Condo Homeowners Insurance: Coverage That Fits Your Unit

Condo homeowners insurance protects what matters most-your unit, your belongings, and your financial security. Most condo owners assume their building’s master policy covers everything, but significant gaps often exist that leave you exposed.

We at Secord Agency – A Trucordia Business help condo owners understand exactly what they need to protect themselves. This guide walks you through coverage options, identifies common gaps, and shows you how to choose the right policy for your situation.

What Your Condo Insurance Actually Protects

Dwelling Coverage for Your Interior Upgrades

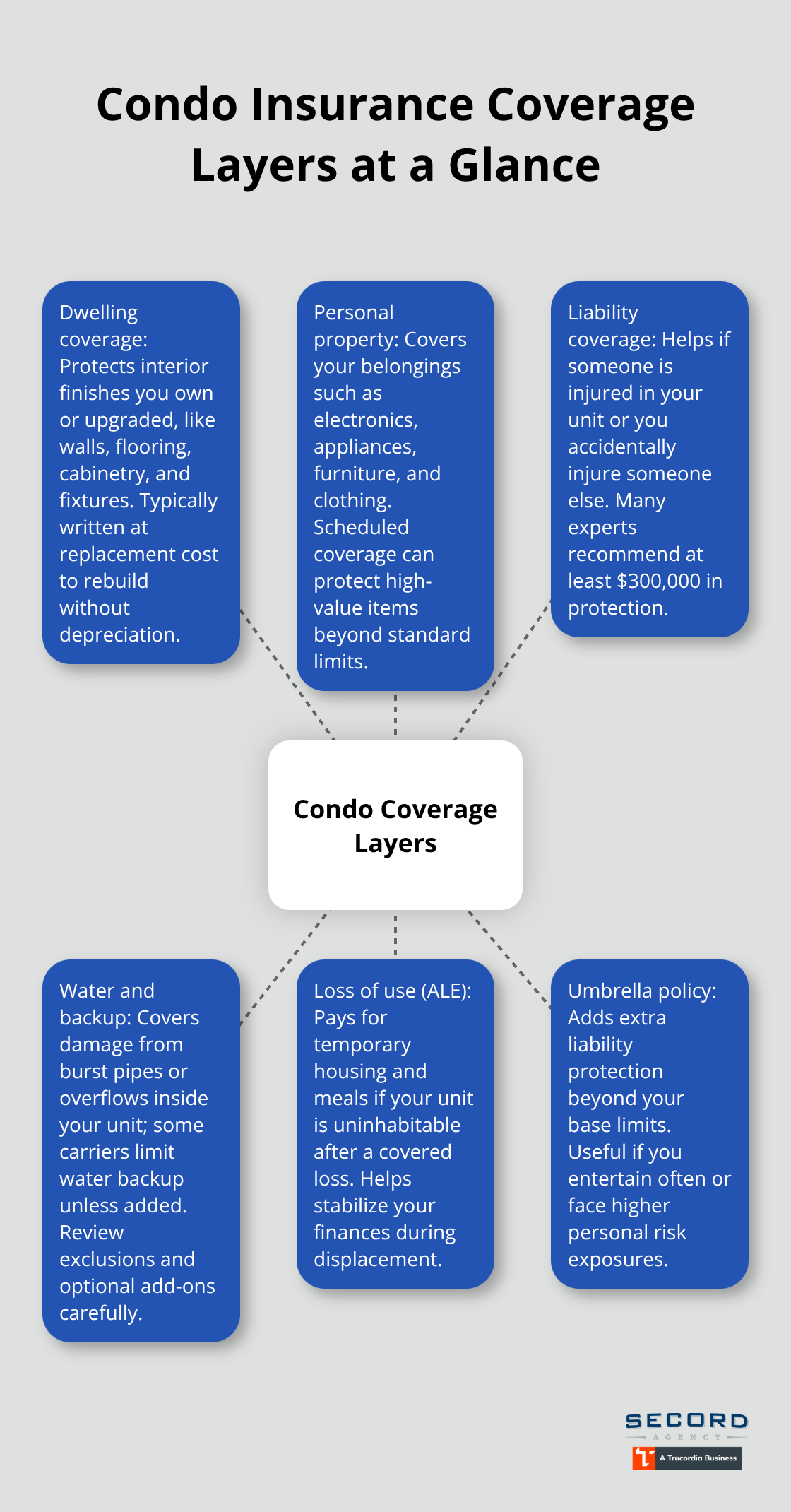

Condo insurance covers three distinct layers of protection that the master policy leaves untouched. Dwelling coverage protects the interior finishes of your unit-the walls, flooring, cabinetry, and fixtures you own or upgraded. This is not the building structure itself, which the association covers. If you’ve invested in a kitchen remodel or installed custom built-ins, dwelling coverage reimburses you to replace those improvements at current costs. Most policies offer this at replacement cost value, which means you receive funds to rebuild without depreciation. Try insuring dwelling coverage at roughly 20 percent of your condo’s market value, though this varies based on construction costs in your area and what the master policy actually covers.

Personal Property and High-Value Items

Personal property coverage protects your belongings-electronics, appliances, furniture, and clothing inside the unit. This coverage matters because the master policy never covers your personal possessions. If you own high-value items like jewelry, art, or watches, standard personal property limits won’t be enough. You’ll need scheduled property coverage as an endorsement to protect those specific items fully. Scheduled coverage ensures you can replace valuable belongings without hitting standard policy caps.

Liability Protection Against Injury Claims

Liability coverage defends you financially if someone is injured in your unit or if you accidentally injure someone else. Most policies start around $100,000, but experts recommend at least $300,000 in liability protection. If you frequently entertain guests or have higher risk activities, an umbrella policy provides additional protection beyond the base coverage. This extra layer shields your personal assets from major claims that exceed your standard limits.

Water Damage and Loss of Use Coverage

Water damage ranks as the leading cause of loss in condo buildings, driven by aging systems, freezing temperatures, and severe weather. Your personal policy should cover damage from burst pipes or overflowing toilets within your unit, but review exclusions carefully since some carriers limit water backup coverage to an optional add-on. Loss of use coverage, also called additional living expenses, pays for temporary housing and meals if your unit becomes uninhabitable after a covered loss-a practical safeguard that protects your finances during displacement. These protections work together to address the specific risks condo owners face, yet they only tell part of the story. The real challenge emerges when you compare what your individual policy covers against what the master policy actually protects, revealing gaps that could leave you financially exposed.

Where Your Individual Policy Fills What the Master Policy Misses

What the Master Policy Actually Covers

The master policy your condo association maintains covers the building structure, common areas like hallways and elevators, and liability for the association itself. Roof damage, exterior wall repairs, and damage to shared spaces fall under that umbrella. The association’s policy is funded through your monthly dues, but it protects the building as a whole, not your personal financial interests. This separation creates a hard boundary that forces you to carry your own coverage.

Why Your Personal Coverage Cannot Wait

The master policy deliberately excludes your unit’s interior and everything inside it. This gap means you must carry individual condo insurance to protect what the association’s policy leaves uninsured. Without your own policy, you face a manageable deductible or catastrophic out-of-pocket costs when something goes wrong. Your personal liability minimum of $300,000 also stands separate from the association’s general liability. If someone slips in your unit and sues, the association’s coverage does not protect you individually. Your condo policy shields your personal assets from judgment.

Water Damage: Where Gaps Create Real Costs

Water damage illustrates the gap perfectly. When a burst pipe floods your unit, the master policy covers damage to the building’s structure if the pipe is in a common wall. Your individual policy covers the water damage inside your unit, your flooring, cabinetry, and personal property. However, many condo associations have raised water deductibles because high deductibles keep small claims from piling up on the association’s loss history, keeping premiums lower for everyone. If damage straddles the boundary between common area and your unit, you could owe your share of that steep deductible while your personal policy covers the interior portion.

Legislation and Your Repair Responsibility

Condo owners in British Columbia discovered a harsh reality when legislation required unit owners to repair damage to their own units regardless of cause. This left them responsible even when the association’s negligence caused the loss. The practical takeaway: contact your association for the exact master policy deductible amounts for water, earthquake, and other major perils. Then confirm your personal policy covers your portion of those costs. These gaps are not theoretical-they directly determine whether you recover fully after a loss or absorb tens of thousands in uninsured damage. Understanding exactly what your association covers and what you must protect yourself allows you to make informed decisions about the right coverage levels for your situation.

How to Choose the Right Condo Insurance Policy

Inventory Your Belongings and Calculate Coverage Needs

Start with a complete inventory of everything inside your unit and estimate what it would cost to replace today. Photograph your belongings, note serial numbers on electronics, and gather receipts or recent valuations for high-value items. This inventory becomes your foundation for determining personal property limits. Next, measure your unit’s square footage and research local construction costs per square foot in your area to calculate a realistic dwelling coverage amount. The 20 percent rule of thumb works, but only if you know your condo’s actual market value and understand what your master policy excludes.

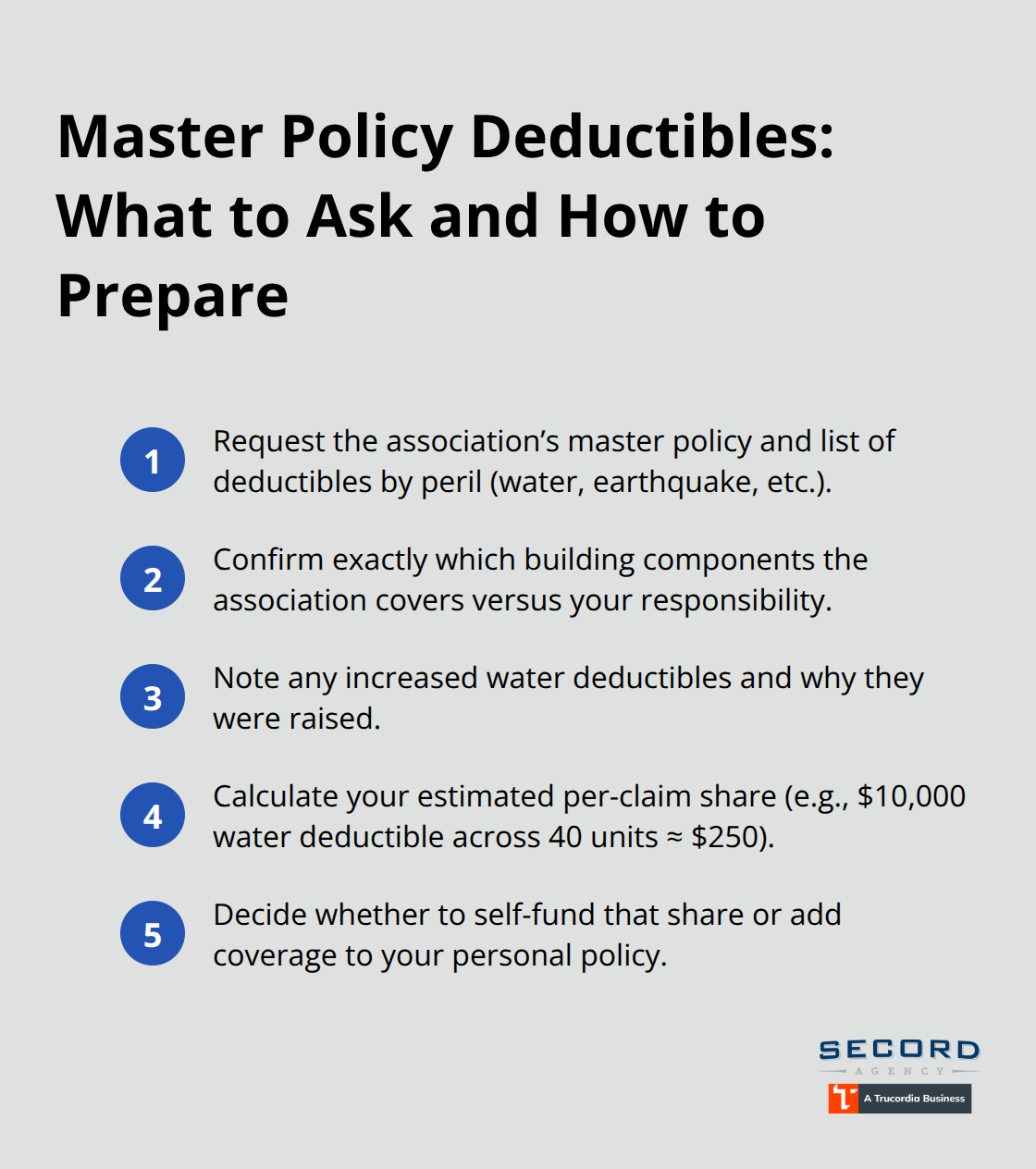

Request Master Policy Details from Your Association

Contact your condo association and request a copy of their master policy details. Ask specifically for water damage deductibles, earthquake deductibles if you live on the West Coast, and exactly what building components they cover. Many associations have raised water deductibles significantly in recent years because water damage remains the leading cause of loss in condo buildings. Once you know those deductible amounts, you can calculate your potential out-of-pocket exposure and decide whether your personal policy should cover those gaps. If your association carries a $10,000 water deductible and you have 40 units, your share could reach $250 per claim. Your personal policy should address whether you want to absorb that cost or transfer it to insurance.

Compare Quotes Across Multiple Carriers

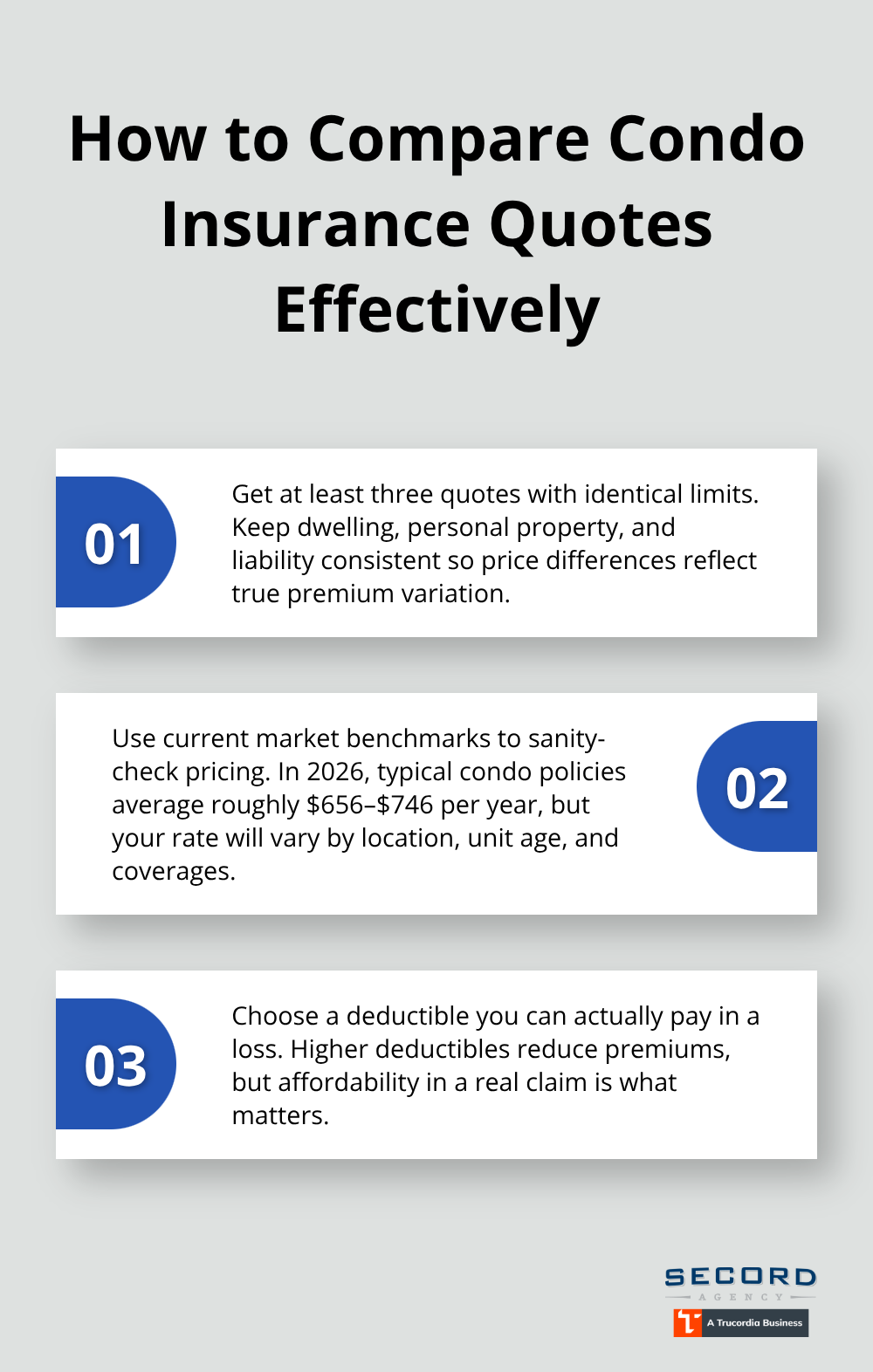

Gather quotes from at least three carriers and compare the same coverage limits across each quote. As of 2026, average condo insurance costs range from roughly $656 to $746 per year according to Insurance.com using Quadrant Data Services, though your actual premium depends heavily on location, unit age, and coverage choices. Request quotes with identical dwelling coverage amounts, personal property limits, and liability minimums so you can see real price differences rather than coverage differences. Higher deductibles directly lower premiums, but only select a deductible you can actually afford to pay out-of-pocket when a loss occurs.

Update Your Policy After Changes to Your Unit

Review your policy annually, especially after renovations or major purchases. If you upgraded your kitchen or added built-in cabinetry, that improvement must be reflected in your dwelling coverage limits. Changes to your unit’s condition, value, or contents warrant a policy adjustment to maintain adequate protection. An independent agent can review your master policy and help you determine the exact coverage gaps your individual policy needs to fill, ensuring you do not overpay for redundant coverage while protecting yourself against genuine risks specific to your unit and location.

Final Thoughts

Condo homeowners insurance fills the gaps that your association’s master policy leaves open, protecting your unit, your belongings, and your personal assets from financial ruin. Water damage remains the leading cause of loss in condo buildings, and many associations have raised their deductibles significantly in recent years, which means your personal policy must address whether you want to cover your share of those steep deductibles or face the cost yourself. Earthquake deductibles on the West Coast create similar exposure, especially in high-rise buildings where your share of a building-wide deductible can reach thousands of dollars.

Your policy demands attention after renovations, major purchases, or changes to your unit’s condition. An annual review ensures your dwelling limits match your improvements, your personal property coverage reflects what you actually own, and your liability protection remains adequate for your lifestyle. As of 2026, average condo insurance costs range from roughly $656 to $746 per year, but your actual premium depends on your location, unit age, and the specific coverage you choose.

We at Secord Agency – A Trucordia Business shop multiple carriers to find condo homeowners insurance that fits your specific unit and your budget. Our team reviews your master policy details, identifies the gaps your individual policy must fill, and helps you avoid overpaying for redundant coverage while protecting yourself against genuine risks. Contact us today to get quotes and ensure your strategy is solid.