Condo Association Insurance Washington: Coverage for the Building and Residents

Condo association insurance in Washington protects the building itself, but it leaves gaps that individual unit owners need to fill. Most condo owners don’t realize their association’s master policy won’t cover their personal belongings or provide liability protection inside their unit.

At Secord Agency – A Trucordia Business, we help condo owners understand exactly what they’re protected against and where they need additional coverage. This guide breaks down the difference between association policies and individual condo insurance so you can make informed decisions about your investment.

What Your Association’s Master Policy Actually Covers

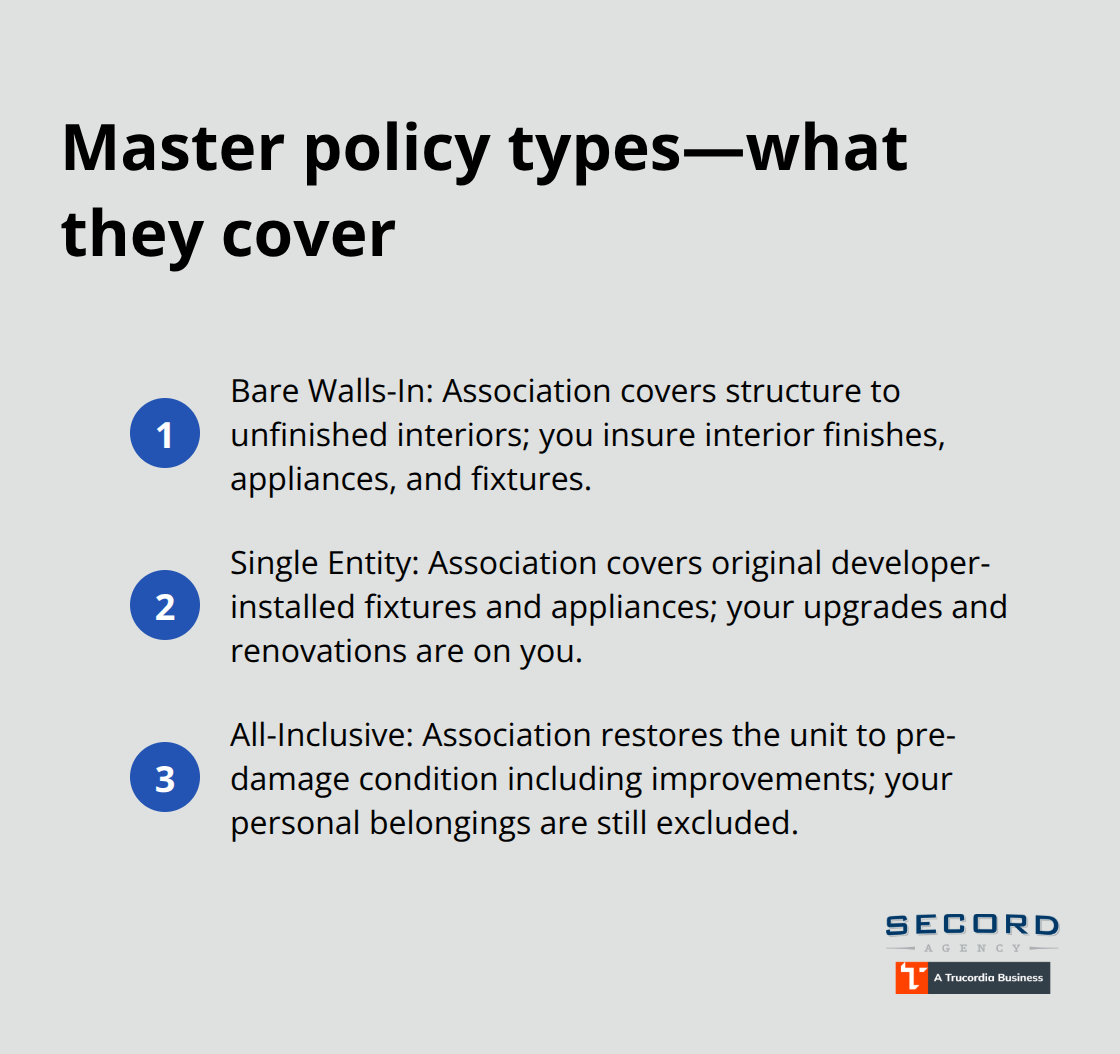

Washington law requires condo associations to maintain property insurance on the building structure and common areas, but the scope depends on which master policy type the association selected. Under RCW 64.34.352, associations must carry property insurance at a minimum of 80% of the actual cash value of the insured property at purchase and at each renewal, excluding land and foundations. The three master policy categories-Bare Walls-In, Single Entity, and All-Inclusive-determine exactly what gets covered inside and outside individual units, and this distinction directly affects what you’ll need to insure separately.

Understanding Your Master Policy Type

A Bare Walls-In policy covers only the building exterior and structural framing up to unfinished interior walls, leaving you responsible for all interior finishes, appliances, and fixtures. A Single Entity policy extends to original appliances and fixtures installed by the developer but excludes any upgrades or renovations you’ve made. An All-Inclusive policy covers everything needed to restore a unit to its pre-damage condition, including improvements you’ve added, though it still won’t touch your personal belongings. You must review your association’s governing documents or ask the property manager for the Certificate of Insurance to confirm which type applies to your building, because this directly determines your individual coverage gaps.

How Association Liability Coverage Works

The association’s master policy includes general liability insurance protecting the association itself from injury claims or property damage occurring in common areas. Washington law typically requires liability coverage in an amount determined by the board but not less than what the declaration specifies, with standard limits around $1 million per occurrence and $2 million aggregate for many communities. This covers slip-and-fall injuries in hallways, lobby accidents, or damage caused by common-area maintenance failures-but it explicitly does not protect you for incidents within your unit or caused by your actions. The policy also names unit owners as insured persons for liability arising from their interest in common elements only, meaning you’re protected if someone is injured due to an association failure, not due to something you did inside your own unit.

Additional Protections the Association Carries

Associations often carry Directors and Officers insurance protecting board members from personal liability for official decisions, and crime or fidelity coverage protecting association funds from theft or embezzlement. These policies strengthen the association’s financial stability and governance, but they provide no direct protection to individual unit owners. If the association’s liability limits prove insufficient after a major loss, that’s where loss assessment coverage enters the picture for individual owners.

Loss Assessment Coverage Fills the Funding Gap

Loss assessment coverage on an individual condo policy protects you from special assessments the association charges when its master policy limits or reserves fall short after a significant loss. Washington condo owners frequently face water-damage claims exceeding $100,000 from burst pipes or roof leaks, and if the master policy deductible or coverage limit doesn’t cover the full cost, the association bills unit owners for the shortfall. A typical loss assessment endorsement on a homeowners policy starts at around $1,000 of coverage, which is inadequate; try for $50,000 or higher, which costs only tens of dollars more annually according to industry analysis. Higher caps like $25,000 to $100,000 exist but often exclude the master policy deductible itself, meaning you could still face out-of-pocket costs even with the endorsement active. The timing of loss assessment coverage matters significantly-the policy must be in force when the loss occurs or when the assessment is actually charged, so gaps between policy renewals can leave you exposed. Review your association’s most recent reserve study and master policy limits with your insurance agent to set an appropriate loss assessment cap that reflects realistic loss scenarios in your building. Understanding these gaps in association coverage is the first step toward identifying what your individual condo policy must address.

Why Condo Owners Need Individual Insurance Beyond the Association’s Policy

The association’s master policy creates a false sense of security for many condo owners in Washington. You might assume that since your association carries insurance on the building, you’re fully protected-but that assumption will cost you thousands of dollars the moment something goes wrong inside your unit. The master policy explicitly excludes your personal belongings, your actions inside the unit, and any liability you create as an individual resident.

What the Association Policy Does Not Cover

A burst pipe in your bathroom floods your hardwood floors and custom kitchen cabinets. The association’s policy covers structural repair to the framing and drywall, but your personal property and improvements remain your responsibility. A guest trips on your throw rug and suffers a serious injury. The association’s liability coverage won’t touch it because the incident occurred within your unit and resulted from your negligence, not a common-area failure. Water damage claims alone average well over $100,000 in Washington condos, yet most owners discover too late that they’re on the hook for the full amount if their personal policy doesn’t cover it.

Personal Property Protection You Must Carry

Your individual HO-6 condo policy fills these gaps by covering the interior structure of your unit (walls, floors, ceilings, built-in appliances) for named perils like burst pipes, storms, fire, and smoke. The policy also protects your personal property inside the unit against damage, loss, or theft. Without this coverage, you absorb the financial impact of losses that the association’s policy simply does not address.

Liability Coverage for Your Unit and Actions

Personal liability coverage protects you if someone is injured in your unit and sues you for medical bills or property damage-a claim the association’s policy explicitly excludes. Loss assessment coverage shields you from special assessments when the association’s reserves or deductible fall short after a major loss. Most owners carry the minimum $1,000 loss assessment endorsement, which is dangerously inadequate given that a single significant water event can trigger assessments of $10,000 to $50,000 per unit. Try for at least $50,000 in loss assessment coverage, which typically costs only $30 to $50 more per year than the base endorsement.

Additional Protections and Strategic Deductible Coordination

Additional living expenses coverage reimburses hotel stays and meals if your unit becomes uninhabitable due to a covered loss. For high-value items like jewelry or heirlooms, you can add specific endorsements for replacement-cost coverage rather than settling for depreciated actual cash value. The master policy deductible (often $1,000 to $5,000) applies to you as well, so coordinate with your agent to confirm whether your HO-6 should match that deductible or offset it strategically. Understanding these gaps in association coverage and the specific protections your HO-6 must provide sets the foundation for choosing the right policy that actually matches your building’s master policy type and your personal needs.

Choosing the Right HO-6 Policy for Your Washington Condo

Obtain Your Association’s Certificate of Insurance

Contact your property manager or board president to request a copy of your association’s Certificate of Insurance. This document shows the exact master policy type, coverage limits, deductible amount, and what the association actually insures. Many condo owners skip this step and end up purchasing policies that duplicate coverage they already have or miss critical gaps entirely. The Certificate tells you whether your building uses a Bare Walls-In, Single Entity, or All-Inclusive master policy, which fundamentally changes what your HO-6 must cover.

Match Your HO-6 Coverage to Your Master Policy Type

If your association has a Bare Walls-In policy with a $2,500 deductible, your individual HO-6 needs to start covering interior finishes at that deductible threshold. If you’re in an All-Inclusive building, you can reduce your dwelling coverage on the HO-6 since the association handles most structural restoration. The master policy deductible applies to you directly, so coordinate this with your agent rather than purchasing duplicate coverage. Review your association’s reserve study as well, which identifies major components and their remaining useful life. A reserve study showing aging plumbing systems or a roof nearing end-of-life signals higher probability of water damage claims, which should influence your loss assessment coverage selection upward toward $50,000 or more rather than settling for the inadequate $1,000 base.

Compare Quotes Across Multiple Carriers

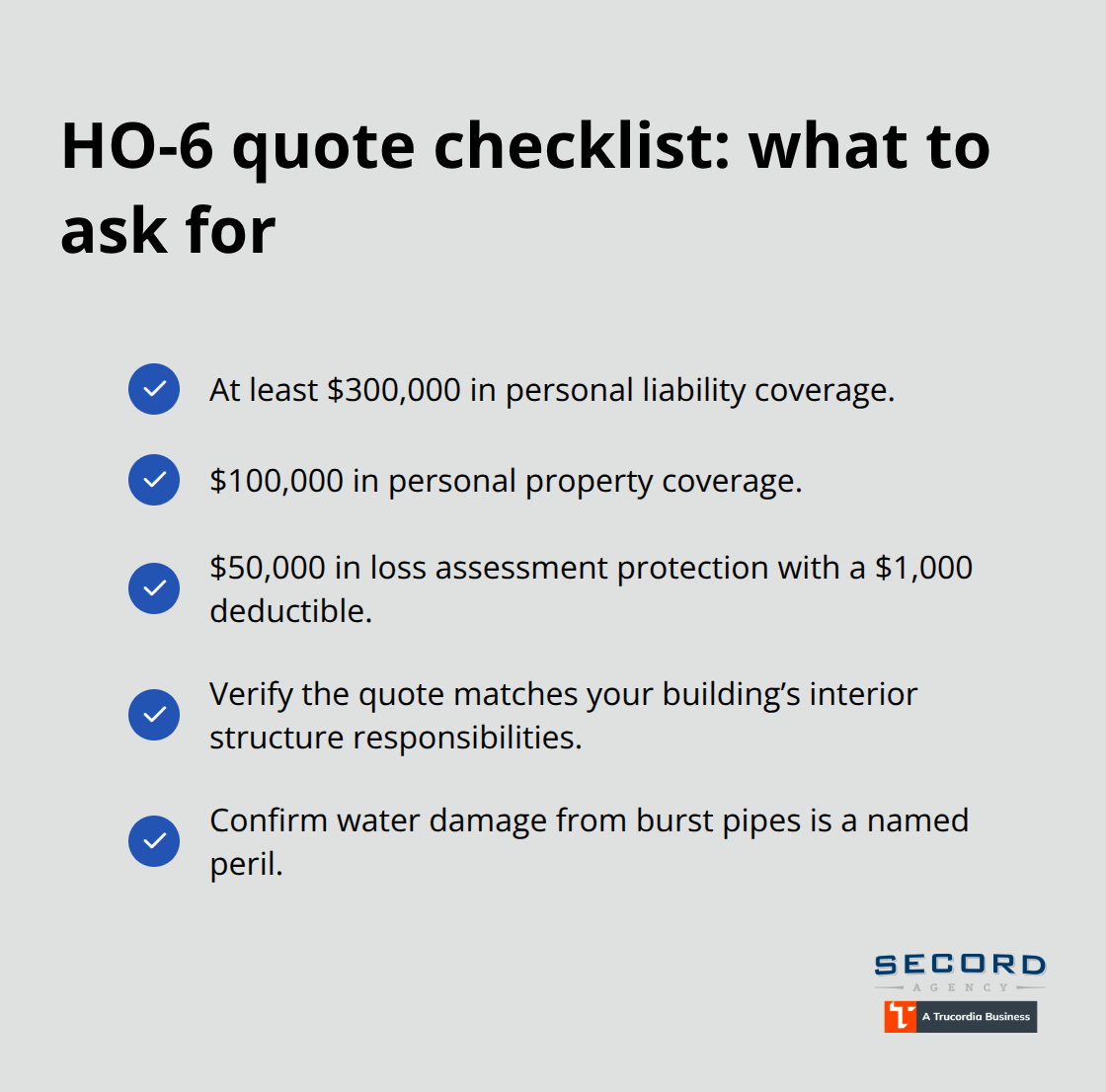

When comparing HO-6 quotes from different carriers, focus on specific numbers rather than price alone. Request quotes that include at least $300,000 in personal liability, $100,000 in personal property coverage, and $50,000 in loss assessment protection with a $1,000 deductible. Verify that the quote covers the interior structure type your building uses and that water damage from burst pipes is included as a named peril.

Evaluate Coverage Details and Replacement Cost

Ask each agent whether the policy provides replacement-cost coverage for personal property or merely actual cash value, which depreciates items significantly. Many agents offer bundling discounts if you combine your condo policy with auto or renters insurance, which can reduce your total premium by 10% to 25%. Try for at least three carrier quotes to compare, since rates and coverage details vary substantially. A licensed agent familiar with Washington condo associations will identify coverage gaps you might miss on your own and explain how your HO-6 coordinates with the master policy deductible, preventing costly surprises after a loss.

Final Thoughts

The gap between what your condo association insures and what you actually need to protect remains substantial. Your association’s master policy covers the building structure and common areas, but it stops at your unit’s interior walls and provides zero protection for your personal belongings or liability you create inside your home. Condo association insurance in Washington operates under state law that separates responsibility between the association and individual owners, and understanding this division prevents the costly mistake of assuming you’re covered when you’re not.

Your individual HO-6 policy must fill whatever gaps your master policy leaves behind, whether that’s interior finishes, personal property, or personal liability protection. A Bare Walls-In policy leaves you responsible for nearly everything inside your unit, while a Single Entity policy covers original fixtures but not your upgrades, and an All-Inclusive policy handles most interior restoration but still excludes your personal property and personal liability. Regardless of which type your building uses, you need personal property coverage, liability protection, and loss assessment coverage (ideally $50,000 or higher) to avoid financial devastation after a water event, fire, or injury claim.

We at Secord Agency – A Trucordia Business specialize in helping Washington condo owners navigate these coverage complexities and shop multiple carriers to find rates and coverage that match your specific building’s master policy. Contact us for a quote and let us simplify your condo insurance so you understand exactly what protects your investment.