Washington Personal Umbrella Insurance: Extra Liability Protection in One Plan

Your home, your car, your savings-one lawsuit could threaten it all. Standard homeowners and auto insurance policies have liability limits that often fall short when serious accidents happen.

At Secord Agency – A Trucordia Business, we see Washington residents underestimate their exposure to major liability claims every day. Washington personal umbrella insurance fills that gap, giving you an extra layer of protection that covers what your other policies don’t.

How Umbrella Insurance Actually Works

Umbrella insurance sits on top of your existing auto and homeowners policies, activating only after those underlying policies hit their liability limits. This is not a replacement for your standard coverage-it’s an additional layer that extends protection when a serious accident or injury claim exceeds what your primary policies cover. If you cause a multi-car accident with 1.2 million dollars in total damages and your auto policy covers only 500,000 dollars, your umbrella policy picks up the remaining 700,000 dollars plus legal defense costs. The structure matters because umbrella coverage activates only when those underlying limits are exhausted, making it far more affordable than raising liability limits on your base policies themselves.

What Your Umbrella Actually Protects

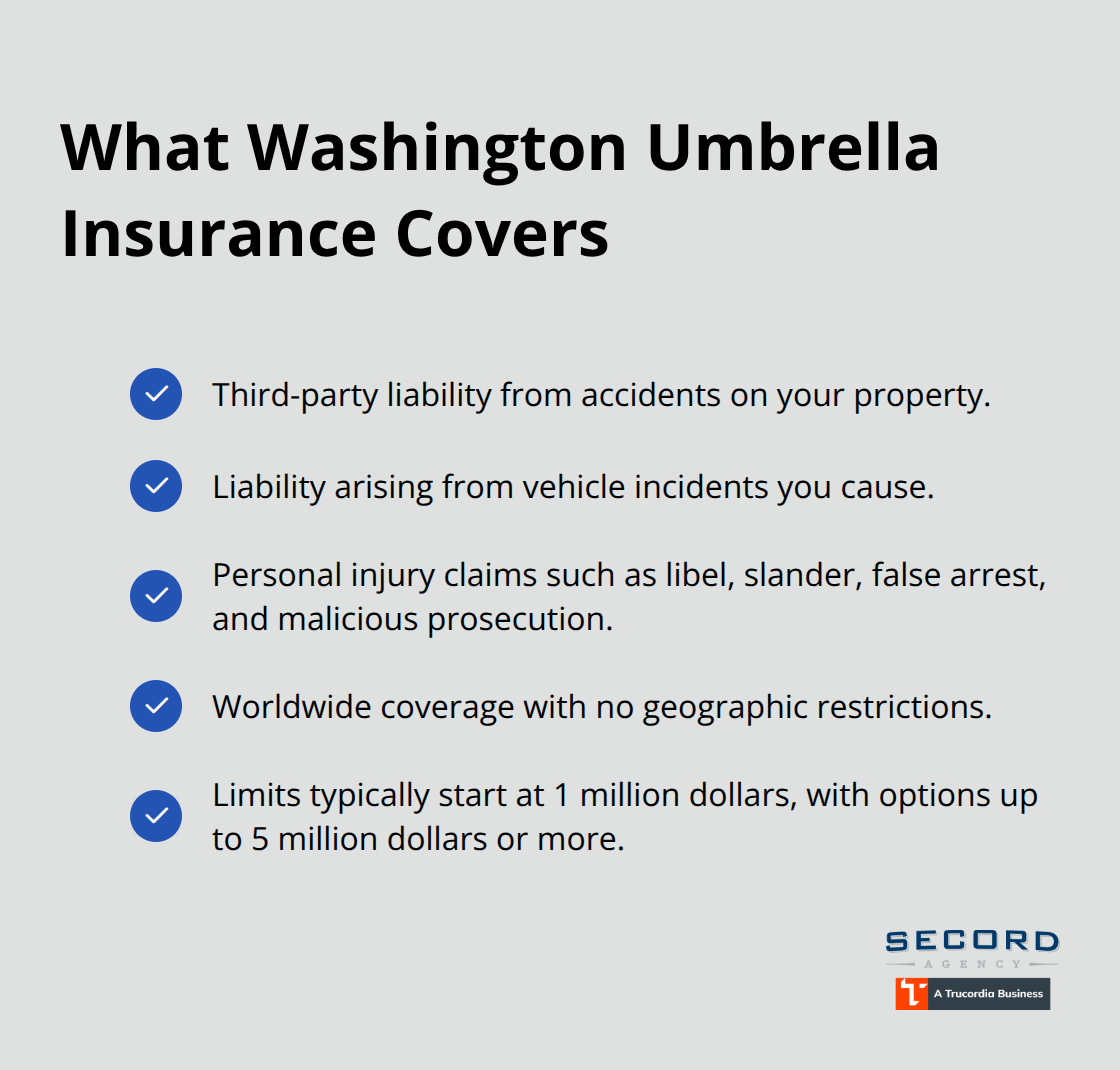

Washington umbrella policies cover third-party liability claims that arise from accidents on your property, vehicle incidents, or personal injury claims including libel, slander, false arrest, and malicious prosecution. These personal injury protections often exceed what standard homeowners or auto policies include, filling real gaps in coverage. Umbrella policies do not cover your own medical bills, damage to your own property, intentional criminal acts, or business liabilities unless you purchase a commercial umbrella separately.

The coverage applies worldwide with no geographic restrictions, meaning protection extends beyond Washington state. Most policies start at 1 million dollars in coverage, though higher limits up to 5 million dollars or more are available depending on your net worth and risk exposure.

The Minimum Requirements That Matter

To qualify for umbrella coverage in Washington, you must maintain underlying auto and homeowners or renters policies with minimum liability limits. Most insurers require at least 300,000 dollars in homeowners liability and 250,000 dollars per person or 500,000 dollars per accident in auto bodily injury coverage. These minimums ensure your base policies have adequate limits before the umbrella activates. A lapse in your underlying policies voids your umbrella coverage entirely, leaving you unprotected. An independent agent can verify your current limits and recommend adjustments to qualify for umbrella protection while keeping overall costs reasonable-this step determines whether you’re truly covered when a major claim strikes.

Who Needs Umbrella Coverage in Washington

High-Risk Life Situations That Demand Extra Protection

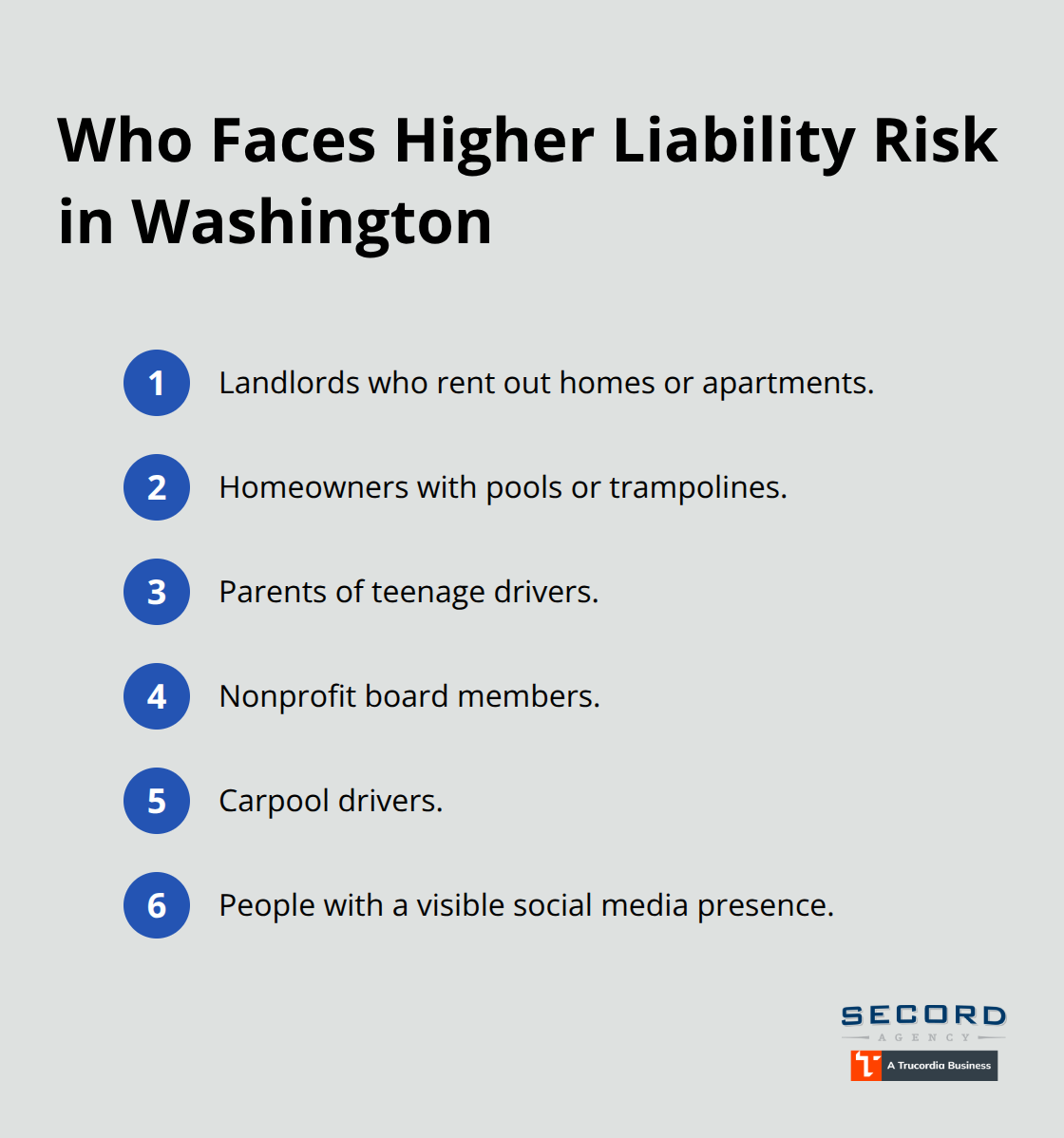

Certain situations and life circumstances create significantly higher liability exposure than others, and Washington residents in these positions face real financial risk without umbrella protection. Landlords top the list-property owners who rent out homes or apartments face tenant injury claims, premises liability suits, and property damage disputes that routinely exceed standard homeowners liability limits. Pool and trampoline owners encounter the same exposure; a single incident involving a guest’s serious injury generates six-figure claims quickly. Parents of teenage drivers represent another high-risk group since young drivers cause accidents at rates substantially higher than experienced drivers, and a multi-vehicle collision easily exceeds the 250,000 dollar per-person auto limit most Washington residents carry.

Nonprofit board members, carpool drivers, and anyone with a visible social media presence also face elevated risk-board members face organizational liability claims, carpool drivers encounter passenger injury exposure, and public figures confront defamation and personal injury claims that standard policies exclude entirely.

How Your Net Worth Determines Coverage Needs

Your net worth and assets determine how much protection you actually need. An ACE Private Risk Services report found that a typical household umbrella policy covering 1 million dollars costs approximately 383 dollars annually, making the expense negligible compared to what you stand to lose. If you own real estate, investment accounts, retirement savings, or a business with significant value, a lawsuit judgment attaches to those assets and potentially reaches future earnings through wage garnishment in Washington. Primary residences receive some exemption protection under state law, but investment properties, rental income, bank accounts, and vehicles remain vulnerable. The calculation is straightforward: if your net worth exceeds 500,000 dollars, umbrella insurance becomes economically rational because the cost of coverage-several hundred dollars annually-is far lower than the risk of losing accumulated wealth.

Assessing Your Personal Risk Profile

Those with net worth under 500,000 dollars may find existing policy limits provide sufficient protection, though this depends entirely on your specific asset mix and state exemptions. An independent agent can assess whether umbrella coverage aligns with what you stand to lose in a major lawsuit and help you understand which of your assets face the greatest exposure. The decision shifts from theoretical to practical once you calculate your actual liability exposure and compare it against the modest annual premium umbrella policies require. Understanding your specific risk profile-your occupation, property holdings, family situation, and net worth-reveals whether umbrella coverage fills a genuine gap in your financial protection strategy.

Choosing the Right Coverage Amount

Calculate Your Actual Liability Exposure

Start with your actual liability exposure, not industry averages. Calculate what a serious lawsuit could cost you by examining your specific situation: Do you own rental property? Do you have a teenage driver? Do you host gatherings regularly? A single incident involving a guest’s serious injury, a tenant’s accident, or a multi-car collision can generate claims exceeding 1 million dollars fast. Court verdicts in Washington regularly reach millions for catastrophic injuries, and that’s before legal defense costs accumulate. Your umbrella limit should reflect the worst realistic scenario you could face, not just what feels comfortable.

Match Your Umbrella Limit to Your Net Worth

Most insurers start at 1 million dollars in coverage, which protects against typical serious incidents but falls short for high-net-worth individuals or those with significant liability exposure. If your net worth exceeds 1 million dollars, jumping to a 2 million dollar umbrella limit adds roughly 75 dollars annually according to Money.com pricing data, making the upgrade economically sensible. For those with net worth above 2 million dollars, a 3 million dollar limit becomes the practical floor since judgments can attach to investment accounts, rental properties, and future earnings through wage garnishment.

Align Your Umbrella with Underlying Policy Limits

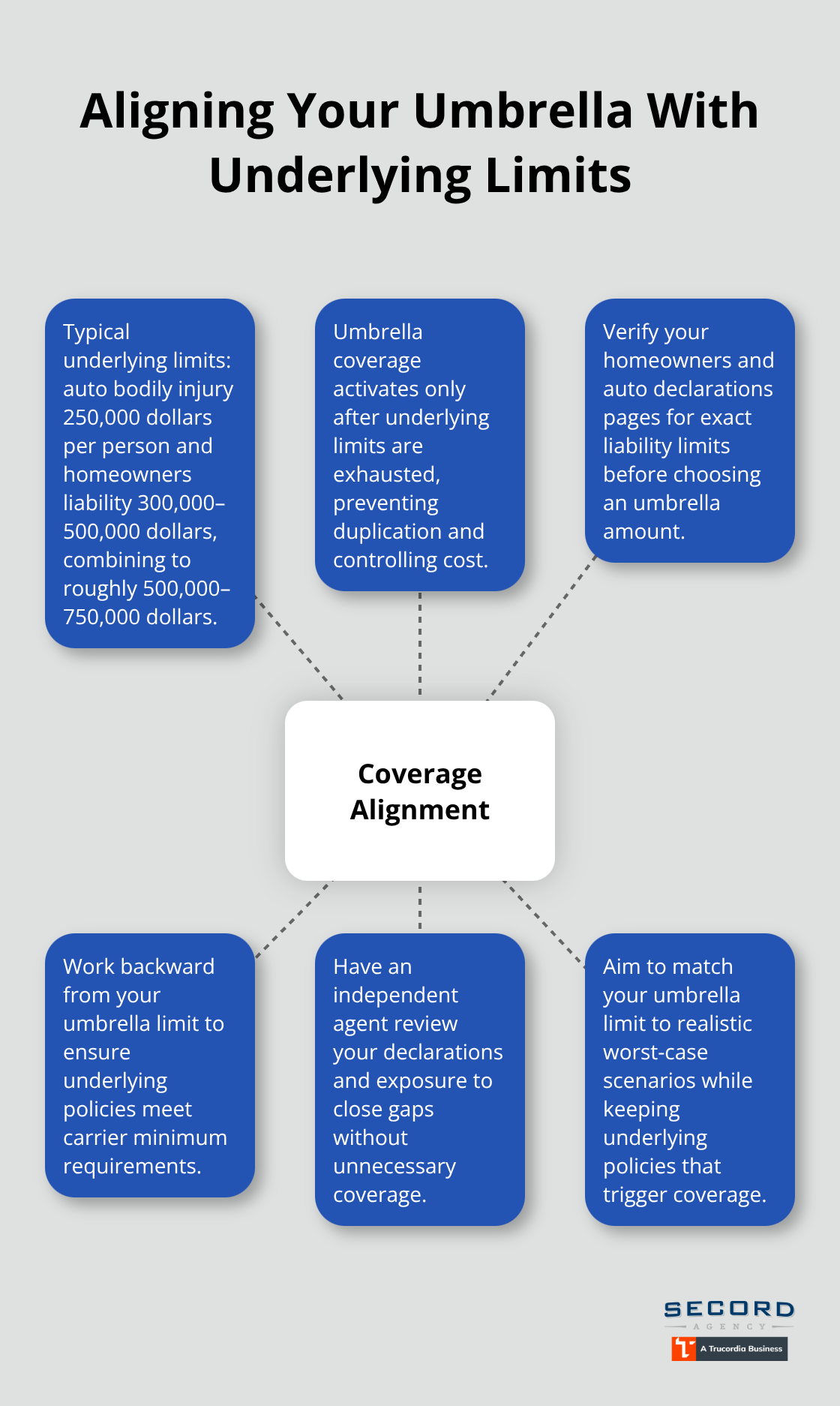

The real work happens when you align your umbrella limit with your underlying policy limits. Most Washington residents carry auto bodily injury limits of 250,000 dollars per person and homeowners liability of 300,000 to 500,000 dollars, creating a combined underlying limit around 500,000 to 750,000 dollars. Your umbrella activates only after these underlying limits exhaust, so a 1 million dollar umbrella leaves a gap if your total underlying coverage sits below 500,000 dollars. Verify your current homeowners and auto declarations pages show the exact liability limits you carry, then work backward from your umbrella choice to confirm your underlying policies meet the minimums most carriers require. An independent agent can review your declarations, calculate your actual exposure based on your property holdings and family situation, and recommend coverage that closes gaps without purchasing unnecessary protection.

The goal is matching your umbrella limit to realistic worst-case liability scenarios while maintaining the underlying policies that trigger umbrella coverage when claims exceed their limits.

Final Thoughts

Washington personal umbrella insurance protects what matters most when standard policies fall short. A single serious accident or injury claim exceeds your auto and homeowners liability limits, exposing your savings, investments, and future earnings to judgment. The financial math is straightforward: umbrella coverage costs a few hundred dollars annually while protecting assets worth hundreds of thousands or millions.

Your actual exposure determines whether umbrella coverage makes sense for your situation. Review your current homeowners and auto declarations pages to confirm your liability limits, then calculate your net worth including real estate, investments, and retirement accounts. If your net worth exceeds 500,000 dollars or you face higher-risk situations like owning rental property or having teenage drivers, Washington personal umbrella insurance becomes economically essential rather than optional.

We at Secord Agency – A Trucordia Business specialize in matching umbrella limits with your underlying policies and your actual risk exposure. Our team reviews your specific situation, verifies your current limits meet minimum requirements, and delivers competitive quotes from multiple insurers. Contact us to discuss your coverage needs and get protected with umbrella insurance that closes gaps without overpaying for unnecessary protection.