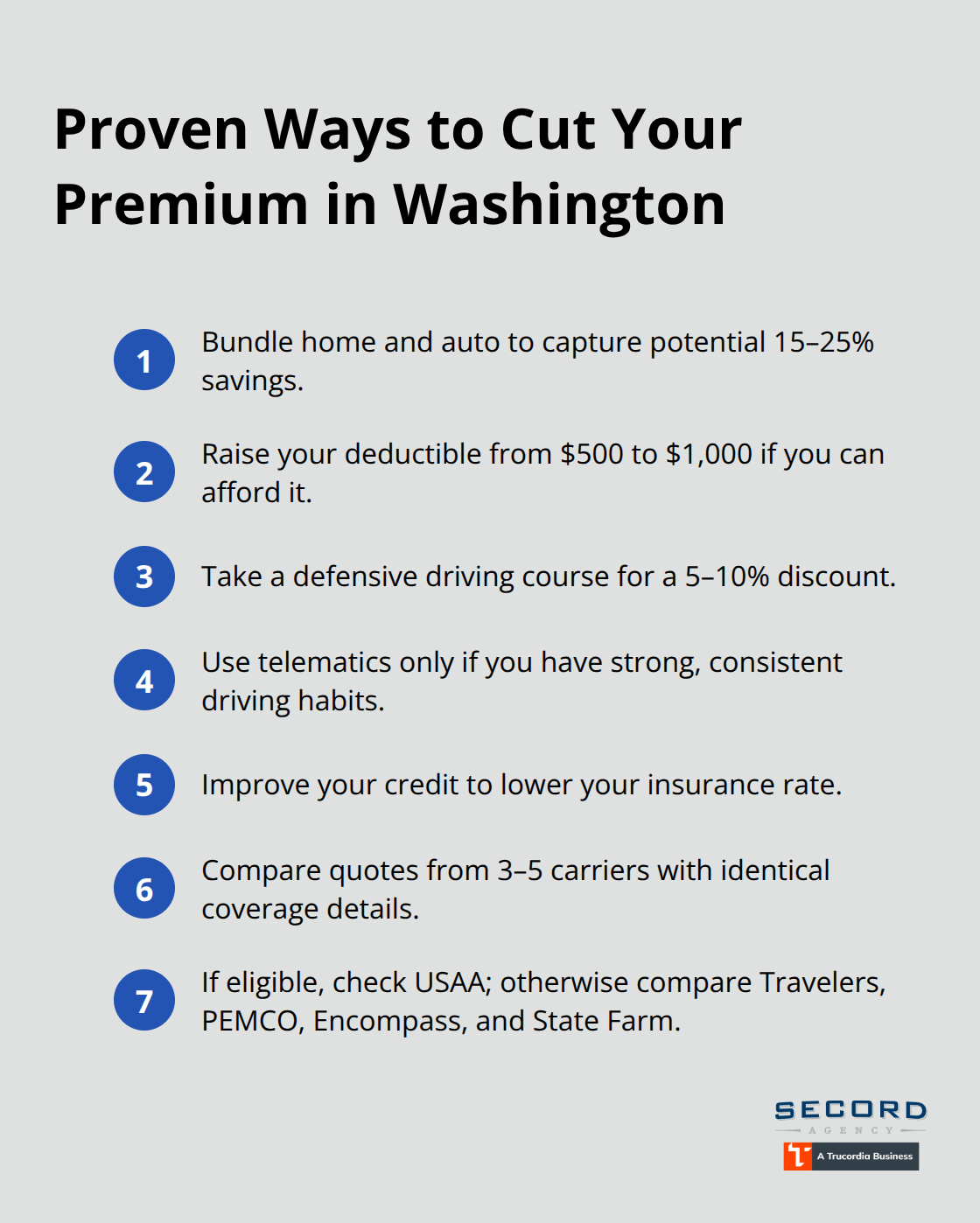

Bundling your home and auto policies with the same insurer typically saves money, though the actual discount varies widely by carrier and your location. Some insurers offer substantial savings-sometimes 15–25% off your auto premium-while others deliver modest reductions. Request a bundling quote from multiple carriers before committing, because one insurer’s bundle discount might undercut another’s single-policy rate. This comparison takes minutes but often reveals hundreds in annual savings.

Raise Your Deductible If You Can Afford It

Increasing your deductible from $500 to $1,000 meaningfully lowers your monthly costs, but only raise it if you can afford to pay that amount out-of-pocket if you file a claim. According to Bankrate data, this single adjustment reduces your premium noticeably without sacrificing the protection you need most. The trade-off is straightforward: lower monthly payments in exchange for higher out-of-pocket costs when accidents happen.

Activate Safe Driving and Telematics Discounts

Safe driving discounts reward accident-free records and sometimes require you to complete a defensive driving course, which typically costs $30–$50 and can reduce your rate by 5–10%. Telematics programs, where an app or device monitors your driving habits, can lower premiums especially for younger drivers, though you should review sample rates before enrolling because a poor driving score might actually increase your costs. These programs work best for drivers confident in their habits.

Improve Your Credit and Shop Multiple Carriers

Credit history still influences your Washington premium despite regulatory changes-drivers with poor credit pay 105 percent more for full coverage car insurance than those with excellent credit according to Bankrate-so paying bills on time and addressing errors on your credit report directly improves your insurance rate. Shopping around is non-negotiable: rates differ substantially across carriers for identical coverage, and gathering quotes from at least three to five insurers takes roughly 15 minutes online. USAA consistently offers the lowest rates in Washington, averaging around $93 monthly for full coverage, but eligibility is restricted to military members and their families. If you don’t qualify for USAA, compare Travelers, PEMCO, Encompass, and State Farm, since these carriers frequently offer competitive pricing across different driver profiles. Request quotes for the exact same coverage levels and deductibles across all carriers so you’re comparing apples to apples, and don’t skip smaller or regional insurers because they sometimes undercut national players in specific areas. Washington’s Insurance Commissioner provides complaint data for each carrier, helping you balance low rates with reliable claims service-paying slightly more for a carrier with fewer complaints often proves worthwhile if you ever need to file a claim.

These strategies lower your costs, but common mistakes can erase those savings just as quickly.

Mistakes That Tank Your Insurance Savings

Cutting your premium requires discipline beyond just choosing the right coverage level. Most Washington drivers accidentally reverse their savings through preventable errors that either spike rates dramatically or leave them legally exposed.

Policy Lapses Create Legal and Financial Disasters

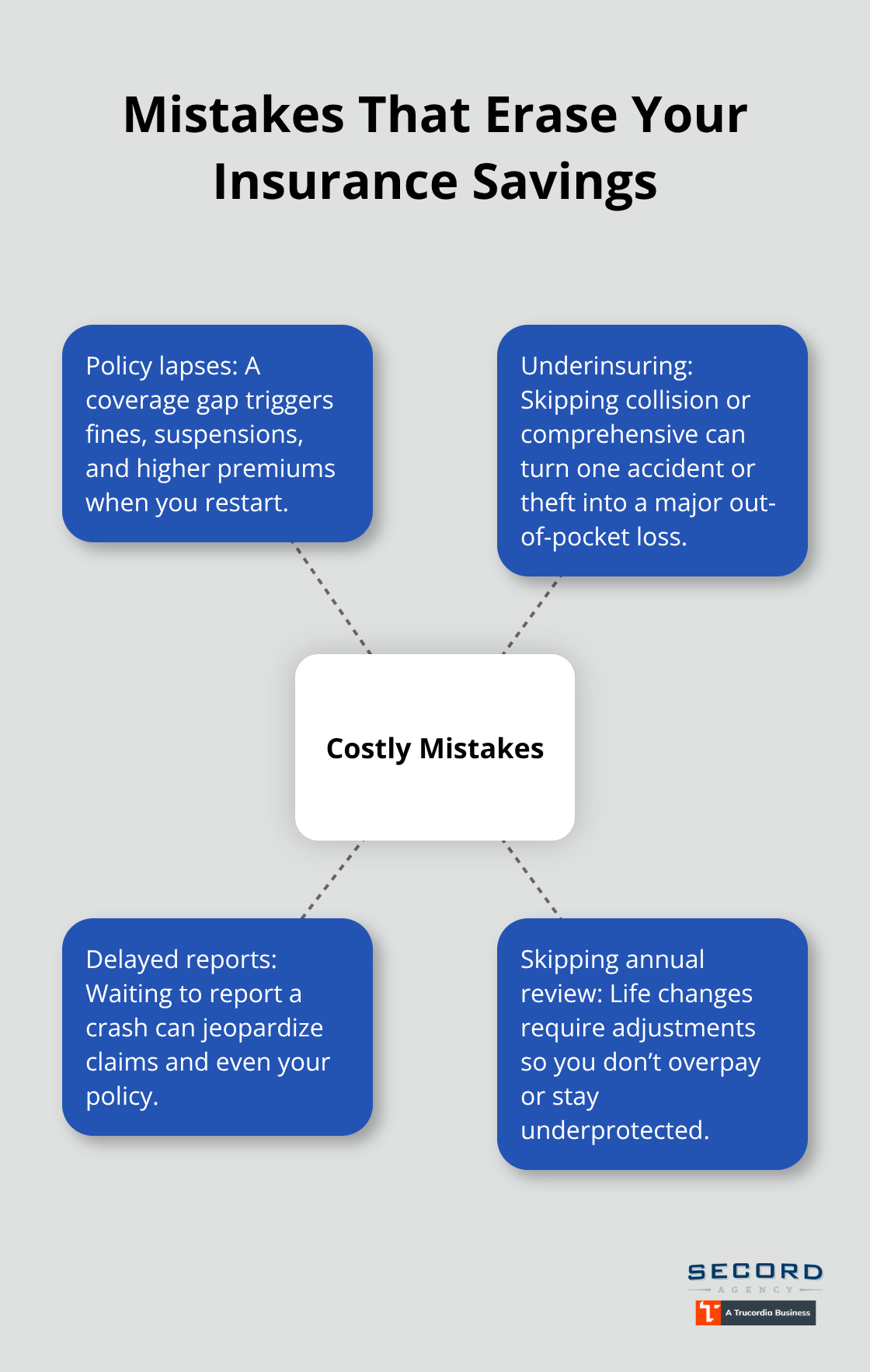

A lapsed policy ranks among the costliest mistakes because Washington law requires continuous coverage, and any gap creates serious consequences. Driving without insurance exposes you to fines starting at $550, potential license suspension, and if you cause an accident, you become personally liable for all damages and injuries. Insurers also penalize lapses heavily: when you restart coverage after a gap, your rate climbs significantly because the gap itself signals risk to underwriters. Set automatic payments through your bank or insurer so renewal happens without thinking about it.

Underinsuring Your Vehicle Backfires in Claims

You save money monthly but face catastrophic costs when accidents happen. Washington’s minimum liability of 25/50/10 covers others but leaves your own vehicle unprotected unless you add collision and comprehensive coverage. Bankrate data shows that drivers with at-fault accidents pay roughly $222 monthly on average, meaning one mistake wipes out years of premium savings if you skipped collision coverage.

The real risk emerges in high-theft areas: Washington experienced nearly 50,000 vehicle thefts in 2022 according to the Insurance Information Institute and FBI data, making comprehensive coverage essential in Seattle, Tacoma, and other urban centers where theft rates run highest.

Delayed Accident Reports Complicate Claims

Reporting accidents promptly matters more than most drivers realize because delays complicate claims and sometimes invalidate coverage entirely. Contact your insurer within 24 hours of any accident, even minor ones, because waiting weeks or months gives insurers grounds to deny claims or cancel policies for misrepresentation. Photograph damage, collect witness information, and file a police report for any collision involving another vehicle or property damage exceeding minor amounts.

Annual Coverage Reviews Prevent Overpaying and Underprotecting

Life changes like paying off a car loan, relocating within Washington, or reaching retirement age should trigger a policy review because your coverage needs shift accordingly. A vehicle worth $5,000 might not justify collision coverage with a $500 deductible, but the same vehicle in a high-theft zip code absolutely should carry comprehensive protection. Secord Agency, a Trucordia business based in Seattle’s Wallingford neighborhood, provides personalized policy reviews to help Washington drivers maintain appropriate coverage without overpaying. These annual check-ins typically reveal opportunities to adjust deductibles, drop unnecessary coverage, or add protections you’ve overlooked-changes that often reduce premiums while improving your actual protection.

Final Thoughts

Finding cheap auto insurance in Washington requires three core actions: understanding what insurers measure, applying proven strategies to lower your costs, and avoiding the mistakes that erase your savings. Your driving record, vehicle type, location, and credit history determine your baseline rate, but you control the outcome through bundling, deductible adjustments, safe driving discounts, and shopping multiple carriers. A clean record saves you thousands over time, while a single lapse or underinsured vehicle costs far more than years of premium reductions.

Start by gathering quotes from at least three carriers using identical coverage levels and deductibles so you compare actual apples-to-apples pricing. USAA offers the lowest rates in Washington if you qualify, but Travelers, PEMCO, Encompass, and State Farm frequently deliver competitive pricing for other driver profiles. Request bundling quotes, ask about safe driving and telematics discounts, and review the Washington Insurance Commissioner’s complaint data to balance low rates with reliable claims service (raising your deductible from $500 to $1,000 cuts your monthly payment meaningfully if you can afford the higher out-of-pocket cost when accidents happen).

An independent agent who shops multiple carriers saves you time and often uncovers discounts you’d miss alone. We at Secord Agency, a Trucordia business based in Seattle’s Wallingford neighborhood, specialize in pairing competitive rates with personalized policy reviews that match your actual coverage needs. Contact Secord Agency to compare quotes and build a policy that protects your budget without sacrificing the coverage you need.