Auto Insurance Discounts Seattle: Smart Ways to Cut Premiums

Seattle drivers are paying more for auto insurance than they need to. Most people leave hundreds of dollars in savings on the table every year simply because they don’t know what discounts exist.

At Secord Agency – A Trucordia Business, we help local drivers find auto insurance discounts in Seattle that actually stick. The right combination of discounts can cut your premiums significantly, and we’ll show you exactly how.

What Discounts Can Actually Lower Your Seattle Auto Insurance Bill

Safe Driver Discounts Reward Your Clean Record

A clean driving record is worth real money in Seattle. Safe driver discounts typically range from 5% to 15% depending on your insurer, and they reward three to five years without accidents or violations. This matters because driving history carries the most weight in how insurers price your policy. If you’ve maintained a clean record, you’re sitting on savings you may not be using yet.

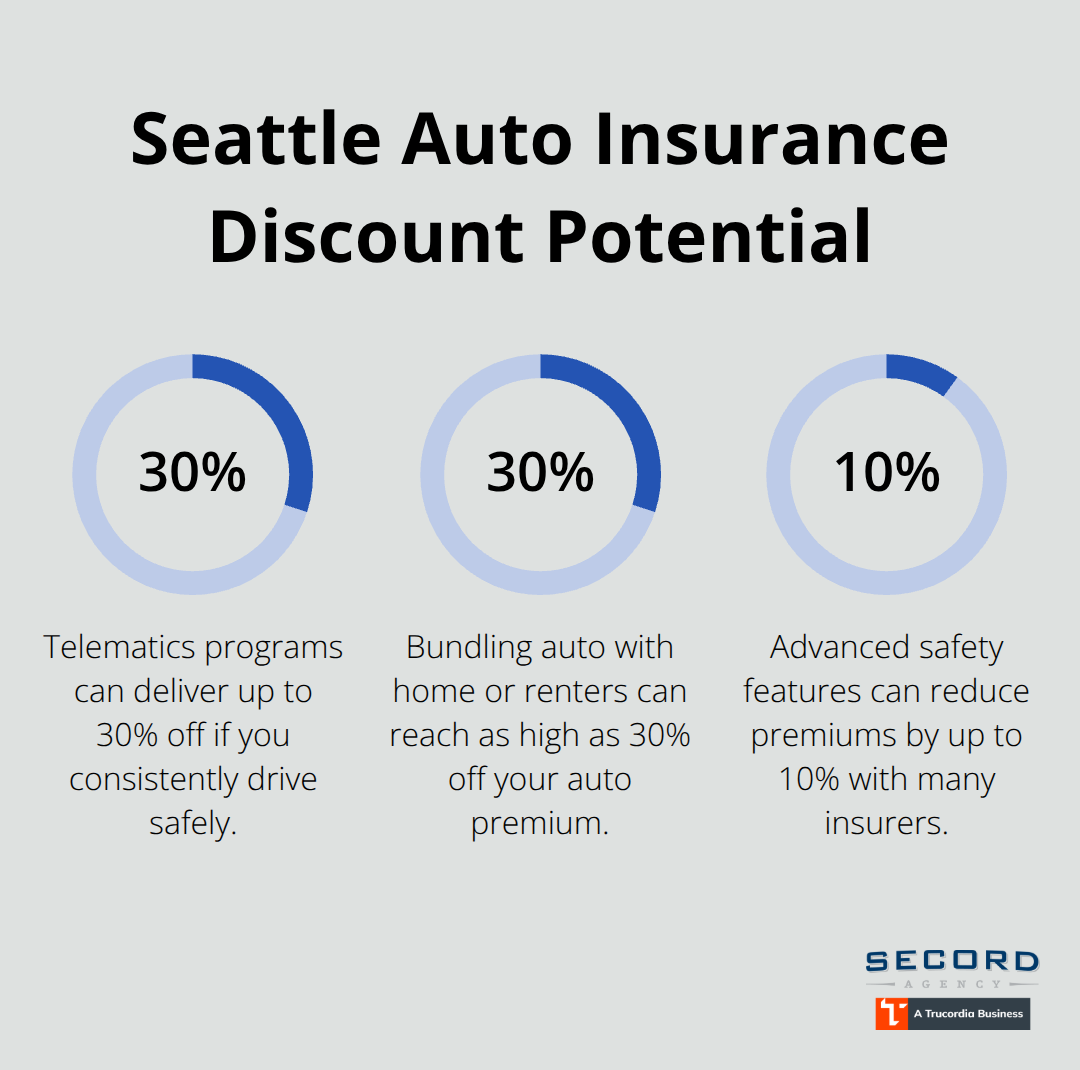

Some carriers sweeten this further with telematics programs that monitor your actual driving behavior-speed, braking patterns, and time of day you drive. These programs can yield discounts up to 30% if you consistently drive safely, though Consumer Reports data shows a more typical median savings around $120 per year. Ask your carrier explicitly whether they offer monitoring programs and what data they collect before you enroll.

Not all safe drivers benefit equally from telematics; if you drive erratically even occasionally, the discount might shrink or disappear entirely.

Multi-Policy Bundling Delivers Immediate Savings

Multi-policy bundling delivers the most immediate savings for most Seattle drivers. Combining auto insurance with homeowners or renters coverage through the same carrier typically cuts 10% to 25% off your auto premium, and some carriers offer bundled discounts as high as 30%. The math is straightforward: a driver paying $2,877 annually for full coverage in Seattle could save roughly $288 to $719 through bundling with a home policy.

However, bundling isn’t automatically the best choice for every household. You need to compare the bundled rate against standalone quotes from other carriers; sometimes a cheaper auto insurer plus a separate home policy costs less overall than bundling with an expensive carrier. This is why shopping multiple carriers matters before you commit to any bundle.

Safety Features Unlock Additional Discounts

Safety features and vehicle technology represent another layer of savings that many drivers overlook. Anti-lock brakes, automatic emergency braking, blind-spot monitoring, and stability control typically unlock discounts of 3% to 10% depending on the insurer. Modern vehicles with these systems installed factory-standard often qualify automatically, but older cars may not.

Ask your carrier specifically which safety features on your vehicle qualify for discounts and whether upgrading to a vehicle with advanced safety systems would lower your rate enough to offset the purchase price over several years. The combination of these three discount categories-safe driving, bundling, and safety features-creates a foundation for meaningful savings that compounds when you apply them together.

How to Actually Compare Rates and Find Hidden Savings

Shop Multiple Carriers to Expose Price Gaps

Shopping multiple carriers is non-negotiable if you want the lowest rate. NerdWallet’s January 2026 analysis shows that for an identical driver profile in Seattle, Direct General quoted around $46.02 per month while State Farm quoted $101.80 per month for the same coverage-a difference of over $660 annually. This isn’t an outlier. Insurers weight driving history, location, age, and credit differently, which means your cheapest option depends on your specific profile, not on brand reputation.

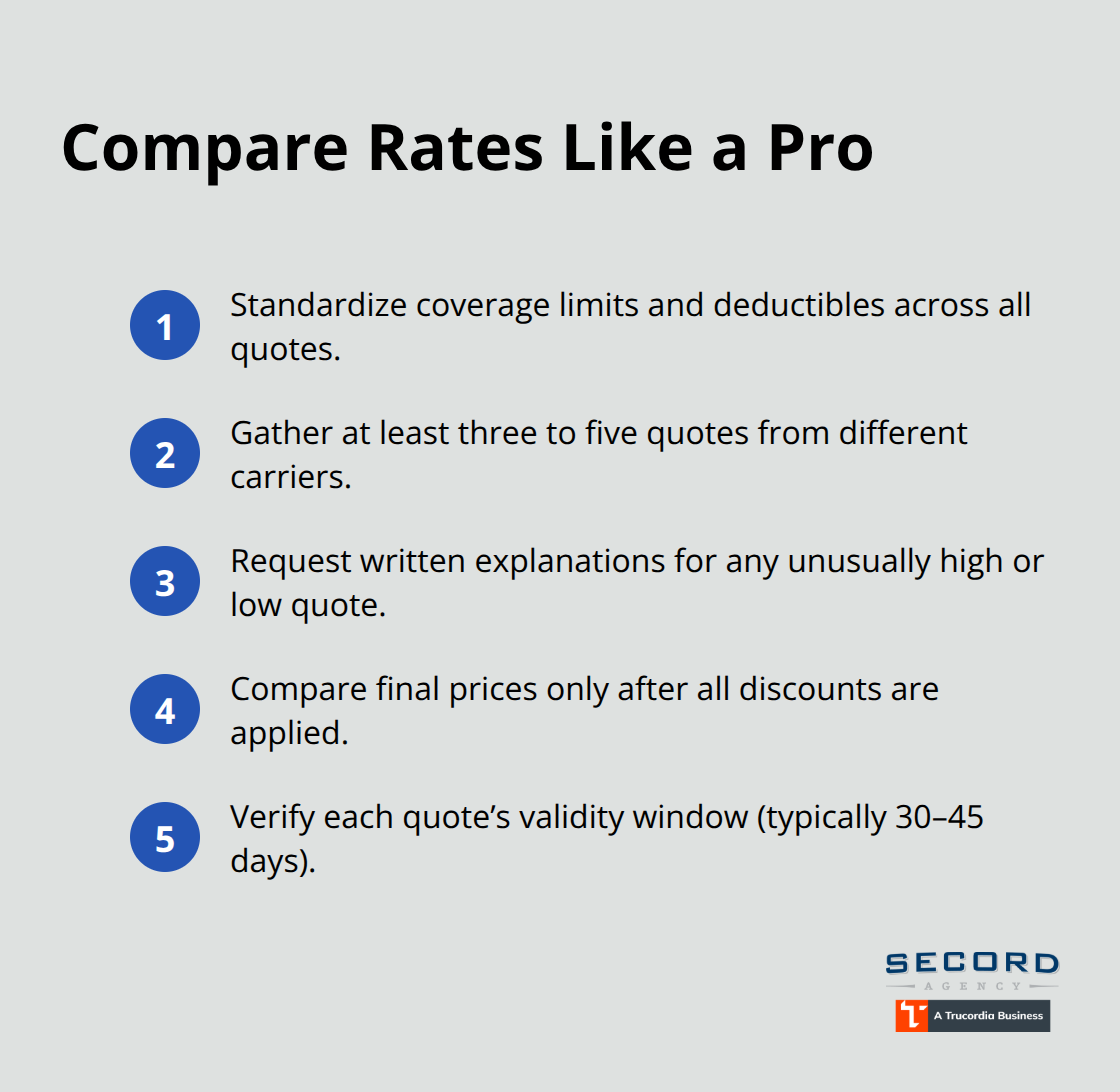

When you get quotes, standardize your coverage limits and deductibles across all carriers so you’re comparing apples to apples. Request written explanations for any quote that seems unusually high or low; sometimes a carrier has flagged something in your record that you can address, or they’ve simply underestimated your risk category.

Consumer Reports data shows that about 30% of policyholders switched insurers in the past five years and saved a median of $461 annually, which tells you that most people are overpaying simply because they haven’t shopped in years. Get quotes from at least three to five carriers every time you review your policy. Most insurers provide estimates within minutes online, and quotes typically remain valid for 30 to 45 days, giving you a window to decide.

Review Your Policy Annually When Life Changes

Your policy isn’t static, and neither should your shopping habits. An annual rate review is essential because your circumstances change-you might move to a safer neighborhood, start working from home, get married, or pay off your car. Each of these events unlocks new discounts or eliminates the need for certain coverages. Washington auto insurance premiums rose about 17.5% year-over-year as of December 2024 according to the Washington Office of the Insurance Commissioner, which means carriers adjust their pricing regularly.

If your premium jumps more than 15% to 20% year-over-year, that’s a signal to shop immediately. Large increases often signal that you’re no longer getting competitive pricing, and a quick comparison with other carriers can reveal substantial savings. Don’t wait for renewal notices to prompt action; set a calendar reminder to shop every 12 months regardless of whether your rate increased.

Evaluate Usage-Based Insurance Programs Carefully

Usage-based insurance programs deserve serious consideration if you drive safely and consistently. These telematics programs track your actual driving through a mobile app or device, and Consumer Reports found that enrolling can yield a median savings around $120 per year. Some programs offer substantially higher savings-up to about $931 in certain cases-if your driving patterns are genuinely safe.

Before enrolling, understand exactly what data the carrier collects, how long they store it, and whether they share it with third parties. Ask your current insurer if they offer a usage-based option and how it compares financially to your clean-record discount alone. The privacy trade-off matters; some drivers accept data monitoring for savings, while others prefer traditional discounts that don’t require tracking.

Work with an Independent Agent to Uncover Hidden Discounts

An independent agent shops carriers on your behalf, compares multiple quotes simultaneously, and identifies which discounts you actually qualify for without you spending hours on the phone. This approach often uncovers rate improvements that online quote tools miss because agents have access to carrier-specific programs and can negotiate based on your complete profile. Agents at Secord Agency, based in Seattle’s Wallingford neighborhood, pair competitive rates with fast, local service and provide personalized advice to help you navigate coverage options and ongoing policy reviews.

The combination of multiple quotes, annual reviews, and usage-based programs creates a comprehensive strategy for finding and maintaining the lowest possible rate. Your next step involves taking action on these strategies-starting with gathering quotes and identifying which discounts apply to your specific situation.

Why Local Agents Beat Online Quotes

Independent Agents Shop Multiple Carriers at Once

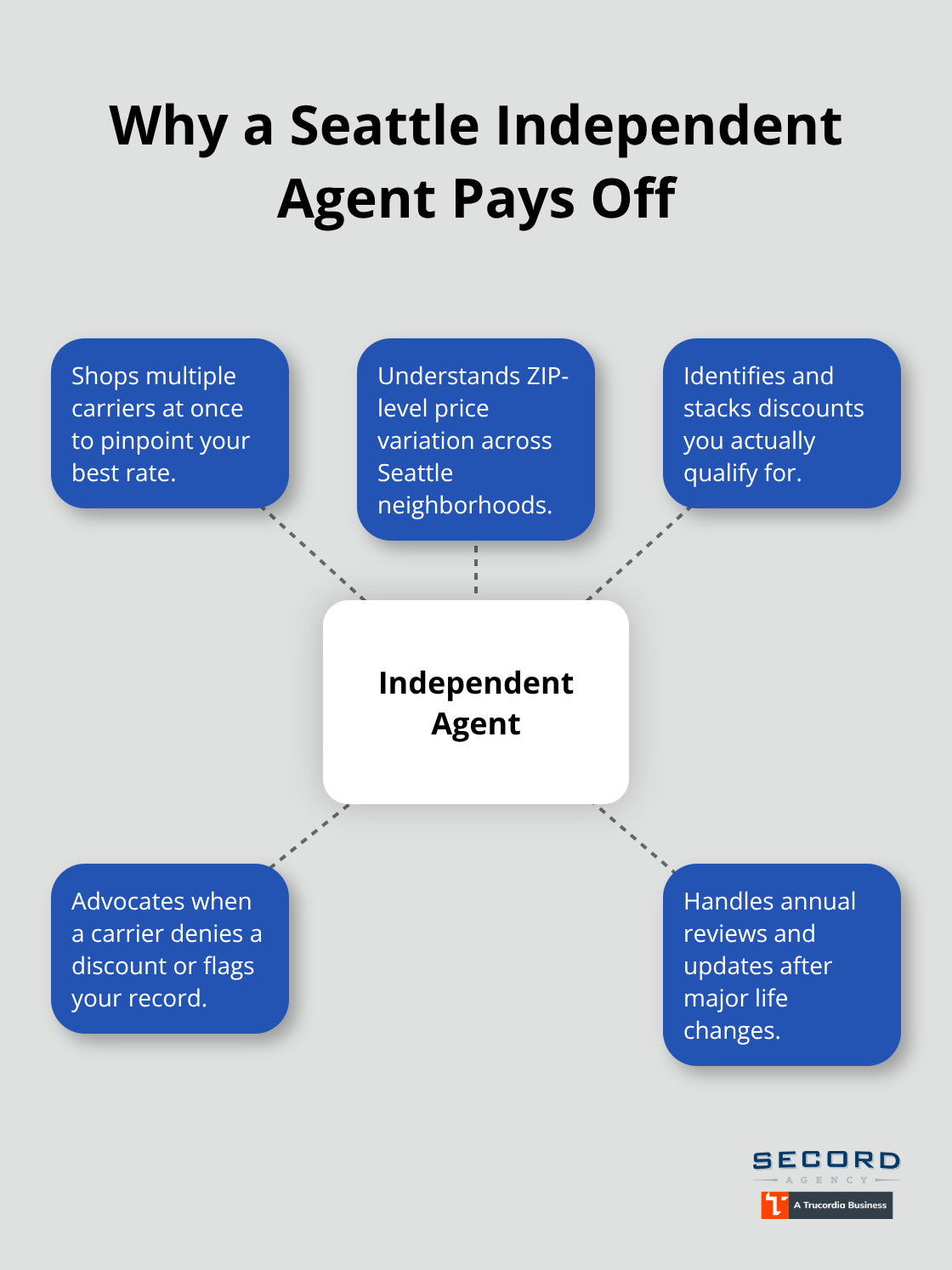

An independent agent eliminates the friction that costs you money. When you shop online, you enter your information into one carrier’s system at a time, wait for a quote, then repeat the process with another insurer. This approach takes hours and leaves gaps because you’re unlikely to identify every discount you qualify for. A local agent uses a comparative rater to shop multiple carriers simultaneously on your behalf, compares their exact pricing for your profile, and identifies discounts you’d miss on your own. This matters because insurers don’t volunteer all their discounts, and reps handling online quotes have no incentive to surface savings that reduce what you pay.

A Consumer Reports analysis found that about 30% of policyholders switched insurers in the past five years and saved a median of $461 annually, yet most people never switch because the comparison process feels overwhelming. An agent removes that friction entirely. They know which carriers weight your specific factors-your age, driving history, location within Seattle, vehicle type, and credit score-most favorably and can predict which company will offer the best rate before you fill out a form.

Local Knowledge Reveals Hidden Rate Variations

Seattle’s insurance market varies dramatically by ZIP code. NerdWallet’s data shows that ZIP 98110 averages roughly $65.42 per month for identical driver profiles while ZIP 98101 averages $143.81 per month, a gap of over $900 annually. An agent familiar with Seattle’s neighborhoods understands these variations and can advise whether your current ZIP code’s higher costs warrant more aggressive shopping or whether moving to a safer area would lower your rate enough to justify the move.

Washington auto insurance premiums rose about 17.5% year-over-year as of December 2024 according to the Washington Office of the Insurance Commissioner, partly because weather-related claims and modern vehicle repair costs keep climbing. An agent tracks these trends and alerts you when they affect your specific rate, then repositions your coverage before your renewal hits.

Agents Advocate for Coverage That Protects Your Assets

An agent understands Washington state’s minimum liability requirements of 25/50/10 and can advise whether higher limits like 50/100/250 make sense for your asset protection, something online quote tools rarely address. When a carrier denies a discount or flags something in your record, an agent advocates on your behalf to clarify the issue or find alternative coverage that costs less. This advocacy prevents costly mistakes that online shoppers often make when they accept the first quote without understanding the full picture.

Ongoing Reviews Keep Your Policy Competitive

An agent handles the administrative work of annual reviews without requiring you to remember to shop every 12 months. When life changes occur-you marry, move, pay off your car, or start working from home-an agent proactively identifies which new discounts apply and adjusts your policy accordingly. This ongoing advocacy prevents you from overpaying during transitions when your coverage needs shift but your policy doesn’t.

Final Thoughts

Seattle drivers waste hundreds of dollars annually by ignoring auto insurance discounts or failing to shop competitively. The strategies outlined here work because they address the core problem: most people accept their current rate without understanding what they’re actually paying for or whether better options exist. Start by gathering quotes from at least three to five carriers using your exact address and standardized coverage limits, then identify every discount you qualify for-safe driver, bundling, safety features, low mileage, good student status, or usage-based programs.

Commit to an annual review and set a calendar reminder for your policy renewal date to shop again, even if your current rate seems reasonable. Washington premiums rose 17.5% year-over-year as of December 2024, and carriers adjust pricing constantly. Life changes matter too-marriage, moving within Seattle, starting remote work, or paying off your vehicle all unlock new discounts or eliminate unnecessary coverages.

The real advantage comes from working with someone who handles this complexity on your behalf. An independent agent shops multiple carriers simultaneously, identifies discounts you’d miss alone, and advocates when carriers deny coverage or flag issues in your record. Contact us for a comprehensive policy review, and we’ll compare your current coverage against multiple carriers to show you exactly how much you could save on auto insurance discounts in Seattle.