Seattle Car Insurance Rates: Finding the Best Value

Seattle car insurance rates vary significantly based on where you live, how you drive, and what coverage you choose. We at Secord Agency – A Trucordia Business know that finding affordable coverage in this market requires understanding what actually affects your premiums.

This guide walks you through the factors that shape your rates, how to compare quotes effectively, and concrete ways to cut your costs without sacrificing protection.

What Actually Drives Your Seattle Car Insurance Costs

Seattle’s car insurance premiums reflect three hard realities that most drivers overlook. Your location, the weather patterns that shape claim costs, and your coverage choices all stack together to determine what you pay each month.

Location Creates Massive Price Gaps

Your ZIP code determines far more of your premium than you might expect. Seattle neighborhoods have vastly different accident frequencies and risk profiles. A driver in ZIP code 98118 pays an average of $3,165 annually, while someone in 98115 pays $2,776 for the same coverage according to data analyzed by NerdWallet. That $389 difference stems entirely from where you park your car.

Accident rates spike in congested urban corridors. Theft varies by neighborhood. Road conditions deteriorate faster in some areas than others. Insurers plug your specific ZIP code into every rate calculation and use years of claims data to price risk block by block. This is why quotes for your exact address matter-a quote from a neighboring ZIP code won’t reflect what you’ll actually pay.

Weather and Climate Push Repair Costs Higher

Washington state’s weather patterns have driven car insurance costs up sharply. Auto insurance rates across Washington increased 17.5% year over year as of December 2024, according to the Washington Office of the Insurance Commissioner. That acceleration stems directly from rising repair bills.

Modern vehicles require expensive repairs for minor damage because they pack safety sensors and electronic systems throughout their frames. Rain, hail, and winter conditions don’t just increase accident frequency-they drive up the cost per claim. Wildfires have also shifted how insurers view risk in parts of Washington, affecting underwriting decisions and availability. Expect your rates to reflect these climate realities.

Coverage Requirements Shape Your Financial Exposure

Washington mandates minimum liability coverage of 25/50/10 (meaning $25,000 per person and $50,000 per accident for bodily injury, plus $10,000 for property damage). That bare minimum satisfies the law but leaves you financially exposed. A serious accident with multiple injuries can easily exceed those limits, putting your personal assets at risk.

Full-coverage policies that include collision and comprehensive protection average around $2,154 annually in Seattle, roughly 12% higher than the state average of $1,919. The gap between meeting state minimums and carrying adequate protection is substantial. Your deductible choice also matters enormously-raising it from $500 to $1,000 can lower your premium meaningfully, but you need cash reserves to cover that deductible if you file a claim.

Understanding these requirements helps you make conscious choices rather than defaulting to either bare-bones coverage or over-insuring. Once you grasp how location, weather, and coverage interact, you’re ready to compare quotes across multiple carriers and identify which insurers offer the best value for your specific situation.

Comparing Quotes Across Seattle Carriers

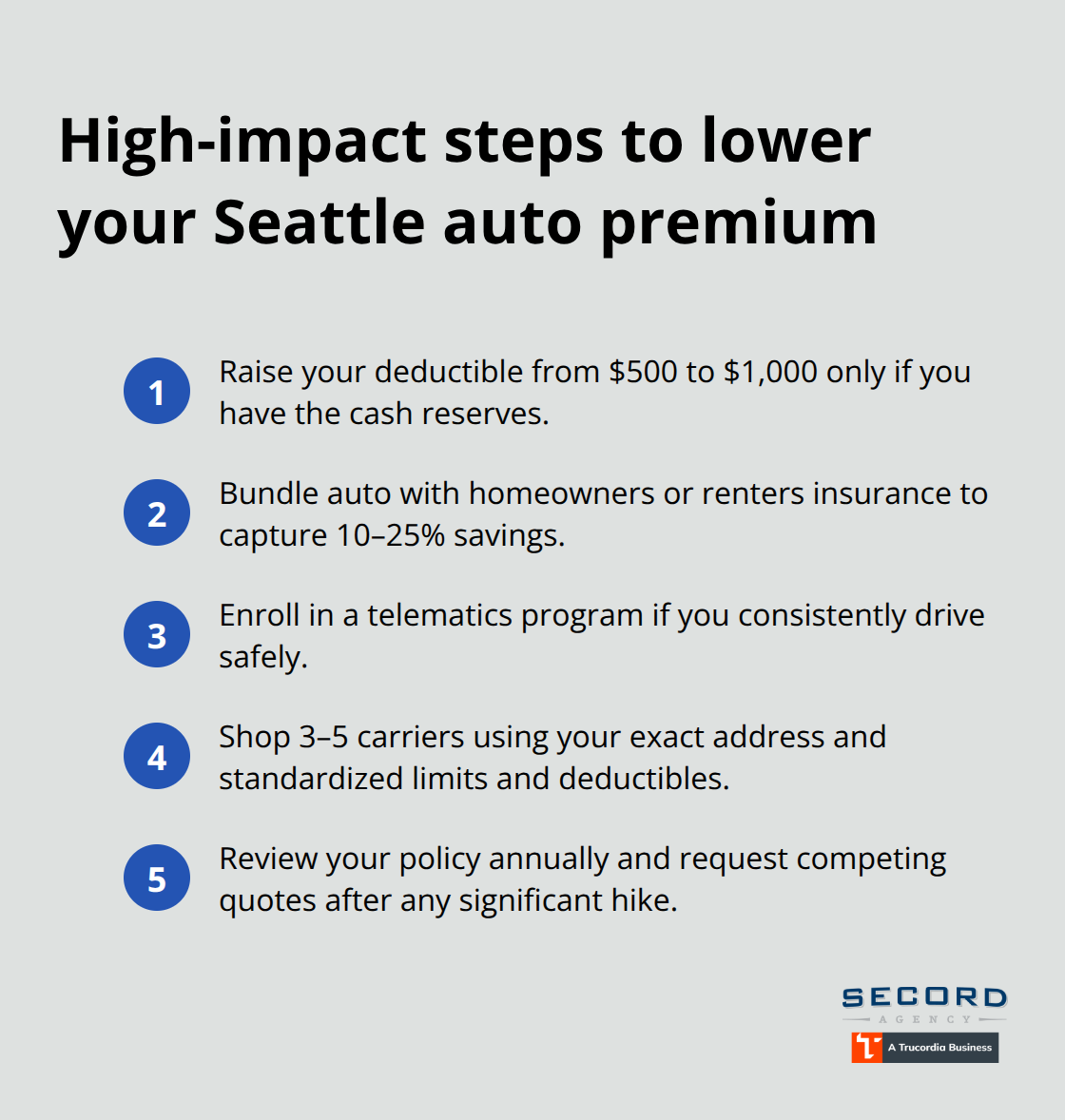

Request quotes from at least three to five carriers using your exact address, vehicle details, and driving history. Your ZIP code affects pricing significantly, so generic quotes won’t work-insurers need your specific address to calculate your actual rate. Most drivers accept the first quote they receive, which costs them real money. That price variation represents thousands of dollars over a few years if you don’t shop around.

Many carriers offer online quote tools that take ten minutes to complete. Write down the coverage limits each quote includes, since comparing $1,500 premiums with different deductibles or liability limits is meaningless. A quote with a $1,000 deductible and $100,000 bodily injury coverage isn’t comparable to one with a $500 deductible and $25,000 limits, even if they come from the same company. Standardize your coverage across all quotes so you actually compare apples to apples.

What Each Coverage Type Actually Protects

Liability coverage pays for damage you cause to other people and their property-it’s mandatory in Washington and non-negotiable. Collision coverage pays to repair your own vehicle after an accident with another car or object, regardless of fault. Comprehensive coverage handles theft, weather, vandalism, and animal strikes. Uninsured motorist protection covers you if you’re hit by someone without insurance.

Most Seattle drivers need all four, but the coverage limits matter enormously. Washington’s minimum 25/50/10 liability leaves you exposed; serious accidents regularly exceed those limits and put your personal assets at risk. Raising limits to $100,000 per person and $300,000 per accident costs far less than you’d expect and protects your financial future.

Deductibles work backwards from how people think: a $1,000 deductible means you pay $1,000 out of pocket when you file a claim, while the insurer pays the rest. Raising your deductible from $500 to $1,000 typically lowers your premium by 15–25%, but only choose this if you have cash reserves to cover it.

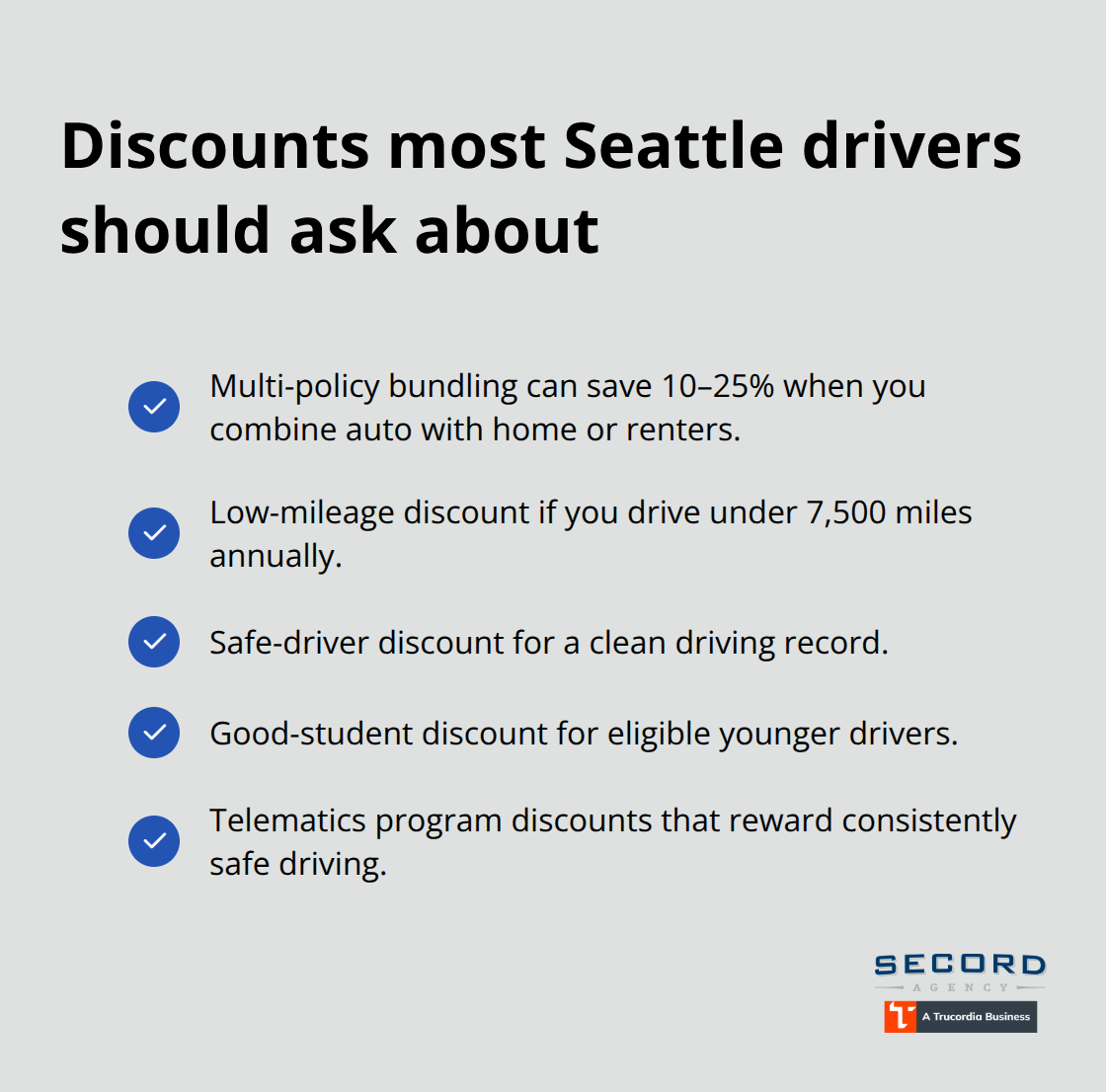

Spotting Discounts That Lower Your Rate

Insurers hide discounts throughout their pricing structures, and most Seattle drivers never ask about them. Multi-policy bundling-combining auto with homeowners or renters insurance-typically saves 10–25% on your auto rate. Low-mileage discounts apply if you drive under 7,500 miles annually; many Seattle residents qualify if they use public transit or work from home. Safe-driver discounts reward clean records, while good-student discounts help younger drivers. Some insurers offer telematics programs that track your driving habits and reward safe behavior with rate reductions.

Ask each carrier specifically what discounts you qualify for before accepting a quote, since representatives don’t always volunteer this information. Price variation between carriers shows how dramatically insurers price risk differently based on their underwriting models and loss history.

Understanding Rate Differences Between Carriers

Request written explanations for rate differences between quotes, especially if one carrier is significantly higher. Each insurer weights factors like your age, location, and driving history differently, which explains why one company charges substantially more than another for your exact profile.

Don’t automatically choose the cheapest quote if the insurer has poor customer service ratings-claims handling matters when you actually need your insurance. An independent agency can shop multiple carriers on your behalf and explain the differences between quotes, saving you time and helping you avoid costly mistakes.

Once you’ve identified which carriers offer competitive rates for your specific situation, the next step involves taking concrete action to lower your costs even further through strategic coverage adjustments and policy reviews.

Cut Your Seattle Car Insurance Costs Without Losing Protection

Raise Your Deductible to Lower Monthly Premiums

Increasing your deductible from $500 to $1,000 typically cuts your premium by 15–25%. The math works in your favor if you have $1,000 in cash reserves set aside specifically for this purpose. If your premium drops $30 per month by raising your deductible, you break even on that extra $500 out-of-pocket exposure after 17 months. This strategy only makes sense if you can actually afford to pay that deductible without financial strain when you file a claim.

Most drivers accept their initial quote without questioning whether a higher deductible fits their financial situation. Calculate your break-even point before you commit to this change, and verify that your emergency fund can absorb the larger deductible without creating hardship.

Stack Discounts to Multiply Your Savings

Multi-policy bundling delivers substantial savings at most carriers. Combining auto with homeowners or renters insurance cuts your auto rate by 10–25%. Low-mileage discounts apply if you drive under 7,500 miles annually, which qualifies many Seattle residents who rely on public transit or work remotely. Telematics programs that track your actual driving habits can lower your rate by 10–30% if you consistently drive safely.

Safe-driver discounts reward clean records, and good-student discounts help younger drivers. The critical step is calling your current insurer and asking them to list every discount you qualify for before you accept any quote. Most representatives don’t volunteer this information unless you ask directly. These discounts compound, so qualifying for three or four of them can produce meaningful monthly savings.

Shop Your Rate Annually to Catch Price Increases

Reviewing your policy annually matters far more than most drivers realize because rate changes compound quickly. If you haven’t shopped your rate in the past 12 months, you’re likely overpaying.

A rate hike of 15–20% often signals you should request quotes from competing carriers immediately. Three to five years after a violation like a speeding ticket or at-fault accident, your rate impact drops substantially as that incident ages off your record.

Get Professional Help Comparing Multiple Carriers

An independent agency can shop multiple carriers on your behalf and identify rate improvements you’d miss shopping alone. They handle the comparison work and explain coverage differences clearly, which saves time and prevents costly mistakes when selecting between carriers with significantly different pricing models. This approach works especially well if your driving history includes violations or accidents that complicate rate shopping.

Final Thoughts

Seattle car insurance rates reflect real costs driven by location, weather, and coverage choices. The gap between the cheapest and most expensive quotes for identical coverage often exceeds $1,000 annually, which means your shopping decisions directly impact your wallet. Understanding how ZIP codes, repair costs, and claim frequency shape your premium puts you in control rather than leaving you at the mercy of whatever rate a single insurer quotes.

The strategies that actually work require three concrete actions. Request quotes from multiple carriers using your exact address and driving history, then standardize the coverage across all quotes so you compare identical protection levels. Identify every discount you qualify for-bundling, low-mileage, safe-driver, and telematics programs compound to produce meaningful savings that most drivers never claim, and review your policy annually to shop competing rates whenever you see a significant increase.

We at Secord Agency – A Trucordia Business work with Seattle drivers daily to navigate this exact process. Our team shops multiple carriers to find competitive rates tailored to your specific situation, then pairs those rates with fast, local service and ongoing policy reviews to keep your coverage aligned with your actual needs. Getting a personalized quote takes minutes and costs nothing-reach out to Secord Agency today to see what your Seattle car insurance rates actually cost across multiple insurers.