Comprehensive Auto Insurance Washington: The Full Coverage Guide

Washington drivers need to understand their auto insurance options to stay protected and compliant with state law. Comprehensive auto insurance in Washington covers more than just the basics, and knowing what you actually need can save you money.

At Secord Agency – A Trucordia Business, we help drivers navigate coverage types, rate factors, and policy selection. This guide walks you through everything required to make an informed decision about your coverage.

What Coverage Do Washington Drivers Actually Need?

Liability Coverage: Why Minimums Fall Short

Washington’s minimum liability requirement is 25/50/10-$25,000 per person, $50,000 per accident for bodily injury, and $10,000 for property damage. These minimums are dangerously low. A single emergency room visit runs $3,000 to $5,000 upfront, and six-figure medical bills occur regularly in serious crashes. Newer vehicles cost $8,000 to $12,000 to repair after a collision. If you cause an accident and your liability limits are exhausted, you face a personal lawsuit. Washington uses an at-fault system, meaning the driver responsible for the crash pays damages. You should carry at least $100,000 in bodily injury coverage and $50,000 in property damage if you have any assets to protect.

Collision and Comprehensive: Protecting Your Vehicle

Collision coverage pays for damage to your car from crashes and typically carries deductibles between $250 and $1,500. If you finance or lease your vehicle, your lender requires collision coverage. Comprehensive coverage protects against theft, weather, vandalism, and wildlife-non-collision damage that liability and collision don’t cover. This protection matters most for newer or valuable vehicles where replacement costs run high.

Uninsured and Underinsured Motorist Coverage

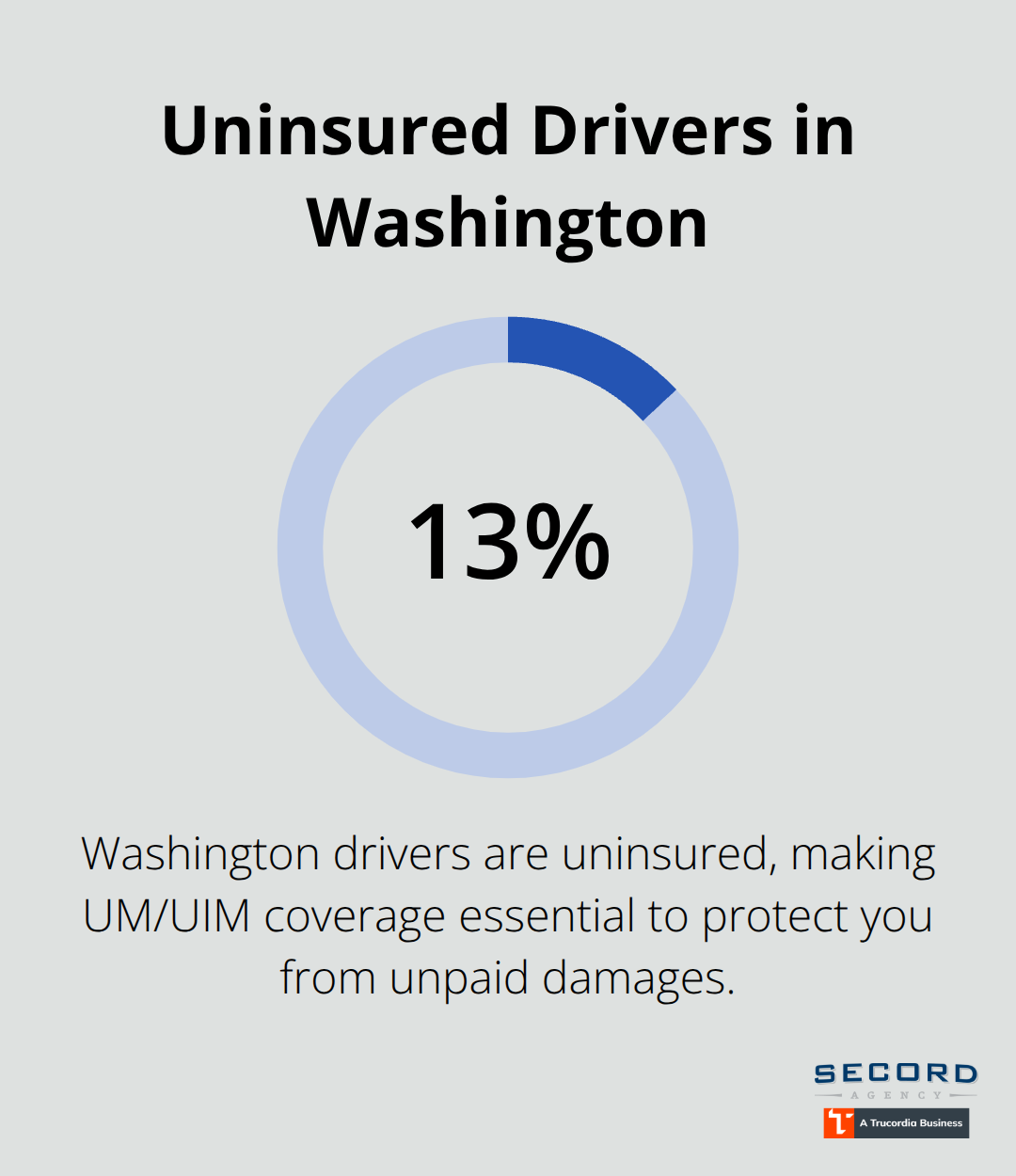

About 13% of Washington drivers are uninsured, making uninsured and underinsured motorist coverage essential. UM/UIM coverage protects you when an uninsured driver hits you or a driver carries insufficient limits. Insurers must offer UM/UIM, though you can decline it in writing. Don’t decline it.

This coverage fills the gap when the at-fault driver cannot pay your damages.

Gap Insurance and Personal Injury Protection

Gap insurance covers the difference between your vehicle’s actual cash value and what you owe on a loan or lease if the car is totaled. This matters most for financed vehicles where you’re underwater on the loan. Personal Injury Protection covers medical expenses, lost wages, and essential services after an accident regardless of fault. Washington law requires insurers to offer PIP, and you can decline, but declining leaves you exposed to uncovered costs.

The gap between minimum requirements and real-world crash costs is substantial. Understanding these coverage types helps you identify where your protection actually breaks down-and that’s where your next policy decision should focus.

Factors That Affect Your Auto Insurance Rates

Driving Record: Your Most Expensive Mistake

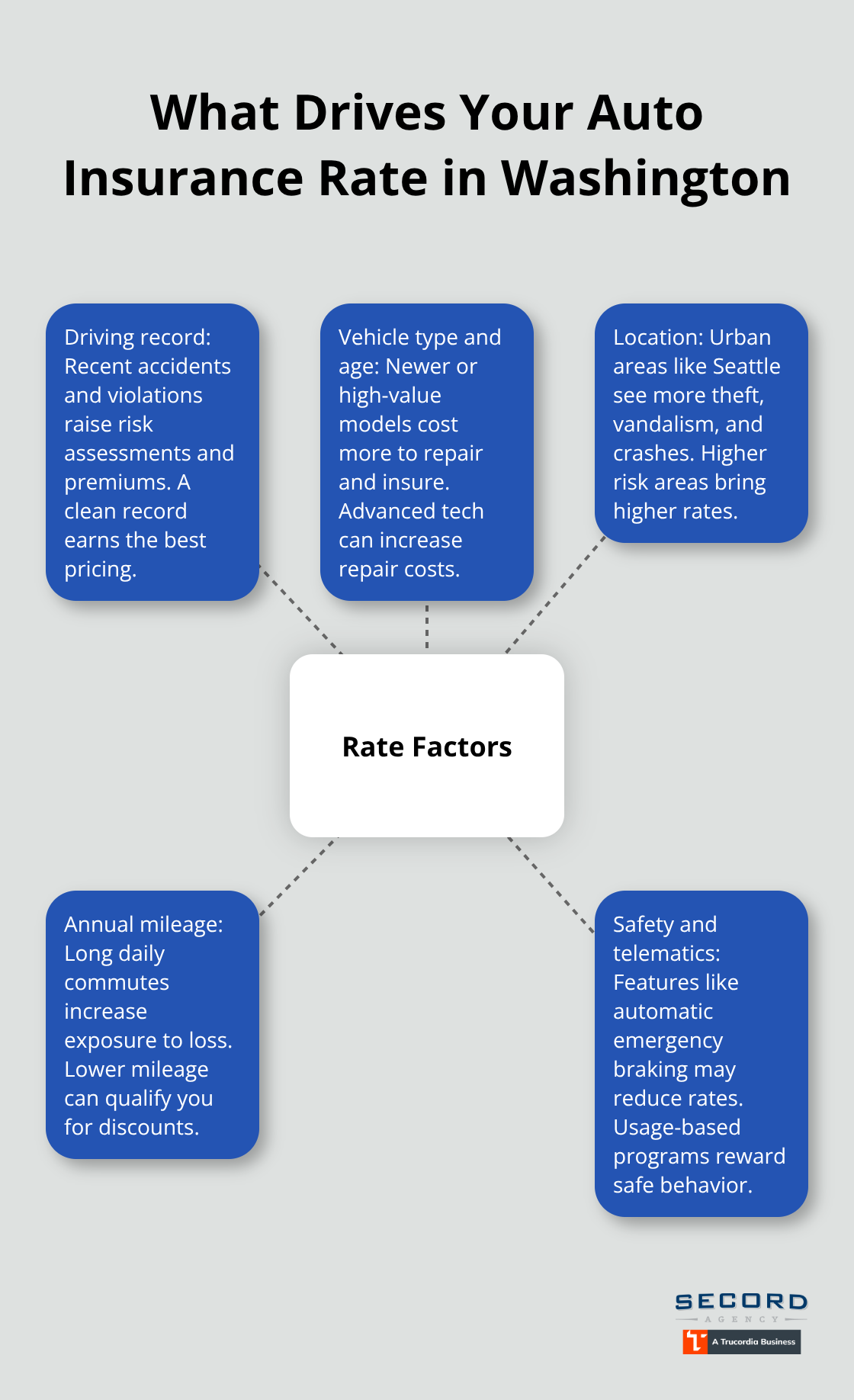

Your driving record is the single most predictive factor in how much you’ll pay for auto insurance, and insurers weight it heavily in their rate calculations. Insurance companies typically review the past three to five years of your driving history when determining your premiums. Multiple violations compound the problem exponentially-two accidents within three years signal to insurers that you represent elevated risk, and your rates reflect that judgment. The Washington Office of the Insurance Commissioner reviews rate filings to ensure they’re reasonable and not unfairly discriminatory, but that doesn’t mean rates stay affordable for drivers with poor records.

If you have a clean driving history, protect it. One mistake costs thousands in premium increases over time. Conversely, if you’ve had incidents, some insurers offer accident forgiveness programs or safe driver discounts after a set period without violations, so shopping around matters more after an accident than before one.

Vehicle Type and Age: What You Drive Matters

Your vehicle’s year, make, model, and repair costs determine how much an insurer will pay in claims if you file a comprehensive or collision claim. Newer vehicles with advanced safety features and expensive replacement parts cost more to insure than older, simpler cars, but they also qualify for safety feature discounts that can offset some costs. A 2024 Honda Accord costs significantly more to repair than a 2010 model, and insurers price premiums accordingly.

Safety features lower your rates because they reduce accident severity and injury risk. Vehicles equipped with automatic emergency braking, lane-keeping assist, and adaptive headlights attract lower premiums from most carriers. Check your vehicle’s safety ratings and features when shopping for quotes-they often yield measurable savings.

Location and Mileage: Where and How Much You Drive

Location amplifies costs further. Urban drivers in Seattle pay higher premiums than rural Washington drivers due to higher theft rates, more frequent accidents, and increased vandalism risk. Annual mileage also matters-drivers who commute 50 miles daily expose themselves to more accidents than those who drive 5,000 miles yearly, and insurers adjust rates upward for high-mileage drivers.

If you work from home or recently shifted to remote work, contact your insurer to lower your mileage estimate; many carriers offer mileage-based discounts or usage-based programs that track your actual driving patterns and reward low-risk behavior with premium reductions. These rate factors aren’t arbitrary-they’re based on actuarial data showing which drivers and vehicles generate the most claims.

Understanding how each factor affects your premium helps you identify where you can make changes to lower costs without sacrificing protection. Once you know what drives your rates, the next step involves comparing actual quotes from multiple carriers to see which one offers the best value for your specific situation.

How to Choose the Right Auto Insurance Policy

Match Coverage to What You Own

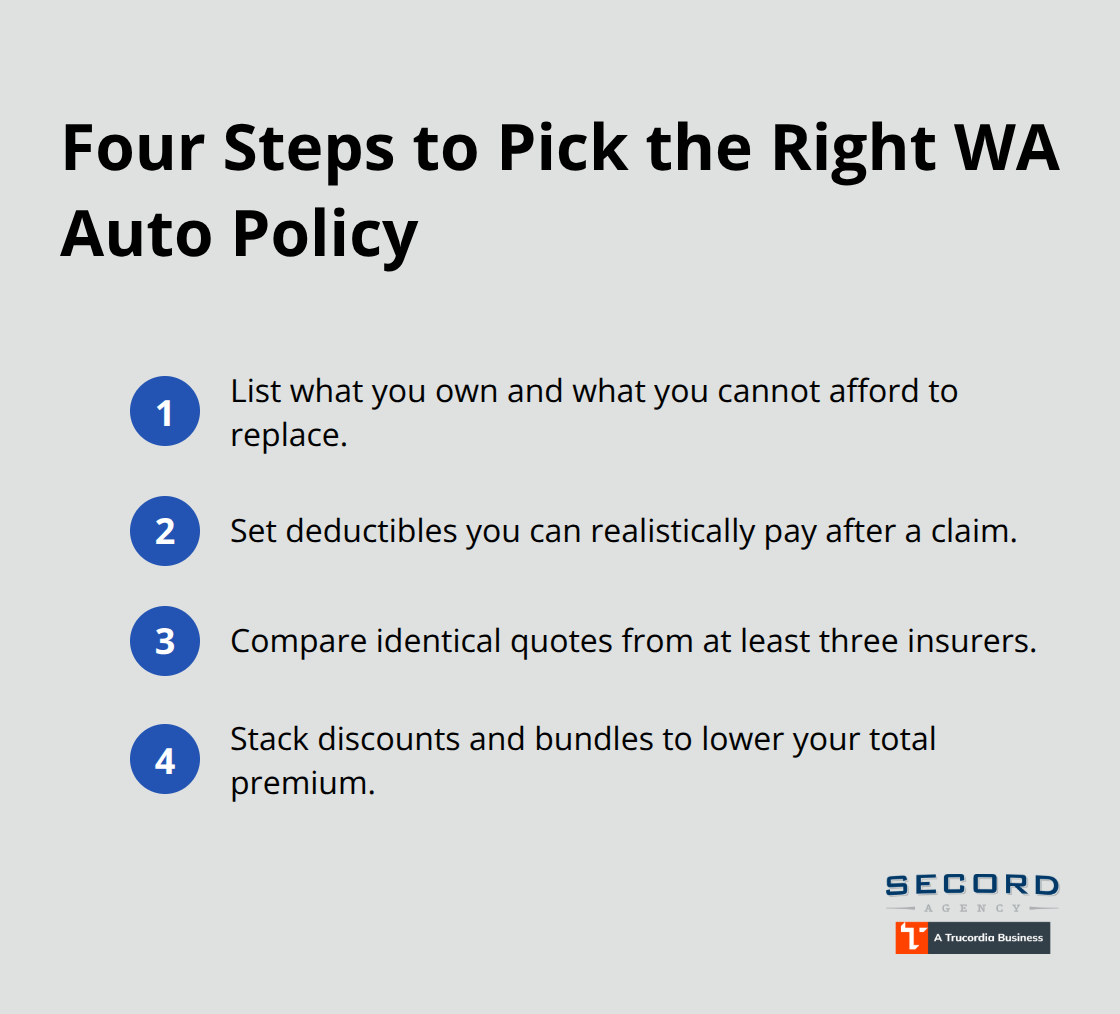

Start by writing down what you actually own and what you’d struggle to replace. If you have a mortgage, your lender requires collision and comprehensive coverage anyway, so that decision is already made. If you own your car outright, the calculation shifts entirely-carrying comprehensive on a 2008 Honda Civic with 180,000 miles makes no financial sense, but comprehensive on a 2023 vehicle worth $35,000 absolutely does.

The deductible you choose matters as much as the coverage itself. A $500 deductible costs more in premiums than a $1,500 deductible, but if you can’t afford to pay $1,500 out of pocket after a claim, the lower deductible protects you from financial strain. Many Washington drivers choose $250 deductibles for comprehensive and $500 for collision, balancing reasonable out-of-pocket costs against premium increases.

Align Coverage with Your Driving Situation

Your driving habits determine what coverage protects you best. If you park on the street in Seattle where theft and vandalism run high, comprehensive becomes genuinely valuable. If you commute on I-5 daily where collision risk spikes, collision coverage with a lower deductible makes sense.

If you have significant assets-a home, savings, retirement accounts-you need higher liability limits because a lawsuit can target those assets. The minimum 25/50/10 won’t defend someone with $200,000 in home equity.

Compare Quotes Across Multiple Carriers

Request identical scenarios across at least three insurers-same vehicle, same coverage limits, same deductibles-so you compare apples to apples rather than guessing. Many Washington drivers skip this step and overpay by hundreds annually. Usage-based insurance programs track your actual driving through a mobile app and reward safe driving with premium reductions of up to 30 percent. These programs work best for drivers under 25 or those returning to driving after incidents because insurers see your behavior directly rather than relying on historical risk factors.

Maximize Discounts and Bundle Savings

Bundling auto insurance with home or renters coverage typically saves 10 to 25 percent, so if you need multiple policies, request bundled quotes. Ask about specific discounts: good student discounts for drivers with 3.0 GPAs or higher, safety feature discounts for vehicles with automatic emergency braking or lane-keeping assist, and low-mileage discounts if you work remotely.

Some carriers offer accident forgiveness after your first incident, which prevents a single claim from permanently raising your rates-this matters far more than you might think. Local insurance agents shop multiple carriers to find coverage that fits your specific situation rather than pushing you toward generic policies that leave gaps or cost more than necessary.

Final Thoughts

Comprehensive auto insurance in Washington requires you to balance state minimums against real-world crash costs, vehicle value, and your personal financial situation. The coverage types we’ve covered-liability, collision, comprehensive, uninsured motorist protection, and gap insurance-form the foundation of adequate protection. Your driving record, vehicle type, location, and mileage determine what you’ll pay, but those factors don’t lock you into any single rate.

Shopping multiple carriers reveals dramatic price differences for identical coverage, often saving hundreds annually. Match your limits to what you actually own and what you’d struggle to replace, then adjust your deductible based on what you can afford out of pocket after a claim. Bundling auto with home or renters coverage typically cuts 10 to 25 percent from your total bill, and discounts for good driving records, safety features, low mileage, and good student grades add up quickly when you ask for them.

We at Secord Agency – A Trucordia Business shop multiple carriers to find coverage that fits your specific situation rather than pushing generic policies that leave gaps or cost more than necessary. Contact us for a personalized quote and let us show you where you’re overpaying and where your protection actually breaks down.