Landlord Liability Coverage Seattle: Protect Your Investment with Confidence

Owning rental property in Seattle comes with real financial exposure. Tenant injuries, property damage claims, and lawsuits can drain your savings fast.

Landlord liability coverage Seattle protects you from these costly risks. We at Secord Agency – A Trucordia Business help property owners build the right insurance strategy for their specific situation.

What Landlord Liability Coverage Actually Covers

The Real Cost of Liability Claims

Landlord liability coverage protects you when a tenant or guest gets injured on your property and sues for damages. This coverage pays for medical bills, legal defense costs, and court settlements-expenses that can devastate your finances without proper protection.

What Your Policy Actually Covers

The policy covers injuries that happen because of your negligence as a property owner, not because of tenant misconduct. If a guest slips on ice you failed to clear from the entryway or falls through a rotten deck board, your liability coverage responds. It does not cover intentional acts, criminal behavior, or injuries the tenant caused through their own carelessness. Most Seattle landlords need at least $500,000 per occurrence in liability protection, though Washington’s comparative negligence laws make higher limits prudent for larger portfolios.

Legal Exposure and Lender Requirements

Washington State imposes no legal mandate to carry landlord liability insurance, but your mortgage lender almost certainly does. If you still owe money on the property, your lender’s loan documents require you to maintain landlord insurance. Beyond lender requirements, the Residential Landlord-Tenant Act creates substantial legal exposure. You must maintain habitable conditions, handle repairs promptly, and follow strict eviction procedures-failures in any of these areas invite lawsuits.

Hidden Risks That Standard Policies Exclude

Earthquake risk in the Cascadia Subduction Zone carries a 10–15% probability of a magnitude 9.0 event within the next 50 years according to the Washington Geological Survey, yet standard policies exclude earthquake damage entirely. Flooding affects more than 175,000 structures in mapped Washington floodplains and is similarly excluded unless you add coverage. These statistics show that liability and property risks are not theoretical-they happen regularly to Seattle landlords.

Pairing strong liability limits with property damage coverage and specialized endorsements for earthquake and flood is the only realistic way to protect your investment. The next section explores the specific types of liability coverage available and how each one addresses different aspects of your exposure.

Coverage Types That Actually Protect Your Rental Investment

General liability coverage forms the foundation of protection, but it alone leaves significant gaps. This coverage handles injuries to tenants or guests on your property and covers your legal defense if someone sues. However, the standard limit of $300,000 to $500,000 per occurrence falls short in Seattle’s high-cost environment. Washington’s comparative negligence laws mean courts can assign partial blame to you even when a tenant shares responsibility for an accident. A tenant slips on your icy stairs while checking their phone-the court might still hold you 40% liable. That $500,000 limit disappears quickly when medical bills, legal fees, and settlements stack up.

Why $500,000 Limits Fail Seattle Landlords

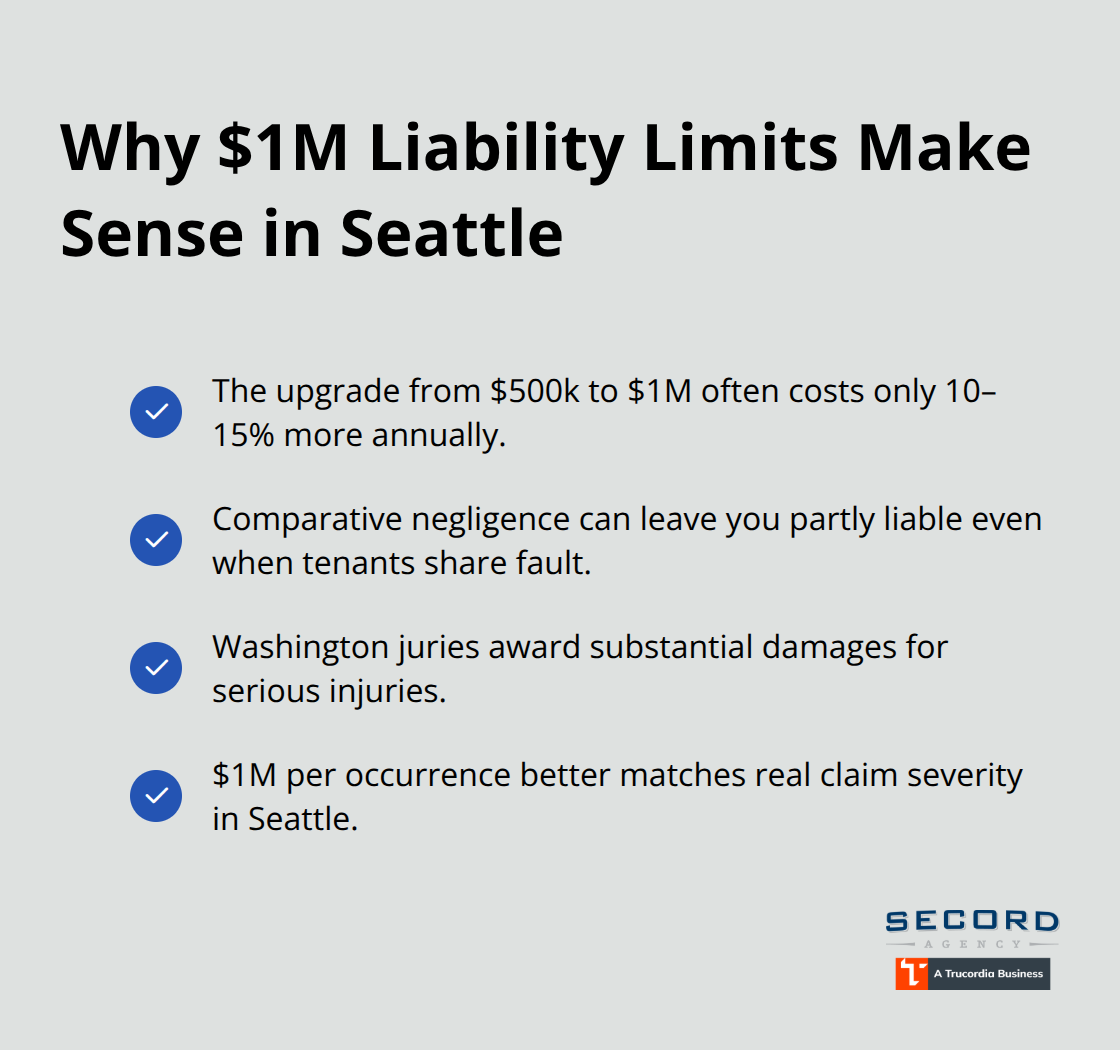

Most Seattle landlords start with inadequate liability limits. The premium difference between $500,000 and $1,000,000 per occurrence is modest-typically 10–15% more annually-making the upgrade practical rather than optional.

You should try $1,000,000 per occurrence for any landlord with multiple properties or higher-value units. This threshold reflects the real cost of serious injury claims in Washington courts, where juries award substantial damages for permanent injuries.

Property Damage Claims Exceed Expectations

Property damage and loss coverage handles the physical destruction of your building and lost rental income during repairs. This is where most landlords underestimate their exposure. Average property damage claims in Washington exceeded $9,800 in 2022 according to the Washington State Office of the Insurance Commissioner, but catastrophic events cost far more. A kitchen fire that displaces tenants for three months means zero rent while you still pay the mortgage. Seattle’s reconstruction costs run $350–$500 per square foot, so a modest 2,000-square-foot building costs $700,000 to $1,000,000 to rebuild.

Your dwelling coverage limit must reflect these real numbers, not some theoretical value. Replacement cost value policies, not actual cash value, are non-negotiable in Seattle. An actual cash value policy subtracts depreciation, leaving you thousands short when you need to rebuild. You must verify your coverage limits match current Seattle construction costs, not the price you paid five years ago.

Umbrella Policies Protect Against Catastrophic Awards

Umbrella liability policies sit above your general liability coverage and activate only after that limit exhausts. Common requirements include $300,000 to $500,000 in auto liability coverage and similar amounts for homeowners or renters liability. A $1,000,000 umbrella policy costs roughly $200–$400 annually and provides catastrophic protection. This matters because a serious injury lawsuit-say a tenant’s permanent spinal injury from a fall you could have prevented-easily exceeds $1,000,000 in damages. Medical care, lost wages, and pain-and-suffering awards in Washington courts regularly surpass this threshold.

Umbrella policies also cover gaps that general liability excludes, making them especially valuable for landlords with older properties or higher-risk tenant situations. Without an umbrella, your personal assets become targets if a judgment exceeds your liability limit. This combination costs less than most people assume and protects your long-term investment growth far more effectively than hoping for luck.

The specific coverage limits you need depend on your property’s age, condition, and tenant profile. The next section walks you through how to assess these factors and select the right policy for your situation.

Selecting the Right Coverage for Your Property’s Actual Risks

Document Your Property’s Specific Hazards

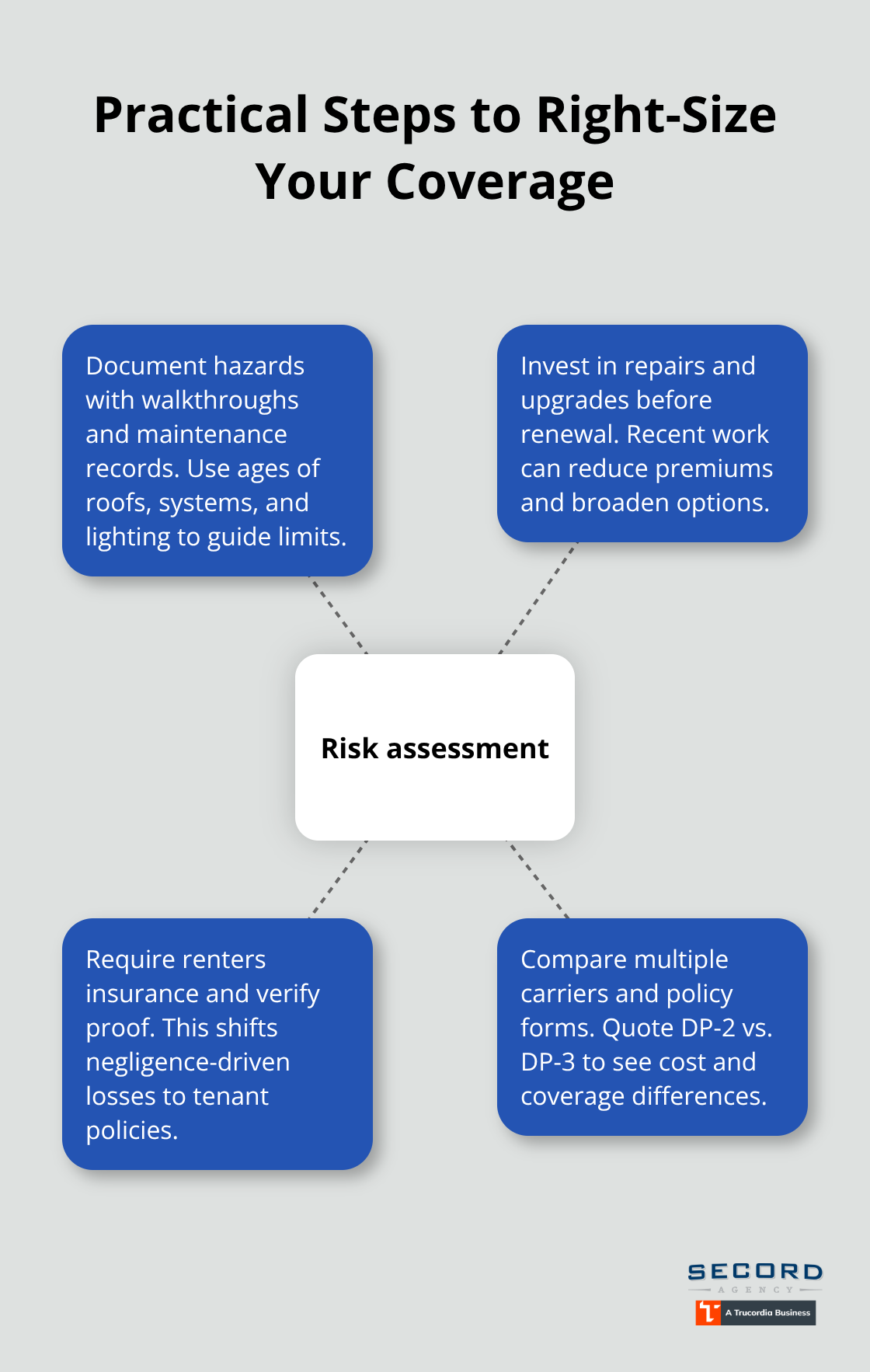

Your property’s age, condition, and tenant profile determine which liability limits and endorsements you genuinely need. A newer building with owner-occupied units demands different coverage than a 40-year-old fourplex in a high-traffic neighborhood. Walk the building and note maintenance issues, system ages, and areas where tenants or guests are most likely to get injured. Icy entryways in winter, worn deck railings, old electrical systems, and poorly lit stairwells create measurable liability exposure.

Properties over 25 years old face harder placement and typically require $300,000 to $500,000 in liability limits just to get quotes, according to FirstMark Insurance Group. If your roof exceeds 10 years, carriers scrutinize water damage claims more carefully. Document everything-maintenance records, repair dates, and system upgrades-because insurers use this information to set your premium and determine whether they’ll offer coverage at all.

Invest in Maintenance to Lower Premiums

Properties with recent roof, plumbing, or electrical work qualify for better rates and broader coverage options, sometimes reducing premiums by 5–10% compared to similar buildings with deferred maintenance. Obtain bids for any planned repairs before renewal to show insurers you’re investing in risk reduction; this positioning often improves both premium and coverage terms.

Require Tenant Insurance Coverage

Your tenant situation shapes coverage needs significantly. High-turnover rental markets with shorter leases carry different risks than long-term tenancies.

Require tenants to maintain renters insurance and verify proof of active policies at lease signing and during occupancy. This single requirement cuts your exposure substantially because tenant negligence won’t trigger your policy if they carry their own coverage.

Compare Multiple Carriers and Policy Forms

Compare quotes across multiple carriers because pricing varies dramatically. FirstMark Insurance Group notes that newer commercial properties typically have 8–10 preferred carriers while older buildings have access to more than 20 carriers, giving you substantial shopping power. Request quotes for DP-2 and DP-3 forms side by side so you see the actual premium difference-often 15–25% separates them, making DP-3’s broader coverage worthwhile for most Seattle landlords.

Final Thoughts

Protecting your Seattle rental investment requires landlord liability coverage Seattle that matches your property’s actual risks, not generic limits that leave you exposed. The combination of adequate general liability protection, property damage coverage, and an umbrella policy creates a financial shield against the real costs Seattle landlords face. Average liability claims in Washington exceed $22,300, and serious injury cases regularly surpass $1,000,000 in damages.

The specific limits and endorsements you need depend on your property’s age, condition, and tenant profile. A 40-year-old fourplex demands different protection than a newer building, and maintenance records matter enormously because insurers use them to set premiums and determine coverage eligibility. Requiring tenants to carry renters insurance with substantial liability limits reduces your exposure significantly and demonstrates risk management to carriers.

Working with a local Seattle insurance agent who understands Washington’s specific hazards-earthquake risk, flooding, and comparative negligence laws-makes the difference between adequate coverage and costly gaps. Contact Secord Agency – A Trucordia Business for a personalized review of your current landlord insurance or to get quotes on new coverage that fits your specific property and budget.